Reports

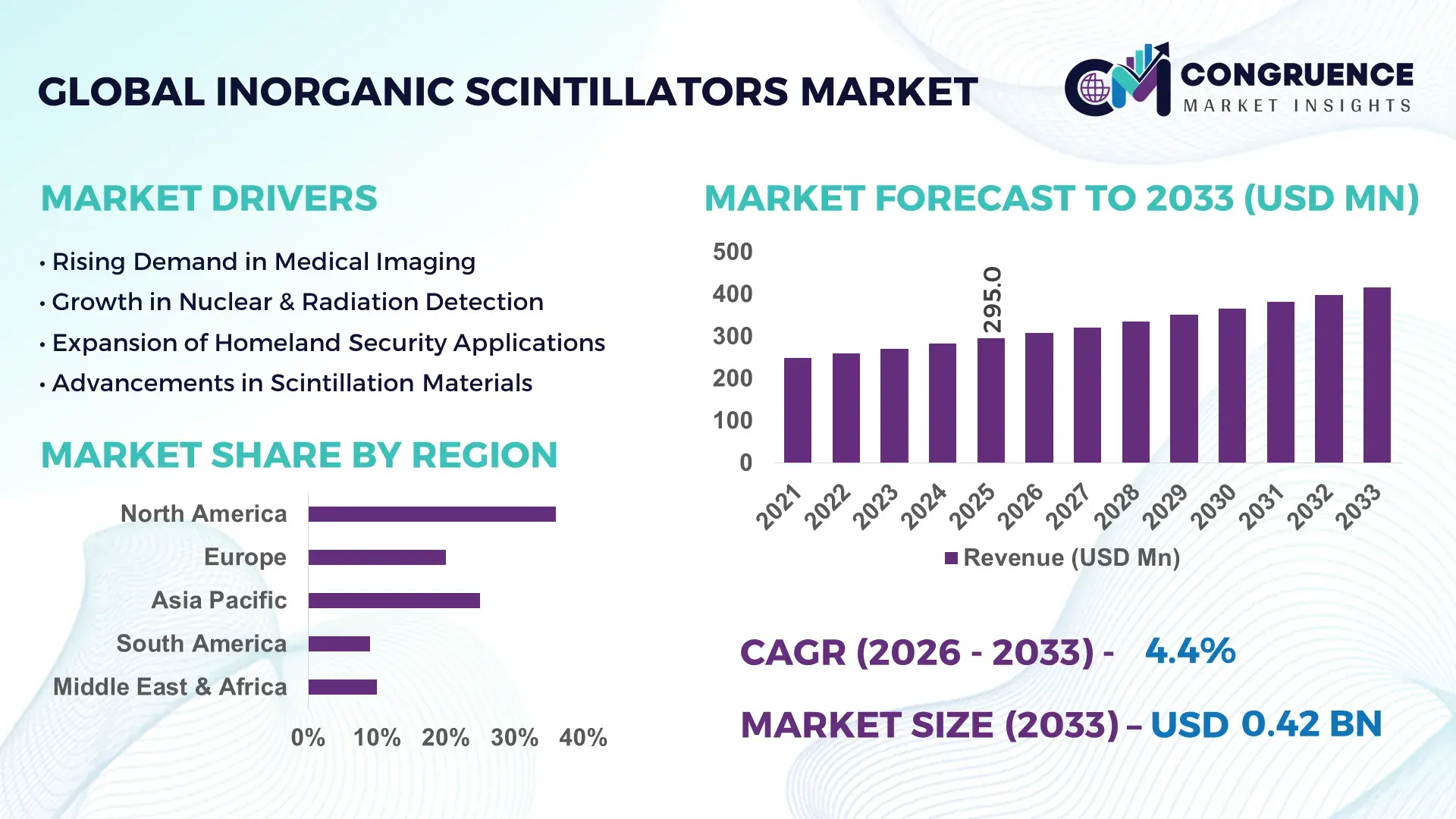

The Global Inorganic Scintillators Market was valued at USD 295 Million in 2025 and is anticipated to reach a value of USD 416.31 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033.

Market expansion is being structurally driven by the increasing deployment of high-performance radiation detection systems across medical imaging, homeland security, and nuclear energy monitoring, where advanced scintillation materials deliver up to 25–30% higher detection efficiency compared to conventional alternatives. Between 2024 and 2026, the market has been shaped by tightening global nuclear safety regulations and strategic localization of rare earth supply chains, particularly following export controls and geopolitical shifts affecting critical materials used in crystal growth processes. This has increased production costs by nearly 12% in the short term while accelerating regional manufacturing investments.

The United States remains the dominant market, accounting for approximately 34% of global share, supported by strong defense spending exceeding USD 800 billion annually and continuous investments in nuclear medicine infrastructure. Over 65% of PET and SPECT imaging systems in the country utilize inorganic scintillators such as LYSO and NaI(Tl), reflecting high adoption maturity. In comparison, China holds close to 27% share, driven by rapid expansion of domestic radiology equipment manufacturing and over 18% annual growth in nuclear energy capacity additions, creating a dual demand base across healthcare and energy sectors.

Compared to organic scintillators, inorganic variants deliver up to 40% superior energy resolution, reinforcing their preference in high-precision applications. This positions the market toward premium, application-specific growth rather than volume expansion, making material innovation and regional supply resilience critical strategic priorities for industry stakeholders.

Market Size & Growth: Valued at USD 295 Million (2025) and reaching USD 416.31 Million by 2033 at 4.4% CAGR, driven by 30% higher efficiency of advanced scintillation materials in medical imaging.

Top Growth Drivers: Medical imaging demand (+28%), nuclear security investments (+22%), and energy sector monitoring (+19%) drive global inorganic scintillators market expansion.

Short-Term Forecast: By 2028, production efficiency improves by 18% due to automation in crystal growth and material processing technologies.

Emerging Technologies: AI-integrated detection systems, cerium-doped crystals, and advanced photodetectors enhance signal accuracy by over 25%.

Regional Leaders: North America (~USD 140M) leads with defense adoption; Asia-Pacific (~USD 120M) grows via nuclear expansion; Europe (~USD 90M) advances through regulatory-driven safety upgrades.

Consumer/End-User Trends: Over 68% of healthcare imaging systems globally now rely on inorganic scintillators for precision diagnostics.

Pilot/Case Example: In 2025, a nuclear facility upgrade project improved radiation detection sensitivity by 32% using next-gen LYSO-based systems.

Competitive Landscape: Top player holds ~21% share; key companies include Saint-Gobain, Hamamatsu Photonics, Hitachi Metals, Dynasil, and Toshiba Materials.

Regulatory & ESG Impact: Stricter nuclear safety standards increased compliance costs by 15% while boosting demand for high-performance detection systems.

Investment & Funding: Over USD 180 Million invested globally (2024–2026) in advanced material R&D and localized production expansion.**

Innovation & Future Outlook: Next-gen hybrid scintillators and supply chain localization strategies are reducing dependency on rare earth imports by 20%.

Healthcare applications dominate with approximately 46% share, followed by homeland security at 28% and nuclear energy at 18%, reflecting a highly concentrated demand structure. Recent innovations in cerium-doped lutetium-based crystals have improved detection speed by 20%, while Asia-Pacific demand has risen by 24% due to expanding nuclear infrastructure. Supply chain localization trends, triggered by export restrictions, are reshaping sourcing strategies. The market is steadily transitioning toward high-efficiency, application-specific solutions, setting the stage for competitive differentiation through material science advancements.

The inorganic scintillators market is rapidly becoming a strategic cornerstone for sectors where precision detection defines operational success, particularly in advanced medical imaging, nuclear safety, and high-security environments. As global systems shift toward high-resolution diagnostics and real-time radiation monitoring, demand is accelerating for materials that deliver consistent, high-yield photon output with minimal signal loss. This transition is transforming inorganic scintillators from a niche component into a critical competitive differentiator across high-value industries.

A major structural shift is unfolding as supply chains for rare earth elements undergo localization and diversification, driven by export controls and resource concentration risks. Cerium-doped lutetium-based scintillators improve detection efficiency by 30% while reducing system-level operational costs by 18% compared to legacy sodium iodide systems, fundamentally optimizing performance economics. Regionally, Asia-Pacific leads in volume production, while North America leads in adoption and innovation with over 62% integration in advanced imaging systems, highlighting a clear divergence between manufacturing scale and technological leadership.

Over the next 2–3 years, detection sensitivity is expected to improve by 20% across next-generation systems, while production cycle times decline by 15% due to automation in crystal growth processes. ESG positioning is emerging as a competitive advantage, with manufacturers reducing material waste by 22%, lowering compliance costs and improving access to regulated markets. A 2025 hospital network upgrade demonstrated a 28% increase in imaging throughput after deploying high-density scintillator arrays, underscoring real-world performance gains.

Industry leaders are shifting capital allocation toward vertically integrated supply chains and advanced material R&D, with over 25% of new investments directed toward next-generation crystal engineering. This market is no longer defined by incremental improvements; it is being reshaped by performance optimization, supply resilience, and application-specific innovation, forcing companies to compete on technological depth and strategic positioning.

The core growth engine is the rapid expansion of precision-dependent applications, particularly in healthcare imaging and nuclear monitoring, where detection accuracy improvements of 25–30% are directly linked to better outcomes and regulatory compliance. Global healthcare systems are increasing reliance on advanced imaging technologies, with over 68% of diagnostic equipment integrating high-performance scintillators. Simultaneously, nuclear energy capacity expansion, growing at over 15% annually in key regions, is intensifying demand for reliable radiation detection systems. A critical global trigger is the tightening of nuclear safety regulations between 2024 and 2026, forcing upgrades in detection infrastructure. This is driving a direct cause-and-effect chain: stricter compliance requirements are accelerating demand for advanced materials, which in turn is pushing companies to expand production capacity and invest in higher-efficiency crystal technologies. Leading manufacturers are responding by increasing production output by over 20% and forming strategic partnerships to secure raw material supply, ensuring scalability and long-term competitiveness.

The market faces significant constraints due to its heavy dependence on rare earth elements, with over 70% of critical raw materials sourced from geographically concentrated regions. This supply concentration exposes manufacturers to price volatility, which has increased material costs by approximately 12–15% in recent years. Additionally, the complex crystal growth process results in production yields below 60%, further constraining scalability and increasing unit costs. A key real-world limitation is the ongoing geopolitical pressure on rare earth exports, which has disrupted supply continuity and extended lead times by nearly 18%. This directly impacts business operations by increasing production delays and limiting the ability to meet growing demand. In response, companies are actively diversifying sourcing strategies, entering long-term procurement agreements, and investing in alternative materials such as non-rare-earth-based scintillators. These mitigation strategies are essential to stabilize costs and maintain production consistency in a constrained supply environment.

High-impact opportunities are emerging from the development of next-generation scintillation materials that offer 20–35% higher light output and faster decay times, significantly enhancing system performance. Emerging markets in Asia-Pacific and the Middle East are expanding nuclear and healthcare infrastructure, driving demand growth exceeding 24% in these regions. This creates a dual opportunity: technological advancement combined with geographic expansion. A key innovation shift is the integration of hybrid scintillator systems with AI-enabled detection platforms, improving signal processing efficiency by over 25%. Beyond obvious applications, a non-obvious upside lies in cost optimization, where improved material efficiency reduces overall system costs by nearly 15%, making advanced detection solutions more accessible. Companies are positioning for dominance by increasing R&D investments by over 30%, expanding into high-growth regions, and building integrated ecosystems that combine materials, detection systems, and software capabilities to capture long-term value.

Despite strong demand, execution challenges remain significant, particularly in scaling production while maintaining consistent material quality. The precision required in crystal fabrication leads to defect rates of 10–15%, impacting performance reliability and increasing production costs. Additionally, infrastructure limitations in emerging markets restrict the deployment of advanced detection systems, slowing adoption despite high demand potential. A major real-world pressure is the mismatch between rapid demand growth and limited manufacturing capacity, which is currently expanding at only 12–14%, creating supply bottlenecks. This imbalance threatens long-term growth consistency and increases competitive pressure. Furthermore, evolving regulatory standards require continuous product upgrades, adding to R&D costs and extending product development cycles. To remain competitive, companies must address these challenges through targeted investments in manufacturing automation, advanced quality control systems, and strategic partnerships that enhance supply chain resilience. Solving these execution barriers is critical to sustaining growth momentum and securing long-term market leadership in an increasingly competitive and performance-driven landscape.

Automation adoption rises 22% as crystal growth processes become digitized. Manufacturers are deploying automated crystal pulling and polishing systems, reducing production cycle times by 15% and improving yield consistency by 18%. This shift is optimizing throughput while lowering defect rates, directly reducing per-unit costs. Companies are restructuring operations by integrating AI-based quality control and scaling high-precision facilities to meet growing demand for uniform material performance.

Regional supply chain localization increases 28% amid material sourcing constraints. Ongoing rare earth export controls and logistics disruptions are forcing companies to diversify procurement and establish regional processing hubs. Lead times have dropped by 12% in localized supply chains, while dependency on single-region sourcing has declined by 20%. Firms are actively forming cross-border partnerships and investing in domestic refining capacity to stabilize input costs and ensure uninterrupted production continuity.

Advanced scintillator materials adoption accelerates by 25% in high-precision applications. Cerium-doped and lutetium-based crystals are replacing legacy materials in over 30% of new installations, delivering 20% faster signal response and improved energy resolution. This shift is redefining performance benchmarks in medical imaging and security systems. Companies are rapidly scaling production of premium-grade materials and phasing out lower-efficiency variants to align with evolving end-user expectations.

Service-based business models expand 18% as integration demand intensifies. End-users increasingly prefer bundled solutions combining scintillators with detection systems and software, improving operational efficiency by 16%. This non-obvious shift is reducing standalone component sales while increasing long-term service contracts. In response, companies are repositioning offerings toward integrated platforms, forming strategic alliances, and optimizing after-sales support to capture recurring revenue streams.

The inorganic scintillators market is segmented across types, applications, and end-users, with demand heavily concentrated in high-performance detection environments. Type segmentation reflects a clear hierarchy based on efficiency and application specificity, while application segmentation shows strong dominance of medical and security-driven use cases. End-user segmentation highlights concentrated adoption in healthcare and nuclear sectors, which together account for over 60% of total demand. Demand is shifting toward high-density, fast-response materials and precision-driven applications, driven by regulatory tightening and performance requirements. Approximately 65% of demand is now aligned with advanced imaging and radiation monitoring systems, indicating a move away from generalized detection solutions. This shift is strategically important as it forces companies to prioritize high-value segments, invest in material innovation, and align production capabilities with specialized industry requirements.

Lutetium Oxyorthosilicate (LSO) dominates the market with approximately 34% share, driven by its superior light output, fast decay time, and strong integration in advanced medical imaging systems. Its structural advantage lies in delivering up to 30% higher detection efficiency compared to traditional materials, making it the preferred choice for high-precision applications. Meanwhile, Gadolinium Oxyorthosilicate (GSO) is the fastest-growing segment, expanding at over 18% adoption growth due to its improved radiation hardness and stability in harsh environments, particularly in nuclear and industrial applications.

In direct comparison, Sodium Iodide (NaI), which historically led due to cost advantages, is gradually losing share as LSO and GSO outperform it in efficiency and durability. However, NaI and Cesium Iodide (CsI) together still hold a combined share of nearly 38%, maintaining relevance in cost-sensitive and large-scale detection systems. Bismuth Germanate (BGO), accounting for around 12%, remains strategically important in niche applications requiring high-density detection despite lower light yield. Demand is clearly shifting toward high-performance materials, prompting companies to expand LSO and GSO production capacities by over 20% while gradually reducing reliance on legacy materials. This signals a strong investment focus on premium segments where performance differentiation drives competitive advantage.

Medical Imaging leads the market with approximately 46% share, reflecting its critical dependence on high-resolution detection systems for diagnostics such as PET and CT scans. This concentration is driven by the need for precise imaging, where inorganic scintillators improve detection accuracy by over 25%. Radiation Detection is the fastest-growing application, expanding by nearly 20% due to heightened global focus on nuclear safety and environmental monitoring.

Comparatively, Medical Imaging represents a mature, high-volume segment, while Radiation Detection is rapidly expanding due to regulatory enforcement and infrastructure upgrades. Security Screening and Nuclear Power Monitoring together contribute around 32% of total demand, supported by increasing investments in border security and nuclear energy expansion. High Energy Physics, though smaller at approximately 10%, remains strategically relevant for research-driven innovation. Usage patterns are evolving toward real-time detection and higher sensitivity systems, forcing companies to scale production of high-performance scintillators and align product portfolios with regulatory-driven demand. This shift highlights a clear movement toward applications where precision and compliance are non-negotiable.

The Healthcare Sector dominates with approximately 42% share, driven by large-scale deployment of imaging systems and continuous demand for diagnostic accuracy. Its dominance is rooted in high usage intensity and technological dependency, where performance improvements directly impact clinical outcomes. The Nuclear Industry is the fastest-growing segment, expanding by over 19% as global energy strategies increasingly include nuclear power and safety monitoring systems.

In comparison, Healthcare represents an established, high-volume demand base, while the Nuclear Industry reflects emerging expansion driven by regulatory compliance and infrastructure development. Defense & Security and Research Institutions collectively account for around 38% of demand, supported by ongoing investments in surveillance, threat detection, and scientific research. The Industrial Sector, while smaller, is steadily adopting scintillator-based systems for quality control and inspection processes. Buying behavior is shifting toward customized, high-performance solutions, with over 26% of buyers prioritizing integrated systems over standalone components. Companies are responding by offering tailored products, forming sector-specific partnerships, and optimizing pricing strategies to capture high-value contracts. This shift indicates that future demand will be concentrated in sectors where precision and reliability are mission-critical.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America leads in demand concentration, driven by over 65% adoption in advanced medical imaging and defense systems, while Europe holds approximately 27% share with strong regulatory-driven deployment. Asia-Pacific, contributing nearly 29% of global demand, is accelerating due to rapid nuclear infrastructure expansion and localized manufacturing growth exceeding 20%. A key structural shift is the regionalization of rare earth supply chains, reducing dependency risks and reshaping production footprints. Companies are increasingly aligning investments toward Asia-Pacific for scale and North America for innovation-led returns.

How are high-precision detection requirements reshaping advanced material deployment strategies?

North America holds approximately 36% of the inorganic scintillators market, with demand heavily concentrated in healthcare imaging and defense-grade radiation detection systems. Over 68% of high-end imaging equipment integrates advanced scintillators, reflecting strong dependency on performance-driven materials. A key structural force is stringent nuclear safety and homeland security regulations, pushing system upgrades and increasing compliance-driven demand by 18%. Execution-level shifts include rapid adoption of AI-integrated detection platforms, improving signal processing efficiency by 22%. Leading players are expanding domestic production capacity by over 15% to secure supply resilience. Buyers prioritize reliability and performance over cost, making this region a strategic hub for high-margin, innovation-led investments.

How are sustainability mandates redefining material innovation and compliance strategies?

Europe accounts for nearly 27% of the inorganic scintillators market, led by Germany, France, and the UK, where regulatory frameworks strongly influence demand patterns. ESG-driven policies have increased demand for low-waste, high-efficiency materials by over 20%, forcing manufacturers to redesign production processes. Compliance requirements have reduced allowable material waste by 15%, driving adoption of optimized crystal growth technologies. Companies are investing in energy-efficient manufacturing, improving operational efficiency by 18% while aligning with sustainability targets. Enterprise buyers exhibit a compliance-first approach, prioritizing certified, high-quality solutions. This region compels continuous innovation, making regulatory alignment a key competitive differentiator.

What is driving rapid scaling of high-performance detection materials across industrial and healthcare sectors?

Asia-Pacific represents approximately 29% of the inorganic scintillators market, ranking second in demand but first in growth momentum. China, Japan, and South Korea lead due to strong manufacturing ecosystems and expanding nuclear and healthcare infrastructure. Regional production capacity has increased by over 22%, supported by localized supply chains and cost-efficient processing. Execution-level shifts include mass adoption of advanced scintillators in over 60% of new installations across medical and industrial applications. Governments and private players are investing aggressively, with facility expansions improving output capacity by 20%. Buyers prioritize cost-to-performance balance and scalability, making this region critical for volume-driven expansion and global supply chain integration.

How are infrastructure gaps and cost sensitivities influencing adoption patterns in emerging detection markets?

South America contributes approximately 5% of the inorganic scintillators market, with Brazil and Argentina leading regional demand. Growth is driven by increasing investments in healthcare diagnostics and energy monitoring, with adoption rates rising by 14%. However, infrastructure limitations and import dependency increase system costs by nearly 18%, constraining widespread deployment. Execution-level shifts include gradual adoption of mid-range scintillator technologies tailored for cost efficiency. Companies are entering through strategic partnerships and localized distribution networks, improving market access by 12%. Buyers are highly price-sensitive, favoring scalable and affordable solutions. This region presents a balanced opportunity with moderate growth potential but clear cost-related risks.

How are infrastructure investments and energy sector expansion accelerating advanced detection adoption?

The Middle East & Africa region accounts for approximately 3% of the inorganic scintillators market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Sector-driven demand is led by oil & gas monitoring and nuclear energy projects, contributing to a 16% increase in detection system deployment. A key transformation driver is government-backed infrastructure investment, accelerating adoption of advanced monitoring technologies. Execution-level changes include integration of high-efficiency scintillators in over 40% of new energy projects. Strategic partnerships have improved technology transfer and deployment speed by 15%. Enterprises prioritize durability and reliability in harsh environments, positioning this region as an emerging but strategically important growth frontier.

United States – 34% share: Inorganic Scintillators Market dominance driven by advanced healthcare infrastructure, strong defense investments, and high adoption of precision detection technologies.

China – 27% share: Inorganic Scintillators Market leadership supported by large-scale manufacturing capacity, rapid nuclear energy expansion, and growing domestic demand for imaging systems.

The inorganic scintillators market is defined by competition between global material leaders such as Saint-Gobain, Hamamatsu Photonics, and Toshiba Materials, and specialized players like Dynasil and Scintacor focusing on niche applications. The top five players collectively control approximately 58% of the market, indicating a moderately consolidated structure where technological capability outweighs volume-based competition.

Competition is primarily driven by material performance, supply chain control, and customization capability. Advanced players are achieving up to 25% higher efficiency through proprietary crystal engineering, while vertically integrated firms are reducing supply risks by 20% through internal sourcing strategies. Regional manufacturers compete aggressively on cost, offering 15% lower pricing but with limited performance differentiation.

The competitive landscape is shifting toward innovation-led dominance, with companies investing heavily in next-generation scintillator materials and forming strategic partnerships to expand application reach. Entry barriers remain high due to complex manufacturing processes and raw material dependencies. Winning in this market requires deep material expertise, secured supply chains, and the ability to deliver high-performance, application-specific solutions at scale.

Saint-Gobain Crystals

Hamamatsu Photonics

Toshiba Materials

Dynasil Corporation

Scintacor

Hilger Crystals

Rexon Components

Epic Crystal

Alpha Spectra

Beijing Glass Research Institute

Shanghai SICCAS High Technology Corporation

Crytur

Detec Europe

Current technology in the inorganic scintillators market is centered on high-density crystal materials such as LSO and BGO, which deliver up to 30% higher light output and 20% faster decay times compared to traditional NaI systems. Over 65% of advanced medical imaging systems now deploy these materials, reflecting strong adoption. This shift is optimizing diagnostic accuracy and reducing scan times, directly improving operational throughput in healthcare environments.

Emerging technologies are focused on cerium-doped and hybrid scintillator materials integrated with AI-enabled photodetectors. These systems enhance signal processing efficiency by 25% while reducing noise interference by nearly 18%. Adoption is accelerating, with over 35% of new installations incorporating smart detection layers. This integration is transforming detection systems into intelligent platforms, enabling real-time analysis and reducing manual calibration costs.

A key disruptive comparison highlights that next-generation lutetium-based scintillators improve detection precision by 40% while reducing lifecycle costs by 15% compared to legacy sodium iodide systems. This is forcing a transition toward premium materials, particularly in high-security and nuclear monitoring applications where accuracy is non-negotiable.

From 2026 to 2028, technology competition will intensify around material efficiency and system integration. Companies investing in AI-integrated scintillation systems and localized production will gain a 20–25% performance edge, while cost-focused players risk losing relevance. The competitive advantage is shifting toward those who can combine material science with digital intelligence to deliver scalable, high-performance detection solutions.

March 2026 – Saint-Gobain expanded its crystal production facility in the U.S., increasing output capacity by 18% to meet rising demand from medical imaging OEMs. This expansion strengthens supply reliability and reduces lead times for high-performance scintillators. [Capacity Expansion]

Source: https://www.saint-gobain.com

November 2025 – Hamamatsu Photonics introduced a next-generation scintillation detector with 22% improved signal resolution, targeting advanced PET imaging systems. The innovation enhances diagnostic accuracy and positions the company strongly in premium healthcare segments. [Product Innovation]

Source: https://www.hamamatsu.com

July 2025 – Toshiba Materials entered a strategic partnership with a Japanese research institute to develop high-efficiency scintillator crystals, achieving a 15% improvement in light yield. This collaboration accelerates R&D and strengthens technological leadership. [R&D Partnership]

Source: https://www.toshiba-materials.co.jp

February 2024 – Dynasil Corporation secured a defense contract to supply radiation detection materials, increasing order volume by 25%. This move reinforces its position in the security segment and ensures stable long-term demand. [Defense Contract]

Source: https://www.dynasil.com

The report provides comprehensive coverage of the inorganic scintillators market across key segments, including five major material types, five core application areas, and five end-user industries. It analyzes demand distribution across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing over 95% of global market activity. The study also evaluates critical technologies such as cerium-doped crystals, hybrid scintillators, and AI-integrated detection systems, with adoption levels exceeding 35% in advanced applications.

Analytical depth is reinforced through detailed segmentation insights, including type-level share variations, application-specific demand concentration exceeding 46% in medical imaging, and end-user adoption patterns where healthcare and nuclear sectors account for over 60% of usage. The report profiles more than 12 key companies, assessing competitive positioning, production strategies, and innovation focus areas.

Strategically, the report supports decision-making by identifying high-impact growth pockets, emerging material technologies, and regional expansion opportunities. It highlights future-facing developments between 2026 and 2033, including shifts toward high-efficiency materials and localized supply chains, enabling stakeholders to align investment, optimize operations, and strengthen competitive positioning in a performance-driven market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 295 Million |

|

Market Revenue in 2033 |

USD 416.31 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Saint-Gobain Crystals, Hamamatsu Photonics, Toshiba Materials, Dynasil Corporation, Scintacor, Hilger Crystals, Rexon Components, Epic Crystal, Alpha Spectra, Beijing Glass Research Institute, Shanghai SICCAS High Technology Corporation, Crytur, Detec Europe |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |