Reports

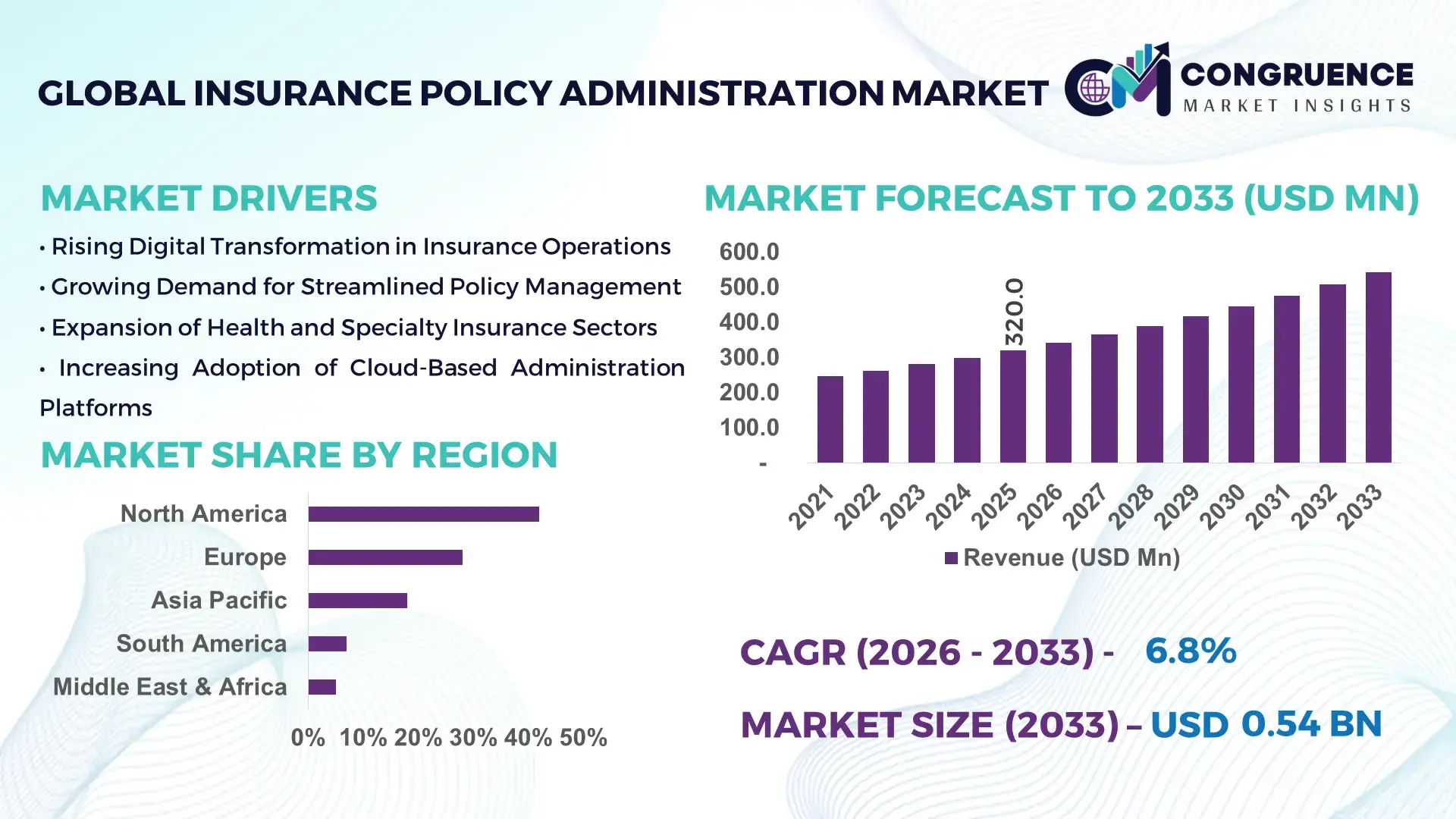

The Global Insurance Policy Administration Market was valued at USD 320.0 Million in 2025 and is anticipated to reach a value of USD 541.7 Million by 2033, expanding at a CAGR of 6.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing adoption of digital solutions and automation in insurance operations.

The United States leads the Insurance Policy Administration Market with advanced production capacity and high levels of investment in modern insurance platforms. Key applications include life insurance, health insurance, and property & casualty segments, supported by sophisticated cloud-based policy administration systems. Technological advancements such as AI-driven underwriting and blockchain-based policy verification are rapidly being deployed, with over 65% of large insurers adopting these systems for improved efficiency and data security.

Market Size & Growth: USD 320.0 Million in 2025, projected to USD 541.7 Million by 2033, driven by automation and digital adoption.

Top Growth Drivers: Digital transformation adoption 72%, operational efficiency improvement 65%, regulatory compliance optimization 58%.

Short-Term Forecast: By 2028, AI-driven policy administration is expected to reduce processing time by 40%.

Emerging Technologies: AI-based claim processing, blockchain-enabled policy management, cloud-native insurance platforms.

Regional Leaders: United States USD 185.0 Million, Europe USD 130.0 Million, Asia Pacific USD 95.0 Million by 2033; Europe shows rapid adoption in SMEs.

Consumer/End-User Trends: Increasing preference for online self-service platforms, with 60% of policyholders using digital portals for claims.

Pilot or Case Example: In 2025, a U.S. insurer implemented AI underwriting, reducing approval time by 38%.

Competitive Landscape: Market leader: Guidewire Software (~22%), competitors: Duck Creek Technologies, Sapiens International, FINEOS, Majesco.

Regulatory & ESG Impact: Introduction of digital compliance frameworks and data privacy regulations; insurers are increasing ESG reporting.

Investment & Funding Patterns: USD 210 Million in recent technology upgrades and venture investments in policy administration startups.

Innovation & Future Outlook: Integration of AI, cloud, and blockchain to drive process efficiency, enhance customer experience, and reduce manual errors.

Recent innovations in the Insurance Policy Administration Market focus on cloud-native platforms and AI-enabled automation, driving growth across life, health, and P&C insurance sectors. Regulatory support, digital adoption, and emerging analytics tools are transforming operations, with regional variations in adoption intensity. Market participants are investing in scalable, high-security platforms, enabling faster claims processing, policy management, and risk assessment.

The Insurance Policy Administration Market is increasingly critical for operational efficiency and regulatory compliance. Cloud-native platforms deliver 35% faster processing times compared to legacy on-premise systems. The United States dominates in volume, while Europe leads in adoption with 60% of insurers implementing AI-driven policy management solutions. By 2028, predictive analytics and AI are expected to reduce claim processing errors by 45%, while ESG initiatives are driving insurers to achieve a 30% reduction in paper-based policy management by 2030. In 2025, a leading U.S. insurer achieved a 38% reduction in approval time through AI-assisted underwriting initiatives. The market is positioned as a pillar of resilience, compliance, and sustainable growth, integrating emerging technologies with robust regulatory frameworks to enhance operational efficiency and customer experience.

The Insurance Policy Administration Market is shaped by rapid digital transformation, increasing demand for efficiency, and stringent regulatory requirements. Automation and cloud adoption are driving operational improvements, while AI and blockchain technologies are streamlining policy management, claims processing, and fraud detection. The market is influenced by evolving consumer preferences for digital self-service and seamless policy experiences. Insurers are increasingly deploying integrated platforms to optimize workflow, enhance customer engagement, and ensure regulatory compliance, fostering a more agile, data-driven operational environment.

Digital transformation is enhancing process efficiency, with AI-enabled platforms reducing policy issuance time by up to 40% and automated workflows decreasing administrative errors by 35%. Cloud adoption allows insurers to scale operations rapidly and improve data accessibility. The integration of advanced analytics facilitates better risk assessment, while mobile and web portals are improving customer engagement. These advancements collectively accelerate operational efficiency, reduce overhead costs, and enable faster adaptation to regulatory changes, directly impacting market growth.

Many insurers still rely on legacy systems, which are costly to maintain and challenging to integrate with modern platforms. Migration to cloud or AI-driven systems can involve high initial investment and extended implementation timelines. Data interoperability issues and regulatory compliance challenges further restrict operational flexibility. Approximately 42% of insurers report integration hurdles with existing core systems, slowing adoption of innovative technologies. This limitation affects efficiency gains, reduces scalability, and increases operational risk.

The growing demand for AI-powered claims processing, blockchain-based policy verification, and cloud-native administration systems presents significant opportunities. Increasing adoption of digital channels by 60% of policyholders allows insurers to implement self-service solutions, reducing costs and improving user satisfaction. Expansion into underserved insurance segments, such as microinsurance and specialized health policies, creates new revenue avenues. Strategic partnerships and investments in insurtech startups offer additional scope for technological advancement and market expansion.

Strict data protection regulations require insurers to invest in secure, compliant platforms. Cybersecurity threats pose risks of sensitive policyholder data breaches, potentially incurring penalties. Compliance monitoring consumes significant operational resources, with over 45% of insurers reporting increased administrative load due to regulatory updates. High implementation costs for secure and fully integrated systems challenge smaller players, slowing technology adoption. Ensuring interoperability while maintaining compliance is an ongoing operational hurdle.

Expansion of Cloud-Based Administration Platforms: Cloud adoption increased by 55% among insurers in 2025, providing scalable infrastructure and reducing on-premise maintenance costs.

AI-Driven Underwriting and Claims Processing: AI tools improved claim approval efficiency by 38% and reduced manual processing errors by 33%, streamlining workflow.

Blockchain for Policy Security: Blockchain-enabled verification systems are being piloted in 25% of large insurers, ensuring secure and transparent policy management.

Increased Consumer Self-Service Adoption: 60% of policyholders now use digital portals for claims and policy management, driving development of mobile-first interfaces and customer-centric solutions.

The Insurance Policy Administration Market is segmented comprehensively across types, applications, and end-users, reflecting the varied requirements of the global insurance ecosystem. By type, solutions range from core policy administration platforms to modular add-ons, supporting automated claims processing, underwriting, and customer management functions. Application segmentation spans life insurance, health insurance, property & casualty, and specialty insurance, each leveraging digital tools to enhance operational efficiency and customer service. End-users include large insurers, mid-sized insurance firms, and specialized brokers, with digital adoption and workflow automation driving platform deployment. Increasing regulatory compliance, cloud adoption, and AI-based analytics are influencing segmentation, with 60% of large insurers now integrating advanced policy administration tools.

Core Policy Administration Systems currently account for 48% of adoption, making them the leading type due to their comprehensive capabilities in managing policy lifecycle operations, claims processing, and regulatory compliance. Modular Add-Ons represent 30% of the market, offering flexible integration for specific tasks like underwriting or document management. Emerging Digital Platforms, including AI-assisted and cloud-native solutions, currently contribute a combined 22% share but are witnessing rapid adoption due to automation and data analytics benefits.

In 2025, a major U.S. insurer implemented an AI-assisted policy administration module to streamline claims verification, reducing manual processing time by 35% across over 2 million active policies.

Life Insurance administration currently holds the leading share at 42%, driven by the complexity of policy management, actuarial computations, and regulatory oversight. Health Insurance is the fastest-growing application segment, supported by rising digital health initiatives and telemedicine integration, currently contributing 28% to adoption. Property & Casualty and Specialty Insurance collectively account for 30%, serving niche requirements such as risk-specific underwriting and automated claims processing. Consumer adoption trends show that in 2025, over 38% of insurance firms globally piloted AI-enabled systems for life insurance customer management. Additionally, 55% of policyholders prefer digital self-service portals for claims and policy adjustments.

According to a 2025 report, AI-powered health insurance claims platforms were deployed in over 120 hospitals across Europe, improving claims verification speed by 40% and reducing processing errors significantly.

Large insurers dominate the end-user segment with a 50% share, leveraging core administration systems to manage extensive policy portfolios efficiently. Mid-Sized Insurance Firms are the fastest-growing end-users, driven by digital adoption and automation, currently representing 28% of system deployments. Brokers and specialty insurers account for a combined 22%, using policy administration platforms for tailored services, compliance management, and customer engagement. Industry adoption rates indicate that 60% of top-tier insurance companies have integrated cloud-native solutions, while 45% of mid-sized insurers are piloting AI modules to improve processing efficiency.

In 2025, a Gartner study reported that AI adoption among mid-sized health insurers increased by 25%, enabling over 300 firms to reduce claim processing times and enhance customer service delivery.

North America accounted for the largest market share at 42% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

In North America, the market encompasses over 1,200 insurance firms, with more than 60% of large insurers implementing cloud-based and AI-driven policy administration systems. Europe follows closely with a 28% share, driven by Germany, the UK, and France, where regulatory compliance and digital workflow adoption are critical. Asia-Pacific, including China, India, and Japan, represents 18% of the market by volume, fueled by mobile AI adoption and fintech integration. South America and Middle East & Africa contribute 7% and 5%, respectively, with Brazil, Argentina, UAE, and South Africa leading regional deployment. Across regions, adoption varies: North America emphasizes enterprise-scale automation in healthcare and finance, Europe focuses on explainable policy administration solutions, and Asia-Pacific prioritizes mobile-first platforms.

North America holds a 42% share of the global Insurance Policy Administration Market, with major demand driven by healthcare, finance, and life insurance sectors. Key regulatory changes, including enhanced data privacy and digital compliance mandates, have accelerated adoption of cloud-based and AI-powered platforms. Technological advancements such as predictive analytics, machine learning for claims automation, and blockchain-enabled policy verification are becoming standard. Local players, like Guidewire Software, are expanding modular offerings to enable real-time claims processing and policy lifecycle management. Regional consumer behavior shows higher adoption among large insurers seeking efficiency in healthcare and finance, with over 65% of enterprise users preferring automated self-service portals.

Europe represents 28% of the Insurance Policy Administration Market, with Germany, the UK, and France leading adoption. Regulatory frameworks such as GDPR and Solvency II drive demand for secure, explainable policy administration systems. Emerging technologies, including AI-assisted underwriting, blockchain verification, and cloud-native platforms, are widely integrated. Local players like Sapiens International are enhancing SaaS solutions to meet regulatory and sustainability standards. Regional consumers show strong preference for transparency and regulatory compliance, with 58% of insurers implementing AI-assisted reporting tools, ensuring secure policy management across both life and property & casualty lines.

Asia-Pacific accounts for 18% of the market, with top-consuming countries including China, India, and Japan. Infrastructure trends emphasize cloud migration and digital insurance hubs, while technology adoption focuses on AI-powered customer portals and mobile-first policy management systems. Local players, such as ZhongAn Online, are leveraging AI to automate claims processing and improve customer onboarding. Regional consumer behavior is influenced by mobile penetration and digital literacy, with 62% of policyholders preferring mobile-enabled self-service policy platforms. Insurance firms are also investing in regional innovation centers to integrate fintech solutions and streamline workflow efficiency.

South America contributes 7% of the global Insurance Policy Administration Market, with Brazil and Argentina as leading countries. Demand is driven by insurance modernization in banking, media, and energy sectors. Infrastructure trends include digital policy workflows and AI-based claims management. Government incentives for fintech and digital insurance adoption support market expansion. Local players, such as Porto Seguro, are implementing automated claims processing systems, reducing turnaround times by over 30%. Consumer behavior emphasizes digital portals for language-localized policy management, with over 50% of policyholders preferring mobile access.

Middle East & Africa accounts for 5% of the global market, with major growth countries including the UAE and South Africa. Demand is supported by oil & gas, construction, and financial services sectors. Technological modernization includes adoption of cloud-based systems, AI for policy lifecycle automation, and blockchain for secure verification. Local regulations and trade partnerships incentivize digital adoption and compliance. Regional consumer behavior reflects preference for digital solutions in urban centers, with 48% of insurance policyholders using online portals. Players like Sanlam South Africa are deploying AI-enabled policy management to reduce manual interventions and improve efficiency.

United States – 42% Market Share: High production capacity, strong enterprise adoption, and advanced technology integration drive leadership in policy administration.

Germany – 14% Market Share: Extensive regulatory framework and widespread adoption of digital and AI-assisted insurance solutions support market dominance.

The Insurance Policy Administration Market is moderately consolidated with a competitive landscape featuring over 50 active global competitors providing a range of core systems, modular solutions, and cloud-native platforms. The top five companies collectively hold around 58–62% of deployment footprints among large insurers, reflecting a balance between established leaders and emerging InsurTech challengers. Key incumbents like Guidewire Software, Duck Creek Technologies, Insurity, Sapiens International, and SS&C Technologies are intensifying competition through strategic initiatives such as cloud migration partnerships, modular product launches, and integration of AI capabilities to enhance policy lifecycle automation, underwriting analytics, and claims processing efficiency. Several mid‑tier players such as DXC Technology and Majesco are pursuing platform modernization with AI‑enabled SaaS solutions that are being adopted by mid‑sized and regional carriers, contributing to broader competitive pressure.

Innovation trends reveal strong focus areas including predictive analytics, low‑code/no‑code configuration tools, API‑first architectures, and blockchain‑based verification modules, leading to differentiation beyond legacy core systems. Partnerships between technology integrators (e.g., Accenture with core platform vendors) and cloud hyperscalers are reshaping service delivery models, while smaller, agile InsurTech startups are carving niches with specialized automation workflows and user‑centric interfaces. The market’s competitive environment is dynamic, with annual contract growth rates for leading platforms exceeding 20% among early adopters, indicating robust demand for modern policy administration solutions in both property & casualty and life insurance segments.

Sapiens International Corporation

SS&C Technologies

DXC Technology

Majesco

SAP SE

Microsoft Corporation

Oracle Corporation

Cognizant

FurtherAI

BriteCore

Openkoda

Vertafore

Regure

The Insurance Policy Administration Market is experiencing rapid technological evolution driven by digital transformation, automation, and data‑centric decisioning. Cloud‑native architectures are redefining deployment models, with many carriers shifting from on‑premise core systems to scalable SaaS platforms that support real‑time updates, integrated data stores, and multi‑tenant environments. This shift enhances resilience, reduces IT overhead, and enables insurers to onboard new products and services faster. In tandem, artificial intelligence and machine learning are being embedded into core workflows such as automated underwriting, predictive risk profiling, and intelligent claims adjudication, reducing manual intervention and accelerating throughput across millions of policies. Policy administration solutions are leveraging natural language processing (NLP) and large language models to process unstructured documents, interpret policy clauses, and assist agents in handling complex customer queries with high accuracy and reduced turnaround times.

Integration of APIs and open ecosystems is enabling insurers to connect policy administration platforms with external data sources including telematics, IoT devices, and third‑party analytics, enriching risk models and improving personalization of offerings. Platforms are increasingly adopting low‑code and no‑code configuration tools to empower business users to adapt workflows without heavy reliance on development teams, accelerating time‑to‑value for insurers. Another emerging area is blockchain and distributed ledger technologies, which are being explored for secure, auditable transaction records and privacy‑preserving claim automation, especially in multi‑party ecosystems. Additionally, cybersecurity enhancements, such as multi‑factor authentication and encryption‑at‑rest/in‑transit, are becoming foundational requirements in modern administration systems given the sensitivity of policyholder data. The combined effect of these technologies is driving improved operational efficiency, enhanced customer experiences, and stronger compliance capabilities for insurance carriers and their ecosystem partners.

• In September 2025, Guidewire Software Inc. was recognized as a Leader in the 2025 Gartner Magic Quadrant for SaaS P&C Core Platforms, North America, with its InsuranceSuite placed highest for Ability to Execute and furthest for Completeness of Vision, reinforcing its cloud and AI‑enabled core platform market position. Source: www.businesswire.com

• In May 2025, insurers increasingly migrated to the Guidewire Cloud platform for core modernization, with many carriers replacing legacy on‑premise systems with modular, cloud‑based policy administration solutions to enhance scalability, agility, and customer personalization. Source: www.businesswire.com

• In May 2025, Duck Creek Technologies’ Formation ’25 conference hosted nearly 800 industry professionals, showcasing the company’s advancements in AI‑powered platforms and cloud‑native solutions reshaping underwriting, claims, and customer engagement processes. Source: www.duckcreek.com

• In March 2025, Accenture expanded its strategic partnership with Guidewire Software to accelerate cloud‑based policy administration deployments for property and casualty insurers, combining Accenture’s transformation capabilities with Guidewire’s core platform offerings.

The Insurance Policy Administration Market Report provides a comprehensive examination of the insurance technology ecosystem, covering key solution types, application domains, deployment models, and end‑user segments. It spans both property & casualty and life insurance administration systems, detailing features such as policy lifecycle management, billing modules, claims integration, and compliance workflows. Geographic coverage includes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with insights into regional adoption patterns, technology readiness levels, and regulatory influences shaping market behavior.

The report analyzes product types including core policy administration platforms, modular add‑ons, cloud‑native SaaS solutions, and API‑first architectures, outlining their roles in supporting automated underwriting, real‑time data processing, and intelligent customer engagement. Application segments are detailed across life, health, property & casualty, and specialty insurance lines, with emphasis on digital transformation priorities in each. End‑user insights cover large insurers, mid‑sized carriers, brokers, and InsurTech firms, noting adoption drivers such as operational efficiency, customer self‑service demand, and risk management optimization. Emerging niche segments such as AI‑powered policy analytics, mobile policy servicing apps, and blockchain‑enabled verification services are included to illustrate future technology inflection points.

Additionally, the report addresses competitive dynamics, profiling leading global players, innovation trends, partnerships, and product launches that influence strategic decision‑making. It also examines ecosystem enablers such as cloud infrastructure providers, integration partners, and regulatory frameworks that drive platform modernization. This broad scope offers decision‑makers actionable insights into market segmentation, technology evolution, and strategic investment opportunities within the Insurance Policy Administration domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 320.0 Million |

| Market Revenue (2033) | USD 541.7 Million |

| CAGR (2026–2033) | 6.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Guidewire Software Inc., Duck Creek Technologies, Insurity, Sapiens International Corporation, SS&C Technologies, DXC Technology, Majesco, SAP SE, Microsoft Corporation, Oracle Corporation, Cognizant, FurtherAI, BriteCore, Openkoda, Vertafore, Regure |

| Customization & Pricing | Available on Request (10% Customization Free) |