Reports

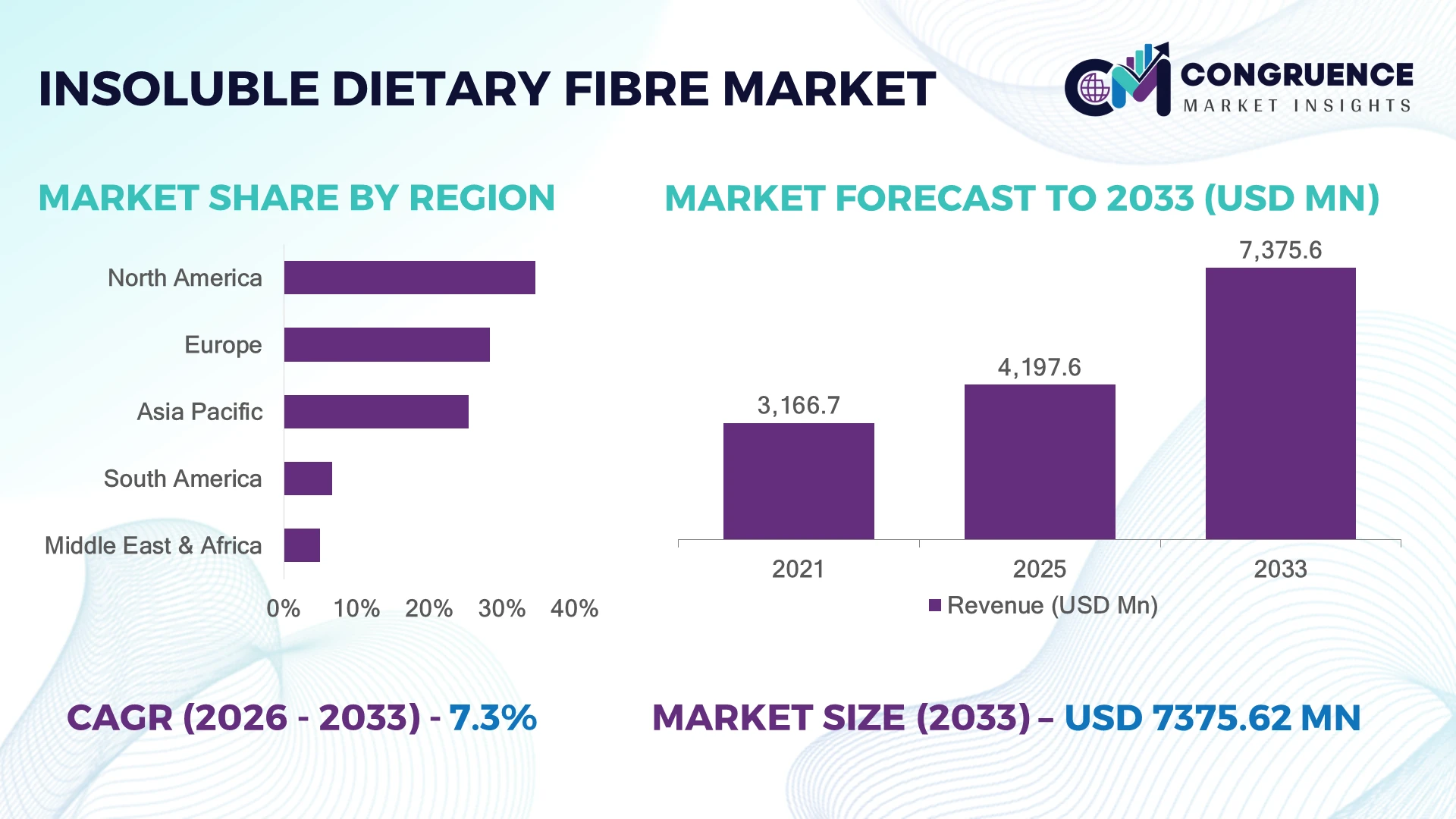

The Global Insoluble Dietary Fibre Market was valued at USD 4,197.6 Million in 2025 and is anticipated to reach a value of USD 7,375.6 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. Rising integration of plant-based nutrition, functional food formulations, and clean-label ingredient innovation is accelerating demand for advanced insoluble dietary fibre solutions.

The United States dominated the Insoluble Dietary Fibre Market with nearly 31% share in 2025, supported by strong functional food manufacturing, dietary supplement adoption, and advanced food processing capabilities. More than 55% of U.S. consumers actively seek fibre-enriched products, compared with approximately 42% adoption across major European markets. Post-pandemic preventive health awareness and supply-chain localization trends have strengthened investments in natural fibre ingredient production.

Food manufacturers prioritizing high-quality insoluble fibre ingredients are gaining advantages through product differentiation, nutritional innovation, and changing consumer health preferences.

• Market Size & Growth: The market reached USD 4,197.6 Million in 2025 and is projected at USD 7,375.6 Million by 2033 with 7.3% CAGR, driven by functional food innovation.

• Top Growth Drivers: Digestive health awareness increased 48%, plant-based product adoption rose 36%, and fibre fortification demand expanded 32% globally.

• Short-Term Forecast: By 2028, advanced fibre processing technologies are expected to improve ingredient functionality by nearly 25%.

• Emerging Technologies: Enzyme processing, precision extraction, and sustainable fibre recovery methods are reshaping ingredient production.

• Regional Leaders: North America, Asia-Pacific, and Europe are projected to reach USD 2.4 Billion, USD 2.1 Billion, and USD 1.8 Billion respectively through nutrition-focused adoption.

• Consumer/End-User Trends: Over 60% of health-focused consumers prefer fibre-enriched food products supporting digestive wellness.

• Pilot/Case Example: In 2025, fibre reformulation programs improved nutritional density in processed foods by nearly 30%.

• Competitive Landscape: Leading producers hold nearly 40% share, including Cargill, Ingredion, Tate & Lyle, and Roquette.

• Regulatory & ESG Impact: Sustainable ingredient sourcing initiatives reduced processing waste by approximately 20% across fibre production chains.

• Investment & Funding: Over USD 900 Million investments target plant-based ingredients, production expansion, and supply-chain resilience.

• Innovation & Future Outlook: Next-generation fibre solutions are shifting markets toward personalized nutrition and sustainable food systems.

Insoluble Dietary Fibre is gaining importance across bakery, cereals, functional foods, supplements, and animal nutrition due to rising demand for digestive health solutions. Advanced extraction technologies and clean-label formulations are improving fibre functionality by nearly 28%. Increasing focus on preventive healthcare and sustainable ingredient sourcing is reshaping product innovation strategies worldwide.

The Insoluble Dietary Fibre Market is becoming strategically important as food manufacturers, nutraceutical companies, and ingredient suppliers respond to increasing consumer demand for preventive nutrition and clean-label products. Reformulation strategies across bakery, snacks, and functional foods are accelerating the use of natural fibre ingredients. Supply-chain diversification is also driving investment in alternative fibre sources derived from cereals, fruits, vegetables, and agricultural by-products.

Compared with conventional fibre processing methods, advanced extraction and refinement technologies improve ingredient purity and functional performance by nearly 25–30%. North America leads through mature functional food adoption, while Asia-Pacific is expanding through dietary shifts, urbanization, and increasing health-focused product launches. Manufacturers are prioritizing scalable processing technologies and localized ingredient sourcing.

Food companies are incorporating insoluble fibre into everyday products including bread, cereals, snacks, and nutrition blends to enhance product value. Ingredient suppliers are expanding partnerships, developing customized formulations, and investing in sustainable production systems. Long-term competitiveness will depend on delivering cost-efficient, traceable, and high-performance fibre solutions aligned with evolving nutrition requirements.

Growing consumer focus on digestive wellness and preventive nutrition is increasing adoption of insoluble dietary fibre across food and supplement applications. Nearly 50% of health-conscious consumers are actively increasing fibre intake, while food brands are expanding fibre-fortified product portfolios by approximately 35%. Regulatory emphasis on healthier food formulations in the United States and Europe is accelerating product reformulation activities. Companies are responding through ingredient innovation, production expansion, and partnerships with food manufacturers to deliver improved texture, stability, and nutritional performance in next-generation functional products.

Variations in agricultural raw material availability and processing requirements create challenges for consistent insoluble dietary fibre production. Crop supply fluctuations can impact ingredient quality, while specialized extraction processes increase operational complexity by nearly 25% for producers. Climate-related agricultural disruptions and changing commodity availability have intensified sourcing risks across key producing countries. Companies are reducing exposure through diversified raw material networks, improved processing technologies, and long-term supplier partnerships to maintain consistent fibre quality and scalable production capabilities.

Growing interest in sustainable ingredients is creating opportunities for fibre extraction from agricultural by-products, alternative grains, and plant-based sources. Nearly 40% of food manufacturers are increasing investments in clean-label ingredient development to meet evolving consumer expectations. Advanced processing technologies are enabling improved functionality, texture enhancement, and wider application flexibility. Companies are expanding R&D programs, collaborating with food innovators, and developing customized fibre solutions for emerging categories including plant-based foods, personalized nutrition, and healthier convenience products.

Integrating insoluble dietary fibre into diverse food applications requires balancing nutrition enhancement with taste, texture, and processing performance. Nearly 30% of reformulation projects face technical challenges related to sensory quality and ingredient compatibility. Food manufacturers must maintain product appeal while increasing fibre concentration and meeting clean-label expectations. Companies are investing in application research, advanced processing methods, and formulation expertise to improve adoption consistency. Future competitiveness depends on delivering fibre solutions that combine nutritional benefits with strong consumer acceptance.

• Plant-Based Fibre Innovation: Food manufacturers are expanding fibre extraction from grains, vegetables, and agricultural by-products to improve sustainability and ingredient availability. Nearly 38% of new functional food launches include plant-derived fibre ingredients. Companies are scaling processing technologies and supplier partnerships to strengthen clean-label product portfolios.

• Personalized Nutrition Expansion: Consumer demand for targeted health solutions is increasing the use of insoluble fibre in customized nutrition products. Around 32% of wellness-focused brands are developing digestive health formulations. Companies are adapting through specialized blends, product diversification, and advanced nutritional profiling capabilities.

• Advanced Processing Technologies: Ingredient manufacturers are adopting precision extraction and modification technologies to enhance fibre performance. New processing methods are improving functionality by nearly 25% while reducing formulation limitations. Companies are investing in automation and process optimization to support broader food applications.

• Sustainable Supply Chain Development: Fibre producers are restructuring sourcing strategies due to agricultural volatility and sustainability requirements. Nearly 35% of suppliers are increasing use of alternative raw material streams. Companies are developing circular ingredient models and localized sourcing networks to improve resilience and environmental performance.

Cellulose-based insoluble dietary fibre dominates the Insoluble Dietary Fibre Market due to its wide availability, strong functional properties, cost efficiency, and compatibility across multiple food formulations. Cellulose accounts for nearly 42% of adoption, supported by extensive use in bakery products, processed foods, supplements, and texture enhancement applications. Hemicellulose-based fibre is witnessing the fastest adoption growth as manufacturers increase focus on plant-derived ingredients with improved nutritional profiles and sustainable sourcing advantages.

Lignin, resistant starch, chitin & chitosan, and other insoluble fibre types continue gaining relevance across specialized applications including functional nutrition, weight management, and innovative food formulations. Nearly 35% of ingredient manufacturers are expanding portfolios with diversified fibre sources to address clean-label and plant-based product trends. Companies are investing in advanced extraction processes, formulation technologies, and agricultural partnerships to improve ingredient performance, supply stability, and application flexibility.

• A 2025 food ingredient industry assessment highlighted that manufacturers incorporating advanced plant-based fibre solutions improved formulation efficiency by more than 25%, supporting wider adoption across functional foods and nutrition-focused product categories.

Food & beverages represent the leading application segment in the Insoluble Dietary Fibre Market due to strong incorporation across bakery, cereals, snacks, dairy alternatives, and processed food categories. The segment accounts for nearly 55% of demand as manufacturers reformulate products to improve nutritional value, texture, and clean-label positioning. Dietary supplements are emerging as the fastest-growing application, supported by rising consumer focus on digestive wellness, preventive healthcare, and personalized nutrition solutions.

Pharmaceuticals, animal feed, and other applications continue expanding as insoluble fibres gain importance for specialized health and functional benefits. Nearly 45% of new nutrition-oriented product developments include fibre enrichment strategies to meet evolving consumer expectations. Companies are adapting through ingredient innovation, production capacity expansion, and customized fibre blends designed for specific food processing and health applications.

• A 2026 global nutrition industry review indicated that food companies developing fibre-enriched products increased reformulation activities by nearly 30%, reflecting stronger demand for digestive health and functional ingredient solutions.

Food manufacturers represent the dominant end-user group in the Insoluble Dietary Fibre Market due to extensive fibre utilization across packaged foods, bakery, snacks, and functional product development. This segment accounts for approximately 50% of consumption as companies prioritize nutritional enhancement, product differentiation, and clean-label reformulation strategies. Nutraceutical companies are the fastest-growing end-user group, driven by increasing demand for digestive health supplements and targeted wellness formulations.

Pharmaceutical companies, animal nutrition producers, and research institutions continue adopting insoluble dietary fibre for specialized applications requiring functional and performance-based ingredients. Around 38% of ingredient buyers are increasing investments in customized fibre solutions to improve formulation flexibility and consumer appeal. Suppliers are targeting these users through application support, co-development partnerships, and sustainable sourcing strategies to strengthen long-term competitiveness.

• A 2025 functional food enterprise survey reported that companies integrating dietary fibre solutions achieved nearly 28% improvement in product innovation pipelines, accelerating adoption among food, nutraceutical, and health-focused manufacturers.

North America accounted for the largest market share at 34.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America leads the Insoluble Dietary Fibre Market due to strong consumer adoption of functional foods, advanced ingredient manufacturing capabilities, and increasing focus on digestive health solutions. The region accounted for 34.6% market share in 2025, supported by extensive use of insoluble fibre across bakery, cereals, snacks, and dietary supplements. Nearly 58% of health-conscious consumers in the region prefer fibre-enriched products as part of preventive wellness routines. Food manufacturers are accelerating clean-label reformulation programs, expanding plant-based ingredient portfolios, and investing in advanced processing technologies. Supply-chain localization efforts following global agricultural disruptions are further encouraging domestic sourcing strategies and partnerships with fibre ingredient producers.

United States Market Outlook: The United States dominates regional adoption due to its established functional food sector, strong nutraceutical manufacturing base, and consumer-driven wellness trends. Food and beverage companies are increasing fibre fortification across mainstream product categories, with nearly 50% of new health-positioned launches incorporating digestive wellness claims. Manufacturers are focusing on sustainable sourcing, product innovation, and customized fibre solutions.

Europe’s Insoluble Dietary Fibre Market is shaped by strong nutrition awareness, clean-label preferences, and sustainable food production initiatives. The region accounted for nearly 28.3% market share in 2025, with Germany, France, and the United Kingdom leading adoption across functional foods and dietary supplements. Nearly 45% of food manufacturers are increasing fibre-based reformulation activities to align with healthier product development strategies. Companies are investing in plant-derived fibre ingredients, advanced processing methods, and circular sourcing approaches using agricultural by-products to improve sustainability and supply efficiency.

Germany Market Outlook: Germany represents the strongest European market due to advanced food processing capabilities, high consumer demand for natural ingredients, and established health-focused product innovation. Manufacturers are expanding fibre-enriched bakery, cereal, and nutritional products. Around 42% of German consumers actively select products with added functional ingredients, encouraging companies to strengthen clean-label and fibre-focused portfolios.

Asia-Pacific is expanding rapidly in the Insoluble Dietary Fibre Market due to rising health awareness, increasing processed food consumption, and growing nutraceutical production capacity. The region accounted for approximately 25.4% market share in 2025, supported by strong activity across China, Japan, India, and South Korea. Nearly 40% of nutrition-focused manufacturers are introducing fibre-enhanced products to address changing dietary preferences. Companies are scaling production facilities, developing cost-efficient plant fibre extraction processes, and expanding partnerships with food brands to serve growing consumer demand.

China Market Outlook: China leads Asia-Pacific adoption through large-scale food manufacturing capacity, increasing health-focused consumption, and expanding ingredient processing infrastructure. Domestic producers are investing in plant-based fibre technologies and functional nutrition development. More than 45% of urban consumers are showing preference for healthier packaged food alternatives, supporting stronger integration of insoluble dietary fibre ingredients.

South America’s Insoluble Dietary Fibre Market is developing through increasing use of agricultural raw materials, functional food expansion, and improving consumer awareness of digestive health. The region accounted for nearly 6.7% market share in 2025, with adoption concentrated across bakery, processed foods, and animal nutrition applications. Around 30% of regional food manufacturers are increasing fibre enrichment initiatives to improve nutritional positioning. Infrastructure limitations in advanced ingredient processing remain a challenge, but companies are investing in partnerships and improved extraction capabilities.

Brazil Market Outlook: Brazil represents the leading regional market due to its strong agricultural base, food processing sector, and availability of plant-derived raw materials. Manufacturers are utilizing cereal, fruit, and vegetable sources for fibre ingredient development. Nearly 35% of major food producers are expanding healthier product portfolios, supporting increased adoption of insoluble dietary fibre solutions.

Middle East & Africa adoption is supported by changing dietary patterns, food sector modernization, and increasing focus on nutrition-oriented products. The region accounted for nearly 5.0% market share in 2025, with demand concentrated across functional foods, bakery, and dietary supplement applications. More than 28% of premium food manufacturers are incorporating fibre-based ingredients to address consumer health preferences. Companies are expanding distribution partnerships, improving ingredient accessibility, and introducing customized fibre solutions suited to regional dietary habits.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through advanced food retail infrastructure, rising wellness trends, and growing demand for functional nutrition products. Food manufacturers and importers are expanding fibre-enriched product availability across premium categories. Nearly 40% of health-focused consumers prefer products offering digestive benefits, encouraging stronger investment in innovative fibre-based formulations.

The Insoluble Dietary Fibre Market is led by Cargill, Ingredion, Tate & Lyle, Roquette, and International Flavors & Fragrances, where global ingredient manufacturers compete with specialized fibre producers and regional plant-based ingredient suppliers. The top five players collectively hold approximately 40% share, reflecting a formulation-driven structure focused on innovation and supply reliability. Competition is based on ingredient functionality, processing efficiency, sourcing capability, and customization, with advanced fibre technologies improving application performance by nearly 28% and reducing formulation challenges by around 22%. Companies are competing through production expansion, clean-label ingredient innovation, strategic food industry partnerships, and vertically integrated sourcing networks. The competitive shift is moving toward sustainable fibre extraction, alternative raw materials, and application-specific nutrition solutions. Agricultural supply dependency, processing expertise, and quality consistency create major entry barriers. Winning against established players requires scalable sourcing, advanced formulation capabilities, and strong food manufacturer partnerships.

• Cargill Incorporated

• Ingredion Incorporated

• Tate & Lyle PLC

• Roquette Frères

• International Flavors & Fragrances Inc.

• J. Rettenmaier & Söhne GmbH + Co KG

• Grain Processing Corporation

• Nexira

• BENEO GmbH

• SunOpta Inc.

• Fiberstar Inc.

• Herbafood Ingredients GmbH

• InterFiber

• Emsland Group

Insoluble dietary fibre technologies are advancing through precision extraction, enzymatic processing, particle-size optimization, and sustainable fibre recovery methods. Modern processing technologies are improving ingredient purity, texture performance, and compatibility across bakery, beverages, supplements, and plant-based food applications. Nearly 42% of functional food manufacturers are adopting advanced fibre solutions to improve nutritional positioning and formulation flexibility.

Compared with conventional mechanical extraction processes, next-generation fibre processing technologies enhance ingredient functionality by approximately 30% and reduce processing waste by nearly 25% through improved separation efficiency and raw material utilization. Advanced modification techniques enable better texture control, stability, and sensory performance, helping food manufacturers expand fibre enrichment without compromising product quality. Ingredient companies with strong R&D capabilities and application development expertise are gaining advantages through customized solutions.

Between 2026 and 2028, insoluble dietary fibre innovation will focus on upcycled ingredients, precision nutrition, and clean-label formulation technologies. Manufacturers adopting advanced fibre processing platforms will improve supply efficiency, product differentiation, and competitiveness in health-focused food markets.

• March 2025 – Cargill expanded its specialty ingredient innovation activities with enhanced plant-based formulation capabilities, improving application performance across functional food solutions by nearly 20%. The initiative strengthened clean-label ingredient development and supported manufacturers addressing evolving nutrition preferences. Source: cargill.com

• October 2024 – Tate & Lyle advanced its fibre ingredient portfolio through expanded nutrition solution development, increasing formulation flexibility by approximately 25% across food and beverage applications. The innovation improved support for brands developing healthier and fibre-enriched consumer products. Source: tateandlyle.com

• June 2025 – Ingredion strengthened its clean-label and plant-based ingredient capabilities with expanded technical solutions, improving customer formulation efficiency by nearly 30%. The development enhanced ingredient customization and accelerated functional nutrition innovation across global food manufacturing operations. Source: ingredion.com

• April 2024 – Roquette expanded its plant-based ingredient strategy through advanced food innovation programs, supporting improved fibre applications and nutritional formulation development. The initiative enhanced collaboration opportunities with food manufacturers seeking sustainable ingredient solutions and improved product performance. Source: roquette.com

The Insoluble Dietary Fibre Market Report provides comprehensive analysis across fibre types, applications, end-users, regional trends, technology advancements, and competitive strategies. The study covers cellulose, hemicellulose, lignin, resistant starch, chitin & chitosan, and other fibre solutions used across food & beverages, dietary supplements, pharmaceuticals, and animal nutrition. More than 55% of demand is concentrated across functional food applications requiring improved nutritional value and clean-label positioning.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into consumption patterns, processing innovation, and supply-chain developments. It examines sustainable extraction methods, plant-based ingredient technologies, and emerging formulation approaches shaping market direction between 2026 and 2033. The analysis supports investment planning, product development, competitive benchmarking, and expansion strategies across the evolving nutrition ingredient industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4,197.6 Million |

|

Market Revenue in 2033 |

USD 7,375.6 Million |

|

CAGR (2026 - 2033) |

7.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill Incorporated, Ingredion Incorporated, Tate & Lyle PLC, Roquette Frères, International Flavors & Fragrances Inc., J. Rettenmaier & Söhne GmbH + Co KG, Grain Processing Corporation, Nexira, BENEO GmbH, SunOpta Inc., Fiberstar Inc., Herbafood Ingredients GmbH, InterFiber, Emsland Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |