Reports

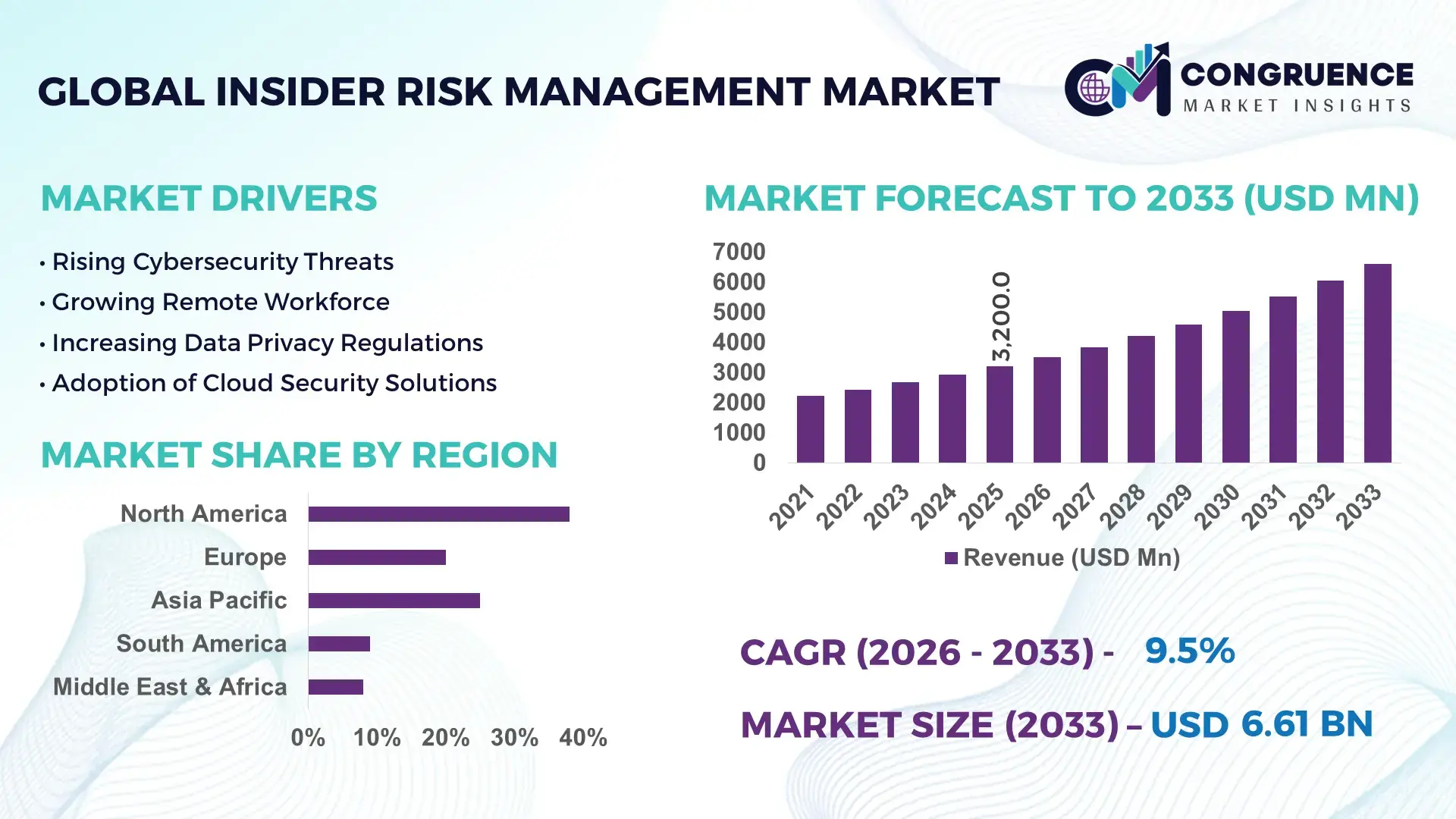

The Global Insider Risk Management Market was valued at USD 3200 Million in 2025 and is anticipated to reach a value of USD 6613.98 Million by 2033 expanding at a CAGR of 9.5% between 2026 and 2033. Enterprise-wide deployment of AI-driven user behavior analytics, zero-trust security architecture, and automated threat detection platforms is accelerating adoption, with organizations reducing insider-related investigation time by nearly 42% through integrated risk orchestration systems.

The United States dominates the global insider risk management landscape with nearly 38% market share, supported by large-scale cybersecurity investments exceeding USD 25 billion across banking, defense, cloud infrastructure, and healthcare ecosystems. More than 71% of Fortune 500 enterprises deployed advanced insider threat monitoring frameworks by early 2026, compared to below 46% adoption across several emerging economies. Federal cybersecurity modernization programs, combined with rapid AI integration into security operations centers, strengthened real-time anomaly detection accuracy by approximately 35%. Compared with conventional rule-based monitoring, behavioral analytics platforms process threat indicators 3x faster while reducing false-positive incidents by nearly 28%.

Companies prioritizing predictive insider intelligence, cross-platform monitoring, and compliance-focused automation are positioning themselves for stronger operational resilience and lower long-term cybersecurity exposure.

Market Size & Growth: USD 3200 Million in 2025 reaching USD 6613.98 Million by 2033, driven by AI-based behavioral monitoring and hybrid workforce security expansion at 9.5% CAGR.

Top Growth Drivers: Remote workforce expansion contributes 34%, regulatory compliance pressure 29%, and privileged access misuse incidents 26% to advanced market acceleration.

Short-Term Forecast: By 2028, automated insider threat response platforms reduce breach investigation time by 41% and improve SOC operational efficiency by 33%.

Emerging Technologies: AI analytics, UEBA platforms, and zero-trust automation improve threat detection precision by 37% across high-growth enterprise security environments.

Regional Leaders: North America exceeds USD 2.4 Billion with AI-led adoption, Europe crosses USD 1.7 Billion through compliance modernization, while Asia-Pacific expands rapidly through cloud-security integration.

Consumer/End-User Trends: Nearly 68% of enterprises prioritize real-time employee risk analytics and continuous credential monitoring across distributed workforces.

Pilot/Case Example: In 2026, a multinational banking deployment reduced insider-related data exposure incidents by 44% through predictive behavior intelligence integration.

Competitive Landscape: Leading vendors control nearly 48% market concentration, with strong competition among cybersecurity analytics, cloud security, and IAM platform providers.

Regulatory & ESG Impact: Compliance automation lowers audit preparation costs by 31% while improving governance transparency amid expanding global cybersecurity mandates.

Investment & Funding: Global cybersecurity and insider threat platform investments surpassed USD 6 Billion in 2025, fueled by enterprise partnerships and cloud-security expansion strategies.

Innovation & Future Outlook: Autonomous risk scoring, adaptive access governance, and AI-led insider prediction models are transforming enterprise cybersecurity positioning through 2028.

Banking, healthcare, and government sectors collectively account for more than 61% of global insider risk management deployments due to rising exposure to credential misuse, data exfiltration, and compliance penalties. AI-enabled behavioral analytics platforms improved insider threat detection precision by nearly 37% in 2026, while cloud-native monitoring solutions reduced incident response delays by 29%. North America leads enterprise-scale adoption, whereas Asia-Pacific records the fastest deployment growth amid accelerated digital workplace expansion and tightening cybersecurity frameworks. Increasing supply chain cyber vulnerabilities and stricter cross-border data governance policies are pushing organizations toward predictive insider intelligence ecosystems, setting the stage for deeper strategic transformation and competitive security differentiation.

Insider risk management has shifted from a compliance function into a board-level strategic cybersecurity priority as enterprises confront escalating data exposure, remote workforce vulnerabilities, and AI-driven cyber manipulation. Financial institutions, healthcare systems, and cloud infrastructure operators are aggressively expanding insider surveillance investments to protect operational continuity and sensitive digital assets. Regulatory pressure surrounding data governance, critical infrastructure protection, and cybersecurity disclosures is accelerating enterprise-wide adoption across advanced economies and high-growth digital markets.

AI-powered behavioral analytics platforms improve threat detection efficiency by 43% while reducing operational investigation costs by 31% compared to legacy rule-based monitoring systems. North America leads in deployment volume, while Asia-Pacific leads in adoption acceleration with 36% higher enterprise onboarding growth driven by cloud-first digital transformation. Over the next three years, automated insider threat orchestration is projected to reduce enterprise breach containment time by nearly 40%. ESG-focused governance frameworks are also creating competitive advantages, with automated compliance monitoring reducing audit overhead by 27% and strengthening investor confidence in cybersecurity resilience.

In 2026, a multinational healthcare network integrated predictive insider intelligence systems and reduced privileged-access misuse incidents by 46% within twelve months. Technology vendors are shifting capital allocation toward unified security analytics, cross-platform monitoring, and identity intelligence ecosystems to capture enterprise modernization demand. Organizations optimizing predictive visibility, adaptive governance, and automated response infrastructure are transforming cybersecurity from a defensive necessity into a long-term competitive advantage.

Hybrid work expansion, rising privileged-access misuse, and AI-powered cyber intrusions are forcing enterprises to modernize insider threat defense infrastructure at unprecedented speed. More than 68% of large enterprises integrated behavior analytics platforms in 2026, while automated threat monitoring improved detection accuracy by nearly 37%. Intensifying geopolitical cyber conflict and stricter cybersecurity disclosure mandates across North America and Europe accelerated enterprise spending on zero-trust architectures and continuous identity verification systems. The direct impact is faster breach containment, lower compliance exposure, and stronger operational continuity. In response, cybersecurity vendors are accelerating cloud-native platform expansion, forming strategic AI partnerships, and increasing investment in predictive analytics engines to optimize enterprise-scale insider risk visibility and incident orchestration capabilities globally.

Enterprise adoption remains constrained by fragmented IT ecosystems, complex regulatory alignment requirements, and rising implementation costs across multinational organizations. Nearly 41% of enterprises report delayed deployment cycles due to legacy infrastructure incompatibility, while integration expenses increased by approximately 24% between 2024 and 2026. Cross-border data localization rules and inconsistent employee privacy regulations are creating operational friction, particularly across Europe and Asia-Pacific markets. These constraints directly increase onboarding timelines, reduce scalability efficiency, and complicate centralized monitoring strategies. To mitigate risk, companies are diversifying cloud-security providers, adopting modular insider risk platforms, and negotiating long-term cybersecurity integration contracts. Vendors are also prioritizing low-code automation frameworks and API-based interoperability to reduce deployment complexity and accelerate enterprise integration performance.

Predictive insider intelligence platforms are redefining enterprise cybersecurity by enabling proactive risk identification, adaptive monitoring, and automated response orchestration across distributed workforces. AI-enabled insider analytics reduced false-positive threat alerts by nearly 33% in 2026, while cloud-native deployment models lowered operational monitoring costs by approximately 28%. Rapid digital expansion across Asia-Pacific, Middle East, and Latin America is opening high-growth enterprise demand pockets, especially among financial services and healthcare providers. A major innovation shift toward autonomous identity intelligence and continuous behavioral scoring is accelerating enterprise modernization strategies. In response, cybersecurity firms are increasing R&D spending, expanding regional security operations centers, and building integrated ecosystems combining IAM, UEBA, and compliance automation capabilities to secure long-term competitive dominance in enterprise cybersecurity markets.

Sustaining insider risk management effectiveness remains challenging due to alert fatigue, workforce privacy concerns, and escalating AI-driven threat sophistication. Security teams currently manage nearly 52% more behavioral alerts than in 2023, while false-positive investigation burdens continue constraining operational productivity across large enterprises. Increasing employee resistance toward continuous monitoring and tightening global privacy regulations are forcing organizations to balance surveillance efficiency with workforce trust and legal compliance. The result is slower response coordination, fragmented governance, and inconsistent risk prioritization. Companies must solve platform interoperability limitations, improve contextual threat accuracy, and strengthen cross-functional cybersecurity collaboration to maintain long-term resilience. Industry leaders are responding through advanced AI refinement, privacy-focused monitoring frameworks, and strategic cybersecurity partnerships designed to optimize scalable, enterprise-grade insider threat intelligence capabilities globally.

41% Faster Threat Correlation Through AI-Native Monitoring Platforms Enterprises are replacing fragmented monitoring tools with AI-native insider risk platforms that correlate user activity, access behavior, and data movement in real time. Nearly 64% of large organizations integrated unified behavioral analytics systems in 2026, reducing investigation workloads by 41% and lowering false-positive alerts by 29%. Companies are restructuring security operations centers around automated risk scoring and adaptive response workflows, optimizing analyst productivity amid persistent cybersecurity labor shortages.

36% Increase in Cloud-Based Insider Surveillance Deployment Across Regulated Industries Financial institutions and healthcare providers accelerated migration toward cloud-native insider monitoring environments as stricter compliance mandates reshaped data governance processes. More than 58% of regulated enterprises shifted from on-premise architectures to centralized cloud surveillance frameworks, improving audit readiness by 33% and reducing infrastructure maintenance costs by 24%. Security vendors are responding through strategic partnerships with identity management providers and expanding regional compliance-focused deployment capabilities.

32% Growth in Asia-Pacific Enterprise Adoption Reshaping Regional Competition Asia-Pacific organizations are rapidly scaling insider risk deployment across telecom, banking, and government sectors following intensified cross-border cybersecurity regulations and supply chain exposure concerns. Regional implementation rates increased by 32% in 2026, while localized threat intelligence integration improved detection response speed by 27%. Global cybersecurity firms are expanding multilingual analytics capabilities and regional security operations partnerships to capture high-volume enterprise demand and strengthen operational localization.

28% Shift Toward Managed Insider Risk Services Redefining Security Operations Models Enterprises are increasingly outsourcing insider threat monitoring to specialized managed security providers to control operational complexity and reduce internal staffing pressure. Managed insider risk services now support nearly 46% of mid-sized enterprises, improving incident response consistency by 31% while lowering operational overhead by 22%. A non-obvious shift is emerging as companies prioritize continuous compliance monitoring over standalone threat detection, forcing vendors to reposition platforms around governance automation and integrated workforce risk intelligence.

The insider risk management market is segmented by type, application, and end-user, with demand increasingly concentrated around AI-driven monitoring and compliance-intensive industries. Behavioral Analytics and Threat Detection Solutions collectively account for nearly 48% of enterprise deployments due to higher detection precision and automated response capabilities. Data Security and Compliance Management dominate application demand across regulated sectors, particularly BFSI and healthcare, which together contribute over 44% of enterprise adoption. Demand is shifting toward cloud-native and integrated risk intelligence platforms as organizations prioritize real-time visibility, workforce monitoring, and cross-platform governance. Companies are expanding AI integration, modular deployment models, and sector-specific customization to capture evolving enterprise cybersecurity requirements and operational efficiency priorities.

Behavioral Analytics dominates the insider risk management market with approximately 31% share due to its ability to identify abnormal employee activity patterns, reduce false-positive alerts, and integrate across cloud-native security ecosystems. Enterprises increasingly prioritize predictive analytics engines because they improve insider threat detection precision by nearly 37% while accelerating incident investigation workflows. Threat Detection Solutions represent the fastest-growing segment, expanding by nearly 29% in enterprise deployment volume during 2026 as organizations shift toward automated anomaly detection and real-time response orchestration. Compared with traditional User Activity Monitoring systems, advanced Threat Detection Solutions process contextual risk indicators nearly 3x faster, redefining enterprise security operations efficiency.

Access Management, Data Loss Prevention, and User Activity Monitoring collectively account for nearly 49% of total deployment demand due to their critical role in compliance governance, credential protection, and workforce visibility. However, demand is steadily shifting toward integrated platforms combining analytics, identity intelligence, and adaptive monitoring capabilities. Vendors are accelerating AI-focused product innovation, expanding cloud integration capacity, and repositioning offerings toward unified insider intelligence ecosystems. Investment concentration is increasingly favoring scalable analytics and automated threat correlation platforms, while standalone monitoring tools face slower enterprise expansion.

Data Security leads the insider risk management market with nearly 28% share as enterprises prioritize protection against unauthorized data movement, credential misuse, and intellectual property exposure across hybrid work environments. High deployment concentration exists within financial services, healthcare, and government sectors where sensitive data governance directly impacts operational continuity and regulatory compliance. Incident Response is the fastest-growing application segment, recording approximately 31% deployment growth in 2026 due to rising demand for automated breach containment and real-time threat mitigation capabilities. Compared with mature Compliance Management deployments, Incident Response platforms are increasingly integrated with AI-powered orchestration systems that reduce response delays by nearly 38%.

Fraud Prevention, Identity Protection, Risk Assessment, and Compliance Management collectively represent around 58% of operational deployments, supported by increasing enterprise focus on governance automation and workforce access intelligence. Usage patterns are shifting from reactive monitoring toward predictive and continuous risk evaluation models. Companies are scaling cloud-based deployment frameworks, integrating identity analytics, and repositioning insider risk platforms as operational resilience tools rather than standalone compliance systems. Demand is increasingly moving toward unified platforms capable of combining detection, response, and governance functions within a single operational environment.

BFSI dominates the insider risk management market with nearly 34% share due to high transaction volumes, stringent regulatory obligations, and elevated exposure to credential misuse and financial fraud. Banks and financial institutions deploy advanced monitoring platforms extensively to secure payment infrastructure, customer records, and privileged-access systems. Healthcare represents the fastest-growing end-user segment, expanding by approximately 30% in 2026 as hospitals and digital healthcare providers strengthen protection around electronic medical records and connected healthcare ecosystems. Compared with the mature BFSI segment, healthcare organizations are adopting cloud-native insider monitoring platforms at a faster pace to address rising ransomware and employee-access vulnerabilities.

Government, IT and Telecom, Retail and E-commerce, and Energy and Utilities collectively account for nearly 51% of enterprise deployments, driven by increasing cyber exposure across critical infrastructure and digital commerce environments. Buying behavior is shifting toward sector-specific customization, subscription-based deployment models, and integrated compliance automation. Vendors are responding through strategic partnerships, tailored pricing structures, and industry-focused analytics capabilities. Demand is increasingly concentrated around organizations managing large distributed workforces and sensitive operational data, creating strong opportunities for scalable insider intelligence and automated governance platforms.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

North America leads in enterprise-scale deployment due to strong cybersecurity spending, advanced cloud infrastructure, and strict insider threat governance frameworks across BFSI, healthcare, and government sectors. Europe captures nearly 27% share, driven by compliance-intensive adoption and privacy-focused workforce monitoring modernization. Asia-Pacific holds approximately 24% market share but is accelerating rapidly through digital workplace expansion, telecom cloud migration, and enterprise AI integration across China, India, Japan, and Southeast Asia. Meanwhile, Middle East & Africa and South America collectively contribute nearly 11% as critical infrastructure protection and financial cybersecurity investments increase. Rising cross-border data regulations and expanding hybrid workforce exposure are reshaping regional deployment strategies. Global vendors are increasingly prioritizing localized compliance capabilities, AI-driven automation, and regional security operations expansion to capture high-growth enterprise demand.

North America commands nearly 38% of global insider risk management demand, supported by large-scale cybersecurity investment across banking, defense, healthcare, and cloud infrastructure sectors. More than 72% of Fortune-level enterprises now deploy AI-enabled behavioral monitoring and adaptive access governance systems to reduce insider-related operational disruption. Tightening cybersecurity disclosure mandates and rising geopolitical cyber threats are accelerating enterprise migration toward unified insider intelligence platforms. Organizations reduced incident investigation timelines by approximately 39% through automated risk orchestration and cross-platform analytics integration during 2026. Enterprises increasingly prefer scalable cloud-native deployment models over fragmented legacy systems due to faster compliance alignment and operational visibility. Technology vendors continue prioritizing regional expansion, AI integration partnerships, and enterprise automation capabilities because North America remains the highest-value market for advanced insider threat intelligence deployment.

Europe accounts for nearly 27% of global insider risk management adoption, driven by strict workforce privacy regulations, digital sovereignty priorities, and compliance-intensive cybersecurity modernization across Germany, France, and the United Kingdom. More than 61% of regulated enterprises upgraded monitoring infrastructure in 2026 to align with expanding employee data governance and cybersecurity accountability requirements. ESG-driven governance practices are also reshaping deployment preferences, forcing organizations to prioritize transparent monitoring systems and automated compliance reporting. Enterprises adopting AI-enabled risk analytics reduced audit preparation workloads by approximately 31% while improving policy enforcement consistency. Companies increasingly favor privacy-centric insider intelligence platforms with localized data processing capabilities. The region continues forcing cybersecurity vendors to innovate around compliance automation, ethical AI governance, and operational transparency to maintain long-term enterprise competitiveness and regulatory alignment.

Asia-Pacific ranks as the fastest-expanding insider risk management market, accounting for nearly 24% of global demand while recording the highest enterprise deployment acceleration across China, India, Japan, and Southeast Asia. Rapid cloud infrastructure expansion, digital banking growth, and large-scale telecom modernization are driving widespread adoption of AI-powered insider monitoring systems. More than 58% of enterprises across major regional economies increased cybersecurity automation spending in 2026 to strengthen workforce access visibility and operational resilience. Localized deployment models improved response efficiency by approximately 28% while reducing operational integration costs. Enterprises prioritize scalable, cost-efficient, and rapidly deployable security architectures capable of supporting distributed workforces and high-volume digital operations. Global cybersecurity providers are expanding regional partnerships, multilingual analytics capabilities, and local security operations infrastructure because Asia-Pacific has become critical for enterprise-scale growth and long-term market expansion.

South America contributes nearly 6% of global insider risk management demand, led by Brazil, Argentina, and Chile as financial services, retail, and telecom sectors accelerate digital security modernization. Rising exposure to credential misuse and online fraud is increasing enterprise demand for real-time monitoring and adaptive identity protection platforms. However, uneven cybersecurity infrastructure maturity and high implementation costs continue constraining enterprise-wide scalability across mid-sized organizations. Nearly 43% of regional enterprises prioritized cloud-based deployment models in 2026 to reduce infrastructure dependency and lower operational expenses. Companies are increasingly adopting subscription-driven security frameworks and localized managed monitoring services to optimize affordability and deployment speed. The region presents strong expansion potential for vendors capable of balancing cost efficiency, localized compliance adaptation, and scalable cybersecurity deployment across rapidly digitizing enterprise ecosystems.

Middle East & Africa accounts for approximately 5% of global insider risk management demand, with the United Arab Emirates, Saudi Arabia, and South Africa leading cybersecurity modernization across energy, government, telecom, and financial sectors. Large-scale smart infrastructure programs and critical infrastructure protection initiatives are accelerating enterprise investment in insider threat intelligence systems. More than 47% of large regional organizations increased cybersecurity automation deployment during 2026 to strengthen workforce monitoring and operational continuity. Governments and state-linked enterprises are forming strategic technology partnerships to improve cyber resilience and localized threat response capabilities. Enterprises increasingly prefer integrated security ecosystems combining access governance, behavioral analytics, and compliance monitoring to reduce operational fragmentation. The region is emerging as a strategic cybersecurity investment hub as digital transformation and infrastructure modernization continue accelerating enterprise security demand.

United States – 38% market share in the Insider Risk Management market, driven by advanced cybersecurity infrastructure, high enterprise AI adoption, and strict regulatory enforcement across BFSI, healthcare, and government sectors.

China – 14% market share in the Insider Risk Management market, supported by rapid digital transformation, expanding cloud infrastructure, and aggressive enterprise cybersecurity modernization initiatives.

The insider risk management market is dominated by competition between global cybersecurity leaders, cloud-security specialists, and AI-driven analytics providers including Microsoft, IBM, Broadcom, Forcepoint, Proofpoint, and CyberArk. The top five players collectively control nearly 49% of enterprise deployments through integrated identity governance, behavioral analytics, and cloud-native monitoring ecosystems. Competition is increasingly centered on AI automation, detection accuracy, deployment scalability, and compliance orchestration, with advanced analytics platforms reducing investigation workloads by 37% and improving response speed by 34%. Global vendors are aggressively expanding managed security capabilities, forming identity-management partnerships, and integrating predictive insider intelligence into unified cybersecurity platforms. Regional providers compete through customization flexibility and lower operational costs, particularly across Asia-Pacific and South America. Rapid AI disruption, platform consolidation, and evolving workforce privacy regulations are increasing entry barriers. Winning requires scalable automation, cross-platform visibility, localized compliance alignment, and continuous behavioral intelligence innovation.

Microsoft Corporation

IBM Corporation

Broadcom Inc.

Forcepoint

Proofpoint Inc.

CyberArk Software Ltd.

Trellix

Exabeam

Securonix

Netskope

Palo Alto Networks

OpenText Corporation

Rapid7

ManageEngine Corporation

AI-powered behavioral analytics and User and Entity Behavior Analytics (UEBA) platforms currently dominate enterprise insider risk deployments, with nearly 67% of large organizations integrating adaptive risk-scoring engines into security operations workflows. These platforms improve insider threat detection accuracy by approximately 37% while reducing manual investigation workloads by 32%. Compared with legacy rule-based monitoring systems, AI-native analytics platforms process contextual activity patterns nearly 3x faster and lower false-positive incidents by 29%. Enterprises in BFSI, healthcare, and telecom sectors are increasingly consolidating identity governance, access monitoring, and insider threat analytics into unified security ecosystems to optimize compliance efficiency and operational visibility.

Emerging technologies between 2026 and 2028 include machine identity intelligence, autonomous access governance, and LLM-driven anomaly detection systems. More than 58% of cloud-centric enterprises are expanding machine identity monitoring capabilities as non-human identities increasingly outnumber human accounts across digital infrastructure environments. Integrated identity security platforms reduce credential-related response delays by nearly 34% and improve cross-platform visibility through centralized analytics orchestration. Vendors competing in AI-enhanced identity intelligence and adaptive monitoring frameworks are gaining stronger enterprise positioning because organizations now prioritize predictive threat prevention instead of reactive detection alone.

Disruptive innovation is shifting toward agentic AI governance, federated insider intelligence, and zero-trust automation models capable of continuously validating workforce and machine behavior. Advanced AI-driven insider risk systems reduced response time by 47% in pilot enterprise deployments while processing over 10 million log events daily with sub-300ms latency. Companies accelerating investment in explainable AI security models, machine identity governance, and automated policy enforcement are capturing operational advantages through faster compliance alignment, lower investigation costs, and scalable enterprise-wide threat orchestration capabilities.

April 2025 – CyberArk expanded its Identity Security Platform with integrated protection for human, AI, and machine identities, strengthening insider threat governance across hybrid infrastructures. The platform introduced unified privilege controls and automated identity orchestration capabilities, helping enterprises improve identity visibility by over 30%. The move accelerated enterprise demand for consolidated insider intelligence ecosystems. [Unified Identity Shift]

September 2024 – Proofpoint launched expanded AI-driven human-centric security integrations focused on insider threat prevention, SaaS application monitoring, and adaptive behavior guidance. The deployment improved detection coverage across collaboration platforms while strengthening real-time data protection workflows. Enterprises adopting the updated platform reported measurable reductions in account takeover exposure and workforce-related security incidents. [Adaptive Security Expansion]

March 2025 – CyberArk Investor Relations released findings showing 72% of organizations experienced certificate-related outages linked to unmanaged machine identities, forcing accelerated enterprise investment in identity-centric insider risk controls. The report highlighted that 50% of security leaders faced machine identity-related incidents impacting operations, application delivery, and sensitive data access. [Machine Identity Pressure]

February 2026 – Reuters Cybersecurity Coverage reported Palo Alto Networks intensified its AI-security expansion strategy through large-scale identity security acquisitions and integration investments aimed at strengthening insider threat monitoring and real-time observability. The company increased platform integration spending significantly while positioning identity security as a core enterprise defense layer against AI-driven cyber risks. [Platform Consolidation Drive]

This report provides comprehensive coverage of the insider risk management market across core technology segments, operational applications, enterprise end-users, and regional deployment trends. The analysis evaluates key solution categories including Behavioral Analytics, Data Loss Prevention, Access Management, Threat Detection Solutions, and User Activity Monitoring alongside critical applications such as Fraud Prevention, Data Security, Identity Protection, Incident Response, and Compliance Management. The study covers enterprise adoption across BFSI, healthcare, government, IT and telecom, retail and e-commerce, and energy sectors spanning North America, Europe, Asia-Pacific, South America, and Middle East & Africa. Advanced technologies including AI-driven threat analytics, zero-trust security frameworks, machine identity governance, and cloud-native insider intelligence platforms are assessed in detail.

The report analyzes more than 10 major cybersecurity providers and evaluates execution-level market shifts shaping enterprise security transformation between 2026 and 2033. Behavioral Analytics and Threat Detection Solutions collectively account for nearly 48% of deployment demand, while over 64% of large enterprises are transitioning toward integrated insider intelligence ecosystems. The study also examines operational metrics including detection efficiency improvements, cloud deployment acceleration, compliance automation trends, and workforce monitoring adoption patterns.

Strategically, the report supports investment prioritization, product positioning, market expansion, competitive benchmarking, and technology roadmap planning. It highlights high-growth enterprise demand pockets, emerging machine identity risks, and evolving deployment models enabling organizations to optimize cybersecurity resilience, regulatory readiness, and scalable insider threat governance.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3200 Million |

|

Market Revenue in 2033 |

USD 6613.98 Million |

|

CAGR (2026 - 2033) |

9.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, IBM Corporation, Broadcom Inc., Forcepoint, Proofpoint Inc., CyberArk Software Ltd., Trellix, Exabeam, Securonix, Netskope, Palo Alto Networks, OpenText Corporation, Rapid7, ManageEngine Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |