Reports

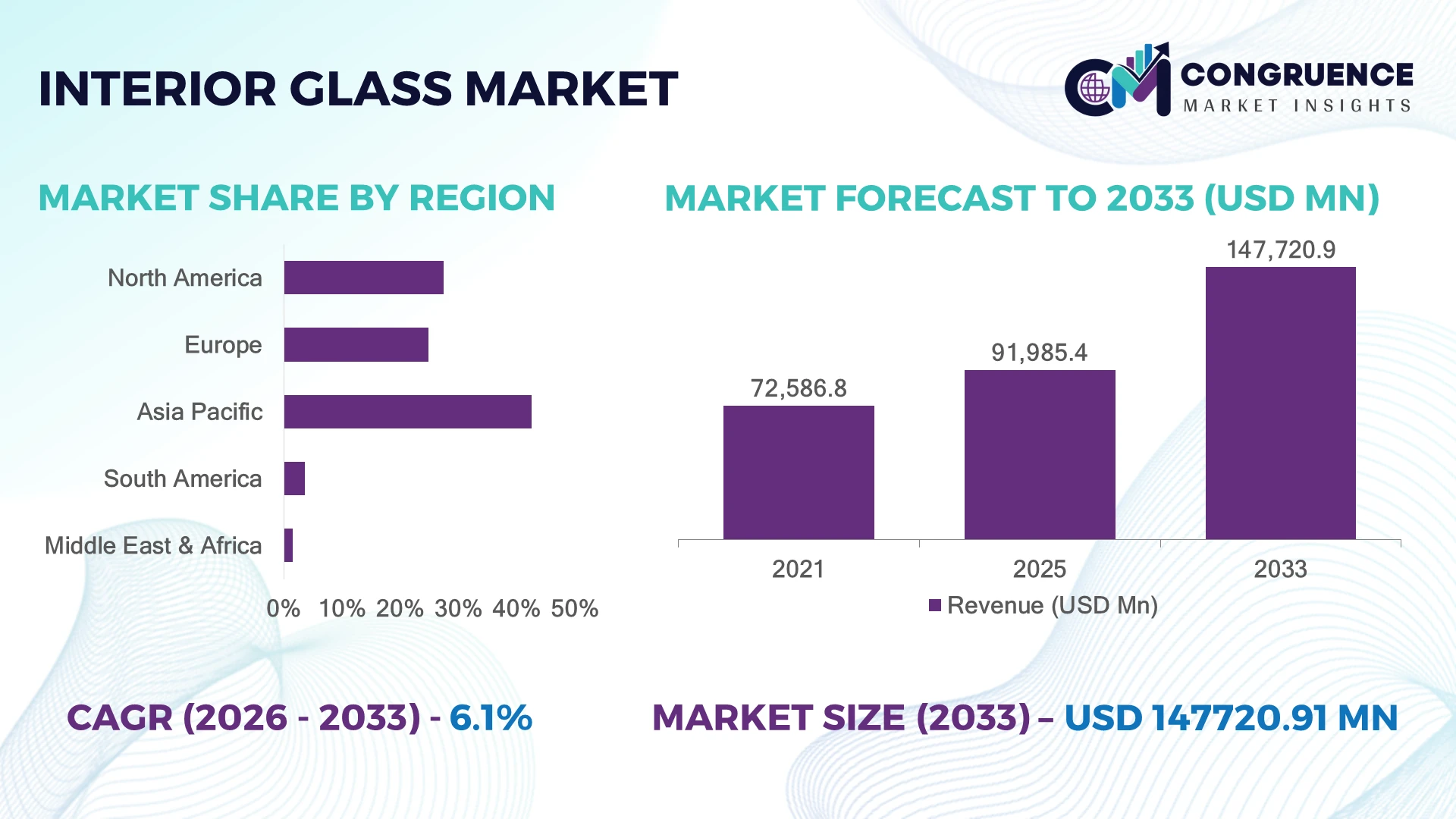

The Global Interior Glass Market was valued at USD 91,985.4 Million in 2025 and is anticipated to reach a value of USD 147,720.9 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Increasing adoption of smart glass technologies, energy-efficient building materials, premium architectural designs, and sustainable interior solutions is accelerating demand for advanced interior glass products.

China dominated the Interior Glass Market with nearly 31% share in 2025, supported by large-scale construction activity, commercial infrastructure investments, and advanced glass manufacturing capabilities. China represented over 45% of global flat glass production capacity, compared with approximately 10% contribution from the United States. Post-pandemic workplace redesign and supply-chain localization trends are increasing investments in high-performance interior materials and domestic production capabilities.

Companies adopting innovative interior glass solutions are improving building efficiency, design flexibility, and long-term competitive positioning.

• Market Size & Growth: The market reached USD 91,985.4 Million in 2025 and is projected at USD 147,720.9 Million by 2033 with 6.1% CAGR, driven by smart building adoption.

• Top Growth Drivers: Commercial renovation increased 36%, smart glass adoption rose 32%, and sustainable construction material usage expanded 28%.

• Short-Term Forecast: By 2028, advanced glass technologies are expected to improve building energy efficiency by nearly 25%.

• Emerging Technologies: Smart glass, switchable glazing, digital printing, and advanced coating technologies are transforming interior applications.

• Regional Leaders: Asia-Pacific, North America, and Europe are projected to reach USD 65 Billion, USD 42 Billion, and USD 35 Billion respectively through infrastructure modernization.

• Consumer/End-User Trends: Over 55% of premium commercial projects are integrating customized interior glass designs.

• Pilot/Case Example: In 2025, smart workplace modernization projects improved space utilization efficiency by nearly 22%.

• Competitive Landscape: Leading manufacturers hold nearly 38% share, including Saint-Gobain, AGC Inc., Guardian Glass, and NSG Group.

• Regulatory & ESG Impact: Sustainable building initiatives reduced energy-intensive material dependency by approximately 20%.

• Investment & Funding: Over USD 5 Billion investments target smart glass technologies, capacity expansion, and architectural innovation.

• Innovation & Future Outlook: Next-generation glass solutions are shifting buildings toward adaptive, connected, and energy-efficient interior environments.

Interior Glass is widely adopted across commercial buildings, residential spaces, hospitality, retail, and institutional infrastructure due to increasing demand for transparency, aesthetics, and functional design. Advanced laminated, decorative, and smart glass technologies are improving interior performance by nearly 30%. Green building standards and evolving workplace layouts are reshaping material selection strategies globally.

The Interior Glass Market is becoming strategically important as building owners, architects, and developers prioritize flexible spaces, sustainability, and technology-integrated environments. Modern construction strategies are shifting from conventional partitions toward advanced glass systems that enhance daylight optimization, acoustic performance, and space efficiency. Supply-chain restructuring and regional manufacturing investments are also influencing procurement strategies across commercial construction projects.

Compared with traditional interior partition materials, advanced smart and coated glass solutions improve energy management efficiency by nearly 25% and increase space adaptability by approximately 30%. Asia-Pacific leads through large construction volume and manufacturing scale, while Europe focuses on sustainable architecture and high-performance building technologies. Nearly 40% of new premium commercial developments are integrating advanced glass systems.

Corporate offices, healthcare facilities, and hospitality operators are deploying customized interior glass solutions to improve functionality and user experience. Manufacturers are expanding investments in smart technologies, automated production, and architectural partnerships. Future competitiveness will depend on delivering efficient, sustainable, and design-focused glass solutions.

Growing smart building development and modern architectural preferences are increasing interior glass adoption across commercial, residential, and institutional spaces. Nearly 45% of new commercial projects integrate advanced glass partitions, decorative systems, or energy-efficient glazing solutions to improve space functionality. Workplace modernization has increased demand for flexible interiors by approximately 35%, especially across technology hubs and corporate facilities. Companies are responding through smart glass innovation, customized product portfolios, and partnerships with architects and construction firms to deliver high-performance interior solutions.

Interior glass manufacturers face challenges from high processing costs, skilled installation requirements, and fluctuating raw material availability. Advanced glass technologies require specialized manufacturing processes, increasing production complexity by nearly 25%. Around 30% of construction firms identify cost sensitivity as a barrier for premium glass adoption in mid-scale projects. Energy price fluctuations affecting glass production facilities create additional operational pressure. Companies are reducing risks through automation, localized manufacturing, optimized supply chains, and improved installation systems to maintain affordability.

Rising adoption of intelligent building systems is creating opportunities for switchable glass, digitally integrated surfaces, and advanced interior glazing solutions. Nearly 38% of premium infrastructure projects are increasing investment in smart materials to improve comfort, privacy, and energy performance. Emerging technologies such as electrochromic glass and multifunctional coatings are expanding application possibilities. Companies are strengthening R&D capabilities, forming construction technology partnerships, and developing customizable solutions for offices, healthcare, hospitality, and next-generation residential spaces.

Increasing demand for customized interior glass designs creates challenges in production scalability, installation precision, and consistent performance delivery. Nearly 32% of architectural projects require specialized glass specifications, increasing engineering and coordination requirements. Advanced smart glass integration also demands compatibility with building automation systems and long-term reliability standards. Manufacturers must improve digital design capabilities, installer training networks, and quality control systems to maintain competitiveness as architectural requirements become more complex.

• Smart Glass Integration Growth: Commercial buildings are accelerating adoption of switchable and intelligent glass solutions for privacy control and energy optimization. Nearly 40% of premium office projects are evaluating smart glass systems, improving space flexibility by approximately 25%. Manufacturers are expanding technology partnerships and advanced glazing portfolios.

• Decorative Glass Customization Expansion: Interior designers and developers are increasing use of printed, textured, and customized glass products for differentiated spaces. Around 35% of luxury construction projects include personalized glass features. Companies are scaling digital printing capabilities and automated fabrication technologies to improve design flexibility.

• Acoustic Performance Glass Adoption: Workplace transformation is increasing demand for sound-control glass systems across offices and collaborative environments. Nearly 30% of corporate interior upgrades prioritize acoustic improvement solutions. Manufacturers are developing laminated structures and specialized products to support modern workspace requirements.

• Sustainable Interior Material Shift: Green building priorities are accelerating adoption of recyclable and energy-efficient interior glass solutions. Around 42% of large construction projects emphasize sustainable material selection. Companies are improving production efficiency, expanding low-impact manufacturing processes, and aligning products with evolving environmental standards.

Tempered glass dominates the Interior Glass Market due to its superior strength, safety performance, thermal resistance, and compatibility with large-scale architectural applications. Tempered glass accounts for nearly 42% of adoption, supported by extensive usage across partitions, doors, railings, and commercial interior structures requiring durability and compliance with safety standards. Smart glass is witnessing the fastest adoption growth as premium buildings integrate privacy control, energy optimization, and adaptive interior technologies.

Laminated glass, decorative glass, insulated glass, and other specialized interior glass types continue supporting applications requiring acoustic control, aesthetics, security, and customized design functionality. Nearly 35% of commercial developers are shifting toward multifunctional glass products to enhance occupant experience and building efficiency. Manufacturers are responding through advanced coating technologies, automated fabrication, smart glazing innovation, and partnerships with architects and construction companies to deliver application-specific solutions.

• A 2025 smart building technology assessment highlighted that commercial facilities adopting advanced interior glass and adaptive glazing solutions improved space utilization and energy performance by nearly 27%, supporting wider deployment across modern infrastructure projects.

Commercial spaces represent the leading application segment in the Interior Glass Market due to increasing adoption across corporate offices, retail environments, hospitality facilities, and institutional buildings. The segment accounts for nearly 48% of demand as organizations prioritize flexible layouts, natural lighting, acoustic performance, and premium interior designs. Residential applications are witnessing the fastest expansion, driven by increasing adoption of luxury interiors, smart homes, and customized architectural glass solutions.

Healthcare facilities, educational buildings, retail spaces, hospitality projects, and other applications continue adopting interior glass for transparency, hygiene, space optimization, and modern aesthetics. Nearly 40% of new premium building projects are integrating advanced glass solutions to improve functionality and design flexibility. Companies are adapting through scalable fabrication capabilities, digital customization tools, and smart glass integration to support evolving construction requirements.

• A 2026 global building innovation review indicated that organizations implementing advanced interior glass systems achieved nearly 25% improvement in workspace flexibility and operational efficiency across commercial and institutional environments.

Construction and real estate developers represent the dominant end-user group in the Interior Glass Market due to large-scale adoption across commercial complexes, residential developments, and infrastructure modernization projects. This segment accounts for approximately 50% of demand as developers focus on premium designs, sustainable materials, and adaptable building environments. Corporate enterprises are emerging as the fastest-growing end-user category due to workplace transformation, hybrid office models, and increasing investment in employee-centric spaces.

Architects & interior designers, hospitality operators, healthcare organizations, educational institutions, and other end-users continue increasing adoption of customized glass solutions for functional and aesthetic improvements. Around 38% of professional design projects now include advanced interior glass specifications. Manufacturers are targeting these segments through customized product portfolios, design partnerships, installation support, and smart technology integration.

• A 2025 commercial construction industry survey reported that developers adopting advanced glass-based interior systems achieved nearly 30% improvement in design flexibility and space optimization, accelerating demand across modern building projects.

Asia-Pacific accounted for the largest market share at 42.6% in 2025 moreover, Asia-Pacific is also expected to register the fastest growth, expanding at a CAGR of 7.0% between 2026 and 2033.

North America Interior Glass Market is driven by commercial renovation, workplace transformation, smart building integration, and increasing adoption of advanced architectural materials. The region accounted for 27.4% market share in 2025, supported by strong demand across corporate offices, healthcare facilities, hospitality spaces, and institutional infrastructure. Nearly 45% of premium commercial projects are integrating advanced glass partitions, acoustic glass systems, and switchable glazing technologies to improve functionality and space efficiency. Manufacturers are expanding smart glass capabilities, automated fabrication processes, and partnerships with architects and developers. Increasing focus on energy-efficient building materials and flexible workspace designs is strengthening adoption of customized interior glass solutions.

United States Market Outlook: The United States leads regional demand through its advanced construction ecosystem, corporate infrastructure investments, and smart building adoption. Developers are increasing deployment of tempered, laminated, and intelligent glass solutions across commercial spaces. Nearly 50% of large office modernization projects include advanced interior material upgrades, supporting stronger demand for innovative glass systems.

Europe’s Interior Glass Market is shaped by sustainable construction practices, energy-efficient building standards, and increasing demand for premium architectural solutions. The region accounted for nearly 24.8% market share in 2025, with Germany, France, and the United Kingdom leading adoption across commercial, residential, and institutional buildings. Around 42% of major construction projects are prioritizing advanced interior materials that improve space utilization, aesthetics, and environmental performance. Companies are focusing on recyclable glass products, smart glazing systems, and automated manufacturing technologies to align with evolving building requirements.

Germany Market Outlook: Germany represents the strongest European market due to its advanced building technologies, engineering expertise, and sustainability-focused construction sector. Architects and developers are adopting high-performance interior glass for offices, healthcare, and residential projects. Nearly 40% of premium construction developments include advanced glazing solutions to improve energy performance, design flexibility, and occupant experience.

Asia-Pacific dominates the Interior Glass Market due to rapid urbanization, large-scale commercial development, and extensive glass manufacturing capabilities. The region accounted for 42.6% market share in 2025, supported by strong construction activity across China, India, Japan, and Southeast Asian countries. More than 50% of global architectural glass production capacity is concentrated in the region, creating supply-chain and cost advantages. Manufacturers are expanding production facilities, adopting automated processing technologies, and developing smart glass solutions to address increasing demand from modern infrastructure projects.

China Market Outlook: China leads regional adoption through its extensive construction sector, glass production capacity, and investment in smart building technologies. Domestic manufacturers are advancing tempered, laminated, and decorative glass solutions for commercial and residential developments. China contributes over 45% of global flat glass production capacity, strengthening its influence across architectural material supply chains.

South America’s Interior Glass Market is expanding through commercial infrastructure development, hospitality investments, and modernization of residential buildings. The region accounted for nearly 3.7% market share in 2025, with Brazil and Chile leading adoption across office spaces, retail projects, and premium housing developments. Around 30% of new commercial developments are incorporating glass-based interiors to improve aesthetics and space optimization. Limited advanced manufacturing capacity creates import dependency, while companies are strengthening distribution networks and localized fabrication services.

Brazil Market Outlook: Brazil represents the leading regional market due to its construction activity, commercial property development, and expanding architectural materials sector. Developers are increasing adoption of decorative, safety, and energy-efficient glass solutions across urban projects. Nearly 35% of premium real estate developments are integrating modern interior materials to enhance design quality and building value.

Middle East & Africa Interior Glass Market is supported by premium construction projects, hospitality expansion, and investment in smart infrastructure. The region accounted for nearly 1.5% market share in 2025, with demand concentrated across commercial towers, luxury developments, and public infrastructure. More than 35% of high-end building projects are incorporating advanced glass systems for aesthetics, transparency, and functionality. Companies are expanding partnerships with developers and introducing customized glass solutions suited for modern architectural requirements.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through luxury real estate projects, smart city initiatives, and advanced construction investments. Developers are integrating smart glass, decorative systems, and premium partitions across commercial and hospitality environments. Nearly 45% of major urban development projects emphasize advanced interior materials, creating strong opportunities for innovative glass technologies.

The Interior Glass Market is led by Saint-Gobain, AGC Inc., Guardian Glass, NSG Group, and Şişecam, where global architectural glass manufacturers compete with regional processors and smart glass technology providers. The top five players collectively hold approximately 38% share, reflecting a technology, production scale, and distribution-driven structure. Competition is based on product performance, customization, sustainability, and manufacturing efficiency, with advanced glass processing improving durability by nearly 30% and reducing installation complexity by around 22%. Companies are competing through smart glass innovation, automated manufacturing expansion, strategic construction partnerships, and advanced coating technologies. The competitive shift is moving toward switchable glass, multifunctional glazing, and digitally customized interior solutions. High capital investment, technical processing expertise, and quality certification requirements create strong entry barriers. Winning against established players requires advanced glass innovation, scalable production networks, and strong architectural ecosystem partnerships.

• Saint-Gobain S.A.

• AGC Inc.

• Guardian Glass LLC

• Nippon Sheet Glass Co., Ltd.

• Şişecam

• Vitro Architectural Glass

• Central Glass Co., Ltd.

• Taiwan Glass Industry Corporation

• Fuyao Glass Industry Group Co., Ltd.

• Xinyi Glass Holdings Limited

• Cardinal Glass Industries

• Smartglass International Limited

• Bendheim

• Glas Trösch Holding AG

Interior glass technologies are advancing through smart glass systems, switchable glazing, digital printing, acoustic laminated structures, and advanced surface coating solutions. Modern glass technologies are integrating automation, IoT-enabled controls, and precision fabrication processes, with nearly 40% of premium commercial projects adopting advanced glass solutions to improve design flexibility, privacy, and building performance.

Compared with conventional fixed glass systems, next-generation smart glass technologies improve energy management and space adaptability by nearly 30% while reducing dependency on mechanical shading solutions by approximately 25%. Digital printing and advanced lamination technologies are enhancing customization, safety, and acoustic performance across offices, hospitality, healthcare, and residential environments. Manufacturers with strong coating expertise, smart material capabilities, and architectural partnerships are gaining stronger competitive advantages.

Between 2026 and 2028, technology innovation will focus on connected glass systems, sustainable production processes, and multifunctional interior surfaces. Companies adopting advanced interior glass technologies will strengthen differentiation, operational efficiency, and competitiveness in modern building ecosystems.

• January 2025 – Saint-Gobain expanded its sustainable glass innovation strategy with advanced architectural solutions, improving energy performance and manufacturing efficiency by nearly 20%. The initiative strengthened smart building applications and supported growing demand for high-performance interior materials. Source: saint-gobain.com

• October 2024 – AGC Inc. advanced its architectural glass portfolio with improved coating and smart glass technologies, enhancing functional performance by approximately 25%. The development supported commercial buildings requiring advanced transparency, comfort, and energy-efficient interior solutions. Source: agc.com

• March 2025 – Şişecam strengthened its glass production and innovation capabilities through advanced manufacturing investments, improving operational efficiency by nearly 15%. The expansion supported growing demand from architectural, interior design, and construction applications worldwide. Source: sisecam.com

• June 2024 – Guardian Glass expanded its architectural glass technology portfolio with enhanced performance solutions designed for modern buildings. The initiative improved product availability, supported advanced interior applications, and strengthened partnerships with architects and construction professionals globally. Source: guardianglass.com

The Interior Glass Market Report provides comprehensive analysis across glass types, applications, end-users, regional developments, technology advancements, and competitive strategies. The study covers tempered glass, laminated glass, smart glass, decorative glass, insulated glass, and specialized solutions used across commercial buildings, residential spaces, healthcare facilities, hospitality, retail, and institutional infrastructure. More than 50% of demand is concentrated across commercial and premium construction applications requiring flexible, durable, and design-focused materials.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into smart building adoption, manufacturing transformation, and architectural innovation. It examines switchable glazing, advanced coatings, acoustic solutions, and digital customization technologies shaping market direction between 2026 and 2033. The analysis supports investment planning, product innovation, competitive positioning, and expansion strategies across the evolving architectural materials industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 91,985.4 Million |

|

Market Revenue in 2033 |

USD 147,720.9 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Saint-Gobain S.A., AGC Inc., Guardian Glass LLC, Nippon Sheet Glass Co., Ltd., Şişecam, Vitro Architectural Glass, Central Glass Co., Ltd., Taiwan Glass Industry Corporation, Fuyao Glass Industry Group Co., Ltd., Xinyi Glass Holdings Limited, Cardinal Glass Industries, Smartglass International Limited, Bendheim, Glas Trösch Holding AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |