Reports

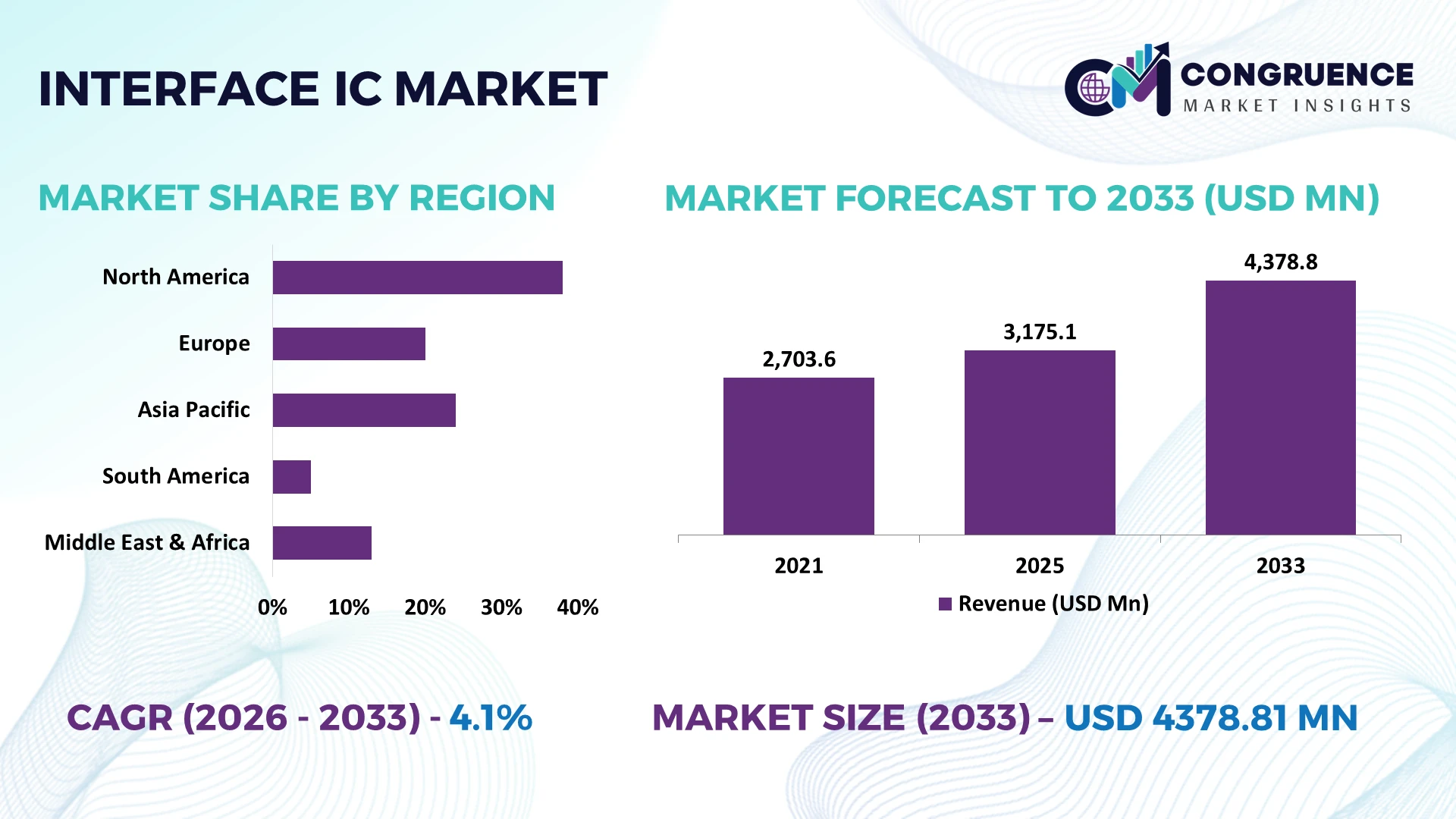

The Global Interface IC Market was valued at USD 3175.05 Million in 2025 and is anticipated to reach a value of USD 4378.81 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Growth is being accelerated by rapid deployment of high-speed automotive communication protocols, AI server connectivity, industrial automation, and next-generation consumer electronics requiring low-power, high-bandwidth interface solutions.

China remains the dominant country, accounting for approximately 34% of global electronics manufacturing capacity while expanding semiconductor investment through large-scale national initiatives. Automotive electronics, industrial equipment, and consumer devices continue driving Interface IC adoption, with advanced packaging utilization exceeding 60% across leading fabrication ecosystems. Compared with Japan's mature analog semiconductor base, China delivers significantly higher production scale, while ongoing technology restrictions continue reshaping global semiconductor supply chains during 2026.

Strategically, manufacturers should prioritize resilient regional supply networks, advanced interface technologies, and automotive-grade product portfolios to strengthen long-term competitive positioning.

Market Size & Growth: USD 3175.05 Million (2025) to USD 4378.81 Million (2033) at 4.1% CAGR, supported by AI infrastructure and automotive semiconductor integration.

Top Growth Drivers: Automotive electronics (+18%), industrial automation (+15%), and high-speed data connectivity (+22%) continue expanding advanced Interface IC deployment.

Short-Term Forecast: By 2027, high-speed interface solutions improve system efficiency by 14% while reducing signal latency across advanced electronic platforms.

Emerging Technologies: AI accelerators, PCIe Gen6, and chiplet architectures increase high-performance interface integration by over 20%.

Regional Leaders: Asia Pacific exceeds USD 2300 Million, North America approaches USD 950 Million, and Europe surpasses USD 700 Million through EV and industrial automation adoption.

Consumer & End-User Trends: More than 65% of new connected devices integrate advanced interface standards supporting higher bandwidth and lower power consumption.

Pilot/Case Example: In 2026, automotive communication platform upgrades improved data transfer efficiency by approximately 28% in intelligent vehicle systems.

Competitive Landscape: Leading suppliers collectively control nearly 45% of the global market, including Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, and Renesas Electronics.

Regulatory & ESG Impact: Energy-efficient semiconductor manufacturing reduces operational power consumption by nearly 12% while strengthening regional supply-chain resilience.

Investment & Funding: More than USD 8 Billion in semiconductor expansion investments supports regional fabrication, strategic partnerships, and advanced packaging capacity.

Innovation & Future Outlook: Next-generation chiplet connectivity, ultra-low-power interfaces, and automotive networking accelerate global product differentiation and long-term semiconductor competitiveness.

Interface IC Market demand is strengthening across electric vehicles, industrial robotics, AI servers, and advanced medical electronics where reliable high-speed communication is essential. Product innovation increasingly focuses on ultra-low-power, multi-protocol, and high-bandwidth interface solutions, with adoption of advanced connectivity standards rising by approximately 20%. Ongoing semiconductor supply-chain localization and regional manufacturing expansion continue shaping procurement strategies, setting the stage for deeper strategic market evaluation.

The Interface IC Market has become strategically important as semiconductor connectivity increasingly determines computing efficiency, automotive intelligence, and industrial automation performance. Rising investment in AI infrastructure, electric vehicles, and smart manufacturing is shifting competitive advantage toward companies capable of delivering reliable, high-speed interface solutions. Semiconductor supply-chain restructuring across the United States, Japan, and India is accelerating regional manufacturing diversification while reducing dependence on single-country sourcing for advanced electronic components.

Modern PCIe Gen6 and high-speed serializer/deserializer (SerDes) interface solutions deliver nearly 35% higher data throughput and reduce power consumption by approximately 18% compared with legacy interface architectures, enabling denser computing platforms and lower thermal loads. South Korea and Taiwan continue leading advanced semiconductor manufacturing and packaging, while India is expanding electronics production through fabrication incentives and assembly investments, creating a broader deployment ecosystem for Interface IC suppliers.

Automotive manufacturers integrating zonal electronic architectures are deploying multi-protocol Interface ICs to simplify wiring and improve data reliability across vehicle platforms. Semiconductor companies are expanding R&D partnerships, strengthening advanced packaging capabilities, and localizing production to improve supply resilience over the next two to three years, with AI-enabled devices expected to account for more than 30% of premium interface deployments. Companies that align technology roadmaps with resilient manufacturing and next-generation connectivity standards will secure stronger competitive positioning.

The rapid transition toward AI computing, software-defined vehicles, and industrial automation is strengthening demand for advanced Interface IC solutions. More than 70% of next-generation automotive electronic architectures now rely on high-speed communication interfaces, while industrial Ethernet deployments have increased by approximately 16% across advanced manufacturing facilities. Growing semiconductor localization initiatives in India and the United States are further supporting component availability and production resilience. In response, leading semiconductor companies are expanding automotive-qualified product portfolios, investing in low-power interface technologies, and forming ecosystem partnerships with processor and system manufacturers. This structural transition improves bandwidth, reduces signal integrity issues, and enables scalable electronic platforms for increasingly connected industries.

Advanced Interface IC production remains dependent on leading-edge wafer fabrication, specialty substrates, and advanced packaging technologies, creating persistent operational constraints. Packaging costs have increased by nearly 12% in recent years, while advanced-node manufacturing utilization frequently exceeds 85%, limiting production flexibility during demand surges. Export controls affecting semiconductor equipment continue influencing technology access in China, adding complexity to procurement and product qualification. To reduce operational exposure, manufacturers are diversifying supplier networks, expanding outsourced semiconductor assembly partnerships, and localizing selected production stages. These measures improve business continuity but require disciplined capital allocation and longer supplier qualification cycles before achieving stable deployment.

Growing AI infrastructure, industrial edge computing, and intelligent mobility platforms are creating high-value opportunities for advanced Interface IC suppliers. AI server deployments are expected to expand by more than 25% over the next few years, while demand for high-speed interconnect technologies continues rising across hyperscale data centers. Japan is accelerating advanced semiconductor R&D, supporting innovation in low-power and high-bandwidth interface architectures. Companies are responding through chiplet ecosystem development, strategic technology alliances, and expanded investment in multi-protocol interface portfolios supporting PCIe, USB, Ethernet, and automotive networking. Early participation in integrated connectivity ecosystems provides long-term design wins and strengthens customer retention across multiple electronic platforms.

Increasing electronic system complexity presents significant execution challenges for Interface IC suppliers as devices integrate multiple communication standards within compact architectures. Validation and interoperability testing account for nearly 20% of development cycles, while engineering costs for complex system integration have risen by approximately 15%. Automotive functional safety requirements and AI computing workloads further increase design verification demands, extending qualification timelines. Companies are investing in automated verification platforms, digital design tools, and collaborative engineering partnerships to improve interoperability and reduce deployment risks. Successfully addressing integration complexity will determine long-term competitiveness as customers prioritize scalable, secure, and standards-compliant connectivity solutions across mission-critical applications.

High-Speed Interface Standard Adoption Advanced computing platforms are rapidly shifting toward PCIe Gen6, USB4, and higher-bandwidth Ethernet interfaces, with deployment of high-speed connectivity solutions increasing by approximately 24% and latency reduced by nearly 18%. AI server expansion and data-intensive workloads are accelerating product redesign, prompting semiconductor companies to strengthen processor partnerships and optimize validation workflows for faster commercial deployment.

Automotive Network Architecture Evolution Software-defined vehicles are replacing distributed electronic control units with zonal architectures, reducing wiring complexity by nearly 30% while increasing high-speed interface integration by over 22%. Functional safety requirements and growing EV production are driving suppliers to develop automotive-grade Interface IC portfolios, expand long-term supply agreements, and localize manufacturing to improve delivery resilience.

Regional Manufacturing Diversification Semiconductor supply-chain restructuring is encouraging fabrication and assembly expansion across India, Japan, and the United States, reducing single-region sourcing dependence by roughly 15%. Government-backed manufacturing incentives and geopolitical trade adjustments are encouraging companies to diversify packaging operations, automate quality inspection, and establish regional engineering centers to improve production continuity and customer responsiveness.

Power-Efficient Integration Strategies Electronics manufacturers are integrating multiple communication protocols into single Interface IC platforms, lowering board space requirements by approximately 20% and reducing system power consumption by nearly 14%. This consolidation improves manufacturing efficiency while simplifying product design. Companies are responding through advanced packaging technologies, IP licensing partnerships, and greater investment in configurable interface architectures supporting multiple industrial applications.

Communication Interface ICs hold the largest share of approximately 41% due to their broad deployment across automotive electronics, AI servers, industrial automation, and networking equipment. Their ability to support multiple communication standards, deliver high-speed data transfer, and simplify system integration makes them the preferred choice for large-scale electronic platforms. Display Interface ICs remain a mature segment driven by high-resolution consumer devices, while Audio Interface ICs continue expanding across infotainment systems and professional electronics requiring improved signal quality.

Touch Interface ICs represent the fastest-growing segment as touch-enabled industrial equipment, automotive displays, and medical devices become increasingly interactive. Adoption of advanced human-machine interfaces has increased by nearly 19%, while integrated touch-controller designs reduce component count by approximately 15%. Semiconductor suppliers are introducing multi-function interface solutions, expanding product portfolios, and collaborating with display manufacturers to strengthen system compatibility. Investment priorities are shifting toward scalable, multi-protocol designs capable of supporting future connected devices with lower power requirements.

Consumer Electronics account for approximately 39% of Interface IC demand due to continuous product refresh cycles across smartphones, tablets, laptops, wearables, and smart home devices. High-volume manufacturing, increasing display resolution, and faster data transfer requirements sustain deployment of advanced interface technologies. Communication Devices remain another established application, while Healthcare Devices continue expanding through portable diagnostic systems requiring compact, low-power connectivity solutions.

Automotive Systems are the fastest-growing application as electric vehicles and software-defined architectures require reliable high-speed communication between sensors, processors, and control modules. Automotive Interface IC integration has increased by approximately 23%, while industrial equipment deployments have grown by nearly 16% through smart factory modernization. Companies are expanding automotive-qualified product lines, strengthening manufacturing partnerships, and optimizing application-specific designs to address rising demand across intelligent mobility and industrial automation markets.

Electronics Manufacturers represent the largest end-user group with an estimated 47% market share because of their extensive production of consumer electronics, networking equipment, industrial devices, and computing hardware. Their large procurement volumes, continuous product development, and demand for standardized interface solutions create sustained purchasing activity. Industrial Equipment Providers maintain stable demand through automation upgrades, while Healthcare Device Companies increasingly require specialized low-power Interface ICs for connected medical equipment.

Automotive Companies are the fastest-growing end-user segment as vehicle electrification and intelligent cockpit platforms significantly increase semiconductor integration. Automotive procurement of advanced Interface ICs has expanded by approximately 21%, while customized interface solutions have improved platform integration efficiency by nearly 17%. Suppliers are responding through long-term design partnerships, automotive-grade product customization, localized engineering support, and strategic ecosystem collaboration. Future demand is shifting toward application-specific solutions that deliver reliability, functional safety, and scalable connectivity across increasingly software-driven platforms.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a 4.8% CAGR between 2026 and 2033.

AI Infrastructure and Semiconductor Localization Drive Market Expansion

North America remains a strategic innovation hub for Interface IC development, supported by advanced semiconductor design capabilities, hyperscale data center expansion, and automotive electronics innovation. The region contributes approximately 24% of global demand, with the United States leading deployments across AI servers, cloud infrastructure, and industrial automation. Semiconductor manufacturing incentives continue strengthening domestic production, while leading enterprises expand advanced packaging and design operations. During 2026, multiple fabrication and packaging projects accelerated regional supply resilience, with advanced semiconductor capacity expected to increase by nearly 15% through ongoing infrastructure investments. Companies are prioritizing high-speed connectivity solutions, automotive-grade Interface ICs, and strategic technology partnerships to improve product availability and shorten customer qualification cycles.

United States Market Outlook: The United States remains the regional technology leader through its concentration of semiconductor design companies, AI infrastructure providers, and automotive innovation centers. More than 60% of North American semiconductor design activity is concentrated in the country, supporting continuous demand for advanced Interface IC solutions. Federal manufacturing incentives, expanding wafer fabrication projects, and growing AI computing deployments are encouraging suppliers to localize engineering resources, strengthen ecosystem partnerships, and accelerate next-generation product commercialization.

Automotive Electrification and Industrial Digitalization Strengthen Demand

Europe maintains a strong position through advanced automotive manufacturing, industrial automation, and high-value semiconductor engineering. The region represents nearly 21% of global Interface IC deployment, supported by widespread adoption of Industry 4.0 technologies and intelligent mobility platforms. Automotive electronics suppliers continue integrating high-speed communication interfaces to support software-defined vehicles and advanced driver assistance systems. Sustainability regulations are also encouraging energy-efficient semiconductor solutions across industrial equipment. Manufacturing modernization initiatives have improved smart factory deployment by approximately 18%, prompting Interface IC suppliers to expand collaborative engineering programs and strengthen partnerships with automotive and industrial equipment manufacturers.

Germany Market Outlook: Germany leads the European market through its globally competitive automotive industry, industrial automation expertise, and semiconductor research ecosystem. The country's advanced manufacturing base continues increasing deployment of industrial Ethernet and automotive communication Interface ICs, while digital factory investments have expanded connected production systems by approximately 20%. Domestic manufacturers are strengthening collaboration with semiconductor suppliers to improve product integration, production flexibility, and long-term supply reliability.

Manufacturing Scale and Electronics Production Leadership

Asia-Pacific remains the global production center for Interface IC manufacturing, accounting for approximately 48.6% of total market demand through its integrated semiconductor supply chain and extensive electronics manufacturing ecosystem. China, Taiwan, South Korea, and Japan collectively support large-scale wafer fabrication, assembly, packaging, and electronic device production. Advanced packaging utilization has surpassed 60% among leading manufacturers, while expanding AI hardware and automotive electronics production continues strengthening Interface IC deployment. Companies are increasing fabrication efficiency, diversifying supplier networks, and investing in higher-value semiconductor technologies to improve resilience against geopolitical trade disruptions and evolving customer requirements.

China Market Outlook: China continues leading regional demand through its extensive consumer electronics manufacturing, industrial automation expansion, and electric vehicle production. The country accounts for roughly one-third of global electronics manufacturing capacity, creating sustained procurement demand for Interface IC solutions. National semiconductor development initiatives, increasing automotive semiconductor integration, and expanding domestic production capabilities encourage suppliers to enhance localized manufacturing, strengthen research collaboration, and improve long-term supply security.

Industrial Modernization Supports Steady Adoption

South America represents an emerging Interface IC market where industrial modernization, automotive assembly, and telecommunications infrastructure upgrades continue supporting demand. Although regional production remains comparatively limited, electronics imports and localized assembly operations are increasing deployment across industrial equipment and consumer electronics. Smart manufacturing initiatives have improved connected equipment installations by approximately 14%, while regional technology partnerships are supporting broader semiconductor distribution networks. Companies are balancing expansion opportunities with logistics complexity, infrastructure limitations, and imported component dependence by strengthening distributor relationships and improving localized technical support for enterprise customers.

Brazil Market Outlook: Brazil remains the region's largest Interface IC market due to its diversified manufacturing base, automotive assembly operations, and expanding telecommunications sector. Industrial modernization projects continue increasing semiconductor content across production facilities, while electronics assembly activity supports stable procurement volumes. Government-backed digital transformation initiatives and growing investment in automation technologies are encouraging international semiconductor suppliers to expand distribution partnerships and strengthen application engineering capabilities within the country.

Digital Infrastructure Investment Expands Technology Deployment

The Middle East & Africa market is advancing through large-scale digital infrastructure projects, industrial diversification, and smart city investments. Although the region represents a comparatively smaller share of global Interface IC demand, deployment continues expanding across telecommunications, industrial automation, healthcare equipment, and intelligent infrastructure. Digital transformation initiatives have increased connected infrastructure deployment by approximately 17%, while investments in advanced manufacturing and technology parks are strengthening long-term semiconductor demand. Companies are responding through regional partnerships, technical support expansion, and localized distribution strategies to improve market accessibility and customer engagement.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through industrial diversification initiatives, digital infrastructure expansion, and increasing investment in advanced manufacturing. Smart city projects, data center development, and industrial automation programs are accelerating demand for reliable Interface IC technologies. Technology infrastructure investments continue expanding connected industrial deployments, while international semiconductor companies are strengthening local partnerships, technical training programs, and enterprise engagement to support long-term adoption across strategic sectors.

The Interface IC Market is led by Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, and Renesas Electronics, competing against regional semiconductor suppliers and specialized interface solution developers. Global technology leaders challenge cost-focused Asian manufacturers, while OEM-aligned suppliers compete with independent chip vendors for automotive, industrial, and AI infrastructure design wins. The top five players collectively control approximately 46% of the market through broad product portfolios and long-term customer relationships. Competition is driven by interface speed, power efficiency, packaging capability, and supply-chain reliability rather than pricing alone. High-speed interface products deliver nearly 20% lower power consumption, while advanced packaging reduces footprint by approximately 15%, creating measurable differentiation. Companies are expanding localized engineering, forming processor ecosystem partnerships, investing in chiplet-compatible architectures, and vertically integrating selected packaging operations. The competitive shift favors platform-based connectivity solutions over standalone components, increasing switching costs for customers. Entry barriers include advanced design expertise, qualification cycles, and manufacturing access. Winning requires superior interoperability, resilient supply networks, faster product validation, and application-specific innovation.

Texas Instruments

Analog Devices

Infineon Technologies

STMicroelectronics

Renesas Electronics

NXP Semiconductors

Microchip Technology

onsemi

ROHM Semiconductor

Toshiba Electronic Devices & Storage Corporation

MaxLinear

Diodes Incorporated

Silicon Laboratories

Skyworks Solutions

Current Interface IC innovation is centered on high-speed connectivity, ultra-low-power operation, and multi-protocol integration. PCIe Gen6, USB4, high-speed Ethernet, and advanced SerDes technologies are replacing legacy interface architectures, increasing data throughput by approximately 35% while reducing power consumption by nearly 18%. More than 60% of newly designed AI servers and premium automotive electronic platforms now integrate these advanced interface standards, enabling higher bandwidth, improved signal integrity, and simplified board design. Semiconductor suppliers benefit through stronger design wins and longer product lifecycles across computing, industrial automation, and intelligent mobility applications.

Emerging technologies include chiplet-based architectures, silicon photonics integration, and advanced packaging that combine multiple communication protocols within compact devices. Compared with conventional discrete interface solutions, integrated multi-protocol Interface ICs reduce board space requirements by approximately 20% while improving system reliability. Adoption continues accelerating among automotive manufacturers, hyperscale data center operators, and industrial equipment providers seeking greater scalability, lower thermal loads, and simplified manufacturing workflows.

Between 2026 and 2028, AI edge computing, software-defined vehicles, and industrial digitalization will accelerate demand for configurable, software-enabled Interface IC platforms. Companies investing early in advanced packaging, chiplet interoperability, automated validation, and ecosystem partnerships will strengthen competitive differentiation, shorten customer qualification cycles, and secure strategic positions in next-generation electronic system architectures.

February 2024 Analog Devices expanded its long-term manufacturing partnership with TSMC through JASM in Japan, securing wafer capacity for 40nm and finer process nodes to strengthen supply resilience for high-performance interface and connectivity solutions serving automotive and industrial markets. Source: analog.com

January 2026 Texas Instruments introduced an expanded automotive semiconductor portfolio featuring chiplet-ready processors delivering up to 1200 TOPS AI performance alongside new Ethernet PHY and radar technologies, accelerating advanced vehicle connectivity and reinforcing leadership in automotive interface ecosystems. Source: ti.com

February 2026 Renesas Electronics and GlobalFoundries expanded a multi-billion-dollar manufacturing collaboration to strengthen U.S. semiconductor production capacity, improving long-term supply resilience for chips supporting smart vehicles, industrial automation, and high-performance connectivity applications. Source: renesas.com

May 2026 Analog Devices agreed to acquire Empower Semiconductor for USD 1.5 billion, expanding integrated voltage regulator technology for AI computing platforms and strengthening system-level power delivery capabilities supporting next-generation high-performance semiconductor architectures.

This report provides a comprehensive assessment of the Interface IC Market by evaluating technology evolution, competitive positioning, deployment patterns, and strategic industry developments between 2026 and 2033. The analysis covers four product categories, five major application segments, and four end-user groups, supported by detailed assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It also examines semiconductor manufacturing trends, interface protocol evolution, automotive electronics integration, AI infrastructure, industrial automation, and advanced packaging technologies.

The report evaluates adoption trends, procurement strategies, regional manufacturing capabilities, and innovation priorities across leading semiconductor companies. It highlights changing deployment patterns, including increasing multi-protocol integration and expanding automotive and AI-driven applications, while assessing competitive dynamics, technology roadmaps, supply-chain resilience, and investment priorities. The insights support expansion planning, portfolio optimization, product positioning, partnership evaluation, and long-term strategic decision-making across the evolving Interface IC ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3175.05 Million |

Market Revenue in 2033 | USD 4378.81 Million |

CAGR (2026 - 2033) | 4.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, Renesas Electronics, NXP Semiconductors, Microchip Technology, onsemi, ROHM Semiconductor, Toshiba Electronic Devices & Storage Corporation, MaxLinear, Diodes Incorporated, Silicon Laboratories, Skyworks Solutions |

Customization & Pricing | Available on Request (10% Customization is Free) |