Reports

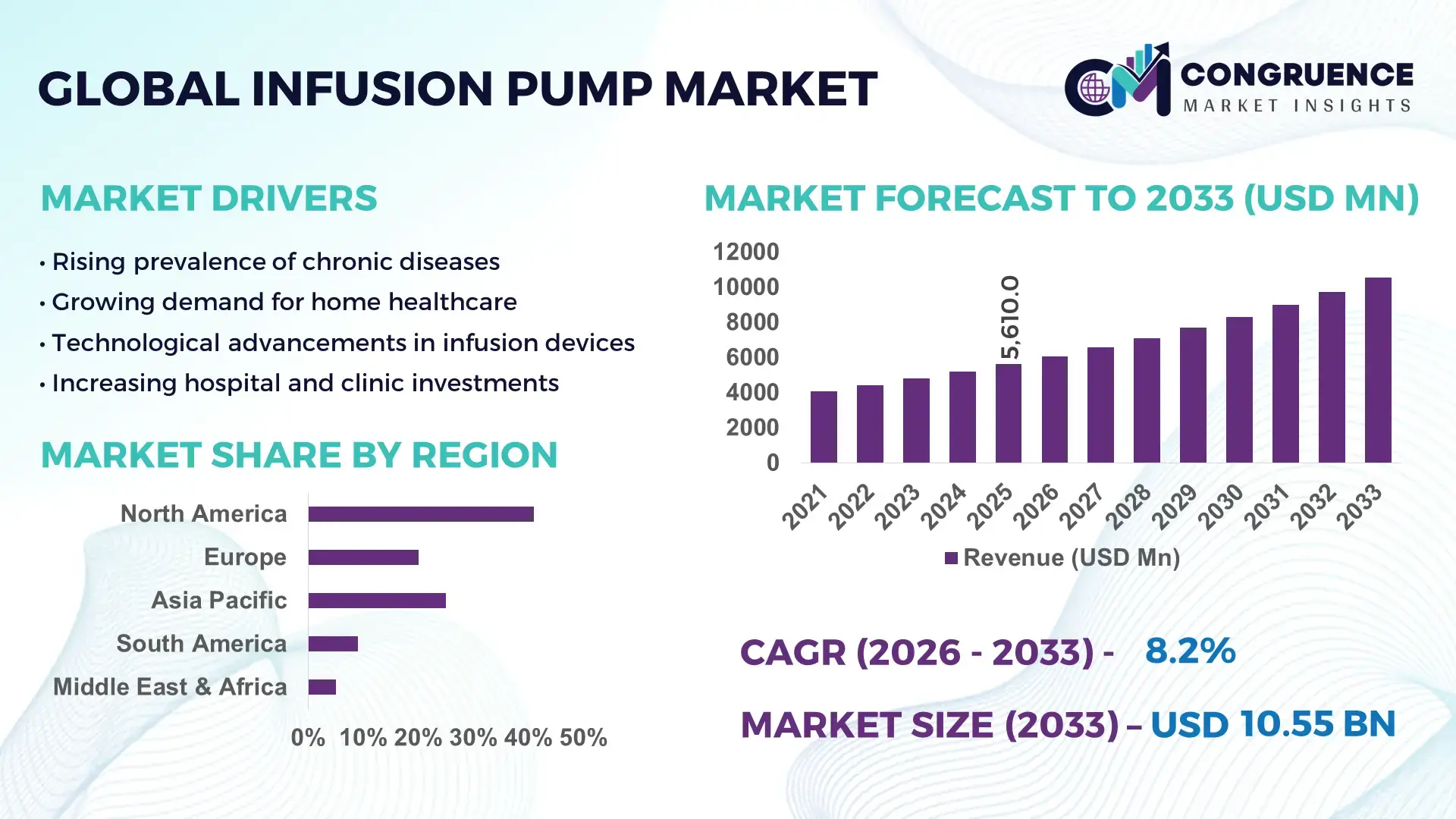

The Global Infusion Pump Market was valued at USD 5610 Million in 2025 and is anticipated to reach a value of USD 10550 Million by 2033 expanding at a CAGR of 8.21% between 2026 and 2033. Growth is primarily driven by rising chronic disease prevalence and the increasing demand for precision drug delivery systems across hospitals and home healthcare settings.

The United States leads the global infusion pump industry with advanced manufacturing capabilities and significant healthcare infrastructure investment. Over 6,000 hospitals across the country utilize smart infusion systems integrated with electronic health records. Annual healthcare spending exceeds USD 4 trillion, supporting large-scale procurement of volumetric and syringe infusion pumps. The country also records more than 37 million hospital admissions annually, creating substantial demand for continuous intravenous therapies. Strong R&D investments exceeding USD 200 billion annually across the medical technology sector have accelerated the development of wireless-enabled, dose-error reduction software (DERS) integrated pumps, improving medication safety and workflow efficiency in acute care environments.

Market Size & Growth: Valued at USD 5610 Million in 2025, projected to reach USD 10550 Million by 2033 at a CAGR of 8.21%, fueled by increased adoption of advanced infusion therapy systems and expanding geriatric populations.

Top Growth Drivers: Chronic disease prevalence +18%, hospital automation adoption +24%, home infusion therapy demand +21%.

Short-Term Forecast: By 2028, smart infusion pump deployment is expected to improve medication accuracy by 30% and reduce adverse drug events by 22%.

Emerging Technologies: Integration of wireless connectivity, AI-enabled drug libraries, and cloud-based infusion monitoring platforms enhancing patient safety and operational visibility.

Regional Leaders: North America projected to exceed USD 4200 Million by 2033 with high smart pump adoption; Europe to surpass USD 3100 Million driven by hospital modernization; Asia-Pacific to reach USD 2600 Million supported by expanding healthcare infrastructure.

Consumer/End-User Trends: Hospitals account for over 60% of demand, with rising home healthcare usage growing at double-digit rates due to cost-efficient chronic care management.

Pilot or Case Example: A 2024 hospital network implementation of interoperable infusion pumps reduced medication errors by 28% and improved workflow efficiency by 19%.

Competitive Landscape: Market leader Baxter International Inc. holds approximately 22% share, followed by B. Braun Melsungen AG, BD (Becton, Dickinson and Company), ICU Medical Inc., and Fresenius Kabi.

Regulatory & ESG Impact: Stricter infusion device safety standards and digital health regulations are promoting smart pump adoption, while sustainability initiatives encourage energy-efficient and recyclable device components.

Investment & Funding Patterns: Over USD 1.8 Billion invested globally in infusion technology upgrades and digital medication management platforms between 2023–2025.

Innovation & Future Outlook: Advancements in closed-loop systems, interoperability with hospital information systems, and portable ambulatory pumps are shaping next-generation infusion therapy delivery models.

The infusion pump market serves critical healthcare sectors including oncology, critical care, pediatrics, and diabetes management, with hospitals contributing nearly 60% of total industry demand, ambulatory surgical centers around 20%, and home healthcare exceeding 15%. Recent product innovations such as programmable smart pumps, wireless data transmission, and advanced safety alarm systems have enhanced drug delivery accuracy and compliance. Regulatory frameworks emphasizing medication error reduction, combined with economic pressures to reduce inpatient stays, are accelerating adoption of ambulatory and wearable infusion systems. Asia-Pacific demonstrates rapid consumption growth due to expanding hospital infrastructure and rising chronic disease burden, while Europe emphasizes compliance-driven upgrades. Long-term industry outlook indicates sustained expansion supported by digital integration, precision medicine trends, and cost-efficient patient-centric care models.

The Infusion Pump Market holds strategic relevance within modern healthcare systems due to its direct impact on medication accuracy, patient safety, and operational efficiency across acute and chronic care settings. With more than 60% of hospital-based intravenous therapies relying on programmable infusion devices, healthcare providers are prioritizing digital infusion platforms to reduce medication errors and optimize clinical workflows. Interoperable smart pump systems integrated with electronic medical records are becoming a core procurement criterion in tertiary hospitals and integrated delivery networks.

From a technology standpoint, AI-enabled dose error reduction software delivers 35% improvement in medication accuracy compared to conventional standalone volumetric infusion pumps. North America dominates in volume, while Asia-Pacific leads in adoption with nearly 48% of newly commissioned hospitals deploying wireless-enabled infusion systems. This regional divergence highlights both infrastructure maturity and rapid digital transformation across emerging economies.

By 2028, predictive analytics–driven infusion management platforms are expected to reduce adverse drug events by 25% and improve nursing workflow efficiency by 20%. Firms are committing to ESG metrics such as 30% recyclable component usage and 20% energy consumption reduction by 2030 to align with hospital sustainability mandates. In 2024, BD (Becton, Dickinson and Company) reported a 28% reduction in infusion-related medication errors across pilot hospitals through advanced interoperability integration initiatives. Strategically, the Infusion Pump Market is positioned as a foundational pillar of clinical resilience, regulatory compliance, and sustainable healthcare delivery, supporting long-term digital transformation and value-based care models.

The global rise in chronic illnesses such as diabetes, oncology conditions, and autoimmune disorders significantly increases demand for continuous drug administration systems. Over 10 million chemotherapy treatments are administered annually worldwide, many requiring precise infusion dosing protocols. Insulin pump therapy adoption has expanded steadily, particularly in developed healthcare systems, improving glycemic control by nearly 20% compared to multiple daily injections. In critical care units, approximately 90% of admitted patients receive intravenous medications, reinforcing reliance on advanced infusion pumps. Aging populations further intensify utilization, as individuals above 65 years represent a growing share of hospital admissions and long-term care services. These demographic and epidemiological shifts are structurally expanding the installed base of infusion devices across hospitals, specialty clinics, and home healthcare settings.

Advanced smart infusion pumps integrated with interoperability software and cybersecurity modules carry higher upfront acquisition costs compared to traditional volumetric devices. A fully integrated hospital-wide infusion management system can require multimillion-dollar capital expenditure, particularly when including training, system upgrades, and network integration. Maintenance expenses, software licensing fees, and periodic calibration requirements increase total cost of ownership. In emerging markets, limited reimbursement coverage for infusion therapies restricts adoption, particularly in smaller hospitals and rural clinics. Additionally, device recalls linked to software glitches or mechanical failures disrupt procurement cycles and increase compliance burdens. Budgetary constraints in public healthcare systems may delay replacement of legacy pumps, thereby moderating near-term purchasing decisions.

The rapid growth of home-based infusion therapy offers significant expansion potential. More than 12 million patients globally receive home infusion services annually, driven by cost efficiency and reduced hospital stays. Portable and wearable infusion pumps enable chemotherapy, antibiotic therapy, and parenteral nutrition administration outside clinical settings. Home infusion care can reduce hospitalization costs by up to 30%, incentivizing insurers and providers to adopt decentralized care models. Technological advancements such as remote monitoring and cloud-based dose tracking further enhance patient safety in non-hospital environments. Emerging markets are also investing in telehealth-enabled infusion programs to address physician shortages and improve rural healthcare access, creating new revenue streams and service-based business models.

Infusion pumps are classified as high-risk medical devices, subject to stringent regulatory scrutiny regarding safety, software validation, and interoperability standards. Compliance requirements demand rigorous clinical testing, post-market surveillance, and quality management systems, increasing development timelines. Cybersecurity vulnerabilities in connected infusion systems pose additional operational risks, as unauthorized access could compromise drug dosage accuracy. Healthcare facilities must implement encrypted communication protocols and network safeguards, adding complexity to deployment. Recurring recalls associated with software errors or alarm malfunctions highlight the critical need for robust risk management. These regulatory and cybersecurity pressures necessitate continuous R&D investment and cross-functional governance frameworks, raising barriers for smaller manufacturers while shaping industry consolidation trends.

• 40% Increase in Smart Pump Integration Across Acute Care Facilities: Hospitals are rapidly replacing conventional infusion devices with interoperable smart pumps capable of real-time data exchange. Over 70% of tertiary hospitals now deploy dose error reduction software, reducing medication administration errors by nearly 30%. Integration with electronic health record systems has improved documentation accuracy by 25% and shortened clinical response times by 18%. Healthcare networks implementing centralized infusion management platforms report up to 22% improvement in workflow productivity, strengthening patient safety protocols and operational transparency.

• 35% Growth in Home-Based and Ambulatory Infusion Adoption: The shift toward decentralized care has led to a measurable rise in portable infusion pump utilization. Approximately 45% of long-term antibiotic and parenteral nutrition therapies are now administered outside hospital settings. Wearable infusion pumps have improved patient mobility by 32% and reduced inpatient stays by nearly 27%. Remote monitoring capabilities have enabled a 20% reduction in unplanned readmissions, reinforcing payer and provider interest in cost-efficient home healthcare infusion solutions.

• 28% Expansion in AI-Enabled Predictive Maintenance Systems: Advanced analytics embedded within infusion platforms are transforming equipment lifecycle management. Predictive maintenance algorithms have decreased device downtime by 26% and reduced unscheduled service interventions by 24%. Nearly 50% of newly installed hospital infusion systems now include wireless fleet management dashboards, enabling real-time asset tracking and software updates. These digital enhancements contribute to a 19% improvement in asset utilization rates and strengthen compliance with safety standards.

• 30% Advancement in Cybersecure and Energy-Efficient Device Design: Manufacturers are embedding multi-layer cybersecurity protocols to address rising concerns around connected medical devices. Approximately 60% of new infusion pump models feature encrypted communication modules, lowering system vulnerability incidents by 21%. Simultaneously, energy-efficient power management systems have reduced standby energy consumption by 25%, aligning with hospital sustainability targets. Recyclable component usage has increased by 18%, reflecting industry commitment to environmentally responsible medical device production.

The Infusion Pump Market is segmented by type, application, and end-user, reflecting diverse clinical requirements and technology adoption patterns across healthcare systems. By type, volumetric pumps, syringe pumps, ambulatory pumps, insulin pumps, and enteral feeding pumps form the core product categories, each designed for specific dosage precision and therapy duration. By application, oncology and chemotherapy administration represent the largest utilization segment, followed by diabetes management, pain management, parenteral nutrition, and critical care infusions. End-user segmentation highlights hospitals as the primary deployment centers, while ambulatory surgical centers and home healthcare providers demonstrate increasing adoption due to decentralized treatment models. Approximately 60% of installed infusion systems are concentrated in acute care hospitals, whereas portable devices account for a growing share in outpatient and home-based care settings. This segmentation framework underscores the market’s alignment with chronic disease prevalence, surgical volumes exceeding 300 million procedures annually worldwide, and expanding digital health integration initiatives that prioritize safety and compliance in drug delivery management.

Volumetric infusion pumps currently account for approximately 38% of total device adoption, maintaining leadership due to their versatility in administering fluids, antibiotics, and chemotherapy in high-volume hospital settings. Syringe infusion pumps hold nearly 24%, widely used in neonatal and critical care units where precise low-flow drug delivery is essential. However, ambulatory infusion pumps are rising fastest, expanding at an estimated CAGR of 9.4%, driven by the growing shift toward outpatient chemotherapy and home-based intravenous therapies. Adoption of ambulatory systems is projected to exceed 30% of total portable device installations by 2033 as healthcare systems reduce inpatient stays.

Insulin pumps contribute around 18% of overall demand, supported by increasing diabetes prevalence exceeding 500 million global cases. Enteral feeding pumps and patient-controlled analgesia pumps collectively represent approximately 20%, serving specialized therapeutic niches.

Oncology and chemotherapy infusion dominate application segments, accounting for nearly 34% of overall device utilization, reflecting the global burden of over 19 million new cancer cases annually. Diabetes management applications hold approximately 27%, primarily driven by insulin pump therapy and continuous subcutaneous insulin infusion systems. However, home-based antibiotic and parenteral nutrition therapies are growing fastest, with an estimated CAGR of 10.2%, supported by a 25% reduction in hospitalization duration for eligible patients receiving outpatient infusion care.

Pain management and critical care infusions collectively contribute around 39% of remaining applications, particularly in surgical recovery units and intensive care settings where 90% of admitted patients require intravenous medications.

Hospitals represent the leading end-user segment, accounting for approximately 62% of total infusion pump installations due to high patient volumes and complex therapy requirements. Ambulatory surgical centers contribute nearly 18%, increasingly adopting compact infusion systems to support same-day procedures exceeding 70% of elective surgeries in developed economies. Home healthcare providers are the fastest-growing end-user group, expanding at an estimated CAGR of 11.1%, propelled by aging populations and reimbursement incentives favoring cost-efficient outpatient care models.

Specialty clinics and long-term care facilities collectively represent around 20% of device usage, particularly for chronic disease and palliative treatment programs. Adoption rates in tertiary hospitals exceed 75% for smart infusion systems integrated with electronic health records, while home healthcare infusion penetration has risen above 35% in developed healthcare markets.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America’s dominance is supported by more than 6,000 hospitals and over 900,000 staffed hospital beds actively utilizing programmable infusion systems. Approximately 75% of tertiary care centers in the region have implemented smart infusion pumps integrated with electronic health records. Europe follows with nearly 28% market share, driven by strong regulatory compliance frameworks and over 2.7 million annual cancer diagnoses requiring infusion-based chemotherapy. Asia-Pacific accounts for about 22% of global demand, supported by expanding healthcare infrastructure, with China and India adding over 50,000 new hospital beds annually. South America holds approximately 5%, while the Middle East & Africa contributes nearly 4%, reflecting gradual modernization of hospital systems and increasing adoption of portable infusion technologies.

How Are Advanced Healthcare Infrastructure and Digital Integration Accelerating Clinical Drug Delivery Systems?

North America commands approximately 41% of the global Infusion Pump Market share, supported by high hospitalization rates exceeding 36 million admissions annually. Key demand drivers include oncology, diabetes management, and critical care services, where nearly 90% of ICU patients require intravenous drug administration. Regulatory oversight by the U.S. Food and Drug Administration has strengthened device safety standards, mandating dose error reduction software in newly approved systems. Digital transformation trends show that over 70% of large hospitals deploy interoperable smart pumps connected to centralized monitoring platforms. Local player Baxter International Inc. continues expanding its smart infusion portfolio with wireless-enabled platforms to enhance medication accuracy. Regional consumer behavior indicates higher institutional adoption, with enterprise healthcare networks prioritizing cybersecurity-compliant infusion fleets and automated drug library updates to improve operational efficiency and regulatory compliance.

How Are Regulatory Compliance and Sustainability Mandates Shaping Advanced Infusion Technologies?

Europe represents approximately 28% of the global Infusion Pump Market, with Germany, the United Kingdom, and France accounting for more than 60% of regional installations. Over 2 million chemotherapy cycles are administered annually within the region, sustaining strong demand for programmable infusion devices. Regulatory bodies such as the European Medicines Agency emphasize strict medical device compliance and post-market surveillance, driving upgrades to smart, interoperable systems. Sustainability initiatives targeting 30% reduction in medical device waste by 2030 are encouraging manufacturers to introduce recyclable components and energy-efficient designs. B. Braun Melsungen AG is advancing digital infusion platforms integrated with hospital IT ecosystems, supporting medication error reduction by nearly 25% in pilot facilities. Regional consumer behavior reflects strong regulatory-driven purchasing decisions, with healthcare providers prioritizing traceability, explainable safety features, and environmental compliance in procurement processes.

What Is Driving Rapid Hospital Modernization and Smart Medical Device Adoption?

Asia-Pacific holds roughly 22% of the global Infusion Pump Market and ranks as the fastest-growing regional segment. China, India, and Japan collectively account for over 65% of regional consumption, supported by expanding tertiary hospital networks and rising chronic disease incidence. More than 100,000 new hospital beds have been added across major economies in the past three years, increasing demand for volumetric and ambulatory infusion pumps. Manufacturing hubs in China and Japan are enhancing domestic production capacity, improving supply chain resilience. Regional innovation centers are focusing on compact, cost-efficient infusion systems tailored for outpatient and rural healthcare settings. Consumer behavior in this region shows growing acceptance of portable and wearable infusion technologies, with home-based therapy adoption increasing by over 20% in urban healthcare markets.

How Are Expanding Healthcare Investments and Trade Policies Supporting Medical Device Deployment?

South America contributes approximately 5% to the global Infusion Pump Market, with Brazil and Argentina representing over 70% of regional installations. Public healthcare infrastructure upgrades have expanded intensive care capacity by nearly 15% in leading economies. Government-backed procurement programs aim to modernize hospital equipment, supporting increased acquisition of programmable infusion pumps. Trade policies facilitating medical device imports have improved technology access, while local assembly initiatives are gradually emerging. Regional consumer behavior indicates demand concentrated in urban hospitals, where oncology and surgical departments account for nearly 60% of infusion pump utilization. Healthcare providers prioritize cost-effective and durable systems due to budgetary constraints, creating opportunities for mid-range smart infusion platforms.

How Are Healthcare Modernization Programs Accelerating Advanced Infusion System Adoption?

The Middle East & Africa region accounts for nearly 4% of the global Infusion Pump Market, with the United Arab Emirates and South Africa leading demand. Healthcare modernization initiatives have increased hospital capacity by over 12% in key Gulf countries. Large-scale public hospital expansions and specialty cancer centers are driving adoption of smart infusion pumps with integrated safety software. Trade partnerships with international manufacturers are strengthening supply chains and improving device availability. Regional technology trends emphasize digital monitoring and centralized medication management platforms. Consumer behavior reflects growing preference for advanced, imported infusion systems in private hospitals, while public facilities focus on scalable and energy-efficient devices aligned with national healthcare transformation programs.

United States – 38% market share: Strong hospital infrastructure, high chronic disease burden, and advanced smart infusion pump integration drive dominance in the Infusion Pump Market.

Germany – 9% market share: Robust medical device manufacturing capacity and stringent regulatory compliance standards support sustained leadership in the Infusion Pump Market.

The Infusion Pump Market exhibits a moderately consolidated competitive structure, with the top five manufacturers accounting for approximately 65% of global installations. More than 25 active international and regional competitors operate across volumetric, syringe, insulin, and ambulatory infusion pump categories, creating strong product differentiation and pricing dynamics. Leading players focus on smart pump platforms integrated with dose error reduction software, wireless connectivity, and cybersecurity frameworks to strengthen hospital contracts and long-term service agreements.

Strategic initiatives such as product launches, hospital partnerships, and interoperability collaborations are shaping competitive intensity. Over 60% of new product introductions in the past three years have incorporated cloud-based drug library updates and centralized fleet management capabilities. Mergers and portfolio expansions have enabled broader therapy coverage, particularly in oncology and diabetes infusion segments. Approximately 70% of large hospital networks now procure infusion systems through multi-year bundled agreements that include software, maintenance, and analytics services, favoring established brands with global distribution capabilities. Competitive positioning increasingly depends on regulatory compliance records, recall management performance, and the ability to deliver measurable reductions of up to 30% in medication administration errors through digital integration.

ICU Medical Inc.

Fresenius Kabi

Smiths Medical

Terumo Corporation

Medtronic plc

Moog Inc.

Nipro Corporation

Technological advancement is fundamentally reshaping the Infusion Pump Market, with smart, interoperable, and data-driven systems becoming standard across modern healthcare facilities. More than 70% of newly installed hospital infusion devices now incorporate dose error reduction software (DERS), capable of reducing medication administration errors by up to 30%. These systems rely on programmable drug libraries containing over 1,000 standardized medication profiles, improving dosing accuracy and compliance with safety protocols. Integration with electronic health record platforms enables automatic documentation of infusion parameters, cutting manual charting time by nearly 20% and enhancing clinical workflow efficiency.

Wireless connectivity and centralized fleet management platforms are gaining traction, with approximately 55% of tertiary hospitals deploying real-time infusion monitoring dashboards. These solutions enable remote software updates, device tracking, and predictive maintenance alerts, lowering unplanned downtime by 25% and improving asset utilization rates by nearly 18%. Cybersecurity has also become a priority, as over 60% of connected infusion pumps now incorporate encrypted communication protocols and multi-factor authentication to mitigate unauthorized access risks.

Emerging technologies include closed-loop infusion systems that integrate patient vital signs with automated drug titration, particularly in intensive care and anesthesia applications. Early pilot deployments demonstrate up to 22% improvement in hemodynamic stability management. Additionally, miniaturized wearable infusion pumps for diabetes and oncology applications have reduced device weight by nearly 30%, increasing patient mobility and therapy adherence by over 15%. Artificial intelligence–driven analytics platforms are being tested to predict dosage adjustments based on patient response patterns, potentially decreasing adverse drug events by 20% in controlled hospital environments. Collectively, these innovations position advanced infusion technologies as central to digital healthcare transformation, regulatory compliance, and precision-driven patient care delivery.

• In February 2024, Baxter International Inc. announced U.S. FDA 510(k) clearance for its Novum IQ large volume infusion pump with Dose IQ Safety Software, enabling integration with electronic health records and advanced dose error reduction capabilities. The system enhances interoperability and supports standardized medication libraries across hospital networks. Source: www.baxter.com

• In April 2024, ICU Medical Inc. received U.S. FDA clearance for its Plum Solo precision infusion pump, expanding its IV performance platform portfolio. The device features a cassette-based delivery mechanism designed to reduce free-flow risks and improve medication safety in acute care settings. Source: www.icumed.com

• In 2024, B. Braun Melsungen AG expanded its Spaceplus infusion pump system rollout across European hospitals, introducing enhanced cybersecurity functions and integrated drug library management. The upgraded platform supports centralized fleet monitoring and aligns with updated EU Medical Device Regulation compliance requirements. Source: www.bbraun.com

• In January 2025, BD (Becton, Dickinson and Company) announced expanded global deployment of its BD Alaris infusion system with updated interoperability features, enabling automated infusion documentation and improved medication management. The upgrade strengthens integration with hospital IT ecosystems and enhances real-time clinical decision support tools. Source: www.bd.com

The Infusion Pump Market Report provides a comprehensive assessment of device categories, therapeutic applications, technological advancements, and geographic deployment trends across more than 25 countries. The report covers key product segments including volumetric infusion pumps, syringe pumps, ambulatory pumps, insulin pumps, enteral feeding pumps, and patient-controlled analgesia systems. Together, volumetric and syringe pumps account for over 60% of global installations, while portable and wearable systems represent a rapidly expanding niche aligned with decentralized care models.

From an application perspective, the report evaluates oncology, diabetes management, critical care, pain management, parenteral nutrition, and antibiotic therapy segments. Oncology and diabetes collectively represent more than 50% of infusion device utilization globally, driven by over 19 million annual cancer cases and more than 500 million diabetes patients worldwide. The study also examines hospital-based installations, which exceed 60% of total deployments, alongside ambulatory surgical centers and home healthcare providers, where portable infusion adoption has surpassed 35% in developed healthcare markets.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing infrastructure expansion, regulatory frameworks, digital health integration, and procurement models. Technological focus areas include smart infusion systems with dose error reduction software, wireless fleet management, interoperability platforms, predictive maintenance analytics, cybersecurity enhancements, and closed-loop drug delivery innovations. Additionally, the report addresses compliance standards, medical device regulations, sustainability initiatives targeting 20%–30% recyclable component usage, and evolving reimbursement models influencing purchasing decisions. This structured coverage enables stakeholders to evaluate competitive positioning, technology adoption patterns, and sector-specific opportunities within the global infusion therapy ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.21% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Baxter International Inc., B. Braun Melsungen AG, BD (Becton, Dickinson and Company), ICU Medical Inc., Fresenius Kabi, Smiths Medical, Terumo Corporation, Medtronic plc, Moog Inc., Nipro Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |