Reports

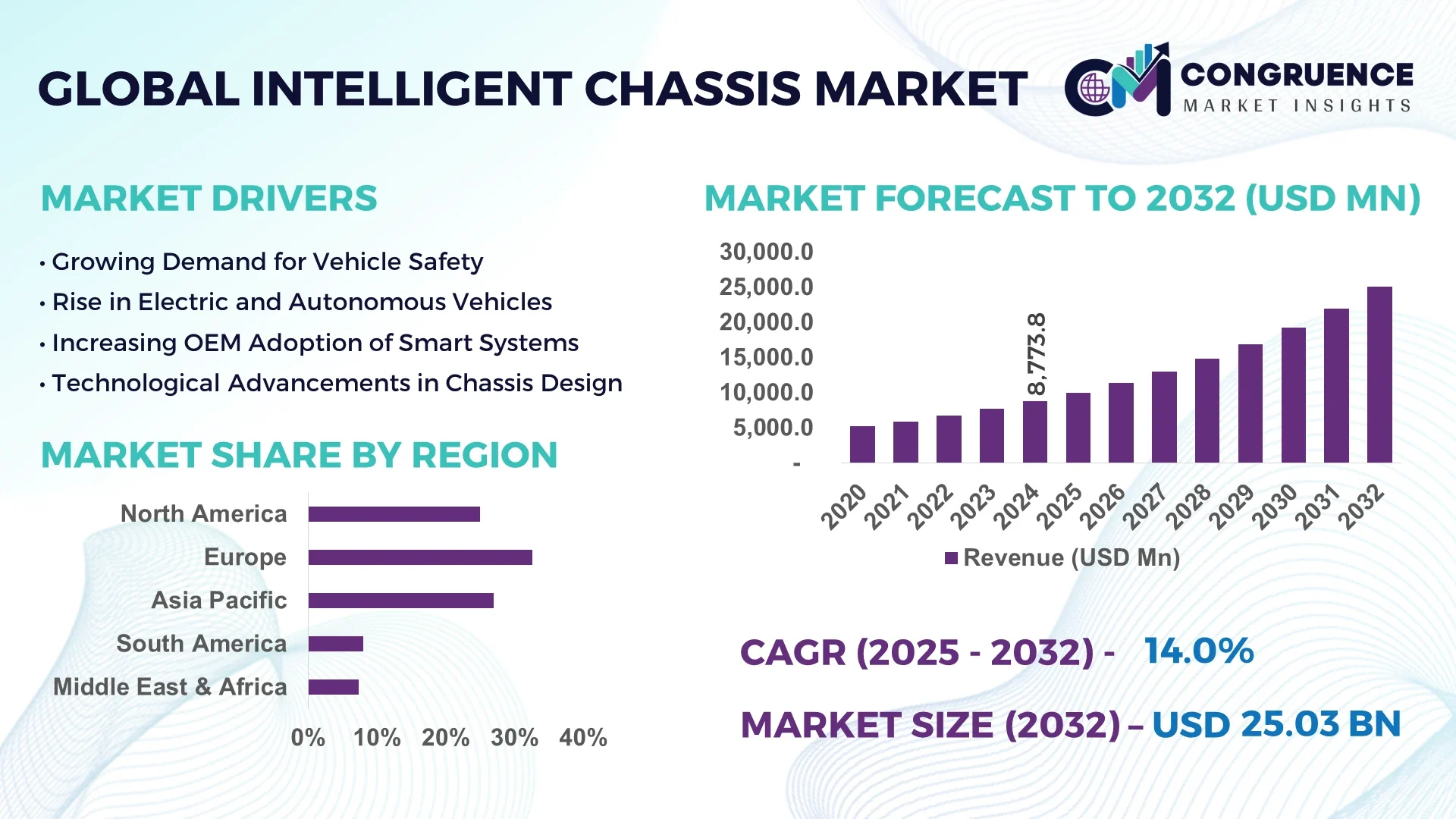

The Global Intelligent Chassis Market was valued at USD 8,773.782 Million in 2024 and is anticipated to reach a value of USD 25,027.97 Million by 2032, expanding at a CAGR of 14.0% between 2025 and 2032.

China leads the global Intelligent Chassis market, with more than 50% of new vehicles sold in 2024 featuring advanced driver assistance systems (ADAS). In comparison, adoption in the United States remains below 40%, making China the most dominant player in intelligent vehicle integration.

The Intelligent Chassis Market is experiencing rapid technological advancements, driven by the increasing demand for safer and more efficient vehicles. An intelligent chassis system integrates various sub-systems like active suspension, steering, braking, and powertrain to ensure real-time adaptability to road and driving conditions. Automakers are incorporating steer-by-wire, brake-by-wire, and active air suspension technologies to offer improved control, comfort, and safety. These features are particularly in demand across luxury and premium vehicle segments. Furthermore, the rise of autonomous vehicles has elevated the importance of intelligent chassis systems, as they provide the structural and technological backbone for automated functions. The commercial vehicle sector is also witnessing increased adoption due to the need for better load management and route optimization. These factors collectively contribute to the significant growth of the intelligent chassis industry.

Artificial Intelligence is playing a pivotal role in reshaping the Intelligent Chassis Market by enabling smarter, more adaptive, and highly responsive automotive systems. AI-driven algorithms are used to continuously monitor vehicle dynamics, driver behavior, and external conditions, making real-time decisions to enhance safety and performance. Through sensor fusion from radar, LiDAR, and cameras, AI interprets data to adjust steering, braking, and suspension systems. AI integration also supports predictive maintenance by identifying potential failures before they occur, minimizing downtime and reducing costs.

OEMs are heavily investing in AI-powered chassis systems to enhance electric and autonomous vehicle functionalities. AI allows the vehicle to autonomously adapt its chassis stiffness based on road surface conditions, improving ride comfort and vehicle handling. This is particularly important in electric vehicles, where battery positioning affects vehicle dynamics. Manufacturers like Tesla, Mercedes-Benz, and NIO are deploying AI-enabled suspension systems that learn from driver behavior and road profiles. Furthermore, AI enhances adaptive cruise control and lane-centering, integral to semi-autonomous and autonomous driving.

As AI adoption in vehicles expands, intelligent chassis systems are becoming central to vehicle architecture, supporting both human and machine-driven mobility with unmatched precision, control, and comfort.

“In January 2024, BYD introduced its new DiSus Intelligent Body Control System, the world’s first mass-produced intelligent body control system developed in-house by a Chinese carmaker. The system integrates intelligent damping, active suspension, and body movement control to enhance driving experience and safety across all models in its Dynasty and Ocean series.”

The growing emphasis on road safety and vehicle stability is pushing automakers to incorporate intelligent chassis technologies. These systems play a critical role in enhancing vehicle control by managing steering, braking, and suspension in real-time. The deployment of systems such as Electronic Stability Control (ESC), Active Yaw Control, and Integrated Vehicle Dynamics has surged. Regulatory bodies in Europe and Asia-Pacific are mandating advanced safety systems in both passenger and commercial vehicles. This has prompted OEMs to invest in integrated chassis control technologies that reduce rollovers, enhance cornering, and improve overall vehicle responsiveness under extreme driving conditions.

The implementation of intelligent chassis systems significantly increases the overall cost of the vehicle due to the inclusion of multiple sensors, control units, and complex mechanical components. These costs are particularly burdensome for mid-range and economy vehicle manufacturers, limiting widespread adoption. In addition, maintenance of these systems requires skilled technicians and expensive diagnostics equipment, which is a deterrent in price-sensitive markets. The frequent need for calibration and software updates also increases ownership costs, creating hesitation among budget-conscious consumers and fleet operators.

The commercial vehicle sector offers strong growth potential for intelligent chassis systems. Fleet operators are increasingly investing in smart technologies to ensure better fuel efficiency, reduce tire wear, and enhance driver comfort. Intelligent chassis systems can adjust suspension and braking dynamics based on load weight and road conditions. Autonomous vehicle development has further opened doors, as these vehicles require precise chassis control for safety and navigation. With governments encouraging autonomous mobility and logistics automation, intelligent chassis platforms are becoming foundational components in next-gen commercial transport.

The integration of multiple vehicle systems—braking, steering, suspension, and powertrain—into a unified intelligent chassis platform is technically challenging. Different components often originate from various suppliers, leading to compatibility issues. Developing centralized control units that manage all subsystems without lag or error is a major hurdle. Additionally, maintaining cybersecurity standards in software-driven chassis platforms is becoming increasingly difficult as vehicle connectivity expands. These technical complexities hinder rapid development and prolong the vehicle design and testing cycles for automakers.

• Integration of Steer-by-Wire and Brake-by-Wire Technologies: The automotive industry is witnessing a swift transition from traditional mechanical systems to electronically controlled steer-by-wire and brake-by-wire technologies. These systems eliminate the need for physical linkages, reducing vehicle weight and allowing more flexible vehicle designs. In 2024, over 30% of new electric vehicles in China and Europe were equipped with steer-by-wire systems, offering enhanced responsiveness and safety. Brake-by-wire adoption is also accelerating, especially in premium and high-performance vehicles, allowing regenerative braking optimization and quicker response times.

• Shift Towards Software-Defined Chassis Platforms: Automakers are increasingly adopting software-defined vehicle architectures, and the intelligent chassis is a key area of focus. Chassis control units are now embedded with real-time operating systems capable of over-the-air (OTA) updates and machine learning-based decision-making. As of 2024, over 45% of new intelligent chassis systems launched by OEMs supported OTA firmware upgrades, enabling continuous improvement in suspension tuning, steering calibration, and braking performance without visiting service centers.

• Growing Use of Lightweight and High-Strength Materials: Intelligent chassis systems are now being developed using a combination of aluminum alloys, carbon composites, and high-strength steel to balance durability and weight reduction. These material innovations are particularly significant in electric vehicles, where chassis weight directly affects driving range. By 2024, nearly 60% of EV chassis platforms incorporated lightweight materials, enhancing efficiency without compromising structural integrity or crashworthiness.

• Increased Deployment in Electric and Autonomous Vehicles: With the expansion of electric and autonomous vehicle production, intelligent chassis systems are becoming a core part of the vehicle architecture. Electric vehicles benefit from active air suspension and torque vectoring systems to enhance range and traction, while autonomous vehicles require integrated systems that allow seamless control and redundancy. In 2024, nearly 70% of autonomous vehicle prototypes tested globally included intelligent chassis modules, showcasing the market's pivotal role in the mobility transition.

The Intelligent Chassis Market is segmented based on type, application, and end-user, each playing a distinct role in market expansion. By type, key segments include active suspension systems, brake-by-wire, steer-by-wire, air suspension, and integrated vehicle dynamics. Among applications, passenger cars, commercial vehicles, electric vehicles, and autonomous vehicles are driving demand. End-user segmentation reveals OEMs, aftermarket providers, and fleet operators as primary stakeholders. The integrated vehicle dynamics segment is emerging as a critical innovation, offering a unified approach to vehicle control. Electric vehicles are driving rapid adoption, particularly among fleet operators and OEMs aiming to enhance vehicle control, efficiency, and adaptability under varying road and load conditions.

The intelligent chassis market includes several critical types: active suspension systems, brake-by-wire systems, steer-by-wire systems, air suspension, and integrated vehicle dynamics. Among these, integrated vehicle dynamics led the market in 2024, accounting for over 28% of total installations across high-end and electric vehicles. This type unifies control of braking, steering, and suspension for optimal vehicle handling. It is particularly prominent in premium and autonomous vehicle segments where performance and safety are paramount.

Steer-by-wire is the fastest-growing segment, with an estimated 35% year-on-year increase in adoption across EVs and concept vehicles. The elimination of the mechanical steering column enables new cabin configurations and improved vehicle response. Brake-by-wire is gaining momentum too, especially in vehicles with regenerative braking, improving braking efficiency and response times.

Meanwhile, air suspension systems remain dominant in heavy-duty and commercial vehicles for their load-leveling ability. Active suspension systems, while prevalent in luxury cars, are now increasingly being adopted in mid-segment vehicles due to falling costs and technological maturity.

Key application segments for intelligent chassis systems include passenger cars, commercial vehicles, electric vehicles, hybrid vehicles, and autonomous vehicles. In 2024, passenger cars held the largest market share, driven by the demand for ride comfort, dynamic performance, and safety among luxury and mid-range vehicles. Over 60% of new luxury sedans in Europe featured intelligent chassis elements such as adaptive dampers and electronic stability control.

However, electric vehicles (EVs) emerged as the fastest-growing application segment, with nearly 50% of new EVs incorporating at least one intelligent chassis function. The integration of these systems in EVs supports improved range, dynamic torque distribution, and smoother ride quality—critical selling points in a competitive market.

Commercial vehicles are also rapidly adopting these technologies to improve load handling, reduce wear, and enhance driver comfort, particularly in logistics and last-mile delivery fleets. Autonomous vehicles, though currently in the early deployment phase, rely heavily on intelligent chassis systems for precision and fail-safe redundancy, marking them as a future growth engine.

The key end-users in the Intelligent Chassis Market include original equipment manufacturers (OEMs), fleet operators, automotive technology providers, and aftermarket service providers. In 2024, OEMs dominated the market, contributing to over 65% of total demand. OEMs are aggressively integrating intelligent chassis platforms into their new model line-ups, especially within electric and luxury vehicle categories, to improve safety, comfort, and driving dynamics.

Fleet operators represent the fastest-growing end-user segment, particularly in the logistics and ride-hailing sectors. These operators are increasingly prioritizing intelligent chassis features to optimize vehicle uptime, reduce maintenance, and ensure driver safety. Around 40% of newly purchased delivery vans in urban markets had intelligent suspension or stability systems in 2024.

Automotive technology providers are also gaining traction by supplying modular chassis platforms and control units, enabling vehicle manufacturers to shorten development cycles. The aftermarket sector, though comparatively smaller, is expanding due to rising demand for upgrades in existing vehicles, particularly for commercial applications in North America and Asia.

Europe accounted for the largest market share at 32.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

The European market has seen strong adoption of intelligent chassis systems driven by stringent vehicle safety regulations and a significant rise in electric vehicle production. Germany, France, and the UK are at the forefront of deploying steer-by-wire and active suspension systems across premium and mid-range vehicles. Meanwhile, Asia-Pacific is witnessing rapid advancements in smart mobility infrastructure and automotive manufacturing. Countries like China, South Korea, and Japan are heavily investing in next-generation vehicle platforms, which include intelligent chassis as a standard offering in electric and autonomous vehicles. In North America, increasing demand for performance vehicles and connected driving systems is boosting the adoption of brake-by-wire and integrated chassis platforms, especially in the United States and Canada. Emerging economies in the Middle East & Africa and South America are also beginning to embrace intelligent chassis in commercial and luxury vehicle segments due to urbanization and improved road safety initiatives.

Rising Integration in Electric Pickup Trucks and SUVs

In North America, the Intelligent Chassis Market is significantly influenced by the surge in electric pickup trucks and sport utility vehicles. In 2024, the U.S. accounted for over 68% of the regional demand, followed by Canada with approximately 22%. Key developments include widespread integration of active suspension systems and torque vectoring modules in electric vehicle platforms such as the Ford F-150 Lightning and Rivian R1T. Over 55% of electric SUVs launched in the region during 2024 were equipped with at least two intelligent chassis technologies. Moreover, the commercial fleet sector is driving demand for brake-by-wire and adaptive suspension systems to optimize fuel efficiency and reduce maintenance costs. With strong investments from OEMs and tech startups, the region is also exploring software-defined chassis capable of remote diagnostics and over-the-air updates, improving vehicle reliability and user experience.

Advanced Integration Across Premium and Electric Vehicles

Europe leads in intelligent chassis adoption due to a high concentration of luxury automakers and progressive environmental regulations. In 2024, Germany led the market with a 38% share of the regional total, followed by France at 21%. Automakers like BMW, Mercedes-Benz, and Audi are deploying integrated vehicle dynamics and active air suspension systems as standard offerings in EVs and hybrid models. Over 60% of premium vehicles manufactured in the region included steer-by-wire or brake-by-wire systems in 2024. The region is also seeing an uptick in intelligent chassis use in compact electric vehicles, reflecting consumer demand for comfort, agility, and safety. With the European Union promoting connected and autonomous mobility, intelligent chassis platforms are becoming essential for next-gen vehicle compliance and performance optimization.

Electrification and Automation Drive Surge in Demand

The Asia-Pacific region is emerging as a hotspot for intelligent chassis system integration due to massive growth in electric and autonomous vehicle production. In 2024, China held the largest regional share at 51%, followed by Japan at 19%. China’s aggressive rollout of EVs and smart city infrastructure is driving mass adoption of steer-by-wire and integrated chassis systems. Over 45% of electric sedans and crossovers launched in China in 2024 featured some form of intelligent chassis technology. Japan and South Korea continue to innovate in active suspension and control systems, particularly in hybrid and luxury vehicles. OEMs in this region are also exploring AI-enabled chassis modules capable of predictive behavior analysis for enhanced driving safety. Asia-Pacific’s focus on electrification, technological self-reliance, and smart transport networks is pushing demand for scalable, software-driven chassis architectures.

Gradual Uptake Across Commercial Fleets and Urban Vehicles

South America’s Intelligent Chassis Market is witnessing steady development, particularly in Brazil and Argentina. Brazil accounted for nearly 62% of the region’s demand in 2024, with Argentina contributing 21%. Commercial vehicles in logistics and public transportation sectors are increasingly incorporating active suspension and electronic braking systems to improve performance on uneven road surfaces. Urban mobility trends in countries like Chile and Colombia are encouraging fleet upgrades with modular intelligent chassis platforms. Though still in early adoption stages, vehicle OEMs are testing steer-by-wire systems in compact electric vehicles suited for urban delivery applications. Growing awareness around safety, durability, and fleet cost optimization is leading to increased deployment of intelligent chassis technologies, especially in public-private transportation partnerships.

Rising Deployment in High-End and Utility Vehicles

In the Middle East & Africa, the intelligent chassis market is expanding primarily through premium vehicle imports and government-led infrastructure upgrades. In 2024, the UAE held 41% of the regional share, followed by Saudi Arabia at 29%. Luxury SUVs and sedans imported into the Gulf countries are frequently equipped with integrated vehicle dynamics, air suspension, and electronic stability systems. The demand is especially high among private and commercial fleets operating in desert and rugged terrains, where adaptive systems enhance both comfort and off-road capability. South Africa is showing early-stage integration in hybrid and commercial transport sectors, focusing on safety compliance and ride efficiency. Government incentives and consumer preference for high-tech vehicles are fueling the adoption of intelligent chassis solutions, particularly in urban mobility and defense applications.

The Intelligent Chassis Market is witnessing intense competition among major automotive component suppliers and technology innovators, each vying to establish dominance through strategic partnerships, R&D investments, and product diversification. In 2024, over 65% of global intelligent chassis installations were dominated by the top 10 companies. Key players are investing in software-defined chassis architecture that integrates control units for steering, suspension, braking, and stability systems. Leading manufacturers are expanding their global footprint through collaboration with OEMs and Tier 1 suppliers, particularly in Asia-Pacific and Europe.

Joint ventures between chassis system specialists and EV makers are reshaping the market structure, with many players entering the electric and autonomous vehicle space. Companies are focusing on the development of integrated modular platforms that enable multi-functional control across diverse vehicle models. With nearly 40% of high-end electric vehicles globally already adopting steer-by-wire or brake-by-wire modules, suppliers with strong mechatronics and electronics capabilities are gaining a competitive edge. Moreover, several players are strengthening their portfolios through strategic acquisitions in sensor technology, simulation software, and AI-based control algorithms.

ZF Friedrichshafen AG

Continental AG

Robert Bosch GmbH

Hyundai Mobis Co., Ltd.

Hitachi Astemo Ltd.

Schaeffler Technologies AG & Co. KG

KYB Corporation

Aptiv PLC

Tenneco Inc.

Magneti Marelli S.p.A.

NSK Ltd.

Mando Corporation

JTEKT Corporation

The Intelligent Chassis Market is being transformed by the convergence of advanced electronics, mechatronics, and software-defined vehicle architectures. As of 2024, more than 52% of newly manufactured premium vehicles were equipped with at least two intelligent chassis features such as active suspension or electronic stability control. Among these, steer-by-wire and brake-by-wire technologies are seeing widespread deployment across electric and hybrid vehicles due to their reduced mechanical complexity and increased responsiveness.

Sensor fusion, combining inputs from gyroscopes, accelerometers, and wheel speed sensors, is enabling real-time adaptive control of chassis behavior based on road and driving conditions. Manufacturers are also incorporating AI-driven control systems that can predict driver intent and road irregularities, optimizing ride comfort and safety. Integrated chassis control units are being designed to handle multi-domain inputs, streamlining communication between vehicle systems and reducing wiring complexity by up to 30%.

The use of silicon carbide (SiC) semiconductors and advanced ECUs is boosting energy efficiency and computational power, essential for autonomous driving features. Furthermore, digital twin technology is being used to simulate chassis performance under various conditions, accelerating product development cycles. These innovations are not only improving vehicle dynamics and safety but also supporting over-the-air software updates, extending system longevity and reducing total ownership costs.

• In March 2024, Bosch unveiled an advanced modular chassis control unit that integrates active suspension, braking, and steering systems into a single platform. This innovation aims to reduce vehicle weight by 15% and enhance overall vehicle stability, particularly in autonomous driving scenarios.

• In April 2024, Continental AG launched a new electronic control unit (ECU) designed for electric vehicles. This ECU optimizes battery management and powertrain performance, enabling vehicles to adapt to real-time driving conditions and manage energy efficiency more effectively.

• In May 2024, ZF Group introduced an electric active suspension system that enhances ride comfort while optimizing fuel efficiency in electric vehicles. The system allows for real-time adjustment of suspension stiffness based on road conditions, leading to improved vehicle stability and safety.

• In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

The scope of the Intelligent Chassis Market Report encompasses a detailed analysis of the global market dynamics, including trends, technologies, and key developments driving the growth of intelligent chassis solutions. As vehicles increasingly adopt advanced systems for enhanced performance, safety, and autonomy, the intelligent chassis market is expected to play a pivotal role in the automotive industry’s future. This report covers various segments such as chassis control systems, suspension technologies, and electronic control units (ECUs), which are becoming essential for the development of smart, connected vehicles.

The report also explores regional variations in the adoption of intelligent chassis systems, with regions like North America, Europe, and Asia-Pacific witnessing rapid growth due to technological advancements and regulatory support for green and autonomous vehicles. Moreover, the report delves into the key players contributing to the market landscape, including OEMs and component manufacturers, who are investing heavily in research and development to enhance vehicle safety and driving experiences.

Additionally, it highlights the potential challenges and opportunities for market growth, including the integration of AI and machine learning in chassis control systems and the demand for electric vehicles (EVs) with high-performance suspension systems. The market scope also includes future growth potential in emerging regions such as South America and the Middle East, where smart automotive solutions are beginning to take off.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 8773.782 Million |

|

Market Revenue in 2032 |

USD 25027.97 Million |

|

CAGR (2025 - 2032) |

14% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ZF Friedrichshafen AG, Continental AG, Robert Bosch GmbH, Hyundai Mobis Co., Ltd., Hitachi Astemo Ltd., Schaeffler Technologies AG & Co. KG, KYB Corporation, Aptiv PLC, Tenneco Inc., Magneti Marelli S.p.A., NSK Ltd., Mando Corporation, JTEKT Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |