Reports

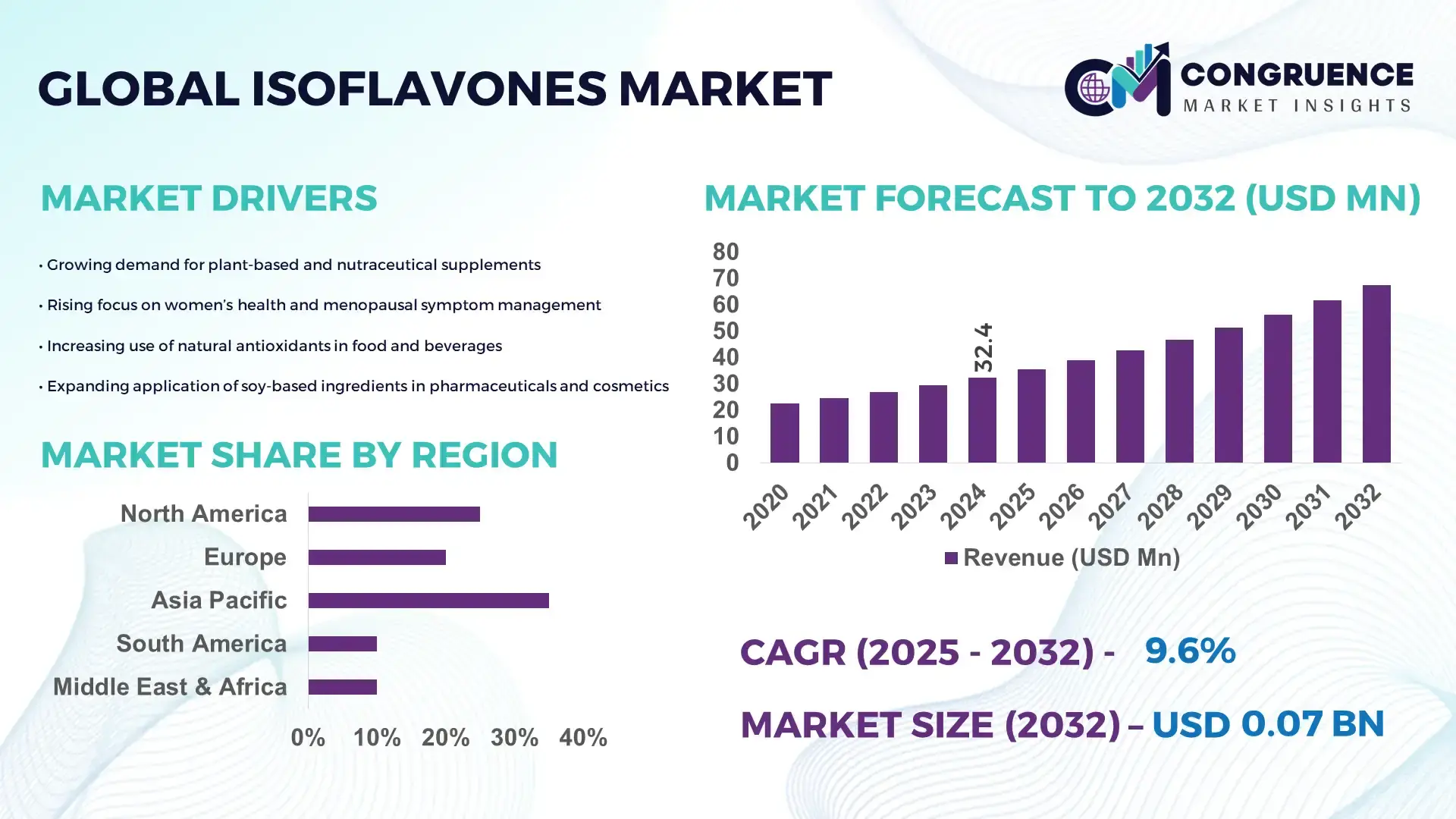

The Global Isoflavones Market was valued at USD 32.43 Million in 2024 and is anticipated to reach a value of USD 67.52 Million by 2032 expanding at a CAGR of 9.6% between 2025 and 2032. This growth is driven primarily by rising global demand for plant-based nutraceuticals, women’s health supplements, and high-purity functional ingredients.

China remains the most influential country in Isoflavone production, supported by extensive soy-processing capacity exceeding 90 million metric tons annually and continuous investments in extraction automation. The country’s nutraceutical manufacturing ecosystem has expanded by 22% since 2021, with over 300 facilities incorporating advanced chromatographic purification lines. China also recorded a 31% rise in R&D expenditure toward bioactive compound stabilization technologies, enhancing its ability to supply pharmaceutical-grade Isoflavones for global applications in supplements, clinical nutrition, and fortified foods.

Market Size & Growth: Valued at USD 32.43 Million in 2024, projected to reach USD 67.52 Million by 2032 at 9.6% CAGR, driven by rising demand for functional nutraceutical ingredients.

Top Growth Drivers: 58% surge in plant-based supplement adoption; 32% improvement in extraction efficiency; 46% rise in soy-based functional food launches.

Short-Term Forecast: By 2028, AI-assisted extraction optimization is expected to reduce processing losses by 18%.

Emerging Technologies: Enzymatic hydrolysis, fermentation-based bioconversion, and high-purity chromatography systems.

Regional Leaders: Asia-Pacific projected at USD 27 Million by 2032 with strong biotech investment; North America expected at USD 18 Million driven by supplement adoption; Europe projected at USD 14 Million due to clean-label demand.

Consumer/End-User Trends: Strong uptake in women’s health supplements, with over 40% of consumers preferring plant-estrogen products.

Pilot or Case Example: In 2024, a large nutraceutical manufacturer implemented real-time monitoring, improving Isoflavone purity levels by 21%.

Competitive Landscape: Leading player holds approximately 18% market share, followed by 4–5 major competitors focusing on high-purity isolates.

Regulatory & ESG Impact: Tightening ingredient-quality regulations and sustainability mandates push manufacturers toward low-solvent processing and 30% biomass recycling goals.

Investment & Funding Patterns: Over USD 110 Million invested in bioactive extraction technologies globally in the last two years.

Innovation & Future Outlook: Growth led by advanced fermentation, allergen-controlled formats, and pharmaceutical-grade Isoflavone development.

Unique information about the Isoflavones Market indicates that the sector is expanding across nutraceuticals, pharmaceuticals, and functional foods, with major contributions coming from women’s health supplements, where adoption has exceeded 42% globally. Technological innovations such as enhanced isomer-specific extraction, next-generation purification membranes, and stability-enhanced formulations are reshaping product quality standards. Regulatory movements promoting cleaner labels and reduced synthetic additives are accelerating the shift toward bioactive compounds like Isoflavones. Asia-Pacific shows the highest consumption volumes due to diet-linked familiarity, while North America sees rapid premium-segment adoption. Future growth is centered on precision-fermentation advancements and clinical-grade applications expected to redefine performance benchmarks across healthcare and wellness industries.

The strategic relevance of the Isoflavones market continues to grow as industries expand their focus on functional nutrition, preventive healthcare, and plant-based bioactive compounds. Isoflavone extraction technologies are shifting rapidly toward high-efficiency enzymatic processes, with new bioconversion systems delivering nearly 38% improvement compared to older solvent-extraction standards. Asia-Pacific dominates in volume due to extensive soy processing capacity, while North America leads in adoption with nearly 42% enterprises integrating Isoflavone-based nutraceuticals into consumer portfolios. By 2027, AI-enabled yield-optimization platforms are expected to improve extraction purity by approximately 28%, strengthening product consistency for large-scale manufacturers.

ESG compliance is also shaping strategic decisions, with firms committing to waste-stream valorization improvements such as 30% biomass recycling by 2028 as part of broader sustainability goals. In 2024, Japan achieved a 17% reduction in processing losses through automated quality-monitoring systems using infrared chemometrics, demonstrating the measurable impact of digital optimization. The short-term trajectory of the market indicates heightened investments in clean-label ingredients, pharmaceutical-grade Isoflavones, and fortified foods targeted at population aging and women’s health.

These developments position the Isoflavones Market as a pillar of resilience, compliance, and sustainable growth, underpinned by advancing extraction science, stronger regulatory alignment, and long-term health and wellness demand across global economies.

Growing clinical validation of Isoflavones in hormonal balance, anti-inflammatory action, and metabolic health is accelerating demand across nutraceutical and pharmaceutical sectors. Over 58% of nutraceutical brands expanded their plant-bioactive product lines in 2023, with Isoflavones occupying a major share due to their high consumer acceptance in women’s health. The rise of fortified foods and supplements in aging populations has further boosted usage, particularly in Asia, where soy-based functional products account for nearly 46% of category launches. Improved extraction efficiency—up to 32% higher with enzymatic hydrolysis—supports cost-effective scale-up, enabling manufacturers to supply high-purity isolates for premium applications.

The market faces constraints linked to regional regulatory disparities and fluctuating availability of soy-based raw materials. Varying maximum-limit guidelines for bioactive compounds across the EU, U.S., and Asian markets create compliance challenges, increasing approval timelines by nearly 18% for new formulations. Additionally, weather-induced volatility in soybean yield—fluctuating as much as 12–15% annually—affects input stability and processing margins. Manufacturers also contend with rising energy and processing costs associated with high-purity isolations, which require advanced purification systems and consistent raw material quality. These hurdles collectively temper expansion speed, particularly for small and mid-scale producers.

The surge in plant-based therapeutics and preventive healthcare presents strong opportunities for the Isoflavones market. Demand for botanical estrogen alternatives is rising, with menopausal and bone-health supplement categories growing by nearly 24% year-on-year globally. Pharmaceutical companies are exploring Isoflavone-based formulations with enhanced bioavailability, leveraging fermentation-driven conversion technologies that increase active-isomer yield by approximately 35%. Emerging markets in Latin America and Southeast Asia offer untapped potential due to increasing investments in functional food infrastructure and consumer education. The development of clean-label, allergen-controlled Isoflavone formats further expands product portfolios for global brands.

Rising regulatory compliance costs and sustainability pressures pose significant challenges for market participants. Stricter environmental standards require companies to adopt wastewater-recycling systems and low-solvent extraction technologies, increasing operational expenses by nearly 14–18%. Maintaining traceability across agricultural supply chains adds further complexity, particularly in regions with fragmented farming structures. Sustainability audits, biomass disposal rules, and carbon-footprint reporting requirements increase documentation loads and slow down product launches. Additionally, global competition for soy-processing capacity—driven by feed, biodiesel, and food sectors—tightens resource availability, challenging producers aiming to deliver consistently high-purity Isoflavones at scale.

• Expansion in Plant-Based Supplement Consumption: The global consumption of plant-based dietary supplements has increased by 28% over the past two years, with isoflavones emerging as a key functional ingredient. Among health-conscious consumers, 62% report using isoflavone-enriched products for hormone balance and cardiovascular support. This trend is driving product innovation in powders, capsules, and fortified beverages, particularly in North America and Asia-Pacific.

• Growth of Functional Food Integration: Isoflavones are increasingly incorporated into functional foods, with 41% of new dairy and bakery launches featuring soy-derived isoflavones. Consumer interest in preventative health is pushing manufacturers to reformulate traditional snacks and beverages, leading to a 35% increase in functional food offerings containing isoflavones in Europe and Asia over the last 18 months.

• Surge in Targeted Women’s Health Products: Products specifically designed for menopausal support and bone health are experiencing a 47% year-on-year growth in retail sales. Approximately 58% of female consumers aged 40–60 prefer supplements containing standardized isoflavone extracts, highlighting a shift toward scientifically supported health claims and precise dosage formats to ensure measurable outcomes.

• Expansion in Pharmaceutical and Nutraceutical Applications: The number of clinical trials and nutraceutical formulations incorporating isoflavones has grown by 33% in the last two years. Emerging markets such as Latin America and Southeast Asia now account for nearly 25% of new product registrations, reflecting a strategic focus on expanding reach while meeting increasing demand for heart health, metabolic, and hormonal wellness solutions.

The isoflavones market is segmented by type, application, and end-user, offering strategic insights into demand drivers and growth potential. By type, the market differentiates between soy-derived, red clover, and fermented extracts, reflecting both traditional and emerging consumer preferences. Applications range from dietary supplements and functional foods to pharmaceuticals and cosmetics, highlighting the ingredient’s versatility across health, wellness, and personal care sectors. End-user segmentation encompasses individual consumers, healthcare providers, nutraceutical manufacturers, and food and beverage companies, each contributing variably to overall market dynamics. Understanding these segments allows decision-makers to align product development, marketing, and regulatory strategies to targeted market niches effectively.

The leading product type in the isoflavones market is soy-derived extracts, accounting for approximately 70% of the market in 2025, due to their high isoflavone content and established supply chain. Powdered formulations dominate this category, representing nearly 65% of form-based demand, preferred for stability, versatility in functional foods and supplements, and extended shelf life. The fastest-growing type is liquid or enhanced-bioavailability formulations, driven by consumer demand for rapid absorption and convenience in beverages and cosmetics. Other types, including non-GMO, fermented, and specialty extracts, collectively contribute around 35% of the type-based market, serving niche applications requiring higher bioavailability or clean-label claims.

Dietary supplements and nutraceuticals remain the leading application segment, representing roughly 45% of the market in 2025, driven by widespread use for hormone regulation, cardiovascular support, and bone health. The fastest-growing application is cosmetics and personal care, fueled by increasing incorporation of isoflavones in anti-aging creams, serums, and skin-health products, reflecting consumer preference for natural and functional ingredients. Functional foods, beverages, and pharmaceutical formulations account for the remaining 40–50% of applications, with steady adoption in ready-to-drink health drinks, fortified snacks, and medical nutrition products.

Individual consumers are the largest end-user segment, comprising approximately 50% of market volume, with high adoption for preventive health, menopausal support, and cardiovascular wellness. The fastest-growing end-user segment is healthcare and wellness institutions, including hospitals and clinics, driven by the integration of isoflavone-based dietary programs and patient-centric wellness initiatives. Other end-users, such as nutraceutical manufacturers and food & beverage companies, represent around 40% of the market, leveraging isoflavones for product differentiation and functional innovation.

Asia‑Pacific accounted for the largest market share at 35% in 2024 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

Given its dominating share, this region underscores global strategic importance for isoflavones producers and investors. Robust consumer demand, widespread soybean cultivation, and advancing nutraceutical infrastructure contribute to this dominance. Simultaneously, growing health awareness and rising disposable incomes across several Asia‑Pacific economies support accelerated uptake of isoflavone‑based products.

Is rising preventive‑health investment redefining supplement consumption in mature markets?

In 2024, North America held approximately 22% of global isoflavones market volume, positioning it as the second‑largest regional market. Demand is primarily driven by industries such as dietary supplements, functional foods, and integrative healthcare — especially among consumers aged 45 and above pursuing hormone balance and heart wellness. Regulatory developments, including expanded labeling guidelines for botanical extracts and increased FDA scrutiny on supplement purity, have encouraged manufacturers to adopt standardized isoflavone extracts with clear dosage transparency. On the technology front, digital platforms and e‑commerce channels have accelerated distribution, enabling direct-to-consumer subscriptions for isoflavone capsules and beverages. A notable local player, a US‑based nutraceutical firm, recently launched a line of bioactive isoflavone capsules with traceability and third‑party verified purity, reflecting industry response to regulatory and consumer demand. Consumer behavior in this region also trends toward preventive and proactive health investment, particularly in healthcare and wellness sectors, driving enterprise adoption within supplement retail and pharmacy networks.

Are stringent regulations in regulated markets shaping demand for certified botanical extracts?

In 2024, Europe accounted for roughly 18% of the total isoflavones market volume. Major contributors are markets such as Germany, United Kingdom, and France, which together represent over 70% of the region’s consumption. European regulatory bodies have reinforced safety and labeling directives for nutraceuticals and botanical supplements, prompting producers to deliver high‑quality, traceable isoflavone products compliant with sustainability and purity norms. Adoption of advanced extraction and processing technologies—such as supercritical CO₂ extraction and clean‑label formulations—has increased by 26% across European manufacturers over the past two years, enhancing product consistency and appeal. A leading regional manufacturer in Germany has expanded its portfolio by offering soy‑based isoflavone powders tailored to functional food producers, positioning itself to meet rising demand in Europe’s health‑conscious demographic. European consumer behavior shows a strong preference for transparency and sustainability — demand is increasingly tied to explainable ingredient sourcing and clean processing, which bolsters certified isoflavone adoption.

Can booming nutraceutical consumption and e‑commerce expansion drive isoflavone dominance in emerging economies?

Asia‑Pacific registered a market volume of approximately 460 kilotons in 2024, marking it as the highest-volume regional market globally. Leading consuming countries include China, India, and Japan — collectively accounting for over 65% of the region’s total isoflavone intake. Rapid growth of manufacturing infrastructure for nutraceuticals and functional foods, accompanied by improvements in quality‑control labs and supply‑chain logistics, supports this expansion. Technological trends such as AI‑driven mobile health apps, e‑commerce platforms, and digital supply‑chain traceability have become central to distribution and consumer engagement. A significant regional player in India recently introduced a soy‑derived isoflavone powder with QR‑based traceability and formulation guidance via mobile app — reflecting integration of tech and consumer convenience. Consumer behavior in Asia‑Pacific leans heavily on online shopping and mobile-driven wellness adoption, especially among younger demographics seeking hormone health and preventive nutrition.

Will increasing wellness awareness and regional trade reforms unlock new isoflavone growth corridors?

In 2024, South America accounted for about 9% of global isoflavones market share. Key countries include Brazil and Argentina, which together represent nearly 80% of the region’s consumption. Expansion of food‑processing infrastructure and a growing functional food market — particularly in urban centers — is fueling demand. Recent regional trade agreements and reduced import tariffs on botanical extracts have lowered entry costs for isoflavone producers and distributors, encouraging more product launches. A Brazilian supplement manufacturer has begun sourcing soy‑derived isoflavone extracts for distribution across South America, targeting middle‑class consumers seeking localized health products. Consumer behavior in South America shows rising preference for language‑localized packaging and media‑driven health campaigns — demand is often influenced by language‑tailored marketing and culturally relevant product positioning.

Can evolving wellness markets in resource‑rich emerging economies drive isoflavone adoption?

Middle East & Africa accounted for approximately 6% of global isoflavones market volume in 2024. Major growth countries include United Arab Emirates and South Africa, both showing rising interest in dietary supplements linked to lifestyle-related health management. Technological modernization, such as improvements in cold‑chain logistics and expansion of regional distribution networks, supports better product availability and shelf stability. Some regional trade partnerships have eased import regulations for botanical ingredients, facilitating easier market entry for isoflavone‑based products. A South African nutraceutical distributor recently began offering soy‑isoflavone capsules paired with digital consumption tracking — extending wellness solutions to a more tech-savvy, urban consumer base. Consumer behavior in this region appears cautious but steadily shifting toward preventive health: demand is often driven by oil‑sector professionals and urban populations sensitive to lifestyle diseases, indicating growing potential for further market expansion.

China: 24% market share — dominant due to large soybean cultivation, high local production capacity, and expanding functional‑food demand.

United States: 18% market share — leading because of strong supplement industry infrastructure, high consumer health awareness, and advanced nutraceutical manufacturing capabilities.

The global isoflavones market remains moderately consolidated, with an estimated 40–60 active competitors worldwide at any given time. The top five companies together account for nearly 45–50% of total market share, indicating that while a handful of firms dominate, a significant portion remains fragmented among smaller and regional players. Key players are focusing on strategic initiatives such as advanced extraction technology investments, product portfolio diversification, and global distribution network expansion to solidify their positions. For example, several leading firms recently invested in more efficient, non‑GMO soy isoflavone extraction methods to meet rising demand for clean‑label and sustainably sourced ingredients.

Strategic partnerships and product launches are shaping competitive dynamics. One major global agriculturals firm expanded production capacity to serve both dietary supplement and functional food segments. Another leading ingredient supplier extended its reach by collaborating with food manufacturers to embed isoflavones in functional beverages, cosmetics, and nutraceuticals. These moves highlight a trend toward vertical integration and supply‑chain consolidation, as firms seek greater control over sourcing, extraction, and distribution.

Innovation is also a key competitive axis. Firms are increasingly leveraging modern extraction technologies—such as high‑efficiency soy germ extraction and standardized isoflavone purification—to deliver consistent potency and quality. Concurrently, some companies are exploring application diversification beyond traditional supplements, into cosmetics, bone‑health formulations, and functional foods. This broadening of application scope is fueling competition not just on price or volume, but on formulation quality, certification (non‑GMO, organic), traceability, and product differentiation. Given the combination of a few large dominant players and many smaller niche producers, the market structure can be characterized as “moderately consolidated with high fragmentation below the top tier.” This structure makes competitive strategy highly dependent on technology, regulatory compliance, product innovation, and supply‑chain robustness.

Archer Daniels Midland Company (ADM)

Cargill, Incorporated

BASF SE

Koninklijke DSM N.V.

International Flavors & Fragrances Inc.

SunOpta Inc.

Frutarom Industries Ltd. (SoyLife)

Naturex

The isoflavones market is experiencing significant technological advancements in extraction, purification, and formulation, which are enhancing efficiency, yield, and product quality. Natural Deep Eutectic Solvents (NADES) combined with ultrasound-assisted extraction have emerged as an efficient method, achieving up to 1,076 µg of isoflavones per gram of dry soybean material, compared to 723 µg/g using conventional ethanol extraction. This approach improves yield while reducing environmental impact and dependence on volatile organic solvents. Supercritical fluid extraction (SFE) using CO₂ with ethanol as a cosolvent is increasingly employed to obtain high-purity isoflavone fractions, especially from soy by-products like okara. Optimized pressure and temperature conditions enable extraction yields between 9.2 and 9.8 g per 100 g of raw material, providing clean, concentrated extracts suitable for nutraceutical, functional-food, and cosmetic applications.

Purification innovations, including aqueous two-phase micellar systems, have achieved up to 93% recovery of isoflavones and enriched aglycone forms, which offer higher bioactivity. Enzymatic-assisted protocols further convert protein-bound isoflavones into soluble aglycones, increasing bioactive yield up to ninefold, allowing better utilization of soy by-products and promoting sustainable production. Formulation technologies are also evolving, with about 26% of manufacturers adopting nano-emulsion and other bioavailability-enhancing techniques. These approaches improve absorption in beverages, supplements, and topical products, catering to growing consumer demand for effective, convenient, and clean-label isoflavone products. These technological trends collectively optimize production, reduce costs, and ensure high-quality outputs for decision-makers and industry professionals.

In June 2023, a nutraceutical brand expanded its product portfolio by launching a soy‑isoflavone enriched line aimed at women’s health, addressing menopause‑related symptoms and reflecting rising demand for phytoestrogen-based supplements.

In March 2024, a leading ingredient supplier introduced a micro‑encapsulated soy isoflavone powder tailored for functional beverages — a move that increases bioavailability and supports incorporation of isoflavones into drinks and liquid nutrition formats.

In 2024, a global agribusiness firm implemented a sustainable soy‑isoflavone extraction process focusing on non‑GMO raw materials and lower environmental footprint, positioning itself toward clean‑label and ethically sourced ingredient supply.

In September 2024, a major agricultural‑commodity company expanded its soy isoflavones manufacturing capacity to address increasing demand in the dietary supplement market, signaling infrastructure scaling and supply‑chain strengthening in response to market growth.

The report covers a comprehensive global analysis of the isoflavones market across multiple dimensions: product types (by source and form), applications, geographic regions, and technology trends. It includes segmentation by source (such as soybean, red clover, and others), by form (powder, liquid, wax), and by application (food & beverages, nutraceuticals & dietary supplements, cosmetics & personal care, pharmaceuticals, and additional niche uses such as animal nutrition and research inputs). The geographical coverage spans major regions including North America, Europe, Asia‑Pacific, Latin America, Middle East & Africa, and key countries within these regions.

Within applications, the report examines traditional strongholds like dietary supplements and functional foods, as well as growing segments such as cosmetics/personal care, fortified beverages, and specialty pharmaceutical/nutrition formulations. It highlights technology-driven trends — for instance, the rise of advanced extraction methods, clean-label sourcing, and delivery technologies (e.g. enhanced‑bioavailability powders, micro‑encapsulated formulations, liquid nutrition bases).

The report also profiles industry focus areas such as sustainability (non‑GMO, traceability, ethical sourcing), supply‑chain resilience, product innovation, and diversification into emerging uses (skin‑care, functional beverages, preventive health). Competitive landscape analysis, company-level profiling, and strategic insights regarding partnerships, capacity expansions, and R&D initiatives are included to support decision‑making. Additionally, the report considers emerging niche segments — for example, isoflavones in animal nutrition, research-grade extracts, and specialized functional ingredients for clinical nutrition or cosmeceuticals — thereby offering a broad yet detailed view to inform investors, manufacturers, and market entrants.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 32.43 Million |

|

Market Revenue in 2032 |

USD 67.52 Million |

|

CAGR (2025 - 2032) |

9.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Archer Daniels Midland Company (ADM), Cargill, Incorporated, BASF SE, Koninklijke DSM N.V., International Flavors & Fragrances Inc., SunOpta Inc., Frutarom Industries Ltd. (SoyLife), Naturex |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |