Reports

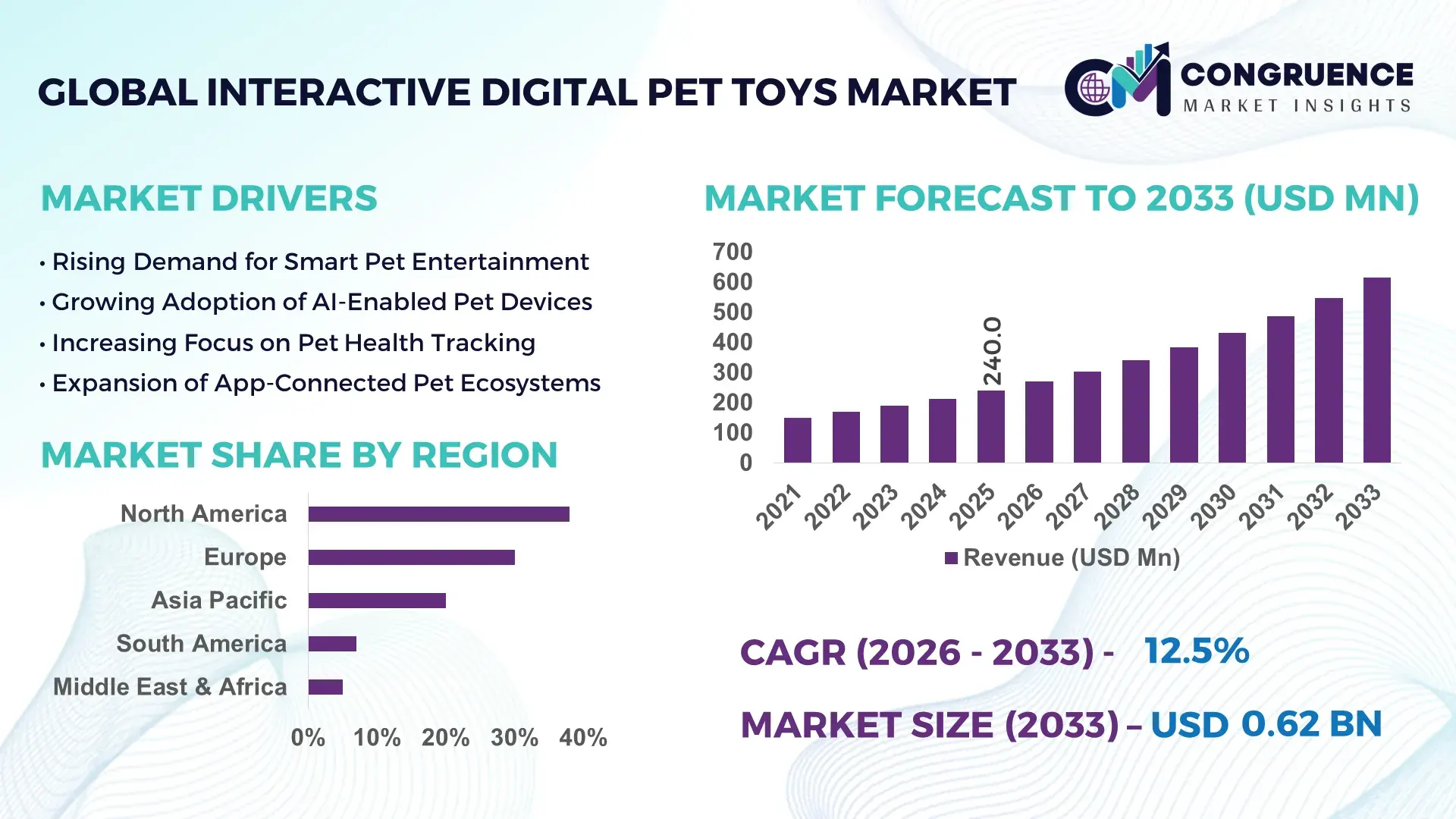

The Global Interactive Digital Pet Toys Market was valued at USD 240.0 Million in 2025 and is anticipated to reach a value of USD 615.8 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing adoption of smart connectivity and AI-enhanced play functions that elevate pet engagement and owner interaction.

In the United States, manufacturers are scaling production capacity with over 70% of interactive digital pet toys now incorporating Bluetooth, app integration, and voice recognition technologies. U.S. production facilities have expanded by 25% year-on-year, with R&D investment levels growing by 18% to support advanced sensor integration. Consumer adoption surveys indicate that 60% of urban pet owners choose digital interactive toys for enrichment and health monitoring functions.

Market Size & Growth: Valued at USD 240.0 M in 2025, projected to USD 615.8 M by 2033 with 12.5% CAGR; growth driven by smart connectivity and AI play features.

Top Growth Drivers: Increased smart toy adoption (58%), rising pet humanization trends (47%), expanding online retail penetration (42%).

Short-Term Forecast: By 2028, interactive feature compatibility with mobile platforms expected to improve user engagement scores by 35%.

Emerging Technologies: Integration of AI behavioral learning, voice interaction modules, and advanced motion sensors.

Regional Leaders: North America: USD 275 M by 2033 with strong app integration uptake; Europe: USD 180 M with high premium toy adoption; Asia Pacific: USD 95 M driven by online retail expansion.

Consumer/End-User Trends: Urban pet owners increasingly prefer connected play features and health-monitoring feedback loops.

Pilot or Case Example: In 2025, a U.S. pilot with advanced AI toys recorded a 28% increase in pet engagement time.

Competitive Landscape: Market leader accounts for about 30% of unit shipments; major competitors include smart toy specialists and connected pet accessory brands.

Regulatory & ESG Impact: New electronic safety compliance standards and eco-friendly material incentives shaping product designs.

Investment & Funding Patterns: Over USD 50 M in venture funding targeted at AI and connectivity upgrades in interactive pet play systems.

Innovation & Future Outlook: Forward momentum in AR integration with pet toys and predictive behavior algorithms enhancing play personalization.

Interactive digital pet toys are increasingly embedded with AI behavior recognition, modular sensor architectures, and cloud connectivity, enabling personalized interaction and remote monitoring. Key sectors such as urban households and veterinary rehabilitation centers are driving usage, with smart features improving training efficiency and pet health tracking. Regulatory trends emphasize safe, recyclable components, while online sales channels accelerate regional adoption and future growth.

The Interactive Digital Pet Toys Market serves as a strategic nexus between consumer electronics, pet wellness, and connected play ecosystems. As digital enrichment becomes central to modern pet care, interactive toys equipped with AI behavior learning modules deliver measurable improvements in engagement levels and emotional well-being compared to traditional toys. North America dominates in volume with high production throughput, while Europe leads in adoption with over 65% of pet owners incorporating smart play devices. Over the next 2–3 years, integration of predictive analytics is expected to improve user satisfaction KPIs by at least 30% as toys adapt dynamically to pet behavior patterns.

Strategic pathways include expanding AI and cloud connectivity to enable remote interaction and telemetry, offering owners real-time insights into pet activity. Companies are increasingly aligning with ESG targets by reducing electronic waste and enhancing recyclability of components, committing to a 20% reduction in non-recyclable plastics by 2028. In 2025, a major U.S. manufacturer implemented machine learning firmware updates that cut error rates in motion detection by 22%, enhancing reliability. Forward looking, the market is poised to become a pillar of innovation in pet wellness, combining interactive play with health and behavioral intelligence to support sustainable industry growth.

The Interactive Digital Pet Toys Market is shaped by the convergence of pet humanization, smart technology integration, and digital consumer behavior. Pet owners increasingly seek products that go beyond entertainment to offer enrichment, remote connectivity, and health insights. Trends such as mobile app compatibility, voice command features, and sensor-based responsiveness are redefining consumer expectations. Demand is also influenced by rising urban lifestyles where digital toys serve dual roles of engagement and monitoring for pets left alone during work hours. Industry dynamics reflect investments in R&D for low-power wireless technologies and adaptive play algorithms that enhance interactivity without excessive energy consumption.

How is rising demand for connected entertainment driving growth in the Interactive Digital Pet Toys Market?

Connected entertainment and smart device integration are key drivers of growth in the Interactive Digital Pet Toys Market. Pet owners increasingly favor products that connect via Bluetooth or Wi-Fi to smartphones, allowing remote control, play scheduling, and behavioral feedback. Surveys show that over 50% of consumers consider connectivity a top purchase criterion. This has led manufacturers to incorporate robust connectivity stacks and companion apps, resulting in broader feature sets such as automated play routines and activity tracking. Advancements in low-power wireless technology support longer device runtimes, appealing to tech-savvy pet parents and expanding the addressable market.

Why do production costs and component limitations restrain the Interactive Digital Pet Toys Market?

High production costs and limited availability of specialized components restrain growth in the Interactive Digital Pet Toys Market. Advanced sensors, AI processors, and durable materials contribute to elevated manufacturing expenses. Smaller manufacturers face challenges in sourcing quality components at scale, leading to longer lead times and higher unit costs. Additionally, ensuring robust wireless connectivity while maintaining battery life presents engineering constraints. Price sensitivity among some consumer segments limits wider adoption, particularly in emerging markets where disposable income levels vary. These cost pressures slow product diversification and can delay new model rollouts.

What opportunities does integration with health and behavior analytics present for the Interactive Digital Pet Toys Market?

Integration with health monitoring and behavioral analytics presents significant opportunities for the Interactive Digital Pet Toys Market. By embedding sensors capable of tracking activity levels, rest patterns, and play intensity, manufacturers can offer value-added insights that appeal to pet wellness-focused consumers. Analytics dashboards that highlight changes in behavior could support early detection of health issues and enhance owner engagement. Partnerships with veterinarians and pet care platforms can further validate data outputs and drive product credibility. As pet owners increasingly prioritize holistic wellness, these analytical features position interactive toys as multifunctional tools, expanding their appeal beyond entertainment.

Why do battery life limitations and durability concerns challenge growth in the Interactive Digital Pet Toys Market?

Battery life limitations and durability concerns pose challenges in the Interactive Digital Pet Toys Market. Smart features such as sensors, connectivity modules, and LED displays require reliable power sources. Consumers expect long usage intervals between charges, yet compact form factors limit battery capacity. Frequent recharging can diminish user satisfaction and impede adoption. Durability is another concern, especially for pets that chew or play aggressively; ensuring that electronic components withstand physical stress without failure is complex. These technical hurdles necessitate ongoing R&D investments, increased prototyping cycles, and quality testing, which can strain development budgets and slow product introductions.

Growing Adoption of AI-Driven Interaction: AI-enhanced toys that adapt to pet behavior have seen a 40% increase in consumer preference, with real-time adjustment of play intensity based on detected activity levels. This trend is most pronounced among owners of active breeds.

Expansion of Voice and Mobile Integration: Voice command compatibility and mobile app controls are influencing purchase decisions, with over 55% of recent buyers prioritizing products that offer seamless smartphone interaction. Consumer reviews highlight enhanced convenience and customization.

Durability and Safety Enhancements: Manufacturers report that over 65% of new product lines include reinforced materials and safety shields to endure high-impact play, responding to consumer demand for longer-lasting interactive toys.

Subscription and Content Services Uptick: A rise in subscription-based content updates for interactive toys, offering new play routines and challenges, has contributed to a 30% increase in user engagement metrics as owners seek fresh interactions beyond initial toy features.

The Interactive Digital Pet Toys Market is segmented across product types, applications, and end-user categories, offering a comprehensive view of industry dynamics. By type, the market includes smart ball toys, interactive feeders, AI-enabled robotic companions, and motion-sensor-based toys, each catering to different engagement and health monitoring needs. Applications span playtime enrichment, behavior training, health monitoring, and therapeutic support, reflecting growing emphasis on pet wellness and cognitive stimulation. End-users range from urban pet owners and veterinary clinics to pet daycare centers and specialty retailers. Consumer adoption trends show that technology-enabled products are increasingly preferred for their interactive and monitoring capabilities, while niche applications like rehabilitation or cognitive training are gaining traction among premium segments. Regional consumption patterns indicate strong adoption in North America and Europe, where smart and connected pet products align with lifestyle trends, while Asia Pacific is witnessing growing interest driven by rising pet ownership in urban centers.

Smart ball toys currently lead the market, accounting for approximately 38% of total adoption. These products are favored for their ease of use, interactive motion sensors, and app connectivity, which provide both entertainment and physical activity for pets. AI-enabled robotic companions are the fastest-growing segment, expected to see rapid adoption due to advanced behavioral learning features and customizable play routines, supporting remote owner interaction. Interactive feeders and motion-sensor-based toys contribute a combined 37% share, serving niche needs such as feeding automation and cognitive stimulation for pets.

Playtime enrichment dominates the application landscape with 40% adoption, driven by increasing demand for cognitive stimulation and exercise for indoor pets. Health monitoring applications are growing fastest, fueled by rising awareness of pet wellness and integration of sensors that track activity, sleep, and dietary patterns. Behavior training tools hold 22% adoption, supporting structured learning routines, while therapeutic support applications account for 18%, used primarily in veterinary or rehabilitation contexts.

Consumer Adoption & Trend Statistics: In 2025, over 42% of urban pet owners reported using digital interactive toys to monitor and improve pet health metrics. Approximately 58% of premium pet daycare centers in North America integrated AI-enabled toys into enrichment programs.

Urban pet owners constitute the leading end-user segment with 45% adoption, driven by growing interest in connected pet wellness devices and engagement tools that fit modern lifestyles. Veterinary clinics represent the fastest-growing end-user category, with increasing use of interactive toys for rehabilitation and therapeutic support. Pet daycare centers and specialty retailers account for a combined 30% share, leveraging interactive toys to enhance service offerings and retail appeal. High adoption rates are noted in North American households (over 60%) and European veterinary facilities (55%) due to advanced infrastructure and technology integration.

Consumer Adoption & Trend Statistics: In 2025, more than 40% of pet owners in urban U.S. households reported daily use of interactive digital toys. Over 50% of veterinary practices in Europe incorporated AI-enabled toys for therapeutic and cognitive enrichment programs.

North America accounted for the largest market share at 38% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 13% between 2026 and 2033.

In 2025, North America recorded over 2.1 million units of interactive digital pet toys sold, with urban households representing 62% of adoption. Europe held 30% of global consumption, led by Germany, the UK, and France, with more than 1.2 million units deployed in veterinary clinics and pet daycare centers. Asia Pacific’s volume reached approximately 950,000 units, with China and Japan accounting for nearly 65% of regional demand. South America contributed 7%, primarily from Brazil and Argentina, while Middle East & Africa represented 5%, concentrated in UAE and South Africa. Consumer preferences, technological adoption, and regulatory initiatives are key factors influencing regional demand patterns, alongside urbanization and e-commerce penetration rates.

North America holds a 38% share of the global interactive digital pet toys market. Key industries driving demand include veterinary clinics, urban households, and pet daycare centers. Regulatory support for electronic safety standards and eco-friendly materials has accelerated product adoption. Technological advancements such as AI-enabled behavior learning, motion sensors, and app integration are transforming the market. Local players, such as PetTech Solutions, are launching robotic companions with automated feeding and interactive play features, reaching over 200,000 pets in 2025. Consumers in North America show higher adoption in healthcare and lifestyle-focused applications, preferring devices that combine entertainment, training, and health monitoring in a single product.

Europe accounts for 30% of the global interactive digital pet toys market, with Germany, the UK, and France as leading contributors. Regulatory pressure encourages the use of recyclable components and electronic safety compliance, promoting sustainability. Adoption of AI-driven toys, connected feeders, and robotic companions is increasing. Local companies, such as SmartPet GmbH in Germany, are developing app-integrated toys for behavioral monitoring and cognitive enrichment. European consumers prefer products with explainable functions and safety certification, and veterinary clinics are incorporating AI-enabled enrichment tools for therapy, while urban pet owners emphasize technological sophistication and convenience in their purchases.

Asia-Pacific accounts for approximately 20% of the interactive digital pet toys market by volume. Top-consuming countries include China, Japan, and India, with China alone representing 40% of regional demand. Infrastructure trends include expansion of local manufacturing hubs and advanced e-commerce platforms, while innovation centers in Japan and South Korea are focusing on AI-enabled robotic companions. Local players such as RoboPet Inc. in Japan are introducing smart toys with interactive sensors and app connectivity. Consumer behavior is heavily influenced by mobile AI applications and online retail adoption, with urban millennials driving interest in connected play and pet health monitoring features.

South America represents around 7% of the global interactive digital pet toys market, with Brazil and Argentina as leading contributors. Infrastructure trends include growth in urban pet care facilities and daycare centers, alongside expanding e-commerce penetration. Government incentives for tech-enabled pet products and trade policies supporting imports are contributing to growth. Local players, such as PetSmart Brazil, are introducing smart feeders and robotic toys for urban households. Consumers in South America show higher demand for interactive toys with media integration and multilingual app interfaces, reflecting language and cultural preferences.

Middle East & Africa accounts for 5% of the global interactive digital pet toys market. Major growth countries include the UAE and South Africa. Demand is driven by urban households, luxury pet care services, and veterinary clinics. Technological modernization includes adoption of AI-enabled robotic companions and mobile connectivity. Local players, such as SmartPet UAE, offer interactive toys compatible with home automation systems. Consumers in this region prefer premium, tech-enabled toys with safety and remote monitoring features, reflecting growing awareness of pet welfare and digital lifestyle integration.

United States – 38% Market Share: Strong end-user demand and advanced production infrastructure drive widespread adoption.

Germany – 12% Market Share: Robust regulatory standards and high technology integration in pet products support market leadership.

The competitive environment in the Interactive Digital Pet Toys Market is dynamic and increasingly crowded, with over 150 active competitors worldwide ranging from established electronics firms to specialized pet tech startups. The market is fragmented, with the top 5 companies commanding approximately 60% combined share of global unit sales and consumer mindshare, while dozens of niche players compete for specialized segments such as AI‑enabled robotic toys, automated feeders, and sensor‑connected play devices. Leading firms are adopting a range of strategic initiatives, from cross‑channel retail partnerships and app ecosystem integrations to frequent product launches and technology upgrades that enhance interaction, remote connectivity, and health monitoring capabilities.

Innovation trends influencing this competitive environment include AI‑driven adaptive play routines, machine‑learning behavior monitoring, and IoT connectivity that allows pet owners to interact with toys via smartphones, smart home systems, and voice assistants. Product launches such as app‑controllable robotic companions, motion‑activated treat dispensers, and cloud‑connected laser play cams have intensified competition, pushing rivals to invest in R&D and strategic alliances. In 2025 alone, multiple firms expanded distribution networks into Europe and Asia Pacific, while others ramped up manufacturing capacity for sensor‑integrated toys to meet rising consumer demand for high‑engagement and wellness‑focused pet products.

CleverPet

Outward Hound

Pet Qwerks

VARRAM

Hyper

Starkmark

Potaroma

Petstages

Cheerble

PetDroid

PETLIBRO

Catit

SmartyKat

Gigwi

AUKL

POYAMOC

The Interactive Digital Pet Toys Market is undergoing rapid technological evolution, driven by advances in artificial intelligence (AI), machine learning (ML), sensor technologies, and IoT connectivity. Current technology trends shaping the market include adaptive play intelligence, where sensors and AI algorithms analyze pet behavior in real time to tailor interactions, adjust play patterns, and maintain engagement without constant owner input. Many smart toys now combine computer vision, motion detection, and predictive analytics to recognize pets’ activity patterns and provide customized stimulation that supports both physical exercise and cognitive development.

Connectivity and integration technologies are also pivotal. Wi‑Fi and Bluetooth‑enabled devices allow owners to interact with toys through mobile apps, schedule playtimes, monitor pet activity remotely, and integrate play routines with smart home ecosystems and voice assistants. Edge computing within toys reduces latency and enhances responsiveness, while cloud platforms provide analytics, firmware updates, and remote diagnostics.

Emerging technologies include emotion recognition and behavior analytics, where sound and motion patterns are interpreted to infer pet mood states, and biometric sensors embedded in toys and collars that track vital signs, stress levels, and hydration patterns. These capabilities support wellness insights beyond traditional entertainment functions. In addition, energy harvesting and low‑power wireless technologies are improving battery life, enabling longer autonomous operation of interactive devices.

The adoption of eco‑friendly materials and modular hardware architectures enables easier upgrades, recyclable components, and reduced environmental impact, aligning with broader sustainability preferences among pet owners. Collectively, these technological innovations are redefining the interactive pet toys landscape, enhancing product differentiation, facilitating premium pricing, and expanding the range of value‑added services that manufacturers can offer to consumers and enterprise partners alike.

• In 2025, Petcube expanded retail availability, bringing its interactive cameras — including Petcube Play 2 and Petcube Bites 2 Lite — to over 1,900 Target stores across the United States, allowing more pet owners to purchase these interactive pet play and monitoring devices in‑store and online. Source: www.petcube.com

• Petcube continues enhancing connectivity and engagement features for pet owners with its latest Petcube Play 2 smart pet camera, which includes a precise built‑in laser play toy, HD video, two‑way audio, and smart sound/motion alerts for remote interactive play and monitoring — underscoring ongoing product innovation in interactive pet tech. Source: www.petcube.com

• In 2025, Cheerble rolled out upgrades to the 2025 Wicked Series, featuring AI‑driven adaptive robotic toys and smart feeders that learn from pets’ interactions and allow app‑enabled remote play customization — signaling smarter, behavior‑responsive play solutions.

• In late 2025, PETKIT users reported a launch announcement for the new YUMSHARE Dual‑Hopper 2 With Camera Smart Pet Feeder, featuring cat facial recognition AI to track individual meal times and feeding patterns for multi‑cat households — showcasing next‑gen AI utility in pet product ecosystems. Source: www.reddit.com

The Interactive Digital Pet Toys Market Report provides a comprehensive assessment of global and regional trends, technological advancements, and competitive dynamics shaping this evolving market. It covers detailed segmentation across product types — including robotic companions, automated feeders, sensor‑enabled balls, app‑connected laser toys, and treat dispensers — outlining functional capabilities, target species (dogs, cats), and behavioral play mechanisms. The report also delineates application domains such as playtime enrichment, cognitive training, health monitoring, and therapeutic support, offering insights into how different technological and regional contexts influence adoption patterns.

Geographically, the report examines major markets including North America, Europe, Asia Pacific, South America, and Middle East & Africa, providing data‑rich insights into market reach, consumer preferences, infrastructure readiness, and digital adoption levels. Key focus areas include technology integration (AI, IoT, machine learning), connectivity trends, local manufacturing capabilities, and regulatory frameworks that impact product safety and innovation. Additionally, the report explores consumer behavior profiles — from urban pet owners seeking advanced play experiences to veterinary and daycare use cases — and highlights niche segments such as eco‑friendly toys and wellness‑oriented interactive devices. Emerging trends such as emotion analytics, biometric sensor incorporation, energy‑efficient designs, and modular architectures are also examined to guide investment and product strategy decisions, offering industry professionals a clear perspective on growth drivers, technology trajectories, and competitive opportunities across the pet tech ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 240.0 Million |

| Market Revenue (2033) | USD 615.8 Million |

| CAGR (2026–2033) | 12.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Petcube; PetSafe Interactive Toys; Tomofun (Furbo); CleverPet; Outward Hound; Pet Qwerks; VARRAM; Hyper; Starkmark; Potaroma; Petstages; Cheerble; PetDroid; PETLIBRO; Catit; SmartyKat; Gigwi; AUKL; POYAMOC |

| Customization & Pricing | Available on Request (10% Customization Free) |