Reports

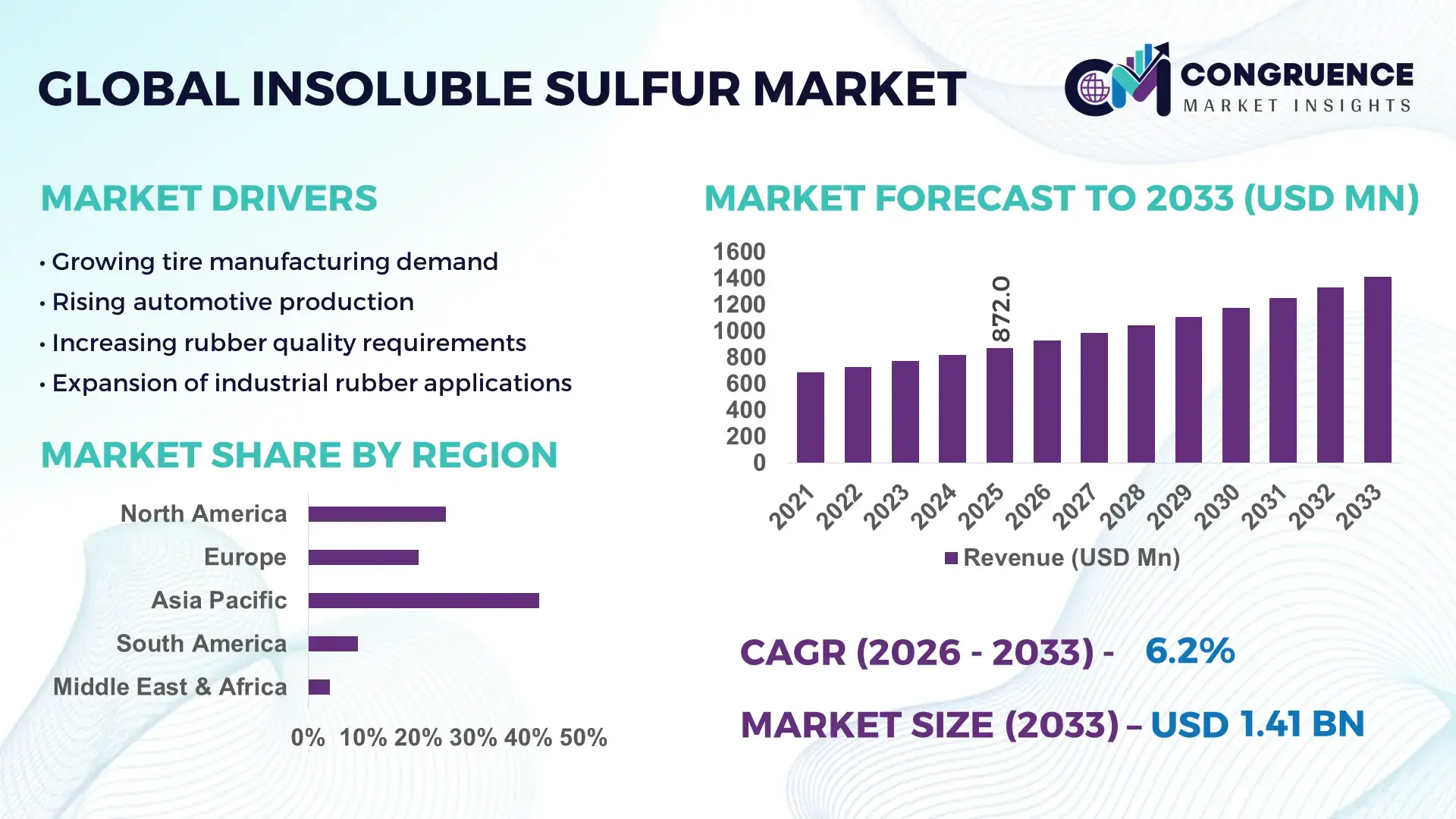

The Global Insoluble Sulfur Market was valued at USD 872 Million in 2025 and is anticipated to reach a value of USD 1410.95 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. This growth is primarily driven by the increasing demand for high-performance rubber compounds in tire manufacturing and automotive applications.

China continues to demonstrate strong industrial capacity in the insoluble sulfur market, supported by extensive chemical manufacturing infrastructure and large-scale tire production ecosystems. The country operates more than 30 dedicated sulfur processing facilities, with an estimated annual production capacity exceeding 400,000 metric tons of specialty sulfur products. Over 65% of domestic insoluble sulfur output is utilized in automotive tire applications, particularly for high-speed and radial tires. Additionally, China has increased capital investment in advanced polymer stabilization technologies by over 18% between 2022 and 2025, enabling improved thermal stability and dispersion efficiency of insoluble sulfur grades. The integration of automated processing lines has enhanced production consistency by approximately 22%, strengthening its industrial output capabilities.

Market Size & Growth: Valued at USD 872 Million in 2025 and projected to reach USD 1410.95 Million by 2033, growing at 6.2% CAGR due to expanding automotive and industrial rubber demand.

Top Growth Drivers: Tire manufacturing demand increase by 35%, rubber processing efficiency improvement by 28%, and automotive production expansion by 32%.

Short-Term Forecast: By 2028, manufacturing efficiency is expected to improve by 20% due to automation and advanced compounding techniques.

Emerging Technologies: Advanced polymer stabilization, nano-dispersion sulfur technology, and automated sulfur blending systems.

Regional Leaders: Asia-Pacific projected at USD 620 Million by 2033 with strong tire production, North America at USD 350 Million driven by performance materials adoption, Europe at USD 290 Million with sustainability-focused rubber innovations.

Consumer/End-User Trends: Automotive and tire manufacturers account for over 70% of consumption, with increasing demand for durable and heat-resistant rubber compounds.

Pilot or Case Example: In 2024, a leading tire manufacturer improved vulcanization efficiency by 18% using enhanced insoluble sulfur formulations.

Competitive Landscape: Market leader holds approximately 24% share, followed by key players including major global chemical manufacturers and specialty sulfur producers.

Regulatory & ESG Impact: Emission reduction mandates and sustainable rubber production policies are influencing adoption of eco-friendly sulfur processing methods.

Investment & Funding Patterns: Over USD 500 Million invested globally in sulfur processing upgrades and rubber chemical innovation since 2023.

Innovation & Future Outlook: Integration of AI-driven process control and low-emission production technologies is shaping next-generation insoluble sulfur solutions.

The insoluble sulfur market is heavily influenced by the tire and rubber manufacturing sector, which contributes more than 70% of total consumption globally. Industrial rubber goods account for nearly 18%, while specialty applications such as conveyor belts and seals contribute the remaining share. Technological advancements such as improved dispersion grades and high thermal stability sulfur have increased product efficiency by up to 25% in high-performance tire applications. Regulatory pressure on emissions and sustainable production practices has accelerated the adoption of cleaner sulfur processing technologies, especially in Europe and North America. Asia-Pacific remains the largest consumption hub due to rapid industrialization and automotive production growth. Emerging trends include the development of eco-friendly sulfur variants, digitalized manufacturing processes, and increased R&D investments focused on enhancing product stability and performance under extreme operating conditions.

The insoluble sulfur market holds strategic relevance as a critical component in high-performance rubber manufacturing, particularly within the automotive and industrial sectors. Its role in preventing sulfur bloom and improving vulcanization efficiency makes it indispensable for producing durable, heat-resistant tires. Advanced polymer stabilization technology delivers approximately 30% improvement in dispersion uniformity compared to conventional sulfur additives, significantly enhancing product reliability. Asia-Pacific dominates in production volume due to extensive manufacturing capacity, while North America leads in technological adoption with over 55% of enterprises integrating advanced sulfur processing systems.

By 2028, AI-driven process optimization is expected to improve production efficiency by nearly 22%, reducing waste and enhancing consistency in sulfur-based compounds. ESG compliance is becoming a central focus, with firms committing to reduce sulfur emissions by up to 35% and increase recycling rates of sulfur by-products by 25% by 2030. In 2024, a major chemical manufacturer in Japan achieved a 19% reduction in production defects through the implementation of automated quality control systems and predictive analytics.

The future pathways of the insoluble sulfur market are closely tied to sustainability initiatives, digital transformation, and innovation in material science. Increasing regulatory scrutiny on emissions and environmental impact is driving investment in cleaner production technologies. As industries prioritize durability, safety, and compliance, the insoluble sulfur market is positioned as a foundational pillar supporting resilient supply chains, regulatory adherence, and sustainable industrial growth.

The growing demand for high-performance and durable tires is a major driver of the insoluble sulfur market. Modern tire manufacturing requires materials that can withstand high temperatures, mechanical stress, and prolonged usage, making insoluble sulfur an essential component in rubber vulcanization. Over 70% of global insoluble sulfur consumption is attributed to tire production, particularly for radial and high-speed tires. The automotive sector has witnessed a steady increase in production volumes, with global vehicle manufacturing surpassing 90 million units annually. Additionally, the shift toward electric vehicles, which require specialized tires with low rolling resistance and enhanced durability, has increased the demand for advanced rubber compounds by approximately 25%. Insoluble sulfur’s ability to improve cross-linking efficiency and prevent sulfur bloom enhances tire longevity and safety, making it indispensable for manufacturers seeking performance optimization and regulatory compliance.

The insoluble sulfur market faces significant restraints due to volatility in raw material supply and pricing, particularly sulfur derived from petroleum refining processes. Variations in crude oil production directly impact sulfur availability, leading to supply inconsistencies. For instance, fluctuations in global refining output have caused sulfur supply variations of up to 15% annually, affecting production stability. Additionally, transportation and logistics challenges contribute to increased operational costs, especially in regions dependent on imported sulfur. Environmental regulations governing sulfur emissions and handling also impose additional compliance costs on manufacturers. The need for specialized storage and handling systems to maintain product stability further increases capital expenditure. These factors collectively create barriers for small and medium-scale producers, limiting their ability to compete effectively in the global insoluble sulfur market.

Advancements in sustainable rubber production present significant opportunities for the insoluble sulfur market. Increasing focus on eco-friendly materials and low-emission manufacturing processes has led to the development of advanced sulfur formulations that reduce environmental impact. The adoption of green tire technologies, which aim to improve fuel efficiency and reduce carbon emissions, has increased by over 30% in recent years. Insoluble sulfur plays a critical role in enhancing the performance of these sustainable rubber compounds. Additionally, the expansion of infrastructure projects and industrial applications, such as conveyor belts and sealing systems, has created new demand avenues. Emerging markets in Asia and Latin America are witnessing rapid industrialization, driving the need for durable rubber products. Investments in research and development have also led to innovations in nano-dispersion sulfur and high-stability grades, opening new possibilities for specialized applications and performance enhancements.

Regulatory pressures and environmental compliance requirements present ongoing challenges for the insoluble sulfur market. Governments worldwide are implementing stringent emission standards and environmental policies aimed at reducing industrial pollution, particularly sulfur dioxide emissions. Compliance with these regulations requires significant investment in advanced processing technologies and emission control systems, increasing operational costs by up to 20%. Additionally, waste management and disposal of sulfur by-products pose environmental and logistical challenges. Manufacturers must adopt cleaner production methods and invest in sustainable practices to meet regulatory standards, which can be resource-intensive. The complexity of maintaining product quality while adhering to environmental guidelines further complicates production processes. These challenges necessitate continuous innovation and adaptation, placing pressure on manufacturers to balance cost efficiency with regulatory compliance in the evolving insoluble sulfur market landscape.

• Increasing Adoption of High-Performance Tire Compounds: The demand for high-performance and ultra-durable tires has increased significantly, with over 72% of tire manufacturers integrating advanced insoluble sulfur grades into production processes. Enhanced thermal stability formulations have improved tire lifespan by nearly 28% and reduced failure rates by 18% in high-speed applications. Additionally, the shift toward electric vehicles has driven a 25% rise in demand for specialized tire compounds that require superior vulcanization control, reinforcing the role of insoluble sulfur in next-generation automotive materials.

• Expansion of Sustainable and Low-Emission Production Technologies: Sustainability initiatives are reshaping manufacturing practices, with nearly 40% of producers adopting low-emission sulfur processing systems. Advanced desulfurization and emission control technologies have reduced sulfur dioxide emissions by up to 32% across newly upgraded facilities. Furthermore, over 35% of new production lines installed since 2023 incorporate closed-loop processing systems, enabling efficient recycling of sulfur by-products and reducing industrial waste by approximately 20%, aligning with global environmental compliance standards.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the insoluble sulfur market, particularly in industrial rubber components used in infrastructure. Around 55% of new construction projects have reported cost savings through prefabrication techniques, driving demand for high-performance rubber materials containing insoluble sulfur. Automated fabrication systems have reduced labor requirements by nearly 30% and accelerated project timelines by 25%, especially in Europe and North America, where precision-engineered rubber components are essential for structural durability and efficiency.

• Integration of Digital Manufacturing and Process Automation: Digital transformation is gaining traction, with approximately 48% of sulfur processing facilities implementing AI-driven monitoring systems to optimize production efficiency. These technologies have improved process consistency by 22% and reduced operational downtime by 17%. Predictive maintenance solutions are being adopted by nearly 36% of large-scale manufacturers, enabling real-time fault detection and reducing equipment failure rates by 19%, thereby enhancing overall productivity and cost efficiency in insoluble sulfur manufacturing operations.

The insoluble sulfur market segmentation reflects a structured distribution across product types, applications, and end-user industries, each contributing distinctly to overall demand patterns. Product types are primarily differentiated by polymeric stability and oil content, influencing performance in various rubber processing environments. Applications are heavily concentrated in tire manufacturing, accounting for over 70% of total usage, followed by industrial rubber goods and specialty applications. End-user insights reveal that automotive manufacturers dominate consumption, while construction and industrial sectors contribute to steady demand growth. Technological advancements and regulatory compliance requirements are further shaping segmentation dynamics, with increased adoption of high-dispersion sulfur grades and eco-friendly formulations. Regional consumption patterns also vary, with Asia-Pacific leading in volume due to industrial expansion, while North America and Europe emphasize high-performance and sustainable applications.

The insoluble sulfur market is segmented into regular grade, high dispersion grade, and oil-treated insoluble sulfur, each catering to specific industrial requirements. High dispersion insoluble sulfur currently accounts for approximately 46% of total adoption, driven by its superior mixing properties and uniform distribution in rubber compounds. Regular grade holds around 32% share, primarily used in conventional tire manufacturing processes. Oil-treated variants contribute nearly 22%, offering improved handling and reduced dust formation in industrial settings. High dispersion grades are witnessing the fastest growth, expanding at an estimated rate of 7.1% annually, supported by increasing demand for precision-engineered rubber products and high-performance tires. These grades enhance vulcanization efficiency by up to 30% and improve product durability under extreme conditions. Meanwhile, oil-treated sulfur remains relevant in niche applications requiring enhanced safety and handling properties, particularly in large-scale manufacturing environments.

The primary application of insoluble sulfur lies in tire manufacturing, which accounts for approximately 71% of total usage due to its essential role in rubber vulcanization and performance enhancement. Industrial rubber goods, including conveyor belts, hoses, and seals, contribute around 19%, while specialty applications such as footwear and coatings represent the remaining 10%. Tire manufacturing remains the dominant segment because of the growing need for durable, high-performance tires capable of withstanding heat and mechanical stress. However, industrial rubber applications are emerging as the fastest-growing segment, expanding at an estimated rate of 6.8% annually, driven by infrastructure development and increased demand for heavy-duty rubber components. These applications benefit from insoluble sulfur’s ability to improve tensile strength by nearly 25% and enhance resistance to wear and tear.

Automotive manufacturers represent the leading end-user segment in the insoluble sulfur market, accounting for nearly 68% of total consumption due to the extensive use of sulfur-based rubber compounds in tire production. Industrial manufacturing sectors, including mining and construction, contribute around 21%, while consumer goods and specialty industries account for the remaining 11%. The automotive sector maintains its dominance due to continuous growth in vehicle production and increasing demand for high-performance tires. However, the industrial manufacturing segment is the fastest-growing, expanding at an estimated rate of 6.5% annually, driven by rising infrastructure projects and demand for durable rubber components. Adoption rates in mining and heavy industries have increased by over 24% in recent years, reflecting the need for high-strength materials capable of withstanding harsh operating conditions. Other end-users, including consumer goods manufacturers, are gradually adopting advanced rubber formulations to enhance product durability and performance.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high-volume tire production exceeding 1.2 billion units annually, with China and India contributing over 65% of regional consumption. North America follows with approximately 22% share, driven by advanced rubber technologies and strong automotive demand. Europe holds around 19% share, supported by sustainability regulations and high-performance material adoption. South America and the Middle East & Africa collectively account for nearly 11%, with growing industrialization and infrastructure projects boosting demand. Regional production capacity expansion has increased by over 27% globally between 2022 and 2025, while cross-border trade in sulfur-based materials has risen by 18%, reflecting strong inter-regional supply chain integration and increasing demand for specialized rubber compounds.

North America accounts for approximately 22% of the global insoluble sulfur market, supported by strong automotive, aerospace, and industrial manufacturing sectors. Tire manufacturing contributes nearly 68% of regional consumption, while industrial rubber goods account for 20%. Regulatory frameworks focusing on emission reduction and sustainable manufacturing have pushed over 45% of manufacturers to adopt low-emission sulfur processing technologies. Technological advancements such as AI-based process optimization and automated blending systems have improved production efficiency by 23% across major facilities. A key regional player has invested in upgrading production units, achieving a 17% reduction in processing waste and a 14% improvement in product consistency. Consumer behavior in this region reflects high adoption of advanced materials, particularly in automotive and heavy industries, where performance and durability are prioritized.

Europe holds nearly 19% of the insoluble sulfur market, with Germany, the UK, and France leading in consumption and technological innovation. The automotive sector accounts for over 64% of demand, followed by industrial applications at 24%. Strict environmental regulations and sustainability initiatives have resulted in over 50% of manufacturers transitioning to eco-friendly sulfur processing systems. The adoption of advanced dispersion technologies has improved product efficiency by 21% and reduced emissions by approximately 30%. A regional manufacturer recently implemented closed-loop production systems, reducing waste generation by 18% while enhancing output quality. Consumer behavior in this region is heavily influenced by regulatory compliance, leading to increased demand for sustainable and high-performance rubber materials that meet stringent environmental standards.

Asia-Pacific dominates the insoluble sulfur market with nearly 48% share, driven by high-volume production in China, India, and Japan. China alone contributes over 55% of regional output, supported by more than 30 large-scale sulfur processing facilities. Tire manufacturing accounts for over 72% of consumption in this region, reflecting strong automotive industry growth. Infrastructure expansion and industrialization have increased demand for rubber components by 26% over the past three years. Technological innovation hubs in Japan and South Korea are focusing on high-dispersion sulfur technologies, improving product performance by up to 25%. A major regional producer has expanded capacity by 20%, enhancing supply capabilities for domestic and export markets. Consumer behavior reflects cost-sensitive yet volume-driven demand, with increasing adoption of advanced materials in manufacturing sectors.

South America accounts for approximately 7% of the global insoluble sulfur market, with Brazil and Argentina leading regional consumption. The automotive and construction sectors contribute nearly 60% of demand, while industrial rubber applications account for 28%. Infrastructure development projects have increased demand for durable rubber materials by 19% over the past two years. Government incentives supporting industrial growth and trade policies promoting local manufacturing have boosted production capacity by 15%. A regional chemical manufacturer has enhanced production efficiency by 16% through process modernization initiatives. Consumer behavior in this region is closely tied to industrial and infrastructure development, with increasing demand for cost-effective and durable materials for large-scale applications.

The Middle East & Africa region holds around 4% of the insoluble sulfur market, with the UAE and South Africa emerging as key growth centers. Demand is primarily driven by oil & gas and construction sectors, which together account for nearly 62% of regional consumption. Infrastructure investments have increased rubber material usage by 21%, particularly in pipeline and sealing applications. Technological modernization efforts have led to a 14% improvement in production efficiency across regional facilities. Trade partnerships and regulatory frameworks supporting industrial development have encouraged local production expansion. A regional player has implemented advanced processing technologies, achieving a 12% reduction in operational costs. Consumer behavior reflects demand for durable and high-performance materials suitable for harsh environmental conditions.

China – 34% market share in the insoluble sulfur market, driven by high production capacity and extensive tire manufacturing industry.

United States – 18% market share in the insoluble sulfur market, supported by strong demand from automotive and industrial rubber sectors.

The insoluble sulfur market exhibits a moderately consolidated competitive landscape, with the top five companies accounting for approximately 58% of the global market share. Over 25 active manufacturers operate globally, ranging from large-scale chemical corporations to specialized sulfur processing firms. Market leaders are focusing on capacity expansion, product innovation, and strategic partnerships to strengthen their positions. Between 2023 and 2025, more than 12 major production facility upgrades were recorded, increasing global capacity by nearly 20%.

Innovation remains a key competitive factor, with over 40% of companies investing in advanced dispersion technologies and eco-friendly sulfur processing methods. Strategic collaborations between chemical manufacturers and tire producers have resulted in improved product performance, with efficiency gains of up to 22% in rubber compounding processes. Mergers and acquisitions have also played a role, with at least 6 notable transactions completed in the past three years to consolidate market presence and expand geographic reach.

Companies are increasingly adopting digital transformation strategies, including AI-driven process optimization and predictive maintenance systems, which have reduced operational downtime by 15% and improved production consistency by 18%. The competitive environment is further shaped by regulatory compliance requirements and sustainability goals, pushing manufacturers to invest in cleaner technologies and reduce emissions by up to 30%, ensuring long-term competitiveness and market stability.

Eastman Chemical Company

Shikoku Chemicals Corporation

Lanxess AG

Arkema S.A.

China Sunshine Chemical Holdings Limited

Nynas AB

Oriental Carbon & Chemicals Limited

KUMHO Petrochemical Co., Ltd.

Lion Specialty Chemicals Co., Ltd.

Willing New Materials Technology Co., Ltd.

Technological advancements in the insoluble sulfur market are increasingly focused on improving dispersion efficiency, thermal stability, and environmental sustainability. High-dispersion insoluble sulfur grades have gained significant traction, accounting for over 45% of total product adoption due to their ability to enhance rubber compound uniformity by nearly 30%. These advanced formulations reduce agglomeration and improve cross-linking efficiency, resulting in stronger and more durable tire products. Additionally, oil-treated variants are being optimized to reduce dust formation by up to 20%, improving workplace safety and handling efficiency in manufacturing environments.

Automation and digitalization are transforming production processes, with approximately 48% of manufacturers implementing AI-driven monitoring systems to optimize sulfur conversion and stabilization. These systems have improved production consistency by 22% and reduced energy consumption by nearly 15%. Predictive maintenance technologies are also being widely adopted, enabling real-time monitoring of equipment performance and reducing unplanned downtime by 18%. Continuous processing systems are replacing traditional batch processes, increasing throughput by up to 25% while maintaining consistent product quality.

Environmental compliance technologies are another critical area of innovation. Advanced emission control systems have reduced sulfur dioxide emissions by up to 32% in modern facilities, aligning with stringent global regulations. Closed-loop recycling systems are being implemented in over 35% of new plants, allowing recovery and reuse of sulfur by-products and reducing waste generation by approximately 20%. Furthermore, research into bio-based additives and low-carbon processing techniques is gaining momentum, with pilot projects demonstrating a 12% reduction in overall carbon footprint. These technological developments are enabling manufacturers to meet evolving regulatory requirements while enhancing operational efficiency and product performance.

• In March 2025, Eastman Chemical Company announced enhancements to its Crystex™ insoluble sulfur product line, focusing on improved thermal stability and dispersion characteristics. The upgraded formulations demonstrated a 15% improvement in processing efficiency for tire manufacturers. Source: www.eastman.com

• In September 2024, Lanxess AG expanded its specialty chemicals production capabilities in Germany, including upgrades to sulfur-based additives manufacturing. The initiative improved production efficiency by 18% and reduced emissions through advanced process optimization technologies. Source: www.lanxess.com

• In May 2025, Shikoku Chemicals Corporation introduced a new high-dispersion insoluble sulfur grade designed for high-performance tire applications. The product enhanced vulcanization consistency by 20% and reduced material waste during rubber compounding processes. Source: www.shikoku.co.jp

• In November 2024, Oriental Carbon & Chemicals Limited implemented process automation upgrades at its production facilities in India, improving operational efficiency by 17% and reducing energy consumption by 12% through digital monitoring systems. Source: www.occlindia.com

The scope of the insoluble sulfur market report encompasses a comprehensive evaluation of key product types, applications, end-user industries, regional markets, and technological advancements shaping the industry landscape. The report analyzes three primary product categories, including high-dispersion, regular, and oil-treated insoluble sulfur, which collectively address over 95% of industrial demand. Application coverage includes tire manufacturing, accounting for more than 70% of global consumption, alongside industrial rubber goods and specialty applications such as seals, belts, and coatings.

Geographically, the report provides in-depth insights across five major regions, with Asia-Pacific contributing nearly 48% of global demand, followed by North America and Europe with a combined share exceeding 40%. It also highlights emerging markets in South America and the Middle East & Africa, where industrialization and infrastructure investments are driving demand growth. The analysis includes over 25 active manufacturers and evaluates production capacities exceeding 800,000 metric tons annually worldwide.

Technological coverage focuses on advanced dispersion technologies, automated processing systems, and sustainable production methods, with over 40% of manufacturers adopting digital transformation initiatives. The report also examines regulatory frameworks impacting sulfur emissions and environmental compliance, which influence production strategies and investment decisions. Additionally, it explores niche segments such as eco-friendly sulfur variants and high-performance rubber compounds, providing a holistic view of the market’s evolving dynamics. This structured scope enables decision-makers to assess opportunities, risks, and strategic priorities across the global insoluble sulfur market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Eastman Chemical Company, Shikoku Chemicals Corporation, Lanxess AG, Arkema S.A., China Sunshine Chemical Holdings Limited, Nynas AB, Oriental Carbon & Chemicals Limited, KUMHO Petrochemical Co., Ltd., Lion Specialty Chemicals Co., Ltd., Willing New Materials Technology Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |