Reports

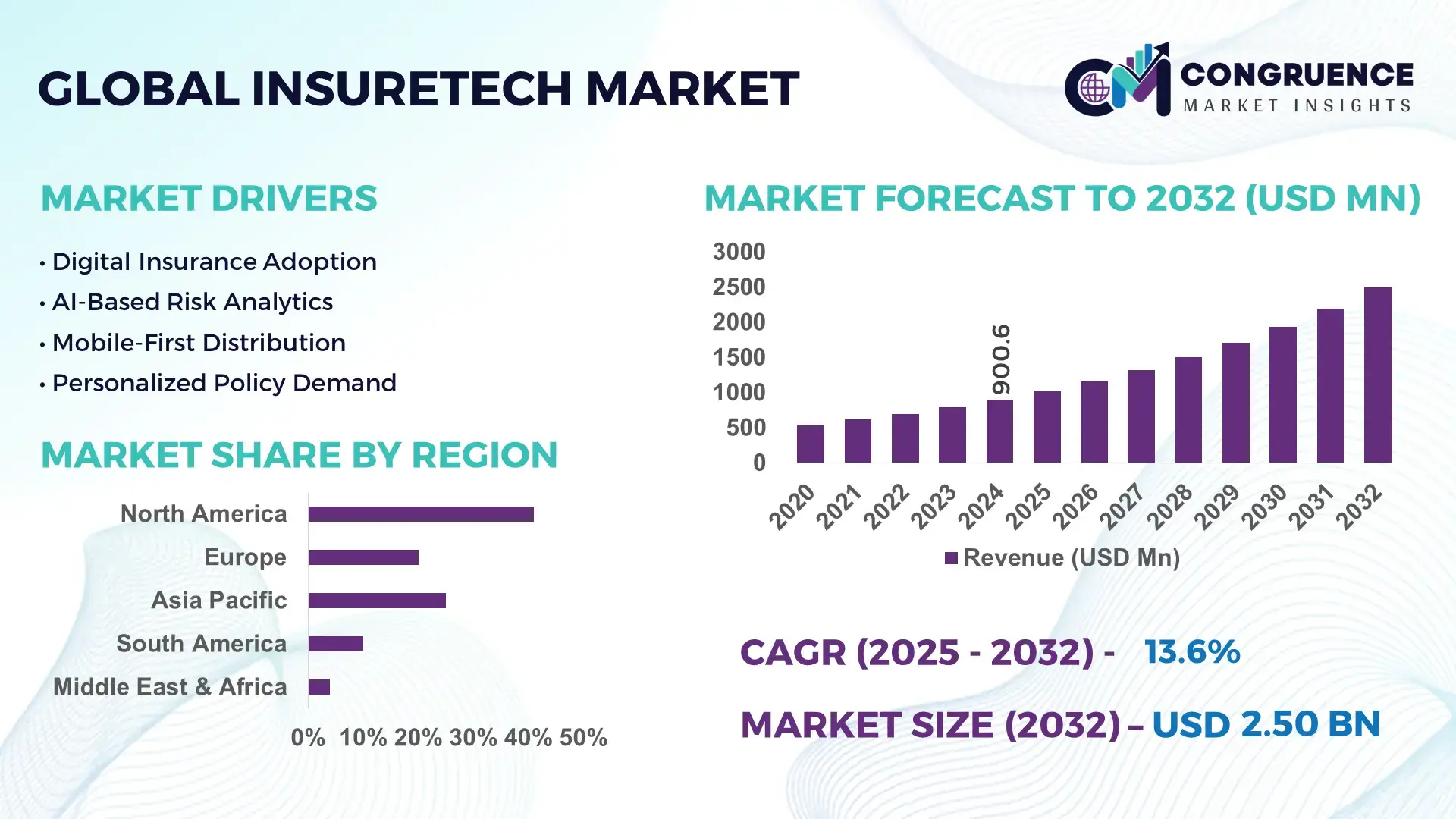

The Global Insuretech Market was valued at USD 900.62 Million in 2024 and is anticipated to reach a value of USD 2497.86 Million by 2032 expanding at a CAGR of 13.6% between 2025 and 2032. This growth is primarily driven by accelerated digital transformation across insurance value chains, improving underwriting accuracy, claims automation, and customer experience through advanced technologies.

The United States dominates the global Insuretech marketplace, supported by a highly developed insurance ecosystem and strong digital infrastructure. In 2024, the U.S. hosted over 45% of active Insuretech startups globally, with annual Insuretech investment exceeding USD 8.5 billion. The country accounts for more than 60% of AI-enabled insurance platforms deployed worldwide, with widespread application across underwriting, fraud detection, claims processing, and customer engagement. Cloud-based policy administration systems support over 70% of U.S. insurers, while API-driven integrations are used by more than 65% of carriers to connect with third-party data providers. Consumer adoption is strong, with nearly 58% of U.S. policyholders interacting with insurers through digital-only channels, and over 40% using mobile-first insurance services for policy management and claims submission.

Market Size & Growth: Valued at USD 900.62 Million in 2024, projected to reach USD 2497.86 Million by 2032, growing at a CAGR of 13.6%, driven by automation-led efficiency gains and digital-first insurance models.

Top Growth Drivers: AI-based underwriting adoption (42%), digital claims processing efficiency improvement (38%), API-based ecosystem integration expansion (34%).

Short-Term Forecast: By 2028, insurers adopting Insuretech solutions are expected to achieve up to 30% reduction in claims settlement time and 25% operational cost optimization.

Emerging Technologies: Artificial intelligence and machine learning, blockchain-based smart contracts, and IoT-enabled usage-based insurance platforms.

Regional Leaders: North America projected at USD 980 Million by 2032 with strong AI adoption; Europe at USD 710 Million driven by regulatory-backed digital insurance frameworks; Asia-Pacific at USD 620 Million supported by mobile-first insurance platforms.

Consumer/End-User Trends: Rising adoption among retail policyholders, SMEs, and gig economy workers, with increased preference for app-based policy management and real-time claims tracking.

Pilot or Case Example: In 2024, a U.S.-based insurer deployed AI-driven claims automation, achieving a 35% reduction in manual claim reviews and a 28% improvement in customer satisfaction scores.

Competitive Landscape: Lemonade holds an estimated 9% share, followed by ZhongAn, Hippo Insurance, Oscar Health, and Root Insurance.

Regulatory & ESG Impact: Data protection regulations, open insurance initiatives, and ESG-aligned risk assessment tools are shaping product design and technology deployment.

Investment & Funding Patterns: Over USD 10.2 Billion invested globally during 2023–2024, with increasing focus on Series B and C funding for scalable digital platforms.

Innovation & Future Outlook: Expansion of embedded insurance models, cross-platform integrations, and predictive analytics-driven risk pricing are expected to define the next growth phase.

The Insuretech market spans key industry sectors including life, health, property & casualty, and specialty insurance, with property & casualty contributing approximately 38% of solution deployments, followed by health insurance at 31%. Recent innovations such as AI-based fraud analytics, real-time risk scoring, and blockchain-enabled claims validation are reshaping operational models. Regulatory digitization initiatives and data governance frameworks continue to support adoption, while economic factors such as rising insurance penetration in emerging economies are boosting demand. Regionally, North America and Europe lead in platform maturity, while Asia-Pacific shows the fastest growth driven by mobile usage and micro-insurance models. Looking ahead, increased convergence of Insuretech with fintech, healthtech, and mobility platforms is expected to accelerate product personalization and ecosystem-based insurance offerings.

The strategic relevance of the Insuretech Market is increasingly tied to insurers’ ability to modernize legacy operations while maintaining regulatory compliance, cost efficiency, and customer trust. Insuretech solutions are now embedded across underwriting, claims management, fraud detection, and policy administration, enabling insurers to shift from reactive risk coverage to predictive risk prevention. AI-driven underwriting platforms deliver approximately 35% improvement in risk assessment accuracy compared to traditional rule-based underwriting standards, directly influencing loss ratios and capital efficiency.

From a regional perspective, North America dominates in transaction volume, while Asia-Pacific leads in digital adoption with over 62% of insurance customers using mobile-first or app-based insurance platforms. Europe remains a benchmark region for regulatory-aligned innovation, with more than 55% of insurers deploying GDPR-compliant data analytics and open insurance APIs. In the short term, by 2027, AI-powered claims automation is expected to cut average claims settlement cycles by nearly 30%, improving customer retention and reducing administrative overheads.

Compliance and ESG considerations are becoming integral to Insuretech strategies. Firms are committing to ESG metrics such as 40% paperless policy processing and 25% reduction in operational carbon emissions by 2028 through cloud migration and digital documentation. A measurable micro-scenario emerged in 2024, when a U.S.-based insurer implemented AI-led fraud detection, achieving a 32% reduction in fraudulent claims within twelve months. Looking ahead, the Insuretech Market is positioned as a critical pillar of resilience, regulatory alignment, and sustainable growth as insurers adapt to digital risk ecosystems and evolving consumer expectations.

Digital automation is a primary growth driver for the Insuretech Market, as insurers seek to streamline operations and reduce processing inefficiencies. Automated underwriting and claims platforms have reduced manual intervention by up to 45% across early-adopting insurers, enabling faster policy issuance and claims resolution. AI-driven document processing tools now handle over 70% of standard claims documentation in mature markets, significantly lowering error rates. Insurers deploying workflow automation report improvements of 25–30% in employee productivity, allowing skilled resources to focus on complex risk evaluation and customer engagement. Additionally, robotic process automation is being widely used for compliance reporting and policy renewals, supporting scalability without proportional cost increases. These efficiency gains are directly encouraging broader Insuretech adoption across mid-sized and large insurance carriers.

Despite strong growth momentum, data security and integration challenges remain significant restraints for the Insuretech Market. Insurance systems manage large volumes of sensitive personal and financial data, making them prime targets for cyberattacks. In 2024, over 30% of insurers globally reported at least one significant cybersecurity incident linked to third-party technology integrations. Legacy core systems also present integration barriers, with nearly 40% of insurers citing incompatibility issues when deploying cloud-based Insuretech platforms. Compliance with data localization and privacy regulations further complicates cross-border data usage. These challenges increase implementation timelines and technology costs, slowing adoption among risk-averse insurers and smaller regional players.

Embedded and usage-based insurance models present substantial opportunities within the Insuretech Market. Integration of insurance offerings into digital ecosystems such as e-commerce, mobility platforms, and financial apps has expanded insurance touchpoints beyond traditional channels. Usage-based insurance powered by IoT and telematics now supports real-time risk monitoring, with adoption growing across automotive and health insurance segments. Insurers leveraging behavioral data have achieved up to 20% improvement in pricing accuracy and customer retention. Emerging markets are also embracing micro-insurance platforms, enabling low-cost, short-duration coverage for underserved populations. These models create new distribution pathways and product innovation opportunities without relying on conventional agency networks.

Regulatory complexity and skilled workforce shortages pose ongoing challenges to the Insuretech Market. Insurance regulations vary significantly across jurisdictions, requiring localized compliance customization that increases development and maintenance costs. More than 45% of Insuretech providers report delays in product launches due to regulatory approvals and audits. Additionally, demand for AI engineers, data scientists, and cybersecurity specialists exceeds supply, driving up operational costs. Smaller Insuretech firms often struggle to attract experienced talent capable of navigating both technology and insurance compliance requirements. These challenges can limit scalability and slow innovation cycles, particularly for emerging providers operating across multiple regions.

Expansion of AI-Driven Claims Automation and Fraud Analytics: Insurers are increasingly deploying AI and machine learning to automate claims handling and detect fraud in real time. More than 65% of large insurers now use AI-based claims triage systems, reducing manual reviews by nearly 40%. Advanced fraud analytics platforms analyze over 90% of incoming claims data automatically, helping insurers achieve up to 30% reduction in false payouts and significantly faster settlement cycles.

Growth of Embedded and API-Enabled Insurance Distribution: Embedded insurance is becoming a core Insuretech trend, with over 50% of digital insurers integrating APIs into e-commerce, fintech, and mobility platforms. API-based distribution has shortened policy issuance times by nearly 45% compared to traditional channels. In digital-native markets, close to 35% of new personal insurance policies are now issued through non-insurance platforms, reflecting changing customer acquisition models.

Rising Adoption of Usage-Based and Behavior-Driven Insurance Models: Usage-based insurance supported by IoT, telematics, and wearable devices is gaining traction across auto and health insurance segments. Approximately 42% of auto insurers have launched telematics-enabled products, capturing real-time driving data from millions of vehicles. These models have improved risk pricing accuracy by around 20% and increased customer engagement levels by more than 25% through personalized premium adjustments.

Acceleration of Cloud-Native Core Insurance Platforms: Cloud migration is reshaping Insuretech infrastructure strategies, with over 70% of new insurance platforms now deployed on cloud-native architectures. Cloud-based core systems have reduced system downtime by nearly 35% and improved scalability for peak transaction volumes by over 50%. Insurers leveraging cloud infrastructure also report 30% faster product launches, supporting rapid innovation and regulatory updates.

The Insuretech market segmentation reflects the increasing specialization of digital solutions across insurance value chains, structured primarily by type, application, and end-user adoption. By type, software platforms and analytics-driven solutions dominate due to their scalability and integration with core insurance systems, while services-based offerings support customization and regulatory alignment. Application-wise, underwriting and claims management remain central, supported by measurable efficiency gains and automation depth, while fraud detection and customer engagement applications are expanding rapidly. From an end-user perspective, large insurance carriers lead adoption due to scale and capital availability, while SMEs and digital-first insurers represent a high-growth segment driven by cloud-native deployment models. Across all segments, adoption patterns are influenced by regulatory readiness, data maturity, and digital customer penetration, making segmentation analysis critical for strategic positioning and investment planning.

The Insuretech market by type is broadly categorized into software platforms, services, and enabling technologies such as analytics engines and integration middleware. Software-based Insuretech platforms represent the leading segment, accounting for approximately 46% of total adoption, supported by their role in underwriting automation, claims processing, and policy administration. These platforms offer configurable, cloud-native architectures that reduce manual workflows by over 40%. Services-based Insuretech solutions, including system integration, compliance customization, and managed analytics, hold nearly 32% share and are essential for legacy system modernization. Enabling technologies such as AI engines, data orchestration tools, and API gateways collectively account for the remaining 22%, serving niche but high-impact use cases.

Among these, AI-powered analytics platforms are the fastest-growing type, expanding at an estimated 18.5% CAGR, driven by increasing demand for real-time risk scoring and fraud detection. Growth is supported by insurers processing over 80% of structured and unstructured data through analytics layers.

By application, underwriting and risk assessment constitute the leading Insuretech segment, representing nearly 38% of total deployments. This dominance is supported by measurable gains such as 30–35% improvement in pricing accuracy and faster policy issuance. Claims management applications follow closely with around 29% share, leveraging automation to cut average settlement timelines by nearly one-third. Fraud detection and prevention applications account for approximately 18%, while customer engagement, distribution, and policy servicing collectively contribute the remaining 15%.

Claims automation is the fastest-growing application area, expanding at an estimated 17.2% CAGR, fueled by increasing claim volumes and rising expectations for instant settlement. Digital claims tools now process more than 70% of low-complexity claims without human intervention.

From an end-user perspective, large insurance enterprises dominate Insuretech adoption, accounting for approximately 52% of total usage. These organizations leverage scale to deploy end-to-end digital platforms across underwriting, claims, and compliance, often integrating multiple Insuretech vendors. Mid-sized insurers and regional carriers represent about 28% of adoption, focusing on modular solutions to improve efficiency without full system replacement. SMEs, digital-only insurers, and insurtech startups collectively contribute the remaining 20%, but this segment shows the highest growth momentum.

Digital-first insurers and SMEs are the fastest-growing end-user group, expanding at an estimated 19.1% CAGR, driven by cloud-native operations and lower infrastructure barriers. Adoption rates among this group exceed 45% for API-based distribution and embedded insurance models.

North America accounted for the largest market share at 41.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.9% between 2025 and 2032.

North America’s leadership is supported by high enterprise-level digital insurance adoption, with over 72% of insurers deploying AI-based underwriting or claims platforms. Europe follows with nearly 27.4% share, driven by regulatory-backed digital compliance and open insurance frameworks. Asia-Pacific holds approximately 22.6% share, but leads in mobile-first adoption, with more than 60% of policyholders interacting through apps or digital wallets. South America and the Middle East & Africa collectively account for around 8.2%, supported by improving digital infrastructure, rising insurance penetration, and government-backed fintech and insurtech initiatives. Regional dynamics highlight strong contrasts between mature enterprise deployments and high-growth consumer-led digital ecosystems.

The market holds approximately 41.8% share, making it the largest regional contributor. Demand is driven primarily by health, property & casualty, automotive, and commercial insurance sectors, where automation and analytics are mission-critical. Regulatory bodies continue to support digital insurance through sandbox programs and updated data governance frameworks. Over 70% of insurers in the region operate cloud-native core systems, and more than 65% use AI for fraud detection. A notable local player, Lemonade, leverages AI-based claims bots that process simple claims in under 5 minutes, significantly improving customer experience. Consumer behavior shows high enterprise and retail digital adoption, with nearly 58% of customers preferring fully digital policy servicing, particularly in healthcare and financial insurance products.

Europe accounts for nearly 27.4% of the global Insuretech market, with the UK, Germany, and France representing over 65% of regional deployments. Regulatory bodies emphasize transparency and explainability, driving demand for AI models aligned with compliance requirements. More than 55% of European insurers deploy explainable AI tools for underwriting and pricing. Sustainability initiatives encourage paperless operations, with digital documentation adoption exceeding 60% across major markets. A regional player such as ZhongAn Europe focuses on modular insurance APIs to support cross-border digital products. Consumer behavior reflects higher trust in compliant and transparent platforms, with regulatory pressure accelerating adoption of auditable and interpretable Insuretech solutions.

Asia-Pacific ranks third by volume with about 22.6% share, but leads in growth momentum. China, India, and Japan together account for over 70% of regional consumption. Mobile penetration exceeds 75%, supporting app-based insurance distribution and micro-insurance models. Cloud infrastructure investments have increased platform scalability, with over 60% of insurers deploying cloud-native solutions. Innovation hubs in China and India drive AI underwriting and embedded insurance. A leading regional player, ZhongAn, processes over 90% of policies digitally without human intervention. Consumer behavior is shaped by e-commerce and mobile AI apps, with nearly 62% of users purchasing or managing insurance through smartphones.

South America holds approximately 5.1% of the global Insuretech market, led by Brazil and Argentina. Growth is supported by expanding digital payment infrastructure and rising insurance penetration. Government initiatives promoting fintech innovation have increased API-based insurance integrations by nearly 40% over recent years. Local players focus on micro-insurance and usage-based products tailored to regional income profiles. Digital claims platforms have reduced processing times by around 25%. Consumer behavior is strongly tied to language localization and simplified digital interfaces, with over 48% of users engaging through mobile platforms rather than traditional agents.

The Middle East & Africa region represents about 3.1% of the global market, with the UAE and South Africa as primary growth centers. Demand is linked to sectors such as construction, health, and energy insurance. Governments promote digital transformation through smart city initiatives and fintech partnerships. More than 50% of insurers in leading markets have adopted cloud-based policy administration. A UAE-based Insuretech firm has implemented AI claims automation achieving a 30% reduction in settlement time. Consumer behavior varies widely, with strong uptake among urban digital users and growing demand for mobile-based insurance solutions.

United States Insuretech Market – 34.6% share

Dominance driven by large-scale insurance enterprises, advanced AI deployment, and high digital consumer adoption.

China Insuretech Market – 14.8% share

Leadership supported by mobile-first insurance platforms, high transaction volumes, and extensive embedded insurance ecosystems.

The Insuretech market features a moderately fragmented yet rapidly consolidating competitive landscape, shaped by the coexistence of digital-native Insuretech firms, incumbent insurers with proprietary platforms, and specialized technology providers. Globally, there are over 450 active Insuretech companies, with nearly 60% focused on software platforms and analytics, 25% on distribution and embedded insurance models, and the remainder on niche areas such as fraud detection and compliance automation. The top five companies collectively account for approximately 38–40% of total solution deployments, indicating increasing concentration as larger players scale through acquisitions and strategic alliances.

Competition is driven by rapid innovation cycles, with more than 70% of leading players releasing at least one major platform upgrade or new module annually. Strategic partnerships between insurers and technology firms have increased by nearly 45% since 2022, particularly in AI underwriting, claims automation, and API-based distribution. Mergers and acquisitions remain active, with mid-sized Insuretech firms acquiring niche AI or data orchestration startups to strengthen end-to-end offerings. Cloud-native architecture, explainable AI, and cybersecurity-by-design are now baseline competitive requirements, while differentiation increasingly comes from speed-to-market, regulatory adaptability, and scalability across regions. Overall, competitive intensity continues to rise as enterprises prioritize vendors capable of delivering measurable efficiency improvements and compliance-ready digital transformation.

Lemonade, Inc.

ZhongAn Online P&C Insurance

Hippo Insurance

Oscar Health

Root Insurance

Clover Health

Metromile

Next Insurance

PolicyBazaar

Tractable

Shift Technology

Wefox

Bright Health Group

Technology adoption remains the central force shaping operational models and competitive differentiation in the Insuretech Market. Artificial intelligence and machine learning are widely deployed across underwriting, claims management, and fraud detection, with more than 68% of insurers using AI-based risk scoring engines to process structured and unstructured data. These systems improve underwriting accuracy by approximately 30–35% and reduce manual intervention in claims workflows by nearly 40%. Natural language processing is increasingly used to automate customer interactions, enabling chatbots and virtual assistants to handle over 60% of routine service requests without human support.

Cloud computing continues to transform core insurance infrastructure. Over 70% of newly implemented insurance platforms are cloud-native, allowing insurers to scale transaction volumes by more than 50% during peak demand periods. Cloud-based systems also reduce system downtime by around 35%, supporting continuous operations and faster product updates. API-led architectures further enable integration with third-party data providers, payment gateways, and embedded insurance partners, with nearly 65% of insurers now operating open API frameworks.

Blockchain and distributed ledger technologies are emerging as secure solutions for claims validation and policy administration. Pilot deployments show smart contracts automating up to 25% of low-complexity claims, improving transparency and auditability. Internet of Things technologies, including telematics and wearable devices, are increasingly used in usage-based insurance, capturing real-time data from millions of connected devices and improving pricing precision by nearly 20%. Collectively, these technologies are redefining the Insuretech Market by enhancing efficiency, compliance readiness, and customer-centric digital experiences.

• In August 2024, ZestyAI’s Z-WATER™ non-weather water risk model was greenlit for use in underwriting and rating in Illinois, Indiana, Iowa, Louisiana, and Wisconsin, enabling insurers to set property-specific rates for interior water damage with up to 18× greater accuracy than traditional models. (FF News | Fintech Finance)

• In September 2025, Lemonade Inc. reduced its reinsurance cession from 55% to 20% for new and renewing policies, allowing the company to retain a larger share of premiums while reinsurers assume less risk, reinforcing strategic capital retention and underwriting control. (Insurance Business)

• In Q3 2025, Lemonade reported an improvement in claims handling efficiency—nearly tripling automation efficiency—while in-force premiums grew 30% year-over-year, highlighting accelerated digital operations and enhanced AI deployment in claims and pricing. (Insurance Journal)

• In November 2025, ZestyAI expanded regulatory acceptance of its Severe Convective Storm Suite (Z-HAIL, Z-WIND, Z-STORM) into six additional U.S. states (West Virginia, Georgia, South Dakota, Montana, Oregon, Utah), bringing the total number of states where these AI risk models can be used in filings to 29, illustrating broad regulatory integration of advanced storm risk analytics. (Insurance Innovation Reporter)

The Insuretech Market Report encompasses a comprehensive analysis of digital transformation within the insurance technology landscape, covering all major solution categories, emerging technologies, and deployment models. The scope includes segmentation by product types such as AI-based underwriting platforms, claims automation tools, fraud detection and analytics systems, API management and integration solutions, and cloud-native core insurance platforms. Application coverage spans underwriting, pricing, claims lifecycle management, customer engagement, distribution and embedded insurance offerings, and regulatory compliance automation.

Geographically, the report examines performance and trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights into regulatory variations, consumer behavior patterns, and regional innovation hubs. It highlights technology adoption rates—including AI, machine learning, IoT telematics, and blockchain-enabled solutions—and assesses their influence on operational efficiency, risk profiling precision, and product delivery scalability. Industry focus areas also extend into niche segments such as usage-based insurance, micro-insurance platforms, and parametric products tailored to weather and non-weather risks.

The report further maps competitive dynamics, profiling active global players, strategic partnerships, and notable mergers that are shaping the market’s trajectory. It addresses ecosystem enablers including cloud service providers and analytics vendors, as well as end-user insights from insurers, reinsurers, brokers, and digital distribution partners. Emerging trends such as generative AI integration, real-time underwriting, and explainable risk models are examined to offer decision-makers clarity on future demand drivers and innovation pathways.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 900.62 Million |

Market Revenue in 2032 | USD 2497.86 Million |

CAGR (2025 - 2032) | 13.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Lemonade, Inc. , ZhongAn Online P&C Insurance, Hippo Insurance, Oscar Health, Root Insurance, Clover Health, Metromile, Next Insurance , PolicyBazaar, Tractable, Shift Technology , Wefox, Bright Health Group |

Customization & Pricing | Available on Request (10% Customization is Free) |