Reports

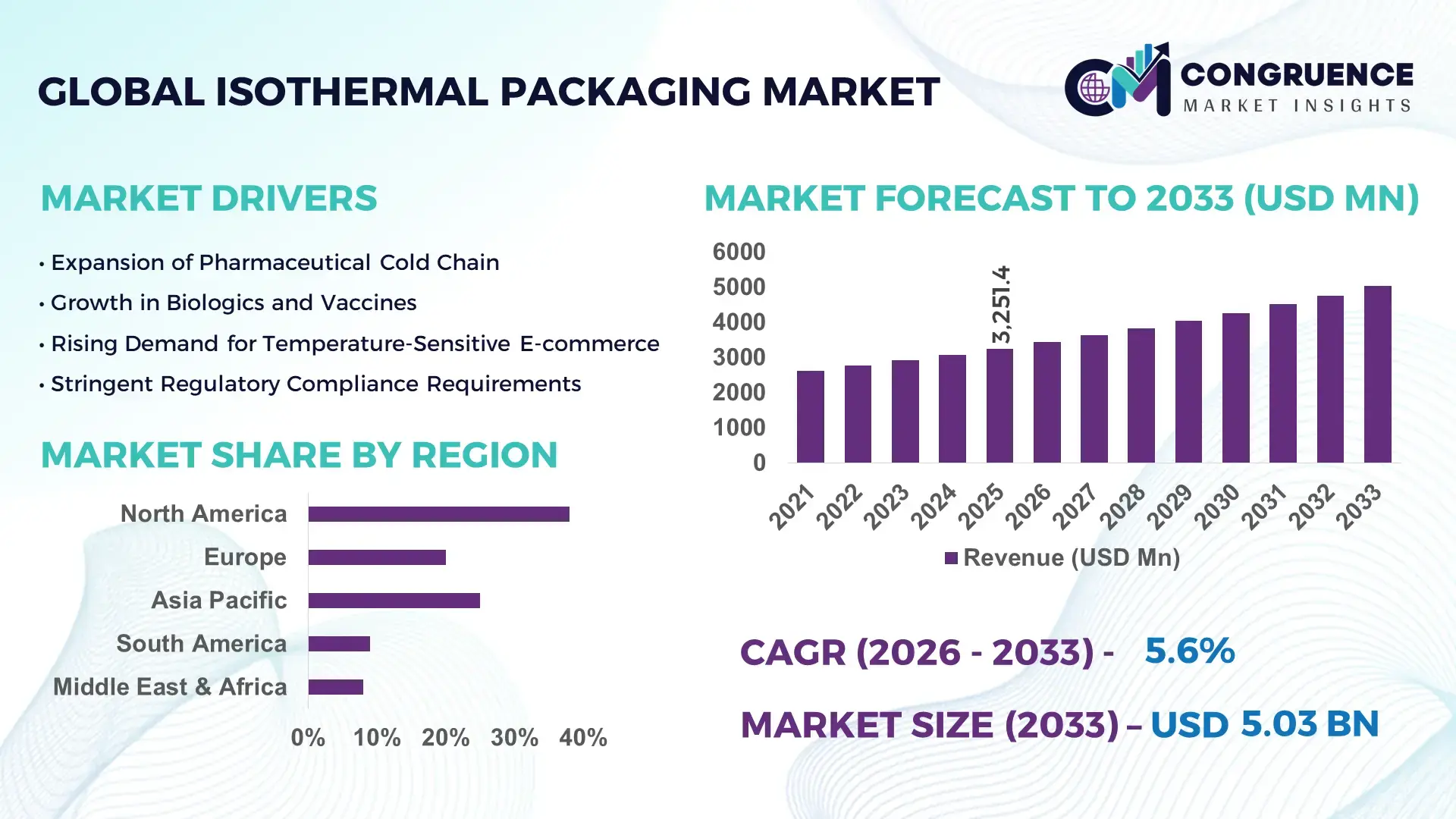

The Global Isothermal Packaging Market was valued at USD 3251.42 Million in 2025 and is anticipated to reach a value of USD 5027.88 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. Growth is primarily supported by rising demand for temperature-sensitive pharmaceutical logistics and expanding global biologics distribution networks.

The United States represents the dominant production and innovation hub within the Isothermal Packaging market, supported by advanced cold chain infrastructure and large-scale pharmaceutical exports. The country operates more than 250 FDA-registered biologics manufacturing facilities, driving high-volume demand for validated thermal packaging systems. U.S.-based manufacturers have invested over USD 600 million in advanced phase change material (PCM) technologies and vacuum insulated panel (VIP) production lines since 2022. Over 60% of temperature-sensitive vaccine shipments within North America rely on qualified isothermal shippers capable of maintaining 2–8°C or controlled room temperature for up to 120 hours. Adoption is particularly strong across biotech exports, clinical trial logistics, and specialty food distribution, reinforcing high-capacity domestic production exceeding 45 million thermal units annually.

Market Size & Growth: Valued at USD 3251.42 Million in 2025, projected to reach USD 5027.88 Million by 2033 at 5.6% CAGR, driven by expanding biologics distribution and cross-border cold chain logistics.

Top Growth Drivers: 38% increase in biologics shipments, 32% rise in e-commerce grocery penetration, 27% growth in global vaccine transportation demand.

Short-Term Forecast: By 2028, optimized reusable isothermal packaging systems are expected to reduce cold chain losses by 18% and logistics costs by 12%.

Emerging Technologies: Vacuum insulated panels (VIP), advanced phase change materials (PCM), IoT-enabled temperature monitoring with real-time data logging.

Regional Leaders: North America projected to reach USD 1680 Million by 2033 with strong pharma exports; Europe to reach USD 1340 Million driven by regulatory compliance; Asia-Pacific to reach USD 1225 Million supported by rapid biologics manufacturing expansion.

Consumer/End-User Trends: Pharmaceutical companies account for over 55% usage, followed by specialty food distributors and clinical research organizations adopting reusable insulated shippers.

Pilot or Case Example: In 2024, a global vaccine distributor reduced temperature excursions by 21% using AI-integrated thermal packaging validation systems.

Competitive Landscape: Sonoco ThermoSafe holds approximately 18% share, followed by Pelican BioThermal, Cryopak, Cold Chain Technologies, and Sealed Air.

Regulatory & ESG Impact: GDP compliance and WHO prequalification standards are accelerating adoption of recyclable insulation materials targeting 30% waste reduction by 2030.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally since 2023 in cold chain expansion, automation, and sustainable packaging innovations.

Innovation & Future Outlook: Growth in smart reusable shippers, carbon-neutral insulation materials, and AI-based route optimization platforms is shaping long-term resilience.

The Isothermal Packaging market is strongly influenced by pharmaceutical logistics, which contributes over 55% of total demand, followed by perishable food distribution at nearly 28% and clinical trial logistics at approximately 10%. Technological innovation is centered on lightweight vacuum insulated panels capable of extending temperature control beyond 96 hours, while advanced bio-based insulation materials are reducing carbon footprints by up to 25%. Stringent regulatory frameworks such as Good Distribution Practice (GDP) compliance requirements are encouraging adoption of validated thermal packaging solutions. North America and Europe exhibit high per-capita consumption due to established biologics exports, while Asia-Pacific demonstrates accelerating uptake driven by expanding vaccine production facilities in India and China. Increasing sustainability mandates and reusable packaging cycles are expected to reshape procurement strategies over the next decade.

The Isothermal Packaging Market holds strategic importance within global pharmaceutical, biotechnology, and perishable goods supply chains due to its role in preserving product integrity during extended transit periods. With over 20% of global pharmaceutical products classified as temperature-sensitive, advanced thermal packaging solutions are critical to minimizing spoilage and regulatory non-compliance risks. New-generation vacuum insulated panel systems deliver 35% longer temperature retention compared to traditional expanded polystyrene containers, significantly improving reliability during international shipments.

North America dominates in shipment volume due to established biologics exports, while Europe leads in adoption intensity with nearly 65% of pharmaceutical enterprises implementing validated reusable thermal shippers. Asia-Pacific is witnessing rapid expansion, particularly in India and South Korea, where biologics manufacturing capacity increased by more than 25% over the past three years.

By 2028, AI-enabled predictive temperature analytics integrated within smart isothermal packaging is expected to reduce cold chain excursion rates by 20% and improve delivery compliance metrics by 15%. ESG-driven transformation is also accelerating, with firms committing to 30% recyclable material integration and 40% reusable packaging cycles by 2030 to align with carbon reduction goals. In 2024, Germany achieved a 17% reduction in pharmaceutical shipment losses through deployment of IoT-integrated thermal monitoring within reusable insulated containers. Such measurable improvements reinforce the Isothermal Packaging Market as a critical pillar of supply chain resilience, regulatory compliance, and sustainable global growth.

The rapid expansion of biologics and vaccine production is a primary growth catalyst for the Isothermal Packaging Market. More than 50% of pharmaceutical pipelines now consist of temperature-sensitive biologic therapies requiring strict 2–8°C or frozen storage conditions. Global vaccine production capacity surpassed 15 billion doses annually, necessitating validated thermal shippers capable of maintaining stability during long-haul transport. Clinical trial activities have increased by over 30% in emerging markets, further boosting demand for certified isothermal containers. Extended transit routes, especially across Asia-Pacific and Latin America, require high-performance phase change material systems capable of sustaining temperature integrity for up to five days. This growing pharmaceutical dependency significantly elevates demand for reliable and regulatory-compliant thermal packaging solutions.

Advanced isothermal packaging solutions rely heavily on premium materials such as vacuum insulated panels and specialized phase change materials, which can increase production costs by 25–40% compared to conventional insulated boxes. Regulatory validation processes, including thermal performance testing and stability certification, require significant investment in laboratory infrastructure and compliance audits. Smaller logistics providers often face financial barriers in adopting reusable thermal systems due to higher upfront capital expenditure. Additionally, fluctuating raw material prices, particularly petroleum-based foams and aluminum components, create pricing volatility. Disposal and recycling complexities of certain insulation materials also impose operational burdens, limiting rapid adoption in cost-sensitive markets.

Reusable and IoT-enabled thermal packaging presents substantial growth opportunities across pharmaceutical and specialty food logistics. Reusable shippers can complete up to 20 distribution cycles, reducing overall packaging waste by nearly 60% compared to single-use alternatives. Smart packaging integrated with GPS and temperature sensors enables real-time shipment visibility, lowering product loss incidents by up to 22%. Emerging markets in Southeast Asia and Africa are investing heavily in cold chain infrastructure, creating untapped demand for durable insulated containers. Sustainability-focused procurement policies in Europe encourage suppliers to offer recyclable insulation solutions, opening pathways for innovation in bio-based materials. These evolving trends position the Isothermal Packaging Market for diversified and technology-driven expansion.

The Isothermal Packaging Market faces significant challenges from stringent global regulatory standards and logistical vulnerabilities. Pharmaceutical shipments must comply with Good Distribution Practice (GDP) guidelines and country-specific health authority requirements, often necessitating region-specific thermal validation. Any deviation can result in rejected shipments or product recalls, increasing operational risk. Cold chain disruptions, including port congestion and flight cancellations, extend transit durations beyond validated timeframes. Additionally, maintaining consistent temperature control in regions with limited refrigeration infrastructure remains difficult. Environmental concerns over single-use plastics further complicate material selection. These combined operational and compliance pressures demand continuous innovation and investment, raising entry barriers for smaller market participants.

• 42% Increase in Reusable Thermal Shipper Deployment Across Pharmaceutical Logistics

The transition toward reusable isothermal packaging solutions has accelerated significantly, with more than 42% of pharmaceutical exporters integrating multi-use insulated shippers into their distribution networks. These systems typically support 15–25 reuse cycles, reducing packaging waste by nearly 60% compared to single-use formats. Reverse logistics programs have expanded by 35% since 2023, particularly in North America and Western Europe, where sustainability mandates are stringent. Deployment of returnable pallet-sized containers has improved load optimization efficiency by 18%, while lifecycle carbon emissions have decreased by up to 28% per shipment under closed-loop recovery models.

• 37% Adoption Growth in IoT-Enabled Temperature Monitoring Systems

Smart isothermal packaging integrated with IoT-based temperature sensors has witnessed 37% growth in adoption among global biologics manufacturers. Real-time GPS and temperature data logging reduce excursion-related losses by approximately 22% during long-haul shipments exceeding 72 hours. Over 65% of large pharmaceutical companies now require digital temperature validation as part of compliance documentation. Cloud-based monitoring dashboards have shortened response times to thermal deviations by 30%, strengthening supply chain resilience and audit readiness.

• 33% Expansion in Advanced Vacuum Insulated Panel (VIP) Utilization

High-performance vacuum insulated panels are increasingly replacing conventional expanded polystyrene, accounting for a 33% increase in usage across validated cold chain systems. VIP solutions extend thermal stability duration by up to 35% and reduce container wall thickness by 20%, enabling higher payload capacity. Europe leads in regulatory-driven adoption, where 58% of pharmaceutical shipments utilize enhanced insulation systems to meet stringent GDP compliance standards.

• 29% Growth in Bio-Based and Recyclable Insulation Materials

Sustainable insulation materials derived from plant fibers and recyclable polymers have grown by 29% in industrial adoption. Manufacturers report up to 25% lower carbon footprints compared to petroleum-based foams. Approximately 48% of new product launches in 2024 incorporated partially recyclable components. Corporate ESG commitments targeting 30–40% packaging waste reduction by 2030 are accelerating procurement of environmentally responsible isothermal packaging formats.

The Isothermal Packaging Market is segmented by type, application, and end-user, each reflecting distinct operational requirements and compliance standards. By type, insulated containers and boxes account for the majority of deployment due to their adaptability across pharmaceutical and food logistics. Advanced pallet shippers and parcel-sized thermal mailers serve niche yet expanding segments. In terms of application, pharmaceutical logistics dominates usage because over 50% of modern drug formulations require temperature control between 2°C and 8°C. Food and beverage distribution, including meal kits and specialty seafood, represents a growing secondary segment supported by expanding e-commerce penetration exceeding 30% in developed markets. From an end-user perspective, pharmaceutical and biotechnology companies represent the largest adopters, while contract logistics providers and research institutions contribute substantially to recurring demand. Regional consumption patterns indicate mature compliance-driven uptake in North America and Europe, while Asia-Pacific demonstrates increasing penetration driven by vaccine production expansion and cross-border biologics exports.

Insulated containers and boxes currently account for approximately 46% of total adoption within the Isothermal Packaging Market due to their versatility in maintaining 2–8°C conditions for up to 120 hours. Pallet shippers represent around 28%, primarily used for bulk vaccine and biologics transportation. Thermal mailers and parcel shippers collectively contribute nearly 18%, serving small-volume e-commerce and specialty food deliveries. Meanwhile, advanced vacuum insulated panel (VIP) systems, though presently representing 8%, are the fastest-growing type with an estimated 7.8% CAGR, driven by demand for extended-duration performance and space optimization benefits of up to 20% payload improvement. Reusable insulated containers are gaining preference due to lifecycle cost reductions exceeding 25% after 15 shipping cycles. Lightweight PCM-integrated systems are also expanding adoption among clinical trial logistics providers requiring strict temperature validation.

Pharmaceutical logistics leads the Isothermal Packaging Market with nearly 55% usage share, reflecting the high proportion of temperature-sensitive biologics and vaccines in global distribution. Food and beverage applications hold approximately 27%, particularly in seafood, dairy, and premium meal kit segments. Clinical trial logistics accounts for around 10%, while chemical and specialty materials applications contribute roughly 8%. While pharmaceutical distribution remains dominant, e-commerce-driven food delivery is the fastest-growing application segment with an estimated 8.4% CAGR, supported by a 31% increase in cross-border perishable shipments. Online grocery penetration in developed economies exceeds 35%, directly elevating demand for reliable insulated packaging solutions capable of 24–72 hour protection.

Pharmaceutical and biotechnology companies represent the leading end-user segment, accounting for approximately 52% of total market adoption due to stringent GDP compliance requirements and increasing biologics output. Third-party logistics providers (3PLs) contribute nearly 24%, driven by outsourced cold chain operations and cross-border distribution complexity. Food retailers and meal kit providers hold around 16%, while research institutions and specialty chemical companies collectively account for 8%. Although pharmaceutical firms dominate current demand, contract logistics providers are the fastest-growing end-user group with an estimated 7.2% CAGR, supported by a 29% rise in pharmaceutical outsourcing contracts over the past three years. Adoption among e-commerce grocery distributors has increased by 26%, reflecting changing consumer purchasing behavior.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America’s dominance is supported by over 250 biologics manufacturing facilities and more than 60% enterprise adoption of validated reusable thermal shippers in pharmaceutical exports. Europe followed with approximately 29% share in 2025, driven by strict GDP compliance standards and 58% penetration of advanced vacuum insulated panels in regulated shipments. Asia-Pacific represented nearly 23% of global demand, supported by vaccine production volumes exceeding 4 billion doses annually across India and China. South America accounted for 6%, while the Middle East & Africa contributed close to 4%, with rising investments in cold chain warehousing exceeding 18% expansion since 2022. Cross-border pharmaceutical trade volumes in developed markets exceeded 800 billion units annually, intensifying the requirement for high-performance isothermal packaging systems capable of maintaining 2–8°C stability for 96–120 hours.

North America holds approximately 38% share of the global Isothermal Packaging Market, supported by high-volume pharmaceutical exports and advanced cold chain networks. Over 55% of temperature-sensitive drug shipments originate from large-scale biologics manufacturing clusters across the United States and Canada. Regulatory oversight under Good Distribution Practice standards has increased inspection frequency by 22% since 2023, pushing enterprises toward validated reusable packaging systems. More than 65% of pharmaceutical firms in this region deploy IoT-enabled temperature monitoring within insulated shippers. Technological advancements include phase change material optimization extending protection duration beyond 120 hours and digital twin-based validation testing reducing compliance timelines by 18%. Sonoco ThermoSafe, a key regional player, has expanded its reusable shipper fleet capacity by 30%, enhancing reverse logistics efficiency. Regional enterprise behavior indicates higher adoption among healthcare and biotech exporters, with over 60% preferring reusable insulated containers to meet ESG targets and reduce packaging waste by up to 40%.

Europe represents nearly 29% of global Isothermal Packaging Market demand, with Germany, the UK, and France contributing more than 65% of regional consumption. Strict GDP compliance regulations and sustainability directives under circular economy frameworks have increased recyclable insulation adoption by 35% since 2022. Approximately 58% of pharmaceutical shipments within this region utilize advanced vacuum insulated panels to meet extended transit stability requirements. Emerging technologies include lightweight bio-based insulation materials reducing carbon emissions by up to 25% and AI-powered shipment validation tools improving audit readiness by 20%. Pelican BioThermal has strengthened its European distribution hubs, increasing reusable shipper circulation cycles by 28%. Consumer and enterprise behavior reflects regulatory pressure driving demand for traceable, explainable thermal packaging systems, with more than 62% of life sciences firms mandating digital temperature documentation for cross-border trade.

Asia-Pacific ranks third in current share at approximately 23% but leads global growth momentum in the Isothermal Packaging Market. China, India, and Japan collectively account for over 70% of regional demand, supported by vaccine manufacturing volumes exceeding 4 billion doses annually. Infrastructure investments in temperature-controlled warehouses have grown by 18% since 2022, particularly in India’s pharmaceutical export corridors. Manufacturing expansion in biologics has increased adoption of extended-duration insulated pallet shippers by 26%. Innovation hubs in South Korea and Singapore are deploying smart packaging integrated with real-time GPS tracking, reducing temperature excursions by 19%. Cryopak has expanded operations within the region, enhancing production capacity for PCM-based solutions by 22%. Consumer behavior is influenced by rapid e-commerce growth, where online grocery penetration has crossed 30%, increasing demand for reliable insulated delivery solutions.

South America accounts for approximately 6% of the global Isothermal Packaging Market, with Brazil and Argentina representing nearly 70% of regional consumption. Pharmaceutical imports and exports have increased by 14% annually in volume terms, driving demand for validated insulated containers capable of maintaining temperature stability across extended shipping routes. Infrastructure upgrades in cold storage capacity have expanded by 16% since 2023. Government trade facilitation policies have reduced customs clearance time by 12%, enhancing cross-border pharmaceutical distribution efficiency. Local logistics providers are investing in reusable insulated packaging fleets, improving cost efficiency by up to 20% across multi-cycle operations. Regional buyer behavior shows growing reliance on compliant packaging formats, particularly among vaccine distributors and specialty food exporters seeking improved reliability and regulatory adherence.

The Middle East & Africa region contributes close to 4% of global Isothermal Packaging Market demand, with the UAE and South Africa leading adoption. Pharmaceutical imports have grown by 15% in volume terms since 2022, increasing the requirement for validated thermal packaging. Infrastructure modernization projects have expanded temperature-controlled warehousing capacity by 21% across key trade hubs such as Dubai and Johannesburg. Technological modernization includes IoT-integrated temperature monitoring systems improving compliance reporting accuracy by 24%. Trade partnerships within the Gulf Cooperation Council have reduced cross-border transit times by 10%, supporting pharmaceutical distribution efficiency. Regional procurement behavior reflects increasing emphasis on reliability, particularly among healthcare providers and humanitarian vaccine programs requiring extended 96-hour temperature stability during transport.

United States – 34% market share: The Isothermal Packaging Market in the United States is driven by high biologics production capacity and over 250 regulated pharmaceutical manufacturing facilities requiring validated temperature-controlled logistics.

Germany – 12% market share: The Isothermal Packaging Market in Germany benefits from strong pharmaceutical exports, strict GDP compliance standards, and advanced adoption of recyclable insulated packaging technologies.

The Isothermal Packaging Market demonstrates a moderately consolidated structure, with the top five companies accounting for approximately 52% of global demand. More than 120 active competitors operate globally, including specialized thermal packaging manufacturers and diversified protective packaging firms. Leading players focus on reusable insulated containers, vacuum insulated panels, and phase change material innovations capable of extending temperature stability by up to 35% compared to conventional systems.

Strategic initiatives include partnerships with third-party logistics providers, expansion of reverse logistics networks, and regional manufacturing facility investments exceeding 25% capacity growth since 2023. Product launches incorporating IoT-based temperature monitoring have increased by 40% over the past two years. Competitive differentiation is centered on compliance validation, sustainability metrics, and lifecycle cost optimization. Companies are also targeting carbon footprint reduction goals of 30–40% by integrating recyclable and bio-based insulation materials. Automation in manufacturing has improved production efficiency by 18%, intensifying pricing competitiveness while maintaining regulatory-grade performance standards.

Sonoco ThermoSafe

Pelican BioThermal

Cold Chain Technologies

Cryopak

Sealed Air

Sofrigam

Va-Q-tec

Tempack

Inmark Packaging

Insulated Products Corporation

Technological innovation in the Isothermal Packaging Market is centered on enhancing thermal performance duration, sustainability metrics, and digital traceability. Vacuum insulated panels (VIPs) now deliver thermal conductivity levels as low as 0.004 W/mK, compared to 0.030–0.040 W/mK in conventional expanded polystyrene, extending temperature stability by up to 35% for shipments exceeding 96 hours. Advanced phase change materials (PCMs) are engineered with melting points precisely calibrated between -20°C and +25°C, enabling multi-temperature configurations within a single insulated shipper. These PCMs maintain thermal equilibrium for 72–120 hours depending on ambient exposure conditions.

Smart packaging integration is accelerating, with over 65% of large pharmaceutical exporters deploying IoT-enabled temperature data loggers embedded within isothermal containers. Real-time monitoring platforms reduce temperature excursion incidents by approximately 20% and improve regulatory audit readiness by 30% through automated compliance documentation. Bluetooth Low Energy (BLE) and GSM-based tracking modules now operate with battery lives exceeding 120 days, enabling reusable shipper monitoring across 15–20 distribution cycles.

Sustainability-driven material innovation is another core focus. Bio-based insulation fibers and recyclable polyurethane foams reduce lifecycle carbon emissions by up to 25% compared to petroleum-derived materials. Lightweight structural redesign has improved payload efficiency by nearly 18%, optimizing air freight utilization. Additionally, AI-driven thermal modeling software shortens validation testing time by 22%, enabling faster product certification. These technology advancements collectively strengthen supply chain resilience, regulatory compliance, and cost efficiency across global temperature-controlled logistics networks.

• In February 2024, Sonoco ThermoSafe launched its Pegasus ULD® bulk temperature-controlled container for pharmaceutical air cargo. The solution offers up to 5 days of thermal performance at 2–8°C and is qualified for extreme ambient ranges from -40°C to +60°C. Source: www.sonocothermosafe.com

• In March 2024, va-Q-tec announced the expansion of its reusable thermal container fleet across Europe, increasing available container units by over 20% to support rising pharmaceutical exports and sustainable closed-loop logistics programs. Source: www.va-q-tec.com

• In April 2024, Pelican BioThermal introduced the Crēdo™ Go reusable parcel shipper in North America, designed for 2–8°C transport with validated durations exceeding 96 hours and supporting reverse logistics programs across clinical trial supply chains.

• In January 2025, Cold Chain Technologies completed the acquisition of a European temperature-controlled packaging provider to expand its global footprint and strengthen sustainable, reusable shipper solutions for life sciences customers.

The Isothermal Packaging Market Report provides comprehensive coverage of product types including insulated containers, pallet shippers, parcel mailers, vacuum insulated panel systems, and advanced phase change material configurations. The report analyzes packaging performance categories ranging from 24-hour to 120-hour thermal stability solutions, addressing both single-use and reusable formats with lifecycle utilization of up to 20 distribution cycles.

Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating more than 20 key countries with emphasis on pharmaceutical export hubs, vaccine manufacturing clusters, and emerging cold chain infrastructure markets. Application coverage includes pharmaceutical logistics representing over 50% of demand, perishable food distribution accounting for approximately 27%, and specialized segments such as clinical trials, chemical transport, and biotechnology research.

The study evaluates technological frameworks including IoT-enabled monitoring, AI-driven thermal modeling, recyclable insulation materials, and carbon footprint optimization strategies targeting 30–40% emission reductions. It further examines regulatory compliance standards such as GDP guidelines, temperature validation protocols, and sustainability mandates influencing procurement decisions. Emerging niches such as bio-based insulation and smart reusable shipper fleets are analyzed alongside digital transformation trends shaping global temperature-controlled supply chains.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sonoco ThermoSafe, Pelican BioThermal, Cold Chain Technologies, Cryopak, Sealed Air, Sofrigam, Va-Q-tec, Tempack, Inmark Packaging, Insulated Products Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |