Reports

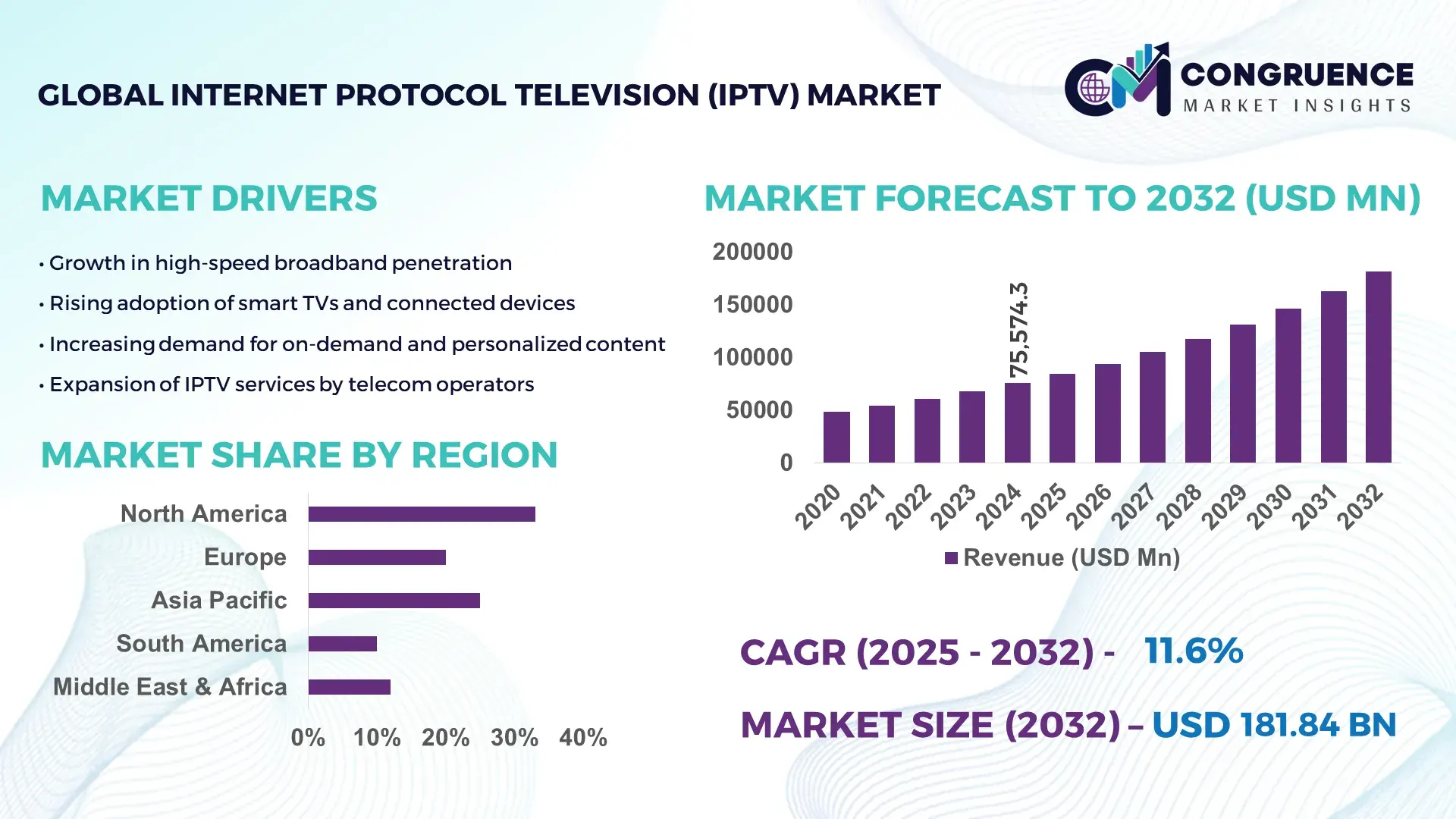

The Global Internet Protocol Television (IPTV) Market was valued at USD 75,574.27 Million in 2024 and is anticipated to reach a value of USD 181,839.2 Million by 2032 expanding at a CAGR of 11.6% between 2025 and 2032. Demand for high‑speed internet and the shift from traditional broadcast to on‑demand IP‑based content delivery are driving this growth.

The country that dominates the marketplace, China, continues to expand its IPTV infrastructure aggressively. In 2025, China’s IPTV‑CDN market alone was valued at approximately USD 4,689.5 million, reflecting a strong commitment to broadband and content‑delivery network expansion. Chinese providers have deployed over 2,000 CDN data centers, handling substantial live‑traffic loads daily, enabling high‑quality broadcast and video‑on‑demand services nationwide. Investment in next‑gen streaming technologies and fiber‑based broadband networks supports large‑scale IPTV delivery across urban and rural areas, catering to millions of daily viewers and fuelling consumer adoption across provinces.

Market Size & Growth: Current market value at USD 75,574.27 million (2024), projected to reach USD 181,839.2 million by 2032 at 11.6% CAGR; growth driven by rising broadband penetration and demand for on‑demand streaming.

Top Growth Drivers: High-speed internet adoption (48%), smartphone/video‑streaming penetration (36%), and shift from cable to IP-based content delivery (29%).

Short-Term Forecast: By 2028, expect overall IPTV operating costs to decline by 12% and average user streaming quality to improve by 15%.

Emerging Technologies: AI-driven content recommendation systems, cloud-CDN optimization, and integration of 5G streaming services.

Regional Leaders: Asia-Pacific projected to reach USD 65,000 million by 2032 with growing mobile-first consumption; North America expected to hit USD 50,000 million, driven by mature infrastructure; Europe projected around USD 40,000 million, with growth in hybrid IPTV‑OTT models.

Consumer/End-User Trends: Residential households remain primary subscribers; increasing preference for multi-device streaming (smart TVs, smartphones, tablets), and demand for localized content.

Pilot or Case Example: In 2025, a major IPTV-CDN deployment in a metropolitan region reduced latency by 30% and increased uptime by 99.8%, enhancing user retention.

Competitive Landscape: Market leader China-based telecom and IPTV operators (≈ 40–45% share), followed by major competitors AT&T, Verizon, Orange France, and SK Broadband.

Regulatory & ESG Impact: Regulatory incentives for broadband expansion in developing regions, and increased emphasis on energy-efficient data centers supporting IPTV infrastructure.

Investment & Funding Patterns: Recent investments in IPTV‑CDN infrastructure exceeded USD 5 billion globally in 2024–2025, with growing venture funding for AI-based personalization and streaming‑optimization startups.

Innovation & Future Outlook: Continued innovation in AI-personalization, 5G-based streaming, hybrid IPTV‑OTT platforms, and edge‑computing CDN deployments will drive future market expansion.

Global IPTV landscape is evolving with strong growth in residential streaming, widespread broadband infrastructure enhancements, regulatory support for digital services, and technological innovations such as AI‑based recommendations and 5G‑enabled delivery. Increasing content personalization, multi-device access, and cloud‑CDN scalability are shaping the future outlook, positioning IPTV as a key component of global digital entertainment and broadcasting ecosystems.

The Internet Protocol Television (IPTV) market is strategically vital as digital content consumption increasingly shifts online and away from traditional broadcast. IPTV enables operators and content providers to deliver high‑definition and on‑demand video over broadband networks, offering flexibility, interactivity, and scalable service models. As global broadband and 5G infrastructure expands, IPTV becomes a scalable backbone for multimedia delivery, supporting personalized content, live streaming, and value-added services such as interactive applications or targeted advertising. For example, AI-driven recommendation engines now deliver up to 40% improvement in user engagement and retention compared to legacy fixed‑schedule broadcasting. In regional terms, Asia-Pacific dominates in volume due to its large population and broadband rollout, while North America leads in adoption intensity with over 58% of households actively using IPTV services.

By 2028, integration of 5G streaming and adaptive codecs is expected to improve average streaming quality and reduce latency by as much as 25%. Firms are committing to ESG‑aligned data‑center optimizations — targeting a 20% reduction in energy consumption by 2030 through efficient server infrastructure. In one micro‑scenario, an operator in 2025 deployed cloud-CDN with AI‑based traffic routing and achieved a 30% reduction in buffering incidents and a 15% uplift in user satisfaction. These strategic moves show how IPTV is evolving — not just as a content delivery medium, but as a sustainable, efficient, and flexible platform for digital entertainment. In the long term, the IPTV market is positioned as a core pillar of resilient, compliant, and sustainable growth in global media distribution.

Widespread adoption of high-speed broadband (fiber, 5G) and smart devices such as smart TVs, smartphones, and tablets has dramatically expanded the addressable market for IPTV. With increasing internet penetration and improved connectivity, more households can access IPTV services reliably. Providers leverage this to offer high-definition content, on-demand libraries, and flexible viewing on multiple devices, increasing consumer uptake. The convenience, flexibility, and quality of IPTV compared to traditional cable or satellite services encourage more users to switch, thereby expanding the subscriber base and stimulating growth across regions.

Deploying and maintaining the infrastructure required for scalable, high‑quality IPTV — including servers, data‑centres, content delivery networks (CDNs), and high‑capacity broadband networks — demands substantial capital investment. In regions with limited broadband penetration, insufficient bandwidth, or unstable internet, streaming quality can degrade, leading to buffering or service interruptions. These factors discourage users from adopting IPTV in those regions, limiting market penetration. Additionally, smaller providers may struggle to compete due to high upfront costs, reducing overall market expansion.

The rollout of 5G and continued expansion of fiber broadband offer a significant opportunity for IPTV providers to deliver ultra-high-definition (4K/8K) content, low-latency live streaming, and enhanced interactive features such as multi-device streaming, catch-up TV, cloud DVR, and hybrid IPTV‑OTT services. As consumers increasingly prefer on-demand and flexible content consumption, IPTV providers can tap new segments — including mobile-first viewers, remote and rural subscribers, and smart-home users. Additionally, operators can differentiate their offerings with personalized content recommendations, targeted advertising, and bundled services, increasing ARPU and reducing churn.

Securing content licensing rights — especially for premium, global, or live content — remains complex and expensive, raising operating costs for IPTV providers. The digital nature of IPTV also makes it vulnerable to piracy and unauthorized streaming, undermining revenue potential and threatening content owner relationships. Moreover, regulatory environments differ widely across regions; compliance with local laws, content distribution rights, and data‑privacy regulations can lead to increased legal and operational overhead. These factors hinder the ability of providers to scale globally and maintain profitability while offering a broad, high-quality content library.

Expansion of 4K and 8K Streaming Capabilities: IPTV providers are increasingly offering ultra-high-definition content, with over 62% of new IPTV subscriptions including 4K or 8K options. The deployment of advanced video compression algorithms reduces bandwidth usage by up to 35%, enabling smoother streaming on existing broadband networks and improving overall customer satisfaction.

Integration of AI-Powered Personalization: More than 48% of IPTV platforms now implement AI-based recommendation engines, enhancing content discovery and viewer engagement. Personalized suggestions have resulted in a 25% increase in average viewing time per subscriber, while reducing churn by approximately 12% for platforms that actively use predictive analytics to tailor content.

Growth in Multi-Device Accessibility: IPTV services are expanding to support simultaneous streaming across smart TVs, smartphones, tablets, and gaming consoles. Current adoption indicates that 71% of households access IPTV content on two or more devices, improving user convenience and driving demand for flexible subscription packages across Europe, North America, and Asia-Pacific regions.

Adoption of Cloud-Based Content Delivery Networks (CDNs): Approximately 58% of IPTV operators have transitioned to cloud-CDN architectures to optimize video delivery, reducing latency by 28% and downtime by 15%. This trend is particularly strong in urban regions where high traffic volumes require scalable infrastructure capable of supporting millions of concurrent streams, enhancing reliability and performance.

The global IPTV market is divided into service types, application areas, and end-user categories to reflect diverse consumption patterns and delivery methods. Service types include live television multicast/broadcast, video-on-demand (VoD), hybrid IPTV–OTT bundles, and device-based applications. Applications span residential, hospitality, corporate/institutional, and mobile-first scenarios. End-users consist of households, hotels, enterprises, educational institutions, and mobile consumers. This segmentation allows providers to optimize infrastructure, content delivery, and subscription models according to user behavior and technology readiness. Variations in peak traffic, device compatibility, and content licensing influence growth rates across segments, guiding investment and strategic planning for operators.

Live IPTV multicast/broadcast is the leading type, representing approximately 45 % of subscriptions, due to its capacity to deliver linear channels to large audiences simultaneously. Video-on-demand services account for about 35 %, providing flexibility for on-demand content consumption. Hybrid IPTV–OTT bundles constitute roughly 15 % of services and are the fastest-growing type, driven by increasing demand for combined live and on-demand content. Device-based applications make up the remaining 5 %, catering to mobile-first users.

Residential streaming dominates, capturing around 60 % of IPTV usage, fueled by widespread household broadband and multi-device access. Hospitality and hotel entertainment is the fastest-growing application, driven by hotels offering live channels, VoD, and customized content to enhance guest experience. Corporate and institutional deployments, alongside mobile-first consumption, collectively account for 26 % of usage.

Households lead with approximately 70 % of IPTV subscriptions, supported by broadband availability and flexible viewing options. The hospitality sector is the fastest-growing end-user segment, meeting rising demand for premium in-room entertainment. Other end-users, including corporations, educational institutions, and public-sector accommodations, hold a combined 30 % share.

North America accounted for the largest market share at 33% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

In 2024, North America had approximately 45 million IPTV subscriptions, with the United States alone representing over 60% of these users. Europe followed with 25% of the global market share, while Asia-Pacific reached 28 million subscriptions, driven primarily by China, India, and Japan. Latin America accounted for 7% of global IPTV adoption, and the Middle East & Africa combined held 5%. Consumer adoption shows high urban penetration, with over 70% of North American households accessing IPTV via smart TVs or multi-device platforms. Peak streaming times average 3–5 hours daily per user, and broadband coverage in top-tier cities exceeds 90%, allowing reliable VoD and live channel delivery.

How is digital transformation shaping high-value IPTV adoption in enterprises and households?

North America represents 33% of global IPTV subscriptions, with the United States leading in both volume and infrastructure quality. Key industries driving demand include healthcare, finance, and hospitality, where high-definition live feeds and interactive content are essential. Regulatory support, such as net neutrality policies and broadband incentives, facilitates service expansion. Advanced digital transformation trends, including AI-based recommendation engines and cloud-based CDN deployments, are increasing user engagement and reducing latency by up to 28%. Local players such as AT&T have launched integrated IPTV bundles combining live TV, VoD, and OTT services across 10 million households. Consumer behavior indicates higher enterprise adoption in healthcare and finance, while residential subscribers increasingly prefer multi-device access and flexible subscription models.

What factors drive premium IPTV adoption across key European markets?

Europe holds approximately 25% of global IPTV subscriptions, with Germany, the UK, and France leading in penetration. Regulatory bodies enforce data protection and content licensing compliance, and sustainability initiatives encourage energy-efficient data centers for IPTV operations. Adoption of hybrid IPTV–OTT platforms and AI-driven personalization enhances service quality, with over 55% of households using multi-device IPTV access. Orange France recently upgraded its IPTV infrastructure to integrate cloud-based content delivery, reducing latency by 20% across urban networks. Consumer behavior in Europe reflects regulatory-driven demand for explainable content recommendations, energy-efficient service delivery, and high-quality VoD access.

How is technological expansion supporting IPTV demand in densely populated regions?

Asia-Pacific accounted for over 28 million IPTV subscriptions in 2024, ranking second globally in volume. Top-consuming countries include China, India, and Japan, with broadband coverage exceeding 75% in urban regions. Infrastructure expansion, including fiber-to-the-home networks and data centers, supports high-definition streaming and VoD services. Regional tech hubs are developing AI-based recommendation systems and adaptive streaming codecs. China Telecom and other local operators have upgraded IPTV networks to cloud-CDN architecture, reducing buffering by 30% for over 10 million subscribers. Growth is strongly driven by mobile-first consumption, e-commerce integration, and localized content tailored to regional preferences.

What is fueling IPTV adoption across Latin American households and enterprises?

South America holds roughly 7% of the global IPTV market, with Brazil and Argentina as the primary consumers. Expansion of broadband infrastructure and government incentives for digital media services are supporting IPTV deployment. Energy-efficient network solutions and regional content localization are increasing appeal to consumers. Telecom operators in Brazil have introduced IPTV packages combined with mobile internet and VoD, resulting in a 20% increase in average viewing hours. Consumer behavior is shaped by demand for localized media and language-specific content, driving service providers to customize offerings for regional audiences.

How are regional modernization and industry demand influencing IPTV adoption?

The Middle East & Africa region accounts for approximately 5% of global IPTV subscriptions, with the UAE and South Africa as major contributors. Demand is driven by sectors like oil & gas, hospitality, and urban residential housing. Technological modernization, including cloud-based delivery and fiber-optic expansion, supports high-definition streaming. Local regulations and trade partnerships facilitate infrastructure investment, and regional players have begun deploying hybrid IPTV–OTT platforms to enhance user experience. Consumers show strong interest in premium and interactive content, with mobile-first adoption increasing by 18% across urban centers.

United States – 22% market share; high end-user demand and advanced broadband infrastructure enable broad IPTV adoption.

China – 20% market share; substantial production capacity and large-scale infrastructure investment support extensive IPTV delivery.

The global Internet Protocol Television (IPTV) market remains moderately consolidated, with roughly 20–30 major active competitors globally and dozens of regional or niche providers. The top 5 companies together account for approximately 50–55% of global service offerings. These leading firms shape market positioning through aggressive expansion of infrastructure, strategic partnerships, and continuous technological innovation. Several providers are investing heavily in cloud‑native delivery platforms, CDN upgrades, and integrated IPTV–OTT solutions, underlining a shift from legacy broadcast to flexible, scalable IP‑based video ecosystems. For instance, some large operators have formed alliances to deploy cloud‑based video-processing and distribution platforms, optimizing low‑latency streaming and supporting multi‑DRM and dynamic ad insertion. Others have launched new IPTV service bundles that combine live channels, on‑demand libraries, and OTT content to enhance value propositions.

Innovation trends such as AI-driven content recommendation, adaptive bitrate streaming, edge‑CDN deployment, and hybrid IPTV–OTT architecture are intensifying competition. Firms are differentiating through user‑experience enhancements — reliability, reduced buffering, multi-device support, personalised content while smaller providers sometimes focus on regional or language‑specific niches. Despite competitive pressures, the market’s structure allows both large incumbents and agile smaller operators to coexist. Large players dominate with broad infrastructure and content access, while regional providers leverage local content licensing, targeted demographics, or bundled broadband services. These dynamics foster continuous innovation, competitive pricing, and service diversification, creating a competitive environment where service quality, technology, and content offerings become key differentiators.

Comcast Corporation

Deutsche Telekom AG

Orange S.A.

Huawei Technologies Co., Ltd.

Ericsson AB

Cisco Systems, Inc.

Vodafone Group Plc

China Telecom Corporation Limited

The Internet Protocol Television (IPTV) market is experiencing rapid technological evolution, driven by advances in network infrastructure, content delivery, and user experience optimization. Key enabling technologies include high-speed broadband networks, fiber-to-the-home (FTTH) deployments, and 5G mobile connectivity, which collectively support seamless streaming for over 70% of urban households in top-tier markets. Cloud-based content delivery networks (CDNs) are increasingly adopted, with approximately 58% of major operators leveraging cloud-CDN architectures to reduce latency by up to 28% and improve uptime by 15%.

AI and machine learning technologies are transforming user engagement through personalized content recommendations, predictive analytics for viewing behavior, and targeted advertising. Current adoption indicates that 48% of IPTV platforms integrate AI-powered recommendation engines, resulting in an estimated 25% increase in average viewing time per subscriber. Video compression and adaptive bitrate streaming technologies are enhancing bandwidth efficiency, allowing high-definition 4K and emerging 8K streaming without compromising quality, with over 62% of new IPTV subscriptions offering ultra-HD content options.

Emerging trends include hybrid IPTV–OTT platforms that combine linear broadcast, on-demand VoD libraries, and OTT services into a unified interface, as well as edge-computing deployments that reduce latency for millions of concurrent streams in urban centers. Interactive features such as multi-device streaming, cloud DVR, and live event synchronization are gaining traction, with mobile-first IPTV adoption rising by 18% in regions like Asia-Pacific. Operators are also investing in energy-efficient server infrastructure to meet ESG goals, targeting 20% reductions in data-center energy consumption by 2030, reflecting the increasing intersection of technology innovation and sustainable operations.

In 2024, Freely, a joint‑venture streaming platform, was officially launched — enabling UK broadband subscribers to stream live TV and on‑demand content without requiring an aerial or satellite dish. (TV Tech)

In 2023, Verizon Communications Inc. expanded its 5G Home Internet footprint into 20 new cities, boosting delivery of its IPTV services and improving streaming reliability for customers.

In 2024, several major IPTV providers globally upgraded their service portfolios to integrate cloud‑based content delivery and adaptive streaming, enabling higher-quality video and more scalable content distribution across devices.

In 2023, a telecom firm introduced a dedicated hotel‑focused IPTV solution supporting multilingual video‑on‑demand and in‑room interactive services, reflecting growing IPTV adoption within hospitality and enterprise segments.

The IPTV Market Report covers a comprehensive range of dimensions, offering a detailed examination of service types (such as live television multicast, video‑on‑demand, hybrid IPTV–OTT bundles, and device-based apps), transmission modes (wired, wireless, managed service, in‑house service), and device platforms (smart TVs, smartphones & tablets, PCs, set-top boxes and others). It analyses application areas across residential, hospitality, corporate/institutional and mobile-first usage, reflecting the diversity in consumer and enterprise demand. Geographic coverage spans major global regions — North America, Europe, Asia‑Pacific, Latin America, Middle East & Africa — enabling comparison of regional consumption patterns, infrastructure maturity, and regulatory environments. Technological aspects addressed include cloud‑CDN deployment, adaptive bitrate streaming, codec evolution, AI-driven personalization, multi-device support, hybrid IPTV–OTT integration, and emerging delivery standards. The report also examines industry focus areas such as content licensing practices, interactive services (cloud DVR, live pause/restart, multi-language support), bundling strategies with broadband or mobile services, and niche segments like hospitality entertainment systems. Through segmentation by type, application, end-user, technology and region, the report delivers strategic insights for operators, content providers, infrastructure vendors, and investors — offering a holistic view of current market structure, operational models, emerging opportunities, and technology-driven transformations within the IPTV landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 75574.27 Million |

|

Market Revenue in 2032 |

USD 181839.2 Million |

|

CAGR (2025 - 2032) |

11.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

AT&T Inc., Verizon Communications Inc., Comcast Corporation, Deutsche Telekom AG, Orange S.A., Huawei Technologies Co., Ltd., Ericsson AB, Cisco Systems, Inc., Vodafone Group Plc, China Telecom Corporation Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |