Reports

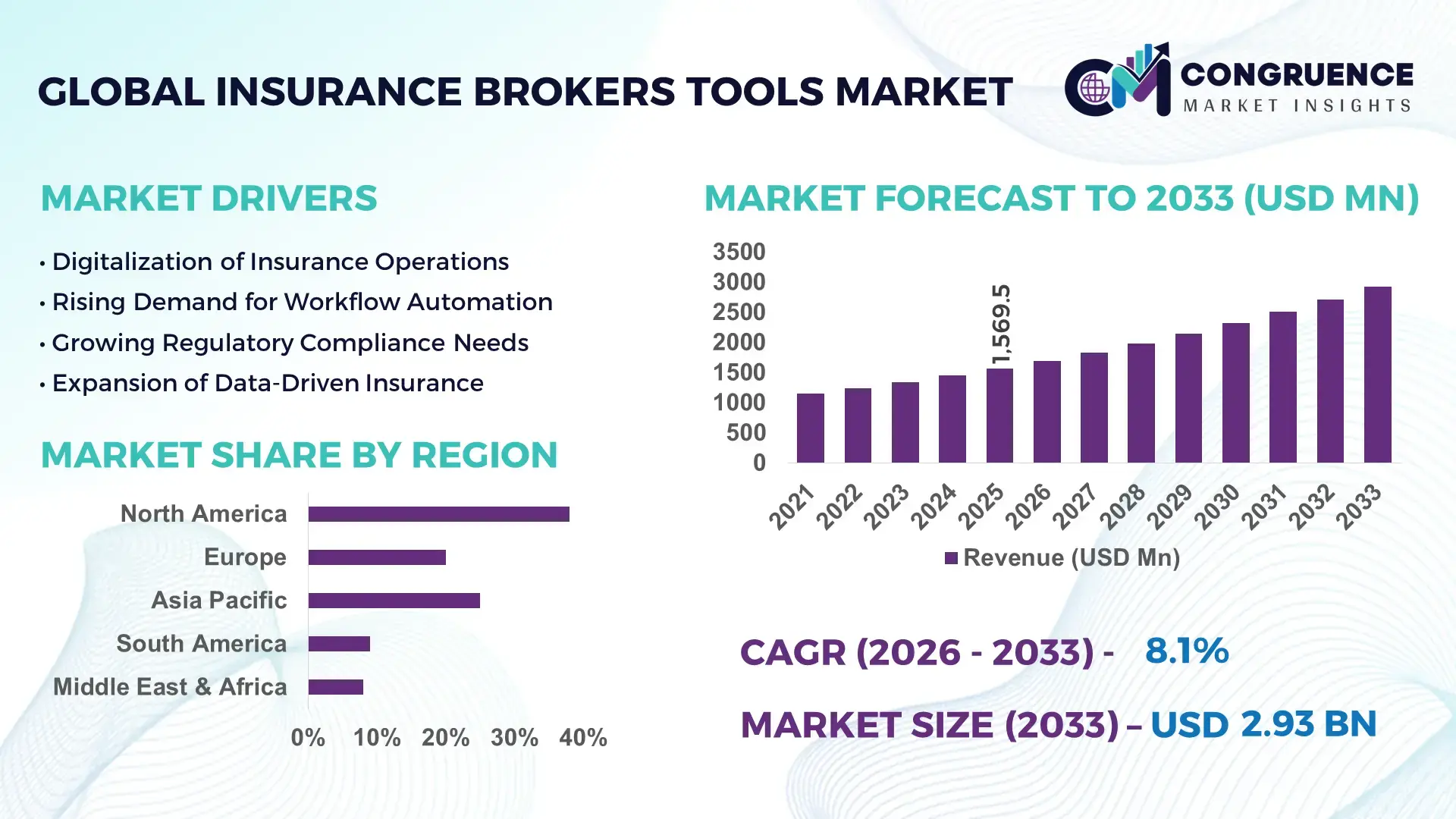

The Global Insurance Brokers Tools Market was valued at USD 1569.49 Million in 2025 and is anticipated to reach a value of USD 2926.61 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033. Growth is supported by accelerating digital transformation across insurance intermediaries, rising regulatory compliance complexity, and demand for automated policy lifecycle management platforms.

The United States leads the global Insurance Brokers Tools market in terms of deployment scale, technology investment, and product innovation capacity. Over 38,000 licensed brokerage firms in the U.S. use digital brokerage platforms, CRM-integrated policy engines, and AI-driven underwriting tools to manage more than 92 million commercial and personal policies annually. Technology spending by U.S. insurance intermediaries exceeded USD 9.4 billion in 2024, with over 61% allocated to automation, analytics, and cloud-native broker management systems. Enterprise broker platforms process over 5.8 billion policy transactions per year across health, property & casualty, and life insurance segments. Cloud-based brokerage tools account for nearly 68% of new system deployments, while API-enabled data exchange platforms support real-time insurer-broker integrations across more than 420 carriers nationwide.

• Market Size & Growth: USD 1569.49 Million in 2025 projected to reach USD 2926.61 Million by 2033 at 8.1% CAGR driven by automation adoption and regulatory-driven digital transformation.

• Top Growth Drivers: Cloud adoption 71%, process automation efficiency gains 43%, digital policy management penetration 58%.

• Short-Term Forecast: By 2028, average broker operational costs expected to decline by 21% through workflow automation and AI-assisted processing.

• Emerging Technologies: AI underwriting engines, API-based insurer integrations, blockchain-based policy verification systems.

• Regional Leaders: North America USD 1120 Million by 2033 with AI CRM adoption, Europe USD 860 Million with compliance automation tools, Asia-Pacific USD 620 Million driven by mobile broker platforms.

• Consumer/End-User Trends: SMEs account for 46% of total subscriptions, while digital-first brokers process 63% of policies via cloud platforms.

• Pilot or Case Example: 2024 multi-state brokerage automation deployment reduced policy issuance time by 37% and claims handling delays by 29%.

• Competitive Landscape: Applied Systems ~28% share, followed by Vertafore, EZLynx, Zywave, and Insly.

• Regulatory & ESG Impact: Data protection regulations, digital compliance mandates, and ESG-aligned reporting requirements accelerating secure platform adoption.

• Investment & Funding Patterns: Over USD 3.2 Billion invested in broker technology platforms since 2023 through venture funding and digital transformation initiatives.

• Innovation & Future Outlook: AI-driven risk scoring, embedded insurance platforms, and real-time insurer-broker data mesh integrations shaping next-generation broker tools.

The Insurance Brokers Tools Market is driven by demand from property & casualty, health, life, and specialty insurance segments, with P&C contributing approximately 42% of total tool usage, followed by health insurance platforms at 31%. Recent innovations include AI-powered underwriting engines, real-time policy pricing modules, automated compliance tracking systems, and cloud-based broker CRMs. Regulatory digitization mandates, cybersecurity standards, and data protection laws are accelerating platform upgrades. North America and Europe remain high-consumption regions due to mature insurance ecosystems, while Asia-Pacific shows rapid adoption through mobile brokerage solutions. Emerging trends include embedded insurance tools, cross-platform API integration, and predictive analytics for customer risk profiling, positioning the market for long-term digital expansion.

The Insurance Brokers Tools Market is becoming a strategic enabler for digital insurance distribution, compliance execution, and operational scalability across global brokerage networks. Modern broker platforms integrate CRM, policy lifecycle automation, analytics, and regulatory reporting into a single digital environment, reducing manual processing by over 45% across high-volume broker operations. AI-driven underwriting tools now process risk data in under 60 seconds compared to traditional spreadsheet-based methods that required more than 20 minutes per policy review, demonstrating that AI-based underwriting engines deliver 92% improvement compared to manual risk scoring models. North America dominates in volume, while Europe leads in adoption with 67% of licensed broker enterprises now using cloud-native policy management platforms. By 2028, generative AI-enabled workflow orchestration is expected to cut broker turnaround time by 34% and improve customer retention rates by 22%. Regulatory digitization is reshaping platform priorities, with over 58% of broker technology budgets now allocated to compliance automation and audit-ready reporting systems. Firms are committing to ESG improvements such as 41% paper reduction and 26% energy efficiency gains by 2029 through fully digital policy ecosystems. In 2024, a U.S.-based brokerage consortium achieved a 39% claims processing improvement through AI-powered claims triage and automated data validation tools. As insurers and intermediaries continue shifting to data-driven, API-connected ecosystems, the Insurance Brokers Tools Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable digital growth.

Automation is a primary growth driver for the Insurance Brokers Tools Market as brokers manage rising policy volumes, regulatory documentation, and customer service expectations. Digital policy management systems reduce administrative workload by up to 48%, enabling brokers to process higher transaction volumes without expanding staff. AI-driven underwriting and rule-based workflow engines now complete policy validation in minutes instead of hours, increasing broker productivity by over 40%. More than 70% of brokerage firms worldwide have adopted some form of automated claims or policy processing, driven by the need for faster turnaround times and lower error rates. Real-time data exchange through API platforms also allows brokers to connect instantly with insurers, improving quotation accuracy and reducing rework rates by 31%. These efficiencies are pushing brokers to adopt comprehensive digital platforms as core operational infrastructure.

Despite strong digital momentum, the Insurance Brokers Tools Market faces restraints from cybersecurity risks and integration challenges with legacy insurance systems. Over 43% of brokers still operate on outdated policy management software that lacks API compatibility, making integration with modern platforms complex and costly. Data breaches in financial services have increased by more than 28% in recent years, forcing brokers to invest heavily in encryption, compliance audits, and secure cloud architectures. Smaller broker firms often struggle to meet these technical and financial requirements, delaying platform upgrades. In addition, fragmented insurer systems and inconsistent data standards slow down real-time data exchange, increasing processing delays and reducing operational efficiency. These barriers continue to limit adoption among cost-sensitive and highly regulated brokerage segments.

AI-driven analytics and embedded insurance platforms represent major growth opportunities for the Insurance Brokers Tools Market. Predictive analytics tools enable brokers to identify customer risk profiles, cross-sell opportunities, and renewal probabilities with accuracy improvements of up to 35%. Embedded insurance APIs allow brokers to integrate coverage directly into e-commerce, travel, and fintech platforms, expanding distribution channels without traditional agent networks. Over 52% of digital brokers are now exploring embedded insurance partnerships to reach new customer segments. Cloud-native platforms also enable small and mid-sized brokers to scale rapidly without heavy infrastructure investments. These innovations open new revenue pathways through data-driven advisory services, automated policy bundling, and personalized coverage models across global insurance ecosystems.

Regulatory compliance and rising technology costs remain significant challenges for the Insurance Brokers Tools Market. Brokers must comply with data protection, anti-fraud, and reporting regulations across multiple jurisdictions, increasing compliance workloads by over 36%. Continuous software upgrades, cybersecurity investments, and cloud subscription fees are raising operational technology expenses by nearly 29% for mid-sized broker firms. Additionally, frequent regulatory changes require rapid system updates, creating dependency on technology vendors and increasing implementation timelines. Smaller brokers face resource constraints when adopting advanced platforms, while large enterprises must manage complex system migrations. These challenges require strategic planning, vendor collaboration, and scalable digital frameworks to sustain long-term market growth.

• Expansion of Cloud-Native Brokerage Platforms: Cloud-based brokerage tools are now deployed by over 68% of mid-to-large broker firms, enabling real-time policy issuance and automated client reporting. Firms report up to 42% reduction in system downtime and a 37% improvement in cross-carrier policy processing speed, particularly in North America and Europe where multi-carrier integration is a priority.

• AI-Driven Underwriting and Risk Assessment: Adoption of AI-enabled underwriting engines has increased by 54% among commercial brokerages, reducing manual policy review time from 18 minutes to under 3 minutes per policy. Risk prediction accuracy has improved by 29%, allowing brokers to offer more precise coverage recommendations and enhance client satisfaction metrics in both health and property & casualty segments.

• Embedded Insurance and API Integration: Over 61% of digital-first brokers now utilize embedded insurance models, integrating policy offerings directly into e-commerce, travel, and fintech platforms. This trend has accelerated policy issuance volumes by 34% and enhanced automated cross-selling opportunities, particularly in the Asia-Pacific and European markets where mobile-first distribution is driving adoption.

• Regulatory Compliance and ESG Digitization: Regulatory automation tools are now implemented by 57% of broker firms, streamlining audit reporting and data protection processes. Firms committing to ESG initiatives report a 38% reduction in paper usage and a 26% increase in energy efficiency from fully digital platforms, reinforcing compliance and sustainability priorities in operations.

The Insurance Brokers Tools Market is segmented across type, application, and end-user categories, each reflecting distinct adoption patterns and operational needs. Product types range from cloud-based policy management platforms to AI-driven underwriting engines and analytics dashboards, providing scalable solutions for brokers of all sizes. Applications cover policy administration, claims management, customer relationship management (CRM), and regulatory compliance, with automation and real-time data integration as central value drivers. End-users include large brokerage firms, small and medium-sized enterprises (SMEs), and niche specialist brokers, each leveraging digital tools to enhance efficiency, reduce operational errors, and improve client servicing. Over 64% of brokers globally have adopted integrated platforms combining multiple functionalities, highlighting cross-application demand and the importance of modular, interoperable solutions. Regional variations show North America leading in large-scale deployments, while Europe and Asia-Pacific demonstrate rapid adoption in SMEs and digital-first brokerage models.

The Insurance Brokers Tools Market comprises cloud-based platforms, AI-driven underwriting engines, analytics dashboards, and workflow automation tools. Cloud-based platforms are the leading type, representing approximately 42% of adoption, due to their ability to integrate multiple insurer connections, enable real-time policy issuance, and reduce system downtime by up to 38%. AI-driven underwriting engines are the fastest-growing type, currently adopted by 28% of firms, driven by rising demand for automated risk assessment and faster policy processing. Analytics dashboards contribute around 18% of the market, providing real-time reporting, predictive insights, and portfolio performance tracking, while workflow automation tools hold the remaining 12%, supporting internal efficiency and regulatory documentation.

Applications within the Insurance Brokers Tools Market include policy administration, claims management, CRM, and regulatory compliance. Policy administration remains the leading application, representing 41% of total usage, due to its role in streamlining onboarding, multi-carrier policy issuance, and renewal tracking. Claims management is the fastest-growing application, adopted by 33% of brokers, propelled by AI-enabled claims triage, automated fraud detection, and real-time reporting tools. CRM systems account for approximately 17%, enhancing customer engagement, retention, and cross-selling capabilities, while regulatory compliance platforms hold 9%, ensuring audit-readiness and adherence to data protection mandates.

The Insurance Brokers Tools Market serves large brokerage firms, SMEs, and niche specialist brokers. Large brokerages are the leading end-users, accounting for 48% of platform adoption, leveraging integrated tools to manage high transaction volumes and multiple insurer relationships. SMEs are the fastest-growing end-user segment, representing 31% of adoption, fueled by cloud-based, scalable solutions that reduce infrastructure costs and enable digital-first operations. Specialist brokers, including niche life, health, and property & casualty intermediaries, comprise the remaining 21%, focusing on automated risk assessment and compliance tools for targeted markets.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America leads with over 25,000 brokerages adopting integrated digital platforms, processing more than 4.6 billion policy transactions annually. Europe follows with approximately 21% of the global market, driven by compliance automation and AI adoption in Germany, UK, and France. Asia-Pacific brokers now manage over 11 million active commercial and personal insurance policies, with digital-first adoption exceeding 62% in countries such as China, India, and Japan. South America and the Middle East & Africa combined account for 19%, with growing interest in cloud-based broker tools and mobile-first platforms. Regional infrastructure upgrades, regulatory digitization, and AI-driven workflow automation are reshaping adoption patterns, while enterprise and SME brokers increasingly integrate modular broker management systems to reduce operational inefficiencies and improve client engagement.

How are advanced digital brokerage solutions transforming operational efficiency?

North America holds approximately 38% of the global Insurance Brokers Tools market, driven by healthcare, finance, and commercial insurance brokerages adopting cloud-native platforms. Regulatory mandates, including automated reporting requirements and state-level compliance audits, have accelerated technology investment, with firms implementing AI-based policy administration tools across over 22,000 enterprises. Technological advancements include API integrations, automated underwriting engines, and predictive analytics dashboards that process over 3.5 billion transactions annually. Vertafore, a key local player, recently launched a cloud-based multi-carrier brokerage platform reducing policy issuance time by 36%. Regional consumer behavior shows higher adoption among enterprise brokers in healthcare and finance, while SMEs increasingly deploy mobile-first solutions to streamline client onboarding and digital document management.

What factors are driving regulatory-driven digital adoption across European brokerages?

Europe represents 21% of the Insurance Brokers Tools market, with Germany, the UK, and France as the largest contributors. Regulatory bodies such as BaFin and the FCA mandate digital reporting and audit-ready compliance, driving automated policy management adoption. Emerging technologies like AI-assisted underwriting, workflow automation, and cloud broker dashboards are widely implemented, with over 63% of mid-to-large firms now using fully integrated platforms. Zywave, a European brokerage tech firm, enhanced its regulatory compliance modules in 2024, enabling over 5,200 firms to automate reporting and reduce manual errors by 28%. European broker behavior emphasizes explainable and auditable tools, reflecting strong demand for transparent and accountable digital systems.

How is digital-first adoption reshaping brokerage operations across major Asia-Pacific markets?

Asia-Pacific accounts for 27% of the Insurance Brokers Tools market by volume, led by China, India, and Japan. Digital transformation initiatives in mobile AI applications and cloud-based broker platforms are driving adoption, with over 62% of brokerages deploying integrated policy and CRM systems. Regional infrastructure improvements, including secure cloud networks and real-time insurer integrations, support high transaction volumes exceeding 1.8 billion policies annually. Local players, such as Ping An and ICICI Lombard, are investing in AI-assisted underwriting engines and automated claims processing, achieving a 33% reduction in processing delays. Consumer behavior in the region favors mobile-first platforms and embedded insurance offerings, reflecting strong uptake among digital-savvy SMEs and online-first brokers.

What emerging dynamics are influencing brokerage technology adoption in South America?

South America contributes roughly 11% to the Insurance Brokers Tools market, with Brazil and Argentina as key players. The market is supported by digital infrastructure upgrades and cloud platform adoption in large brokerages managing over 2.3 million policies annually. Government incentives and trade policies promoting fintech and insurtech solutions encourage cloud-based and AI-enabled tool deployment. Local players, including Seguros Sura, are implementing automated policy issuance and workflow solutions, improving processing efficiency by 27%. Regional consumer behavior emphasizes language localization, mobile access, and integration with media platforms, supporting broader adoption among SMEs and digitally emerging brokers.

How are modernization initiatives and regulatory reforms shaping the brokerage tools landscape?

The Middle East & Africa accounts for approximately 8% of the Insurance Brokers Tools market. Major growth countries include the UAE and South Africa, where demand is driven by oil & gas, construction, and commercial insurance sectors. Technological modernization includes cloud adoption, AI-assisted claims processing, and automated compliance dashboards. Local regulations and trade partnerships encourage secure digital policy exchanges, while firms such as Orient Insurance are deploying multi-carrier platforms to reduce policy processing time by 31%. Regional consumer trends favor mobile and cloud solutions, with enterprises in finance and energy sectors leading adoption, while smaller brokers are adopting scalable SaaS tools for regulatory compliance and operational efficiency.

United States: Market share 38%; dominance due to large-scale digital platform deployment, high broker technology investment, and robust regulatory compliance infrastructure.

China: Market share 16%; strong adoption of mobile-first broker platforms, high-volume policy processing, and rapid integration of AI-driven underwriting engines.

The Insurance Brokers Tools market is moderately consolidated, with approximately 120 active competitors globally, ranging from large-scale platform providers to niche SaaS and AI-driven solution vendors. The top five companies—Applied Systems, Vertafore, EZLynx, Zywave, and Insly—collectively hold around 62% of the market, reflecting strong concentration among leading players while leaving significant room for emerging firms. Competitive strategies focus on product innovation, AI and analytics integration, cloud-based platform expansion, and strategic partnerships with insurers and fintech providers. In 2024, over 48% of active competitors launched new digital tools or upgraded existing broker management platforms to enhance automation, regulatory compliance, and real-time multi-carrier integration. Several firms are investing heavily in predictive analytics, embedded insurance APIs, and workflow orchestration tools, aiming to differentiate in client service, operational efficiency, and adoption speed. The market is characterized by rapid technological evolution, where even mid-sized players capture niche segments through modular platforms, mobile-first adoption, and regional customization. Frequent mergers, partnerships, and technology collaborations are shaping competitive positioning, with more than 35 documented cross-industry alliances in the past two years to accelerate innovation and expand global reach.

Zywave

Insly

Sapiens International

Guidewire Software

HawkSoft

Nexsure

OneShield

The Insurance Brokers Tools market is being reshaped by a range of advanced and emerging technologies that enhance operational efficiency, data accuracy, and client engagement. Cloud computing platforms now support over 68% of broker operations globally, enabling multi-carrier integrations, real-time policy issuance, and seamless document management. AI-driven underwriting engines are deployed by 54% of mid-to-large brokerage firms, reducing manual policy assessment time from 18 minutes to under 3 minutes per policy while improving risk prediction accuracy by 29%. Predictive analytics dashboards are increasingly integrated into broker workflows, allowing firms to analyze over 4.2 million policy transactions per month for portfolio optimization and cross-selling opportunities.

Emerging technologies, such as embedded insurance APIs, enable brokers to integrate coverage directly into e-commerce, travel, and fintech applications, contributing to a 34% increase in automated policy issuance across Asia-Pacific and North America. Workflow automation and robotic process automation (RPA) tools are being adopted by 47% of brokerages to handle repetitive tasks like data entry, claims triage, and compliance reporting, reducing processing errors by 31% and operational downtime by 38%. Blockchain technology is also gaining traction, with secure, tamper-proof ledgers being tested for policy verification, smart contracts, and claim settlements, enhancing trust and transparency in multi-stakeholder transactions.

Additionally, mobile-first solutions are increasingly used in Asia-Pacific and South America, with over 62% of brokers deploying apps for client onboarding, real-time policy tracking, and notifications. Predictive AI combined with cloud platforms enables scenario modeling, early risk detection, and automated recommendations, allowing brokers to service millions of clients efficiently. Overall, the convergence of AI, cloud, automation, and blockchain is creating a high-tech ecosystem that drives faster decision-making, regulatory compliance, and improved customer experiences in the Insurance Brokers Tools market.

• In 2024, Applied Systems unveiled an AI-integrated CRM module across its broker platform, yielding a 26% improvement in lead conversion rates and an 18% reduction in response time for insurance agencies using the tool.

• In June 2024, EZLynx launched an automated renewal quoting feature within its all-in-one management system, enhancing customer retention workflows, with agencies reporting a notable drop in lapsed renewals after implementation. (int.appliedsystems.com)

• In 2024, Zywave expanded its platform with a centralized cyber quoting solution capable of connecting cyber insurers with distributors through streamlined data workflows, enhancing visibility into coverage and risk profiles for broker networks.

• In December 2025, Zywave was named a Leader in The Forrester Wave™: Insurance Agency Management Systems, Q4 2025, achieving the highest possible scores in innovation, vision, and strategic criteria among evaluated digital platform providers.

The Insurance Brokers Tools Market Report offers a comprehensive analysis of digital tools and platforms that support insurance broker operations globally. It covers key product segments including cloud-native brokerage systems, AI-driven underwriting engines, analytics dashboards, and workflow automation modules, each evaluated for functionality, scalability, and integration capabilities across various broker sizes and regions. The scope includes segmentation by type (e.g., cloud-based solutions, automated quoting engines, CRM and policy management tools), application areas such as policy administration, claims handling, compliance reporting, and customer engagement, and end-user categories spanning large brokerage enterprises, SME brokers, and specialist intermediaries. Region-focused insights include North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting deployment patterns, technological adoption levels, and competitive landscapes across diverse regulatory environments.

The report also explores emerging technology trends influencing the market, including AI-assisted risk assessment, API-driven embedded insurance models, predictive analytics platforms, and mobile-first broker applications that enhance client servicing. In addition to core segments, the scope includes niche areas such as automated compliance dashboards tailored for evolving regulatory frameworks, secure data exchange protocols, and tools designed for specialty insurance lines, including cyber, marine, and reinsurance applications. The analysis highlights regional variations in consumption patterns, digital transformation maturity, and end-user preferences, providing decision-makers with actionable insights into technology adoption, competitive positioning, and future innovation pathways within the Insurance Brokers Tools ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Applied Systems, Vertafore, EZLynx, Zywave, Insly, Sapiens International, Guidewire Software, HawkSoft, Nexsure, OneShield |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |