Reports

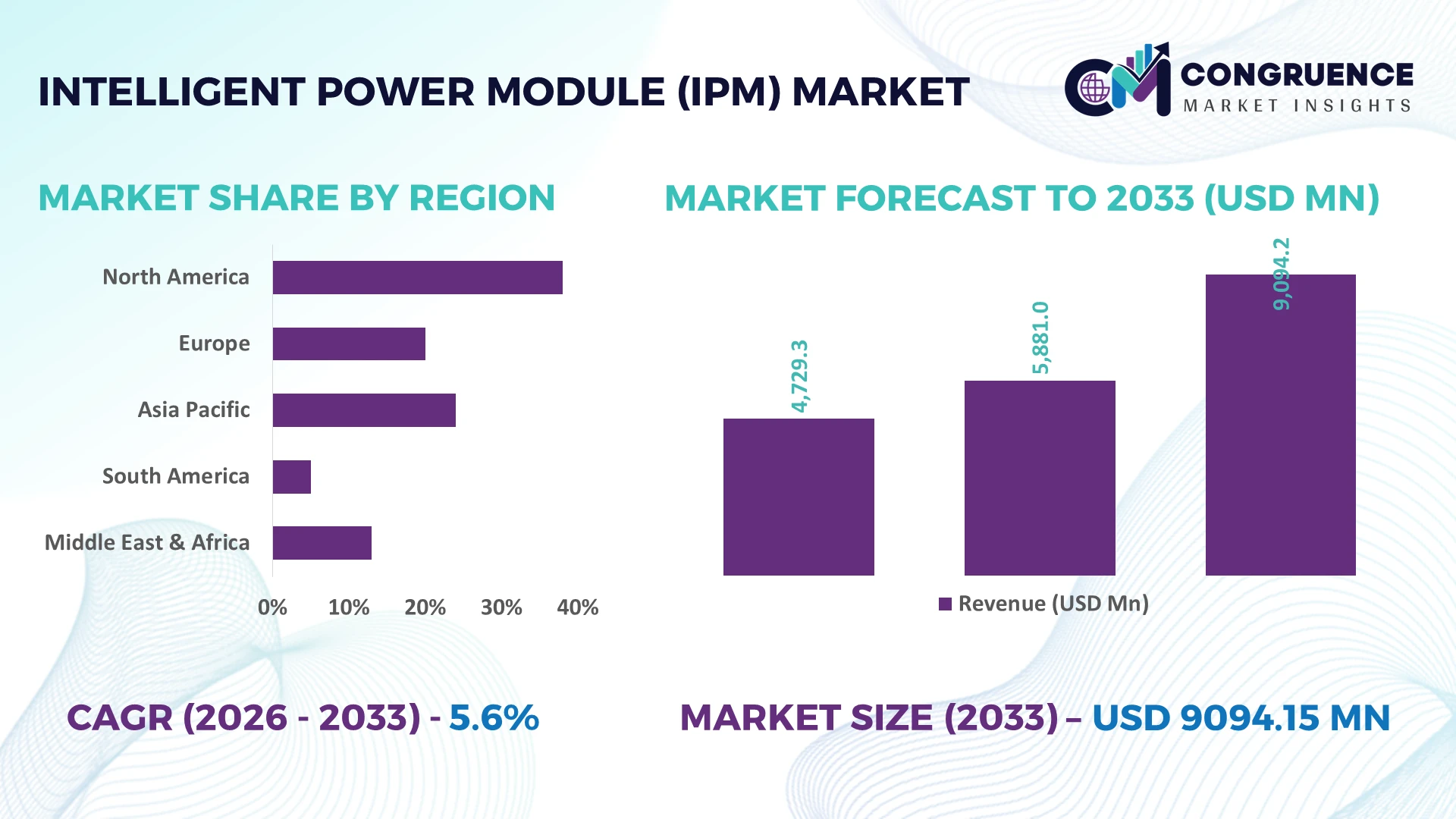

The Global Intelligent Power Module (IPM) Market was valued at USD 5881 Million in 2025 and is anticipated to reach a value of USD 9094.15 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033. Increasing deployment of silicon carbide and insulated-gate bipolar transistor technologies across electric vehicles, industrial motor drives, renewable energy inverters, and factory automation is accelerating the adoption of high-efficiency Intelligent Power Modules with integrated protection functions.

China dominates the global Intelligent Power Module (IPM) Market with approximately 42% of worldwide manufacturing capacity, backed by large-scale semiconductor investments, over 13 million annual electric vehicle production capacity, and rapid industrial automation deployment. Japan leads in premium IPM innovation for industrial and automotive applications, while South Korea continues expanding advanced power semiconductor fabrication. Ongoing semiconductor supply-chain diversification following global trade realignments is reinforcing regional manufacturing resilience and technology investments.

Strategic localization of advanced semiconductor production and next-generation power electronics development will define long-term competitiveness across the global Intelligent Power Module (IPM) Market.

Market Size & Growth: USD 5881 Million in 2025, projected to reach USD 9094.15 Million by 2033 at a CAGR of 5.6%, supported by expanding electric mobility and industrial power electronics adoption.

Top Growth Drivers: EV production (+28%), renewable energy installations (+19%), and industrial automation (+16%) continue accelerating global Intelligent Power Module deployment.

Short-Term Forecast: By 2028, advanced IPM architectures are expected to improve inverter efficiency by 8% while lowering thermal losses by nearly 15%.

Emerging Technologies: AI-assisted power management, silicon carbide devices, and advanced transfer-mold packaging are improving efficiency, reliability, and compact system integration.

Regional Leaders: Asia-Pacific leads with over USD 4.4 Billion opportunity, followed by Europe at nearly USD 2.0 Billion and North America above USD 1.6 Billion through manufacturing expansion.

Consumer/End-User Trends: More than 62% of newly designed industrial motor drive systems now integrate intelligent protection and compact IPM solutions.

Pilot/Case Example: A 2026 industrial automation deployment improved inverter operating efficiency by 11% while reducing maintenance requirements by 21%.

Competitive Landscape: Mitsubishi Electric leads with approximately 18% market share alongside Infineon Technologies, Fuji Electric, ROHM, and onsemi.

Regulatory & ESG Impact: Energy-efficiency regulations enable industrial power systems to reduce electricity consumption by approximately 12% through advanced module integration.

Investment & Funding: More than USD 8 Billion has been committed to semiconductor fabrication, advanced packaging, and regional manufacturing expansion amid supply-chain diversification.

Innovation & Future Outlook: Next-generation wide-bandgap semiconductor modules, digital health monitoring, and highly integrated packaging are strengthening global competitiveness and operational efficiency.

Demand for Intelligent Power Module (IPM) solutions continues expanding across electric vehicles, renewable energy systems, industrial robotics, and high-performance motor drives as manufacturers prioritize compact, energy-efficient power conversion. Advanced silicon carbide integration and intelligent thermal management are improving system reliability, while more than 35% of newly deployed industrial inverter platforms incorporate enhanced protection capabilities. Continued semiconductor localization and resilient supply-chain strategies are reinforcing long-term market expansion, setting the foundation for the strategic analysis that follows.

The Intelligent Power Module (IPM) Market has become strategically important as manufacturers prioritize power efficiency, localized semiconductor production, and resilient electronics supply chains. Accelerating electrification across automotive, industrial automation, renewable energy, and HVAC equipment is reshaping competitive dynamics, while semiconductor supply-chain restructuring after recent geopolitical disruptions is encouraging domestic manufacturing investments and long-term procurement partnerships. IPMs are increasingly viewed as critical components for improving system reliability and reducing lifecycle operating costs.

Compared with conventional discrete power semiconductor assemblies, advanced IPMs reduce component count by nearly 30% while improving system efficiency by approximately 8% through integrated gate drivers, protection circuitry, and optimized thermal management. China leads high-volume manufacturing with extensive industrial deployment, whereas Japan maintains technological leadership in premium automotive and industrial-grade modules focused on reliability and miniaturization. Over the next two to three years, adoption of silicon carbide-enabled IPMs is expected to exceed 25% of new high-performance inverter platforms, particularly across electric mobility and factory automation applications.

Industrial robotics manufacturers are integrating next-generation IPMs into compact servo drives to improve energy efficiency and reduce maintenance intervals, prompting suppliers to expand advanced packaging capacity, strengthen OEM collaborations, and accelerate product development. Companies that combine localized manufacturing, advanced semiconductor technologies, and application-specific innovation will secure stronger competitive positioning and long-term operational advantage.

Electrification of transportation, industrial automation, and renewable energy infrastructure remains the primary structural driver for the Intelligent Power Module (IPM) Market. More than 60% of newly commissioned industrial inverter platforms now incorporate integrated protection functions, while silicon carbide adoption in high-power applications has increased by approximately 22% over the past two years. China's continued investment in domestic semiconductor manufacturing and electric mobility is strengthening component availability and reducing import dependence. In response, leading manufacturers are expanding advanced packaging facilities, investing in high-voltage IPM portfolios, and forming technology partnerships with automotive and industrial OEMs. A key strategic advantage is the growing preference for highly integrated modules that reduce assembly complexity while improving operational reliability across mission-critical power conversion systems.

Persistent dependence on advanced semiconductor wafers, packaging substrates, and specialized manufacturing equipment continues to constrain market scalability. Silicon carbide wafer costs remain approximately 3–5 times higher than conventional silicon alternatives, while packaging material prices have fluctuated by nearly 18% due to supply-chain imbalances. Export controls affecting advanced semiconductor technologies have further complicated sourcing strategies for several manufacturers. Companies are mitigating these pressures by diversifying supplier networks, increasing localized production in countries such as India and Vietnam, and securing long-term procurement agreements with material providers. Operationally, firms capable of balancing production flexibility with strategic sourcing are better positioned to protect margins and maintain delivery consistency during supply disruptions.

Expanding deployment of silicon carbide and gallium nitride technologies is creating new opportunities for higher-efficiency Intelligent Power Modules across electric mobility, smart manufacturing, and renewable power conversion. Advanced wide-bandgap devices reduce switching losses by approximately 20% and improve power density by nearly 35% compared with conventional solutions. Japan and South Korea continue accelerating investment in advanced semiconductor ecosystems, while India's manufacturing incentive programs are attracting new power electronics production. Companies are strengthening research partnerships, expanding application-specific product portfolios, and investing in digital power management capabilities. An emerging strategic opportunity lies in highly integrated IPMs designed for compact industrial robotics and distributed energy storage systems requiring superior thermal performance and intelligent diagnostics.

Increasing system integration is raising engineering complexity across automotive, industrial, and renewable energy applications. More than 45% of manufacturers report longer validation cycles for advanced power electronics, while thermal management requirements increase by approximately 20% as power density continues rising. Compliance with evolving functional safety standards and reliability requirements further extends product qualification timelines, particularly in Japan and Germany's automotive sectors. Companies must expand simulation capabilities, strengthen engineering collaboration with OEMs, and invest in advanced testing infrastructure to accelerate commercialization. Organizations that successfully integrate hardware, software, thermal design, and functional safety into scalable IPM platforms will achieve stronger operational resilience and sustained competitive differentiation.

Advanced Packaging Expansion: Manufacturers are accelerating transfer-mold and double-sided cooling technologies, reducing thermal resistance by nearly 18% while improving power density by around 25%. Capacity utilization at leading Asian semiconductor facilities has exceeded 85%, prompting suppliers to automate packaging lines and expand localized assembly as supply-chain resilience becomes a strategic priority following global semiconductor policy shifts.

Wide-Bandgap Device Adoption: Silicon carbide integration continues replacing conventional silicon solutions in premium inverter platforms, lowering switching losses by approximately 20% and reducing system size by nearly 15%. Japanese and Chinese manufacturers are increasing long-term wafer procurement agreements while expanding collaborative development with automotive OEMs to secure reliable production and shorten qualification cycles.

Smarter Industrial Power Control: More than 60% of newly deployed industrial servo systems incorporate intelligent monitoring and integrated protection within IPMs, reducing unplanned equipment downtime by approximately 18%. Factory digitization initiatives are driving suppliers to embed diagnostic functions and predictive maintenance capabilities, enabling manufacturers to optimize maintenance schedules and improve operational continuity across automated production facilities.

Localized Manufacturing Strategies: Semiconductor localization programs have increased regional component sourcing by nearly 22%, while inventory lead times have declined by approximately 12% through diversified supplier networks. Rather than relying solely on capacity expansion, companies are restructuring procurement models, establishing regional packaging partnerships, and qualifying multiple manufacturing sites to improve delivery reliability and reduce operational exposure to geopolitical disruptions.

IGBT Modules remain the dominant segment as they provide an optimal balance of cost, reliability, and performance across industrial motor drives, renewable energy inverters, and automotive power electronics. Nearly 58% of high-power industrial inverter installations continue utilizing IGBT-based Intelligent Power Modules because of their mature manufacturing ecosystem and proven operational reliability. High Voltage IPMs also maintain strong demand in rail transportation and renewable energy infrastructure, while Low Voltage IPMs remain widely deployed across consumer appliances and compact industrial equipment. Manufacturers continue improving thermal management and package integration to enhance efficiency while lowering assembly complexity.

SiC Modules represent the fastest-growing type as electrified transportation and high-frequency power conversion require greater efficiency and higher switching speeds. Silicon carbide solutions improve power density by approximately 30% while reducing switching losses by nearly 20%, encouraging suppliers to expand dedicated production capacity and strategic technology partnerships. MOSFET Modules continue serving medium-power applications requiring high switching frequency and compact designs. Investment priorities are increasingly shifting toward wide-bandgap semiconductor platforms and application-specific module development to strengthen long-term product differentiation and operational performance.

Motor Drives remain the largest application segment because manufacturing, HVAC, pumps, compressors, and robotics require highly reliable power conversion and integrated protection. More than 60% of industrial automation systems utilize Intelligent Power Modules to improve operational efficiency and equipment reliability. Industrial Automation continues strengthening demand through increasing factory digitization, while Renewable Energy applications expand steadily as advanced inverter architectures improve conversion efficiency and support higher system reliability under varying operating conditions.

Electric Vehicles represent the fastest-growing application as manufacturers prioritize compact, high-efficiency traction inverters and onboard charging systems. Silicon carbide-enabled IPMs improve drivetrain efficiency by approximately 8% while reducing cooling requirements by nearly 15%, encouraging automotive suppliers to accelerate technology partnerships and localized manufacturing. Consumer Electronics maintains consistent demand through energy-efficient appliances and air-conditioning systems, although investment focus is steadily shifting toward transportation and industrial applications where higher power density and intelligent control deliver greater operational value.

Automotive remains the dominant end-user segment as electric vehicles, hybrid platforms, electric compressors, and onboard charging systems require highly integrated Intelligent Power Modules capable of delivering high efficiency and reliable thermal performance. Approximately 55% of newly developed automotive power electronics platforms now integrate advanced IPMs to improve system durability and reduce assembly complexity. Industrial end users continue representing substantial purchasing volume through automation, robotics, and motor control applications where continuous operational performance is essential.

Energy & Utilities is emerging as the fastest-growing end-user segment as utilities modernize renewable energy integration, battery energy storage, and smart grid infrastructure. High-efficiency IPMs improve inverter performance by approximately 10% while reducing maintenance interventions by nearly 15%. Telecommunications continues adopting intelligent power modules for efficient backup power systems, while Consumer Electronics maintains stable procurement for energy-efficient appliances. Manufacturers are responding through customized product portfolios, joint development agreements with OEMs, and regional manufacturing expansion to address evolving infrastructure requirements and application-specific performance expectations.

Asia-Pacific accounted for the largest market share at 52.4% in 2025 however, North America is expected to register the fastest growth, expanding at a 6.3% CAGR between 2026 and 2033.

Accelerated Semiconductor Localization and Industrial Electrification

North America is strengthening its position through semiconductor reshoring, industrial automation, and rapid electrification of transportation. The region contributes nearly 22% of global Intelligent Power Module deployment, supported by investments in domestic chip manufacturing and advanced power electronics production. More than 65% of new industrial automation projects now prioritize energy-efficient power modules with integrated protection functions. Expanding electric vehicle manufacturing and utility-scale battery storage installations are increasing demand for high-performance IPMs, while partnerships between semiconductor suppliers and automotive OEMs are improving technology commercialization. Companies are also increasing advanced packaging capacity to shorten supply chains and improve manufacturing resilience.

United States Market Outlook: The United States leads regional demand through large-scale electric vehicle production, industrial automation, and government-backed semiconductor manufacturing initiatives. More than 70% of North America's advanced power electronics design activity is concentrated in the country, supported by expanding fabrication investments and strong collaboration between semiconductor companies and automotive manufacturers. Enterprise adoption of intelligent motor control systems and renewable energy infrastructure continues strengthening demand for high-reliability IPMs across industrial and transportation applications.

Automotive Electrification Strengthens Technology Leadership

Europe maintains a strong position through premium automotive manufacturing, industrial automation, and strict energy-efficiency regulations. The region represents approximately 21% of global Intelligent Power Module deployment, with increasing investment in silicon carbide technologies and advanced inverter development. More than 55% of newly developed electric drivetrain platforms incorporate intelligent power modules with enhanced thermal performance and functional safety capabilities. Industrial modernization and renewable energy integration continue supporting demand, while manufacturers strengthen regional semiconductor partnerships to improve technology independence and supply security.

Germany Market Outlook: Germany remains Europe's strategic manufacturing hub for automotive power electronics and industrial automation equipment. The country accounts for nearly one-third of regional electric vehicle production capacity while maintaining leadership in factory automation technologies. Leading automotive suppliers and semiconductor manufacturers continue expanding collaborative development programs for next-generation IPMs, strengthening domestic innovation and supporting high-performance industrial and mobility applications.

Manufacturing Scale Drives Global Leadership

Asia-Pacific dominates the Intelligent Power Module market through unmatched semiconductor manufacturing capacity, electronics production, and electric vehicle deployment. The region contributes more than 52% of global market demand, supported by integrated semiconductor ecosystems across China, Japan, South Korea, and Taiwan. Manufacturing utilization at leading facilities consistently exceeds 85%, while continued investment in advanced packaging and wide-bandgap semiconductor technologies strengthens export competitiveness. Regional enterprises continue expanding production capacity and vertically integrating supply chains to improve delivery reliability and manufacturing efficiency.

China Market Outlook: China remains the largest national market, supported by large-scale semiconductor investment, industrial automation expansion, and electric vehicle manufacturing leadership. The country accounts for approximately 42% of global Intelligent Power Module manufacturing capacity while continuing to expand domestic semiconductor production. Government-supported localization initiatives and growing renewable energy deployment are encouraging manufacturers to accelerate advanced packaging, silicon carbide integration, and application-specific product development for domestic and export markets.

Industrial Modernization Expands Power Electronics Adoption

South America continues strengthening Intelligent Power Module adoption through industrial modernization, renewable energy investments, and expanding manufacturing automation. The region represents approximately 4% of global deployment, with increasing installation of energy-efficient motor drives across mining, food processing, and utility infrastructure. Renewable power projects and industrial electrification initiatives are encouraging wider adoption of intelligent power conversion technologies. Although semiconductor manufacturing remains limited, companies are expanding regional distribution partnerships and localized technical support to improve deployment efficiency and customer responsiveness.

Brazil Market Outlook: Brazil leads regional demand through its diversified manufacturing base, renewable energy investments, and expanding industrial automation programs. Large industrial facilities continue replacing conventional motor control equipment with intelligent power solutions to improve operational efficiency and reduce energy consumption. Growth in electric mobility initiatives and utility modernization is encouraging technology suppliers to strengthen local partnerships and engineering support capabilities across key industrial sectors.

Infrastructure Investment Supports Intelligent Electrification

The Middle East & Africa market is advancing through infrastructure modernization, renewable energy deployment, and industrial diversification initiatives. The region contributes approximately 3% of global Intelligent Power Module demand, supported by utility-scale solar developments, smart infrastructure projects, and expanding industrial automation investments. More than 30% of newly commissioned utility-scale renewable projects increasingly integrate advanced power electronics for improved energy conversion efficiency. Technology providers are expanding engineering partnerships and regional service networks to support long-term infrastructure development and operational reliability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through industrial diversification, smart manufacturing initiatives, and significant renewable energy investments. Large infrastructure programs continue driving demand for efficient power conversion technologies across utilities, manufacturing, and transportation. The country's expanding industrial zones and advanced energy projects are encouraging global semiconductor and power electronics suppliers to establish stronger commercial partnerships and localized technical capabilities to support long-term deployment.

Competition is led by Mitsubishi Electric, Infineon Technologies, Fuji Electric, onsemi, and ROHM, collectively controlling approximately 61% of the global market. Global technology leaders compete through advanced semiconductor integration and automotive-grade reliability, while regional manufacturers focus on cost-efficient industrial and appliance IPMs. OEMs increasingly evaluate suppliers on switching efficiency, thermal performance, qualification speed, and long-term supply assurance rather than component pricing alone. Silicon carbide-based modules improve system efficiency by nearly 20%, while advanced packaging reduces thermal resistance by approximately 18%, making technology differentiation a decisive competitive factor. Companies are expanding wafer capacity, strengthening automotive partnerships, investing in localized packaging facilities, and vertically integrating semiconductor manufacturing to secure supply. Competition is shifting from discrete component supply toward complete power electronics platforms combining hardware, software, and intelligent diagnostics. High qualification requirements, capital-intensive fabrication, and stringent automotive reliability standards remain major entry barriers. Winning requires continuous semiconductor innovation, resilient manufacturing, application-specific engineering, and long-term strategic partnerships with automotive and industrial OEMs.

Mitsubishi Electric Corporation

Infineon Technologies AG

Fuji Electric Co., Ltd.

onsemi

ROHM Co., Ltd.

STMicroelectronics N.V.

Toshiba Electronic Devices & Storage Corporation

Alpha and Omega Semiconductor Limited

SEMIKRON Danfoss

Hitachi Energy Ltd.

Vishay Intertechnology, Inc.

Microchip Technology Incorporated

The Intelligent Power Module (IPM) market is rapidly transitioning from conventional silicon-based power devices toward highly integrated silicon carbide and gallium nitride platforms. Wide-bandgap semiconductor technologies reduce switching losses by approximately 20% while increasing power density by nearly 30%, enabling smaller inverter designs and improved thermal efficiency. Around 35% of newly developed high-performance automotive and industrial inverter platforms now incorporate advanced wide-bandgap architectures, reflecting accelerating enterprise adoption across electrified transportation and factory automation.

Integrated gate drivers, embedded protection circuits, digital diagnostics, and AI-assisted condition monitoring are becoming standard competitive differentiators. Compared with conventional discrete power electronics, modern IPMs reduce component count by approximately 30% while improving overall inverter efficiency by nearly 8%. Automotive manufacturers, renewable energy equipment suppliers, and industrial automation companies benefit through lower maintenance requirements, faster system integration, and improved operational reliability. Companies are expanding advanced packaging technologies, chip-embedded architectures, and automated semiconductor manufacturing to strengthen product differentiation.

Between 2026 and 2028, hybrid silicon carbide integration, digital twin-assisted power electronics design, and intelligent thermal management will reshape product development. Advanced transfer-mold packaging, predictive diagnostics, and application-specific module architectures will shorten product qualification cycles while supporting higher reliability. Early technology adopters capable of combining semiconductor innovation with localized manufacturing and software-enabled power management will strengthen competitive positioning across automotive, industrial, renewable energy, and next-generation infrastructure markets.

January 2024 Mitsubishi Electric announced the J3-Series SiC and Si power modules for xEV inverters, introducing six scalable module variants for compact vehicle platforms, strengthening automotive power electronics development and manufacturing flexibility. Source: mitsubishielectric.com

June 2024 Mitsubishi Electric began shipping new Unifull 3.3kV SiC-MOSFET power modules, expanding the product family to three ratings and reducing switching losses for rail and industrial power systems, improving high-power inverter efficiency.

April 2025 Alpha and Omega Semiconductor introduced the Mega IPM-7 intelligent power module series, delivering higher power density for BLDC motor-drive applications and improving application performance across home appliances and industrial equipment. Source: nasdaq.com

March 2025 Infineon Technologies launched next-generation OptiMOS quad-phase power modules delivering industry-leading current density of 2 A/mm² for AI data center power delivery, enhancing power density and lowering total operating costs. Source: infineon.com

The report provides comprehensive coverage of Intelligent Power Module technologies across IGBT Modules, MOSFET Modules, SiC Modules, Low Voltage IPM, and High Voltage IPM. It evaluates deployment across motor drives, electric vehicles, renewable energy, industrial automation, and consumer electronics while assessing demand from automotive, industrial, energy & utilities, telecommunications, and consumer electronics sectors. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by competitive benchmarking of major technology suppliers and manufacturing strategies.

The study evaluates advanced semiconductor technologies, silicon carbide adoption, intelligent packaging innovations, thermal management, and digital power control trends shaping industry evolution between 2026 and 2033. More than 60% of market assessment focuses on high-growth industrial and transportation applications, while strategic analysis covers investment priorities, product differentiation, supply-chain resilience, manufacturing localization, partnership activity, and competitive positioning, enabling stakeholders to identify expansion opportunities, technology investment priorities, and long-term operational advantages.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 5881 Million |

Market Revenue in 2033 | USD 9094.15 Million |

CAGR (2026 - 2033) | 5.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Mitsubishi Electric Corporation, Infineon Technologies AG, Fuji Electric Co., Ltd., onsemi, ROHM Co., Ltd., STMicroelectronics N.V., Toshiba Electronic Devices & Storage Corporation, Alpha and Omega Semiconductor Limited, SEMIKRON Danfoss, Hitachi Energy Ltd., Vishay Intertechnology, Inc., Microchip Technology Incorporated |

Customization & Pricing | Available on Request (10% Customization is Free) |