Reports

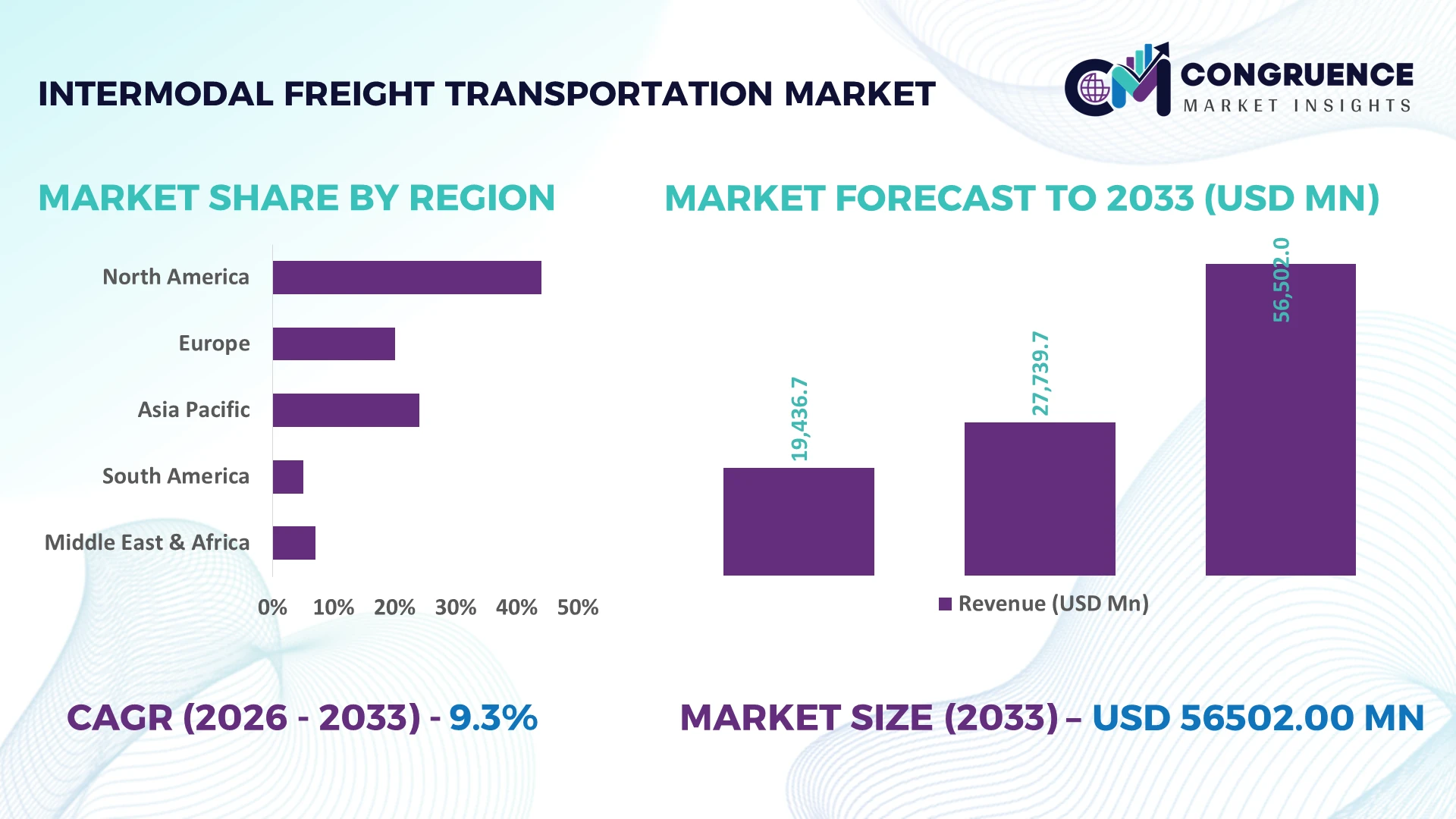

The Global Intermodal Freight Transportation Market was valued at USD 27739.74 Million in 2025 and is anticipated to reach a value of USD 56502 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033. Growth is driven by accelerated rail–road container integration, port automation, cross-border logistics modernization, and digital freight visibility platforms that improve asset utilization and reduce transit delays.

The United States remains the dominant market, handling approximately 38% of North America's intermodal freight volumes through an extensive Class I rail network, major container ports, and sustained infrastructure investments exceeding USD 100 billion. China continues to outperform in rail freight capacity with over 160,000 km of operational railway, supported by smart logistics hubs and cross-border Eurasian corridors. Continued Red Sea shipping disruptions in 2026 further strengthened demand for resilient multimodal routing and digital cargo orchestration across both countries.

Businesses prioritizing resilient, technology-enabled intermodal networks are positioned to strengthen supply-chain reliability while improving long-term logistics efficiency.

Market Size & Growth: USD 27,739.74 million (2025) to USD 56,502 million (2033) at 9.3% CAGR, supported by AI-enabled freight planning and multimodal supply-chain optimization.

Top Growth Drivers: Rail freight utilization +18%, containerized cargo +14%, digital freight visibility adoption +32%, strengthening global logistics efficiency.

Short-Term Forecast: By 2027, automated routing and terminal digitization reduce transit costs by 12% while improving delivery reliability by 15%.

Emerging Technologies: AI dispatching, IoT cargo tracking, and automated container terminals increase fleet utilization by nearly 20%.

Regional Leaders: North America exceeds USD 18 billion, Asia-Pacific surpasses USD 22 billion, Europe approaches USD 12 billion, driven by rail modernization and port automation.

Consumer/End-User Trends: Over 58% of large manufacturers integrate intermodal transportation into procurement strategies to improve supply-chain resilience.

Pilot/Case Example: In 2026, an automated inland logistics corridor improved container turnaround by 24% and reduced terminal congestion by 19%.

Competitive Landscape: Top operators control roughly 35% of organized capacity, with leading participation from J.B. Hunt, Union Pacific, Schneider National, CSX, and Norfolk Southern.

Regulatory & ESG Impact: Low-emission freight initiatives reduce logistics-related emissions by approximately 20% through greater rail-based transportation across strategic corridors.

Investment & Funding: More than USD 30 billion supports terminal expansion, automation, and public-private infrastructure partnerships amid ongoing regional supply-chain diversification.

Innovation & Future Outlook: Digital twins, predictive analytics, and autonomous yard operations accelerate next-generation intermodal ecosystems and network resilience.

Rising demand from e-commerce, automotive manufacturing, retail distribution, and industrial exports continues to reshape the Intermodal Freight Transportation Market. AI-powered route optimization, smart container monitoring, and automated terminal operations improve shipment visibility while increasing operational efficiency by nearly 22%. Ongoing trade corridor diversification and resilient logistics planning in response to evolving global supply-chain conditions are accelerating strategic investments, setting the foundation for the following strategic market discussion.

Intermodal freight transportation has become a strategic pillar for manufacturers, retailers, and logistics providers seeking resilient and cost-efficient supply chains. Ongoing supply-chain restructuring, trade route diversification, and infrastructure modernization are shifting freight from road-only operations toward integrated rail, port, and trucking networks. Digital freight platforms now enable real-time shipment visibility, while stricter transport emissions policies encourage higher utilization of rail-based corridors that lower fuel consumption and improve network reliability.

Technology adoption is reshaping operational performance. AI-enabled route optimization and predictive terminal scheduling reduce container dwell time by approximately 20% and lower empty container movements by nearly 15% compared with conventional dispatch systems. The United States leads in large-scale intermodal network deployment through extensive inland terminals, while Germany emphasizes highly automated freight hubs with digital customs integration and synchronized rail scheduling. Over the next two to three years, automated gate systems and predictive logistics platforms are expected to exceed 45% adoption across major freight corridors, improving asset utilization and shipment accuracy.

A practical example is the expansion of inland logistics parks connected directly to container ports, enabling faster cargo transfers between rail and trucking networks while reducing congestion. Companies are strengthening strategic partnerships with rail operators, terminal operators, and technology providers to expand integrated logistics ecosystems. Organizations that combine digital orchestration with modern intermodal infrastructure will secure stronger competitive positioning, greater operational resilience, and higher service reliability in increasingly complex global freight networks.

The strongest growth catalyst is the integration of digital freight management with expanding rail infrastructure, allowing logistics providers to optimize multimodal cargo movement while reducing transportation costs. AI-based planning improves route efficiency by nearly 18%, automated terminal operations increase container throughput by around 22%, and predictive maintenance reduces equipment downtime by approximately 16%. The United States continues investing in freight corridor modernization, while India is accelerating Dedicated Freight Corridor development to improve cargo velocity. These structural improvements are driving logistics companies to expand inland terminals, establish technology partnerships, and deploy real-time freight visibility platforms. The resulting operational flexibility strengthens service reliability, supports larger shipment volumes, and creates measurable competitive advantages across manufacturing and retail supply chains.

Uneven infrastructure quality and fragmented transport standards continue to constrain efficient intermodal deployment. Port congestion can increase cargo dwell times by more than 25%, while cross-border documentation requirements extend transit schedules by approximately 10–15% on selected trade routes. Limited rail connectivity in several developing economies further restricts seamless container transfers. These structural constraints increase operating costs, reduce fleet utilization, and complicate scheduling accuracy for logistics providers. Companies are responding by diversifying transport corridors, investing in inland distribution centers, negotiating long-term terminal access agreements, and deploying digital documentation platforms that reduce administrative delays. Strengthening interoperability has become a strategic priority for maintaining network efficiency and customer service consistency.

The next wave of opportunity lies in intelligent freight ecosystems combining AI, IoT-enabled containers, and automated logistics hubs. Smart asset tracking improves shipment visibility by nearly 30%, while digital documentation shortens customs processing by approximately 20%. Japan and Singapore continue investing in smart port technologies that integrate automated cranes, predictive cargo scheduling, and digital trade platforms. Logistics providers are expanding research partnerships, investing in cloud-based transportation management systems, and developing integrated multimodal control centers. A less obvious opportunity is the commercialization of predictive capacity marketplaces that dynamically allocate freight across rail, truck, and port assets, improving equipment utilization while reducing idle capacity throughout complex logistics networks.

The primary long-term challenge is coordinating highly connected transport ecosystems across multiple operators, technologies, and regulatory frameworks. System integration projects frequently require implementation periods exceeding 18 months, while cybersecurity incidents targeting logistics infrastructure have increased by more than 30% in recent years. Legacy software and inconsistent data standards continue to limit seamless information exchange between carriers, terminals, and customs authorities. Companies must strengthen cybersecurity architecture, modernize legacy transport management systems, and establish standardized digital interfaces through industry partnerships. Building scalable digital infrastructure alongside workforce training and operational governance will determine long-term competitiveness, service consistency, and the successful expansion of advanced intermodal freight transportation networks.

AI-Driven Network Optimization AI-enabled transport management platforms are reducing route planning time by nearly 35% while improving equipment utilization by approximately 18%. Rising shipment variability and persistent supply-chain disruptions are accelerating deployment across the United States and Germany. Logistics providers are integrating predictive analytics with real-time cargo visibility platforms, enabling faster dispatch decisions, lower empty-container movements, and stronger coordination between rail terminals, ports, and trucking fleets.

Terminal Automation Accelerates Throughput Automated gate systems, robotic container handling, and smart yard management have increased terminal productivity by around 22% while reducing truck turnaround times by nearly 17%. Labor availability challenges and expanding cargo volumes continue to drive investment in automation. Port operators are restructuring workflows, expanding digital partnerships, and standardizing operating systems to improve throughput without proportionally increasing infrastructure capacity.

Cross-Border Corridor Diversification Companies are shifting freight toward alternative rail and inland logistics corridors, reducing dependency on traditional maritime routes. Cross-border rail container traffic has expanded by approximately 14%, while multimodal corridor utilization has improved by nearly 19% following continued geopolitical shipping disruptions. Freight operators are strengthening regional partnerships, expanding inland distribution hubs, and redesigning transport networks to improve resilience against external trade shocks.

Low-Emission Freight Integration Sustainability targets are accelerating modal shifts toward rail-supported transport, lowering transport-related emissions by roughly 20% per shipment compared with long-haul road movement. Digital emissions reporting and fleet electrification initiatives are becoming standard procurement requirements. Logistics providers are expanding low-carbon service portfolios, investing in energy-efficient terminals, and integrating environmental performance metrics into customer contracts and operational planning.

Road-Rail remains the dominant segment because it delivers the strongest balance between transport flexibility, network scalability, and operating efficiency. Approximately 46% of intermodal freight movements across developed logistics markets rely on road-rail integration due to well-established rail corridors and extensive trucking connectivity. Companies continue expanding inland terminals, deploying digital scheduling platforms, and improving rail synchronization to reduce container dwell times by nearly 18%. Road-Sea maintains a significant role in international freight, particularly for export-oriented manufacturing, while Rail-Sea serves heavy industrial and bulk commodity supply chains requiring efficient port connectivity.

Multimodal is emerging as the fastest-growing type as enterprises increasingly seek integrated logistics orchestration across multiple transport modes. Digital freight platforms have increased multimodal shipment visibility by approximately 28%, encouraging greater investment in unified transport management systems. Road-Air continues supporting high-value and time-sensitive shipments, while Rail-Sea benefits from infrastructure modernization in industrial corridors. Logistics companies are strengthening carrier partnerships, expanding digital ecosystems, and prioritizing integrated freight planning to improve service reliability and operational flexibility across increasingly complex supply chains.

Container Shipping continues to dominate application demand because standardized containers simplify transfers across rail, road, sea, and terminal infrastructure while supporting global trade flows. More than 60% of organized intermodal shipments move through containerized transport, with automated container handling improving operational productivity by approximately 20%. Logistics companies are expanding smart container tracking, digital documentation, and terminal automation to strengthen shipment visibility. Bulk Cargo remains essential for mining, agriculture, and energy sectors, while Automotive Logistics benefits from synchronized inbound component deliveries supporting lean manufacturing operations.

E-commerce represents the fastest-growing application as fulfillment networks require rapid, predictable, and scalable freight movement between distribution centers. Shipment visibility adoption has increased by nearly 30%, while automated fulfillment integration has reduced delivery cycle times by approximately 16%. Retail Logistics continues expanding omnichannel distribution capabilities through advanced warehouse connectivity. Companies are investing in AI-driven transportation planning, integrated inventory systems, and strategic logistics partnerships to improve delivery precision while accommodating increasingly dynamic customer demand patterns.

Manufacturing remains the largest end-user because industrial production depends on predictable, high-volume freight movement across domestic and international supply chains. Around 40% of organized intermodal demand originates from manufacturing industries requiring continuous raw material inflows and finished goods distribution. Digital production scheduling has improved freight synchronization by approximately 18%, while integrated logistics planning has lowered inventory holding requirements by nearly 12%. Automotive manufacturers continue expanding just-in-time logistics partnerships, while Logistics Providers increasingly invest in technology-enabled multimodal service platforms.

Retail is the fastest-growing end-user as omnichannel commerce expands nationwide distribution networks and increases demand for flexible freight capacity. Retail logistics automation has improved order fulfillment efficiency by roughly 24%, encouraging broader deployment of integrated transport management platforms. Food & Beverage companies continue prioritizing temperature-controlled intermodal solutions to strengthen product quality during long-distance transportation. Logistics providers are responding with customized service offerings, long-term enterprise contracts, and digital ecosystem partnerships that improve shipment transparency, network responsiveness, and customer retention across multiple industry verticals.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 10.8% CAGR between 2026 and 2033.

Strategic Rail Modernization Strengthens Freight Networks

North America maintains the highest market concentration through an extensive rail freight network, advanced inland terminals, and integrated trucking infrastructure. The region accounts for approximately 36.8% of global intermodal activity, supported by high container throughput across major ports and widespread deployment of digital freight platforms. Automated terminal technologies have improved container handling productivity by nearly 21%, while predictive logistics systems continue reducing transit variability. Continued investment in inland logistics hubs and rail corridor upgrades enables stronger connectivity between ports, manufacturing clusters, and distribution centers. Enterprises are expanding long-term rail partnerships and adopting AI-enabled transport planning to improve network resilience, equipment utilization, and operational efficiency.

United States Market Outlook: The United States leads the regional market through the world's largest Class I freight rail network, advanced port infrastructure, and strong enterprise investment in multimodal logistics. More than 70 major inland intermodal terminals support nationwide freight distribution, while digital transportation management adoption exceeds 55% among large logistics operators. Manufacturers, retailers, and logistics providers continue investing in automated terminals, real-time cargo visibility, and integrated rail-road operations to strengthen supply-chain resilience and improve freight reliability.

Sustainable Freight Corridors Drive Network Transformation

Europe continues strengthening its intermodal freight ecosystem through rail modernization, digital customs integration, and low-emission transport initiatives. Approximately 28% of regional long-distance freight increasingly utilizes intermodal solutions as governments encourage modal shifts toward rail. Automated border processing and synchronized terminal scheduling have reduced selected cross-border freight delays by nearly 18%. Investments in trans-European freight corridors and smart logistics hubs continue improving cross-country cargo movement while supporting industrial competitiveness. Companies are expanding digital freight ecosystems and strengthening cooperation between rail operators, terminal operators, and logistics providers.

Germany Market Outlook: Germany remains Europe's operational hub due to its extensive rail infrastructure, advanced inland terminals, and central manufacturing position. More than 40% of the country's containerized inland freight utilizes integrated rail-road transport. Enterprise investment in digital freight coordination, automated cargo handling, and industrial logistics platforms continues improving supply-chain responsiveness for automotive, machinery, and export-oriented manufacturing sectors while reinforcing Germany's leadership in efficient multimodal freight deployment.

Infrastructure Expansion Accelerates Freight Scale

Asia-Pacific is experiencing the fastest operational expansion through large-scale infrastructure development, manufacturing growth, and logistics digitalization. Rapid deployment of inland logistics parks, smart ports, and high-capacity freight rail corridors continues strengthening regional connectivity. Containerized freight movements have increased by approximately 17% across key industrial economies, while automated terminal deployment has expanded by nearly 24%. Governments and enterprises continue investing in integrated transport corridors that connect ports with industrial manufacturing zones, improving cargo velocity and reducing logistics bottlenecks across export-driven supply chains.

China Market Outlook: China dominates regional deployment through extensive railway expansion, world-leading container ports, and highly integrated manufacturing clusters. The country operates over 160,000 kilometers of railway infrastructure while continuing investment in smart logistics hubs and automated container terminals. Logistics enterprises are strengthening AI-enabled freight coordination, expanding inland distribution networks, and integrating multimodal transport platforms to improve export efficiency, manufacturing competitiveness, and cross-border cargo movement.

Infrastructure Upgrades Support Trade Efficiency

South America continues improving intermodal freight capabilities through port modernization, rail rehabilitation, and logistics corridor development supporting agricultural and mining exports. Intermodal utilization has increased by approximately 13% across strategic export corridors, while container handling efficiency has improved by nearly 15% through terminal modernization initiatives. Infrastructure limitations remain in selected inland areas, encouraging governments and private operators to prioritize freight corridor investment and logistics partnerships. Companies continue expanding distribution networks and integrating digital transport management systems to improve operational consistency and export competitiveness.

Brazil Market Outlook: Brazil leads regional demand through its large agricultural exports, industrial production, and ongoing investment in rail-port integration. Freight operators continue expanding inland logistics terminals connecting farming regions with export ports, while digital shipment monitoring improves cargo visibility across long-distance transport corridors. Strategic investment in multimodal logistics infrastructure strengthens export capacity, lowers transportation complexity, and supports broader industrial competitiveness.

Strategic Logistics Infrastructure Expands Connectivity

The Middle East & Africa market is advancing through major logistics infrastructure investments, port expansion, and integrated trade corridor development. Smart port technologies and automated cargo operations continue increasing terminal productivity, with selected logistics hubs improving container processing efficiency by approximately 20%. Governments are prioritizing multimodal transport strategies linking ports, rail infrastructure, and industrial zones to strengthen international trade competitiveness. Private logistics providers are expanding technology partnerships and modernizing freight management systems to improve operational reliability and network integration.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's leading logistics gateway through advanced port infrastructure, free trade zones, and integrated multimodal transport networks. Continued expansion of rail connectivity and automated logistics facilities supports faster cargo transfers between maritime and inland transport systems. Enterprise investment in digital freight platforms, smart warehousing, and integrated customs processing strengthens regional distribution capabilities while reinforcing the country's strategic position in international freight movement.

The competitive landscape is led by J.B. Hunt Transport Services, Schneider National, Union Pacific, Norfolk Southern, and CSX, competing directly with regional intermodal operators, port logistics specialists, and digitally integrated freight providers. The top five companies collectively control approximately 34% of the organized market, while regional carriers compete through localized capacity and flexible service models. Competition centers on transit speed, network density, digital visibility, and pricing efficiency. AI-driven route optimization improves fleet utilization by nearly 18%, automated terminal operations reduce container dwell time by about 20%, and predictive scheduling lowers operational delays by approximately 15%. Leading operators are expanding inland terminals, forming rail-trucking partnerships, investing in smart logistics platforms, and strengthening end-to-end service integration through vertical coordination. The competitive shift increasingly favors technology-enabled logistics ecosystems over asset ownership alone, accelerating consolidation around digitally connected freight networks. High capital requirements, terminal infrastructure access, and interoperable technology platforms remain major entry barriers. Sustainable competitive advantage depends on integrated infrastructure, digital execution, reliable multimodal capacity, and superior operational responsiveness.

J.B. Hunt Transport Services

Schneider National

Union Pacific Railroad

Norfolk Southern Corporation

CSX Corporation

BNSF Railway

Canadian National Railway

Canadian Pacific Kansas City (CPKC)

CMA CGM

Maersk

DHL Supply Chain

DSV A/S

XPO Logistics

C.H. Robinson

Digital transformation is redefining intermodal freight operations through AI-powered transportation management systems, IoT-enabled cargo tracking, and cloud-based logistics orchestration. AI-driven planning improves route efficiency by approximately 18%, while IoT shipment monitoring reduces cargo exceptions by nearly 25%. Around 52% of large logistics enterprises have deployed integrated freight visibility platforms, enabling continuous monitoring across rail, road, sea, and terminal operations. Companies implementing unified digital ecosystems achieve faster decision-making and stronger network coordination than operators relying on fragmented legacy systems.

Automation is becoming the primary operational differentiator. Automated terminal equipment, robotic container handling, and predictive maintenance outperform conventional manual processes by reducing container turnaround time by nearly 22% and lowering maintenance costs by approximately 15%. Leading rail operators, global logistics providers, and major port authorities benefit most because integrated automation increases throughput without proportional infrastructure expansion. Digital twins further enhance terminal planning by simulating congestion scenarios before physical deployment, improving operational resilience.

Between 2026 and 2028, autonomous yard operations, blockchain-enabled freight documentation, and advanced predictive analytics will accelerate industry modernization. Adoption of intelligent scheduling platforms is expected to exceed 60% among major logistics enterprises, reducing cross-network delays and strengthening supply-chain synchronization. Companies investing early in interoperable digital platforms, cybersecurity, and AI-enabled logistics intelligence will secure measurable operational advantages, stronger customer retention, and superior competitiveness in increasingly connected intermodal freight ecosystems.

January 2025 J.B. Hunt expanded intermodal capacity investments, advancing its plan to grow its fleet toward 150,000 containers by 2027, representing over 40% growth from 2021 levels. The expansion strengthens customer flexibility, improves freight availability, and reinforces its North American intermodal leadership. Source: (J. B. Hunt)

December 2024 Union Pacific expanded intermodal infrastructure by opening the Phoenix Intermodal Terminal after identifying rising Southwest freight demand. The project followed more than USD 33 billion network investment over a decade, improving regional connectivity, terminal access, and containerized freight handling efficiency.

November 2025 DHL Global Forwarding launched an accelerated digitalization initiative to scale AI-powered logistics solutions and improve customer responsiveness. The transformation introduced organizational changes supporting digital deployment, strengthening predictive freight management capabilities and enhancing competitiveness across global transportation networks. Source: (DHL Group)

October 2024 Union Pacific invested in a new Kansas City Intermodal Terminal to expand Midwest freight connectivity, creating its fourth new intermodal ramp in recent years. The facility supports domestic and international container shipments, improving access to industrial markets and strengthening supply-chain efficiency. Source:

The Intermodal Freight Transportation Market Report covers comprehensive analysis across major types including Road-Rail, Road-Sea, Rail-Sea, Road-Air, and Multimodal systems, along with applications such as container shipping, bulk cargo, retail logistics, e-commerce, and automotive logistics. The study evaluates key end-users including manufacturing, automotive, retail, food and beverage, and logistics providers across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines technology adoption patterns including AI-based freight optimization, automated terminals, IoT tracking, digital documentation, and smart logistics platforms. It evaluates competitive positioning, infrastructure modernization, deployment trends, and strategic opportunities supporting business expansion. With more than 50% of leading logistics enterprises adopting integrated visibility solutions, the analysis helps companies identify investment priorities, partnership opportunities, operational improvements, and evolving market directions through 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 27739.74 Million |

Market Revenue in 2033 | USD 56502 Million |

CAGR (2026 - 2033) | 9.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | J.B. Hunt Transport Services, Schneider National, Union Pacific Railroad, Norfolk Southern Corporation, CSX Corporation, BNSF Railway, Canadian National Railway, Canadian Pacific Kansas City (CPKC), CMA CGM, Maersk, DHL Supply Chain, DSV A/S, XPO Logistics, C.H. Robinson |

Customization & Pricing | Available on Request (10% Customization is Free) |