Reports

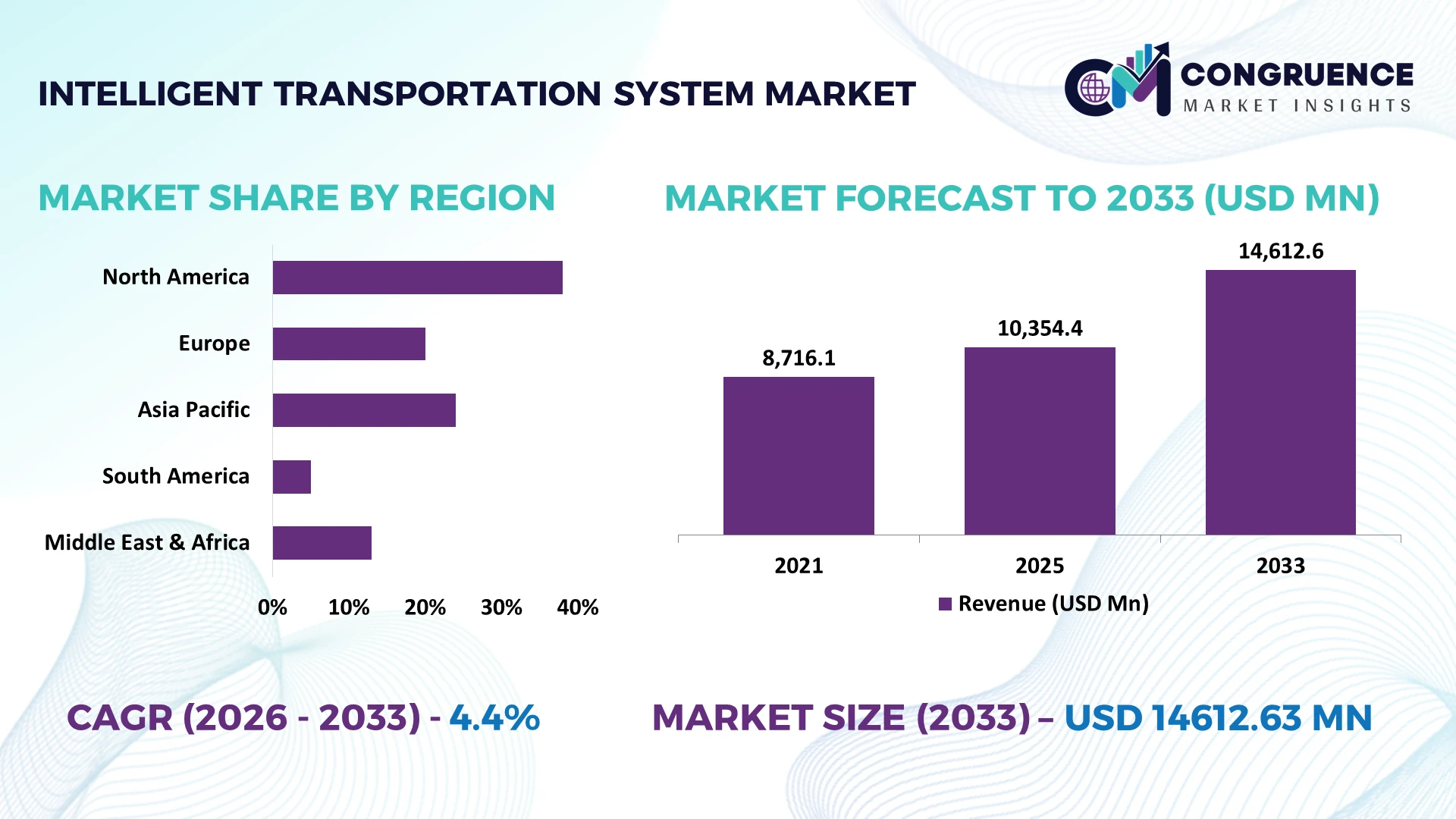

The Global Intelligent Transportation System Market was valued at USD 10354.39 Million in 2025 and is anticipated to reach a value of USD 14612.63 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Growth is driven by expanding AI-powered traffic management, connected mobility infrastructure, vehicle-to-everything (V2X) deployment, and public investment in smart urban transportation networks that improve traffic flow, safety, and operational efficiency.

China remains the dominant market, accounting for approximately 32% of global intelligent transportation infrastructure deployment through large-scale smart city investments and nationwide expressway digitalization, while the United States leads in connected mobility software and V2X innovation with over 75 metropolitan ITS programs. Ongoing infrastructure modernization and resilient transport planning accelerated after global logistics disruptions and geopolitical supply-chain realignment strengthened investment priorities across advanced economies.

The market favors technology providers capable of delivering interoperable, cybersecurity-focused, and scalable transportation platforms aligned with long-term national infrastructure strategies.

Market Size & Growth: USD 10354.39 million in 2025, reaching USD 14612.63 million by 2033 at a 4.4% CAGR, supported by AI-enabled traffic optimization and connected infrastructure expansion.

Top Growth Drivers: AI traffic analytics improve traffic efficiency by over 25%, V2X deployment expands above 20%, and smart highway investments increase nearly 18% across key economies.

Short-Term Forecast: By 2028, intelligent traffic control systems reduce average congestion delays by approximately 15% while improving corridor efficiency by nearly 20%.

Emerging Technologies: AI, edge computing, digital twins, and V2X communications accelerate predictive traffic management and automated incident response across high-growth transport networks.

Regional Leaders: Asia-Pacific exceeds USD 5.8 billion through smart city deployment, North America approaches USD 3.9 billion with connected mobility adoption, and Europe surpasses USD 3.2 billion through sustainable transport modernization.

Consumer/End-User Trends: More than 60% of metropolitan transport agencies prioritize real-time mobility analytics and integrated passenger information platforms.

Pilot/Case Example: A 2026 smart corridor deployment improved travel-time reliability by approximately 22% while reducing intersection delays by nearly 18%.

Competitive Landscape: Leading suppliers collectively control roughly 38% of the market, with Siemens, Thales, Kapsch TrafficCom, Cubic, and Iteris strengthening digital mobility portfolios.

Regulatory & ESG Impact: Smart traffic optimization lowers urban transport emissions by nearly 12% while supporting stricter digital infrastructure and road safety regulations.

Investment & Funding: More than USD 9 billion in public and private infrastructure investments support regional expansion, strategic partnerships, and intelligent mobility modernization.

Innovation & Future Outlook: Next-generation AI orchestration, cloud-native traffic platforms, and autonomous mobility integration strengthen resilient transportation ecosystems amid evolving global supply-chain priorities.

Intelligent Transportation System Market demand is expanding across smart highways, urban traffic management, connected public transit, and logistics optimization. AI-enabled predictive control, edge analytics, and digital twin platforms improve network performance, with operational efficiency gains exceeding 20% in advanced deployments. Accelerated infrastructure modernization and stricter mobility regulations continue to reinforce scalable intelligent transportation investments, setting the foundation for the strategic discussion.

The Intelligent Transportation System Market has become strategically important as governments and enterprises prioritize resilient mobility infrastructure, digital traffic management, and connected transport ecosystems. Infrastructure modernization, stricter road safety regulations, and supply-chain restructuring following recent logistics disruptions are accelerating investment in integrated traffic platforms. Intelligent transport solutions now support competitive differentiation by reducing congestion, improving asset utilization, and enabling real-time operational visibility across urban corridors and freight networks.

AI-enabled adaptive traffic management processes traffic events up to 35% faster than conventional signal control while reducing average intersection delays by nearly 20%, lowering operating costs for transport authorities. China continues deploying intelligent highway infrastructure at a larger scale, whereas Germany emphasizes interoperable mobility platforms and sustainability-focused urban transport integration. Over the next two to three years, connected intersection deployments are expected to expand by more than 25% across major metropolitan networks as vehicle-to-everything communication and edge analytics become standard components of intelligent mobility strategies.

A practical example is the deployment of integrated traffic management platforms combining roadside sensors, connected cameras, and predictive analytics to dynamically optimize signal timing during peak traffic periods. Companies are increasing investments in software-defined transportation platforms, cybersecurity capabilities, and ecosystem partnerships with telecom operators and infrastructure providers to strengthen deployment efficiency. Organizations establishing scalable, interoperable, and data-driven mobility solutions will secure stronger competitive positioning while supporting long-term transportation resilience and operational excellence.

Rapid deployment of intelligent mobility infrastructure is transforming transportation operations through AI-driven traffic optimization, connected sensors, and vehicle-to-everything communication. Intelligent signal control improves traffic throughput by approximately 25%, while predictive analytics reduces incident response times by nearly 30% and lowers urban congestion by around 18%. India and China continue expanding smart corridor projects under national infrastructure modernization programs, encouraging technology integration across highways and metropolitan transport systems. In response, leading companies are expanding digital platform portfolios, forming telecom partnerships, and investing in cloud-native traffic management solutions. The structural shift from isolated traffic systems toward interoperable digital mobility ecosystems is creating sustainable operational advantages and stronger public-sector procurement opportunities.

Fragmented transport infrastructure and incompatible communication standards remain major barriers to large-scale deployment. Nearly 45% of municipal traffic systems still depend on legacy control equipment, while integration expenses can increase project implementation costs by approximately 20%. The United States and several emerging economies face inconsistent interoperability across multiple infrastructure vendors, slowing modernization timelines and limiting operational scalability. These constraints reduce procurement efficiency, delay digital transformation, and increase long-term maintenance requirements. Companies are mitigating these issues by adopting open architecture platforms, localizing component sourcing, negotiating long-term technology contracts, and developing standardized software interfaces that improve compatibility while lowering lifecycle integration costs.

The strongest opportunity lies in AI-enabled mobility ecosystems integrating autonomous traffic control, digital twins, and predictive infrastructure management. Smart analytics can improve transport network efficiency by over 22%, while predictive maintenance lowers infrastructure servicing costs by nearly 18%. Japan is accelerating deployment of intelligent roadside infrastructure supporting connected mobility and automated transport services through national digital infrastructure initiatives. Companies are expanding research partnerships, investing in edge computing, and developing integrated mobility platforms that combine real-time analytics with cloud connectivity. An emerging strategic advantage comes from unified mobility data platforms that enable transport authorities to optimize freight movement alongside passenger traffic within a single operational environment.

Expanding connected transportation networks significantly increases cybersecurity exposure and deployment complexity. More than 60% of intelligent transportation platforms now exchange real-time operational data across multiple stakeholders, while connected infrastructure endpoints continue growing by over 20% annually. Singapore and the United States are strengthening cybersecurity requirements for critical transportation infrastructure, increasing compliance obligations for technology providers. Companies must simultaneously address secure interoperability, workforce shortages in intelligent mobility engineering, and large-scale system integration without disrupting existing transport operations. Organizations investing in zero-trust security architecture, resilient cloud infrastructure, workforce development, and standardized integration frameworks will achieve more reliable deployments and stronger long-term competitive resilience.

AI-Driven Traffic Intelligence AI-enabled traffic orchestration is becoming a standard operational capability, with adaptive signal systems improving intersection throughput by approximately 25% and reducing average travel delays by nearly 18%. Digital infrastructure mandates in China and the United States are accelerating deployment, prompting technology providers to expand AI software portfolios, integrate edge computing, and establish long-term partnerships with telecom operators for real-time network optimization.

Cloud-Based Mobility Integration Transportation agencies are replacing isolated control platforms with cloud-native mobility ecosystems, reducing infrastructure maintenance costs by around 20% while improving multi-agency data exchange efficiency by approximately 30%. Increasing demand for interoperable transport management following supply-chain disruptions is driving vendors to restructure software architectures, strengthen cybersecurity frameworks, and scale subscription-based intelligent transportation platforms across metropolitan networks.

Connected Freight Network Expansion Logistics operators are integrating intelligent transportation platforms with fleet management systems, improving route utilization by nearly 17% and lowering fuel consumption by approximately 12%. India is expanding smart freight corridors to improve cargo movement efficiency, encouraging companies to automate dispatch operations, deploy predictive traffic analytics, and collaborate with digital infrastructure providers to improve end-to-end transportation visibility.

Predictive Infrastructure Monitoring Highway authorities are increasing deployment of IoT-enabled roadside monitoring systems capable of reducing infrastructure inspection time by about 35% while improving maintenance planning accuracy by approximately 28%. Aging transportation assets and stricter operational compliance requirements are encouraging infrastructure operators to adopt predictive maintenance platforms, automate asset monitoring, and strengthen partnerships with sensor and analytics technology providers.

Advanced Traffic Management represents the leading segment, accounting for approximately 36% of market deployment due to its ability to optimize traffic flow, reduce congestion, and integrate seamlessly with AI-based analytics platforms. Transport authorities prioritize these systems because adaptive traffic control improves corridor efficiency by nearly 25% while reducing signal coordination delays by around 20%. Advanced Traveler Information is emerging as the fastest-growing segment as connected mobility applications and real-time navigation services become integral to urban transportation planning. Companies continue investing in scalable software platforms, cloud integration, and predictive analytics to strengthen operational performance.

Advanced Public Transport maintains strategic importance by improving passenger scheduling and multimodal connectivity, while Commercial Vehicle Systems are expanding through intelligent freight monitoring and compliance automation. Advanced Transportation Pricing is gaining traction where congestion management and electronic road pricing policies are strengthening. Vendors are increasing partnerships with infrastructure operators, expanding interoperable product portfolios, and developing modular deployment models to address varying transport network requirements while improving lifecycle cost efficiency.

Traffic Management leads the application landscape with an estimated 39% share because urban congestion reduction and network optimization remain the highest priorities for transportation agencies. AI-driven traffic coordination improves intersection capacity by approximately 24% while reducing incident response times by nearly 30%. Fleet Management is the fastest-growing application as logistics operators increasingly integrate predictive routing, telematics, and real-time traffic intelligence to improve operational efficiency and asset utilization. Companies are strengthening platform integration and automation capabilities to support expanding enterprise demand.

Road Safety continues expanding through connected monitoring, automated enforcement, and predictive incident detection, while Electronic Toll Collection improves traffic continuity by reducing vehicle processing times by nearly 40%. Public Transportation applications are evolving through integrated passenger information systems and digital scheduling platforms. Technology providers are scaling cloud-native mobility solutions, expanding strategic collaborations, and integrating multiple operational modules into unified transportation management ecosystems that enhance long-term operational resilience.

Government Agencies remain the dominant end-user group with approximately 42% of total deployments because they oversee national transportation infrastructure, regulatory compliance, and long-term mobility modernization programs. Large-scale infrastructure initiatives support widespread implementation of connected traffic systems, while centralized procurement enables standardized deployment across multiple jurisdictions. Logistics Companies represent the fastest-growing end-user segment as digital freight operations improve delivery efficiency by nearly 18% and fleet visibility by approximately 25%. Vendors increasingly customize solutions for commercial mobility requirements through scalable software and analytics platforms.

Transportation Authorities continue expanding investments in multimodal traffic coordination, intelligent intersections, and integrated control centers, while Public Transit Operators adopt predictive scheduling and passenger information systems to improve service reliability. Companies are strengthening ecosystem partnerships, introducing flexible deployment models, and tailoring intelligent transportation platforms for specific operational environments. Competitive positioning increasingly depends on interoperable architecture, cybersecurity integration, and industry-specific digital mobility capabilities.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Advanced Connected Mobility Infrastructure Driving Network Efficiency

North America represents approximately 28% of the global Intelligent Transportation System Market, supported by mature digital infrastructure, extensive highway networks, and widespread adoption of AI-enabled traffic management platforms. Connected intersections, predictive traffic analytics, and integrated transportation command centers continue expanding across major metropolitan areas. Public agencies increasingly prioritize interoperable mobility platforms that integrate traffic operations, emergency response, and public transit management into unified digital ecosystems. More than 80 metropolitan transportation programs have implemented intelligent traffic optimization technologies, improving corridor performance and reducing incident response times. Technology vendors continue strengthening partnerships with cloud providers, telecom operators, and infrastructure specialists while expanding cybersecurity capabilities to support critical transportation assets.

United States Market Outlook: The United States leads regional deployment through federal infrastructure modernization initiatives, strong enterprise participation, and advanced digital transportation research. More than 75 major metropolitan areas operate integrated intelligent transportation platforms combining adaptive traffic signals, connected roadway infrastructure, and predictive analytics. Technology companies continue expanding software-defined transportation solutions while collaborating with telecommunications providers and municipal agencies to accelerate nationwide deployment of scalable, secure, and interoperable mobility systems.

Sustainable Digital Mobility Accelerates Infrastructure Modernization

Europe accounts for nearly 24% of global market activity, supported by stringent transportation regulations, advanced digital infrastructure, and sustainability-focused mobility strategies. Governments continue modernizing urban transport through intelligent traffic control, multimodal mobility platforms, and connected road infrastructure. Digital traffic management systems have reduced congestion in several smart city deployments by approximately 18%, strengthening operational efficiency and environmental performance. Transport authorities increasingly integrate vehicle-to-infrastructure communication with public transit management while technology providers expand interoperable software platforms and cross-border mobility solutions supporting seamless transportation operations.

Germany Market Outlook: Germany remains the region's technology leader through advanced automotive engineering, intelligent highway infrastructure, and industrial automation expertise. Nationwide deployment of connected mobility technologies continues supporting digital transportation initiatives, while intelligent traffic management adoption has expanded across major logistics corridors. German enterprises are strengthening partnerships involving automotive manufacturers, mobility software developers, and infrastructure providers to improve operational resilience, freight movement efficiency, and digital transport integration.

Large-Scale Smart Infrastructure Deployment Leadership

Asia-Pacific leads the global market with approximately 41% share, supported by extensive smart city investments, rapid urbanization, and large-scale transportation infrastructure modernization. Governments continue deploying intelligent highways, AI-enabled traffic management platforms, and connected mobility systems across expanding metropolitan networks. China, Japan, and South Korea collectively account for a substantial concentration of intelligent transport deployments, while intelligent intersection installations have increased by more than 30% across priority urban corridors. Technology suppliers continue expanding localized manufacturing, digital platform integration, and strategic collaborations to meet growing infrastructure demand and improve operational scalability.

China Market Outlook: China dominates regional deployment through comprehensive smart transportation planning, extensive expressway digitalization, and large-scale intelligent city programs. The country accounts for approximately one-third of global intelligent transportation infrastructure deployment, supported by strong domestic technology ecosystems and continuous public investment. Local enterprises continue accelerating AI integration, connected roadway development, and cloud-enabled transportation management while strengthening collaboration with communication technology providers to improve nationwide mobility efficiency.

Urban Mobility Modernization Gains Momentum

South America continues strengthening intelligent transportation deployment through expanding urban mobility programs and digital traffic management initiatives. The region represents approximately 5% of global market activity, with transportation agencies focusing on congestion reduction, public transit efficiency, and road safety improvements. Smart traffic signal deployments have improved traffic flow by nearly 15% across selected metropolitan corridors. Although infrastructure modernization remains uneven between countries, public-private partnerships and digital infrastructure investments continue supporting operational improvements. Technology vendors are expanding localized implementation services, cloud-based transport platforms, and integrated mobility management capabilities.

Brazil Market Outlook: Brazil leads regional adoption through large metropolitan transportation networks, smart mobility investments, and expanding intelligent traffic management programs. Major cities continue implementing adaptive signal control, integrated monitoring centers, and connected public transportation systems to improve operational efficiency. Domestic and international technology providers are increasing partnerships with municipal authorities while expanding deployment of intelligent mobility software supporting urban transportation modernization and logistics optimization.

Infrastructure Investment Reshapes Smart Mobility

Middle East & Africa is experiencing accelerated transformation through large-scale infrastructure modernization, digital mobility strategies, and smart city development initiatives. Governments continue prioritizing intelligent traffic management, connected transportation infrastructure, and AI-enabled operational platforms to improve urban mobility and logistics performance. Intelligent transport deployments have expanded by more than 25% across major infrastructure programs, supported by national digital transformation strategies. Technology companies are increasing regional partnerships, establishing local implementation capabilities, and introducing integrated transportation platforms aligned with next-generation infrastructure development.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional innovation through ambitious smart city initiatives, intelligent highway investments, and advanced digital infrastructure. Integrated transportation management platforms are widely deployed across major urban centers, supporting connected mobility and predictive traffic operations. Government-backed digital transformation programs continue encouraging collaboration between infrastructure operators, mobility technology companies, and telecommunications providers, strengthening the country's position as a regional benchmark for intelligent transportation deployment.

Competition is led by Siemens, Kapsch TrafficCom, Thales, Cubic Corporation, and Iteris, while regional infrastructure integrators challenge global technology leaders through localized deployment and lower implementation costs. Hardware OEMs increasingly compete with software-centric mobility platform providers as intelligent transportation shifts toward cloud-native architectures. The top five companies collectively control approximately 38% of the market. Competition centers on AI capability, cybersecurity, deployment speed, and interoperability, with advanced traffic analytics improving operational efficiency by nearly 25% and cloud-enabled platforms reducing lifecycle maintenance costs by around 18%. Companies strengthen market position through strategic infrastructure partnerships, software acquisitions, integrated mobility ecosystems, and vertical expansion across sensors, analytics, and communications. Competitive momentum is shifting toward software-defined transportation platforms as digital infrastructure modernization accelerates and governments prioritize interoperable systems. High certification requirements, cybersecurity compliance, and complex public procurement processes create significant entry barriers. Success increasingly depends on delivering scalable, secure, data-driven platforms with strong integration capabilities, localized implementation expertise, and long-term infrastructure support.

Siemens AG

Kapsch TrafficCom AG

Thales Group

Cubic Corporation

Iteris Inc.

SWARCO AG

Q-Free ASA

TransCore

Yunex Traffic

Huawei Technologies Co., Ltd.

Hitachi Ltd.

Toshiba Corporation

Mitsubishi Electric Corporation

NEC Corporation

Advanced artificial intelligence, edge computing, and vehicle-to-everything communication are redefining intelligent transportation operations by enabling continuous traffic optimization and predictive decision-making. AI-powered adaptive traffic control improves intersection efficiency by approximately 25%, while edge processing reduces response latency by nearly 40% compared with centralized legacy architectures. More than 55% of newly deployed metropolitan traffic management platforms now integrate cloud-based analytics, connected roadside infrastructure, and real-time mobility monitoring, allowing transport operators to improve network visibility and incident response without extensive infrastructure replacement.

Digital twins, predictive maintenance platforms, and IoT-enabled roadway sensors are emerging as the next operational standard. Compared with conventional inspection methods, predictive infrastructure monitoring reduces maintenance planning time by nearly 35% while improving asset utilization by approximately 20%. Technology vendors, telecom operators, and infrastructure integrators gain the strongest competitive advantage because integrated digital ecosystems support faster deployment, lower operational costs, and scalable management of multimodal transportation networks across expanding smart city environments.

Between 2026 and 2028, autonomous traffic orchestration, secure cloud-native transportation platforms, and AI-assisted mobility analytics will become mainstream deployment priorities. Companies investing in interoperable software, cybersecurity frameworks, and digital infrastructure integration today will strengthen operational resilience, accelerate deployment efficiency, and secure long-term competitive differentiation as transportation networks evolve into fully connected intelligent mobility ecosystems.

January 2024 – Kapsch TrafficCom secured a Cooperative Intelligent Transport Systems (C-ITS) contract with Germany's Autobahn GmbH, initially valued at EUR 7 million with expansion potential to EUR 36 million, strengthening smart work-zone safety infrastructure and long-term deployment opportunities. Source: https://www.kapsch.net

October 2024 – Siemens announced the acquisition of Altair Engineering for USD 10.6 billion, expanding its industrial software and AI portfolio to strengthen digital mobility and intelligent infrastructure capabilities, accelerating integrated transportation technology development. Source: https://www.reuters.com

April 2025 – Thales reported 9.9% organic first-quarter sales growth while continuing investment in digital security, transportation signaling, and intelligent mobility technologies, reinforcing its ability to support large-scale smart infrastructure modernization projects. Source: https://www.thalesgroup.com

May 2026 – Siemens reported that demand related to AI-driven infrastructure more than doubled during the quarter, with Smart Infrastructure generating EUR 1.8 billion in first-half orders, strengthening digital transportation ecosystem investments and advanced mobility platform deployment. Source: https://www.onvista.de

The report provides comprehensive coverage of Intelligent Transportation System technologies across Advanced Traffic Management, Advanced Public Transport, Advanced Traveler Information, Commercial Vehicle Systems, and Advanced Transportation Pricing. It evaluates key applications including traffic management, fleet management, road safety, electronic toll collection, and public transportation while assessing demand across government agencies, transportation authorities, logistics companies, and public transit operators. The study also analyzes competitive participation across more than 10 major technology providers alongside evolving deployment patterns and digital mobility adoption trends.

Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting infrastructure modernization, connected mobility deployment, and enterprise digitalization priorities between 2026 and 2033. The report examines AI, IoT, edge computing, cloud-based traffic management, digital twins, and vehicle-to-everything technologies while identifying operational benchmarks, investment priorities, partnership strategies, and competitive positioning. Strategic insights support expansion planning, technology adoption decisions, risk assessment, and long-term business development across established and emerging intelligent transportation ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 10354.39 Million |

Market Revenue in 2033 | USD 14612.63 Million |

CAGR (2026 - 2033) | 4.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens AG, Kapsch TrafficCom AG, Thales Group, Cubic Corporation, Iteris Inc., SWARCO AG, Q-Free ASA, TransCore, Yunex Traffic, Huawei Technologies Co., Ltd., Hitachi Ltd., Toshiba Corporation, Mitsubishi Electric Corporation, NEC Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |