Reports

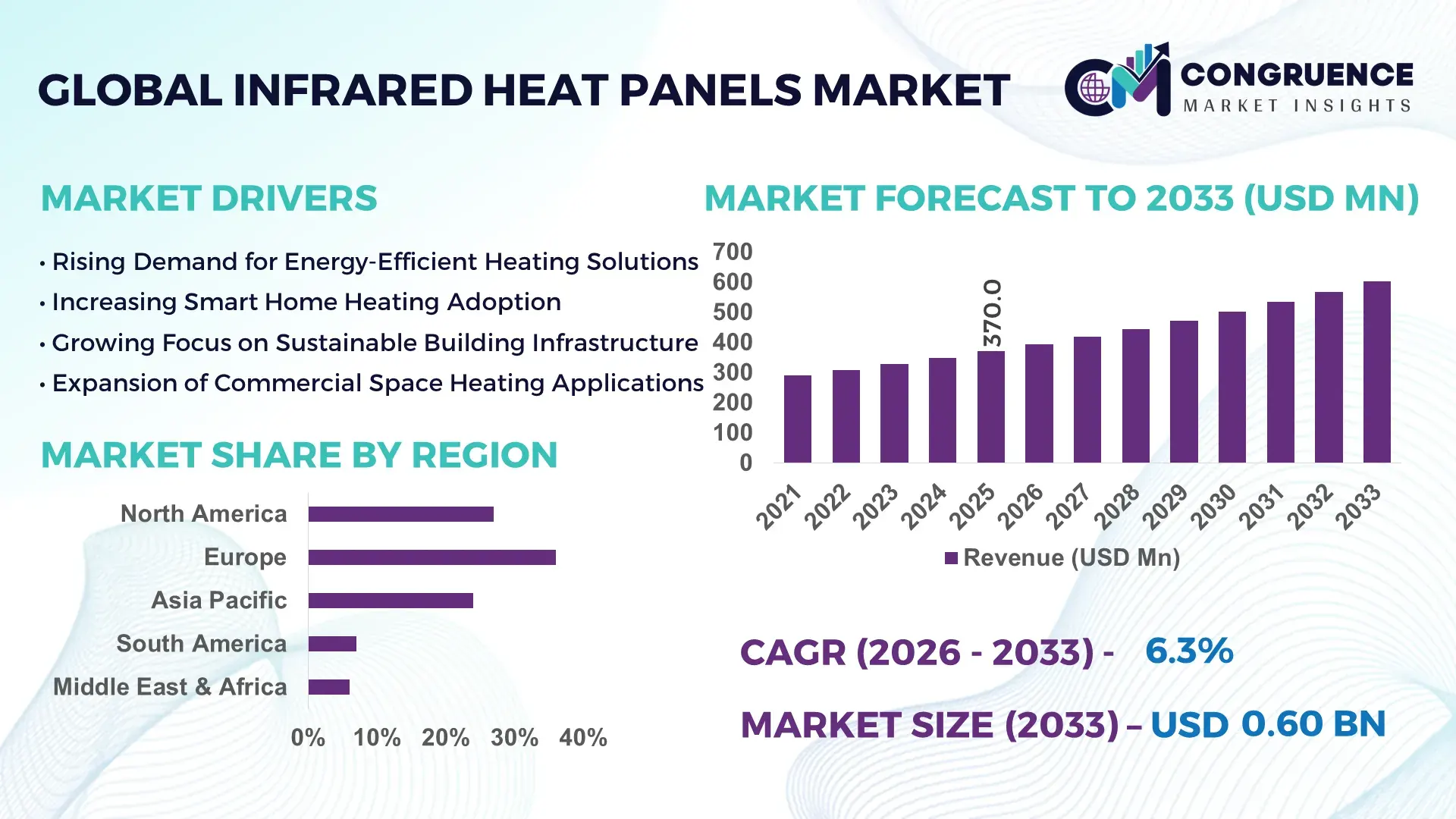

The Global Infrared Heat Panels Market was valued at USD 370 Million in 2025 and is anticipated to reach a value of USD 603.2 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033.

Rising electrification of residential and commercial heating systems, combined with increasing adoption of low-energy radiant technologies, is accelerating deployment of infrared heat panels across smart buildings, industrial warehouses, healthcare facilities, and energy-efficient housing projects. Compared to conventional convection heaters, advanced infrared systems reduce energy consumption by nearly 28% while improving zone-heating efficiency by over 35%, making them increasingly preferred in regions facing high electricity and gas price volatility. Between 2024 and 2026, the market has been reshaped by Europe’s building decarbonization mandates, tightening carbon-emission targets, and supply-chain diversification away from volatile fossil-fuel-dependent heating infrastructure. Demand for wall-mounted and ceiling-integrated infrared systems increased by 22% across retrofit projects as commercial property owners prioritized lower maintenance costs and faster heating response times.

Germany continues to dominate the global infrared heat panels market with approximately 24% market share, supported by aggressive building-efficiency regulations, large-scale smart home adoption, and strong manufacturing capabilities. Over 41% of newly upgraded energy-efficient residential projects in Germany integrated electric radiant heating technologies during 2025, while industrial heating modernization investments exceeded USD 1.2 billion across logistics and automotive facilities. The country also benefits from rapid heat-pump ecosystem expansion and strong integration of IoT-enabled thermal control systems, improving operational energy optimization by nearly 30% compared to legacy electric heating infrastructure.

The competitive landscape is shifting toward intelligent, low-emission heating ecosystems where operational efficiency, energy responsiveness, and regulatory alignment are becoming decisive factors for long-term market positioning and investment allocation.

Market Size & Growth: USD 370 Million in 2025 reaching USD 603.2 Million by 2033, driven by 28% lower energy consumption and accelerating smart-building electrification.

Top Growth Drivers: Energy-efficient heating adoption surged 31%, retrofit installations increased 22%, and carbon-compliance investments expanded 26% globally.

Short-Term Forecast: By 2028, intelligent infrared heating systems are projected to improve heating efficiency by 35% while reducing maintenance costs by 18%.

Emerging Technologies: AI-enabled thermal sensors, graphene-based heating elements, and IoT-integrated control systems improved response efficiency by nearly 27%.

Regional Leaders: Europe exceeded USD 150 Million demand led by retrofit adoption, Asia-Pacific crossed USD 120 Million via manufacturing expansion, and North America surpassed USD 95 Million through smart-home integration.

Consumer/End-User Trends: More than 46% of commercial retrofit projects now prioritize infrared heating for rapid-zone heating and operational energy optimization.

Pilot/Case Example: In 2025, a German logistics project reduced warehouse heating costs by 32% after deploying ceiling-mounted infrared panel systems.

Competitive Landscape: Top five companies control nearly 48% share, with Herschel, Frico, Königshaus, Ecaros, and ThermoUp competing through efficiency-focused innovation.

Regulatory & ESG Impact: EU building-efficiency policies accelerated electric radiant heating adoption by 29% while reducing carbon-intensive heating dependence.

Investment & Funding: Global heating electrification investments exceeded USD 2.4 billion between 2024–2026, fueled by industrial retrofits and regional manufacturing expansion.

Innovation & Future Outlook: Ultra-thin carbon crystal panels and AI-based heat zoning are reshaping advanced infrared heating deployment across high-efficiency infrastructure projects.

Commercial buildings contribute nearly 38% of total infrared heat panel demand due to rising retrofitting activity and pressure to reduce operational energy intensity. Residential applications account for over 34% adoption as smart-home integration and silent heating preferences accelerate deployment. Industrial facilities are increasingly adopting ceiling-mounted infrared systems, improving localized heating efficiency by nearly 30%. Recent graphene-based heating innovations and IoT thermal automation are redefining system responsiveness while European decarbonization mandates and Asian manufacturing expansion continue reshaping global supply dynamics. These shifts are positioning advanced infrared heating technologies as a strategic infrastructure investment priority for energy-focused stakeholders.

The infrared heat panels market is rapidly transforming into a strategic battleground for energy-efficiency leaders, smart-building operators, and industrial infrastructure investors as global heating systems shift away from carbon-intensive technologies. Accelerating electrification targets, rising utility costs, and stricter building-efficiency regulations are forcing commercial and residential operators to adopt precision-controlled heating systems capable of reducing energy waste while optimizing thermal performance. This transition is reshaping procurement priorities across construction, logistics, healthcare, hospitality, and industrial manufacturing sectors.

The market is also experiencing structural pressure from supply-chain realignment and tightening emission regulations across Europe and North America, particularly following energy-security disruptions linked to the Russia–Ukraine conflict. Advanced carbon-crystal infrared technology improves heating efficiency by 35% while reducing operating costs by 24% compared to legacy convection-based electric systems. Europe leads in deployment volume due to aggressive retrofit programs, while Asia-Pacific leads in manufacturing expansion and innovation scaling with over 32% growth in localized production capacity.

Over the next two to three years, smart infrared heating systems integrated with occupancy sensors and AI-driven thermal optimization are projected to reduce commercial energy consumption by nearly 29%. ESG alignment has become a measurable competitive advantage, with low-emission heating retrofits lowering facility compliance costs by approximately 18% across regulated commercial infrastructure projects.

A major logistics operator in Germany reported a 31% reduction in warehouse heating expenses after deploying ceiling-mounted infrared heating systems integrated with automated zoning controls. Simultaneously, leading manufacturers are accelerating capital allocation toward graphene-based heating elements, regional assembly expansion, and smart-control partnerships to secure faster deployment cycles and higher-margin contracts. The market is no longer competing on basic heating functionality alone; companies are competing on energy intelligence, infrastructure integration, operational optimization, and regulatory readiness, making technological positioning and execution speed critical determinants of long-term competitive advantage.

The infrared heat panels market is being reshaped by accelerating electrification trends, building-efficiency mandates, and increasing demand for precision-controlled heating infrastructure. Commercial and residential sectors are rapidly replacing conventional convection systems with radiant heating technologies capable of improving localized thermal efficiency while lowering operational energy consumption. Rising utility-price volatility and stricter emission standards are pushing facility operators toward intelligent electric heating systems with faster response times and lower maintenance requirements. Industrial adoption is also expanding, particularly in logistics, warehousing, and manufacturing environments where targeted heating reduces energy waste by nearly 25%. Simultaneously, manufacturers are investing in thinner heating materials, smart sensor integration, and modular panel designs to improve scalability and installation flexibility. However, the market remains influenced by raw-material pricing fluctuations, electrical infrastructure limitations, and rising competition from heat-pump technologies. Strategic partnerships, regional production expansion, and AI-enabled thermal automation are increasingly defining competitive positioning across the global infrared heat panels ecosystem.

The accelerating transition toward energy-efficient electrified buildings is becoming the primary structural growth engine for infrared heat panels globally. Commercial property operators and residential developers are prioritizing low-energy radiant heating systems capable of reducing electricity consumption by 28% while improving heating responsiveness by nearly 35%. Europe’s tightening building-emission mandates and retrofitting incentives have increased electric heating modernization projects by more than 24% since 2024, forcing rapid adoption across offices, warehouses, healthcare facilities, and residential infrastructure. Rising natural gas price instability following geopolitical energy disruptions has further accelerated the shift toward electrically powered heating technologies. The impact is directly reshaping supplier strategies and capital allocation. Manufacturers are expanding production capacity for carbon-crystal panels, AI-integrated thermal controls, and ultra-thin ceiling-mounted systems to meet rising retrofit demand. Strategic partnerships between smart-building software providers and heating equipment manufacturers have increased by nearly 19% as buyers increasingly demand integrated energy-management ecosystems. Companies are also localizing component sourcing and establishing regional assembly hubs to reduce lead times and strengthen supply-chain resilience. The market is rapidly transitioning from traditional heating equipment sales toward intelligent thermal optimization solutions with long-term operational value.

Despite strong demand momentum, the infrared heat panels market remains constrained by rising raw-material dependency, electrical infrastructure limitations, and installation cost sensitivity. Advanced infrared panels rely heavily on aluminum components, carbon-based heating materials, and semiconductor-driven control systems, all of which experienced price fluctuations exceeding 18% during recent supply-chain disruptions. In many older commercial buildings, electrical retrofitting costs account for nearly 22% of total installation expenditure, slowing large-scale modernization programs.Grid-capacity pressure has also emerged as a structural challenge, particularly across high-density urban regions where electric heating adoption is accelerating faster than power-distribution upgrades. Several European and Asian infrastructure markets continue facing transformer-load constraints and delayed electrification investments, limiting rapid deployment potential. These pressures directly impact project scalability, procurement timelines, and return-on-investment calculations for commercial operators. Companies are mitigating risks through long-term supplier contracts, modular product engineering, and diversification into hybrid thermal systems with lower peak-load requirements. Manufacturers are also increasing investment in lightweight composite heating materials to reduce production dependency on volatile industrial metals. At the same time, firms are expanding installer-training ecosystems to lower deployment complexity and shorten retrofit timelines. Competitive advantage increasingly depends on supply-chain flexibility, electrical integration expertise, and installation efficiency rather than product pricing alone.

The emergence of AI-enabled smart heating ecosystems is opening high-impact expansion opportunities across commercial infrastructure, healthcare facilities, and next-generation residential projects. Intelligent infrared systems integrated with occupancy detection, automated zoning, and IoT energy-management platforms improve thermal efficiency by nearly 33% while reducing operational waste by more than 20%. This shift is redefining infrared heating from a standalone product into an integrated building-performance solution. Demand is rapidly increasing in retrofit-heavy urban markets where building operators are under pressure to reduce emissions without extensive structural reconstruction. Smart infrared deployment in office and logistics environments increased by approximately 27% during 2025 as enterprises prioritized flexible heating control and lower maintenance requirements. Emerging demand pockets are also developing in modular housing, healthcare isolation facilities, and industrial process heating where rapid-response thermal systems provide measurable efficiency gains. Manufacturers are aggressively positioning for future dominance through R&D investment in graphene heating elements, wireless thermal synchronization, and AI-based predictive energy optimization. Strategic ecosystem partnerships between HVAC automation firms and infrared heating manufacturers are accelerating deployment scalability. A non-obvious competitive upside is emerging around data-driven thermal analytics, where companies capable of integrating heating performance insights into broader building-management systems gain stronger long-term customer retention and premium pricing power.

Execution-level scalability risks remain one of the most significant challenges confronting the infrared heat panels market. Large-scale deployment requires electrical infrastructure compatibility, skilled installation networks, and advanced thermal calibration capabilities that remain uneven across regions. Installation complexity in older commercial buildings increases deployment timelines by nearly 21%, while inconsistent energy regulations across countries continue creating procurement uncertainty for multinational infrastructure operators. Performance standardization also remains a critical issue. Lower-cost imported systems often deliver inconsistent heating distribution and reduced lifespan performance, creating buyer hesitation and increasing warranty-related operational costs by approximately 14%. Simultaneously, growing competition from advanced heat-pump systems is forcing infrared manufacturers to demonstrate stronger lifecycle efficiency advantages and faster payback periods. Grid-load limitations represent another long-term pressure point, particularly as electrification accelerates across transportation, industrial automation, and building infrastructure simultaneously. Companies that fail to optimize power management and smart-load balancing risk losing competitiveness in heavily regulated markets. To remain competitive, manufacturers must invest aggressively in intelligent energy-control technologies, installer ecosystems, product certification, and regional production partnerships. Market leadership increasingly depends on execution precision, infrastructure adaptability, and measurable operational performance rather than basic heating functionality alone.

34% Increase in AI-Integrated Thermal Control Deployments Reshaping Smart Heating Operations: Commercial facilities are rapidly integrating AI-enabled infrared heat panels with occupancy sensors and automated zoning systems. Intelligent thermal optimization reduced energy waste by nearly 26% while improving heat-response accuracy by 31%. Companies are restructuring product portfolios around software-connected heating ecosystems as labor shortages and energy-management pressure intensify across large infrastructure assets.

29% Surge in Retrofit Installations Accelerating Across Europe and North America: Building-efficiency mandates and rising utility costs are forcing property owners to replace convection systems with ceiling-mounted infrared panels. Retrofit deployment timelines shortened by 18% due to modular installation designs and wireless control integration. Manufacturers are expanding regional assembly operations to stabilize delivery cycles amid continuing component supply-chain volatility.

41% Expansion in Graphene and Carbon-Crystal Heating Material Adoption Optimizing Performance: Advanced heating materials are redefining panel durability, heat distribution, and response speed. New-generation graphene-based systems improved thermal conductivity by 33% while reducing panel thickness by nearly 25%. Companies are prioritizing lightweight product engineering to improve scalability across modular construction, healthcare infrastructure, and industrial warehousing applications.

22% Shift Toward Subscription-Based Energy Management Models Redefining Commercial Procurement: Commercial buyers increasingly prefer bundled heating-as-a-service contracts that combine infrared systems with predictive maintenance and energy analytics. This model reduced operational maintenance costs by 17% and improved energy-monitoring visibility across multi-site facilities. Providers are forming strategic partnerships with smart-building software firms to strengthen long-term service revenue and customer retention.

The infrared heat panels market is segmented across type, application, and end-user categories, with demand increasingly concentrated around energy-efficient commercial retrofits, smart residential infrastructure, and industrial thermal optimization projects. Ceiling-mounted systems and intelligent wall-panel configurations dominate due to installation flexibility and lower operational energy consumption. Commercial applications account for nearly 38% of deployment volume, while residential adoption continues accelerating through smart-home integration and silent-heating preferences. Demand is also shifting toward healthcare and industrial applications where localized radiant heating improves efficiency by over 25%. End-user purchasing behavior increasingly prioritizes lifecycle energy savings, automation compatibility, and regulatory compliance rather than upfront equipment cost alone. Manufacturers are responding by expanding modular product portfolios, integrating IoT-enabled thermal controls, and strengthening regional distribution networks to capture emerging retrofit and smart-infrastructure opportunities.

Ceiling-mounted infrared heat panels dominate the market with approximately 43% share due to superior space optimization, broader heat distribution, and easier integration across commercial buildings, warehouses, and institutional infrastructure. Their structural advantage lies in reducing floor-space dependency while improving localized heating efficiency by nearly 30%, making them highly scalable for large-area applications. Wall-mounted panels remain widely adopted in residential and hospitality environments because of simplified installation and aesthetic flexibility, collectively contributing around 34% of total demand. Portable infrared heat panels are emerging as the fastest-growing segment, expanding adoption by nearly 26% due to rising demand for flexible heating solutions in modular offices, temporary healthcare units, and hybrid workspace environments. Compared to traditional wall-mounted systems, portable variants provide faster deployment and lower installation costs, although they currently lack the same long-term integration efficiency for large-scale commercial operations. The remaining specialized and hybrid infrared panel systems account for nearly 23% share, serving niche applications requiring smart automation, industrial-grade thermal zoning, or ultra-thin integrated designs. Companies are increasingly prioritizing graphene-enabled ceiling systems, wireless control integration, and lightweight modular engineering to capture high-efficiency retrofit opportunities. Investment momentum is shifting toward scalable intelligent systems capable of delivering measurable operational energy optimization rather than basic standalone heating functionality.

Commercial buildings represent the leading application segment with nearly 38% market share due to aggressive retrofit activity, rising energy-efficiency mandates, and increasing deployment across offices, retail facilities, logistics centers, and healthcare infrastructure. Demand concentration exists because infrared systems reduce localized heating costs by approximately 28% while improving thermal response times in large enclosed environments. Warehousing and logistics applications are particularly accelerating as operators seek targeted heating solutions that minimize wasted energy in high-ceiling facilities. Industrial applications are emerging as the fastest-growing segment, with adoption increasing by nearly 24% as manufacturers modernize process-heating and worker-comfort systems amid rising utility-price pressure. Compared with mature residential deployment, industrial usage is shifting toward intelligent zoning technologies integrated with automated facility-management systems. This operational transition is reshaping supplier priorities toward ruggedized, high-capacity panel systems with advanced thermal controls. Residential and hospitality applications collectively account for nearly 40% of total installations, supported by smart-home integration trends, silent-heating preferences, and compact interior heating requirements. Companies are responding by introducing ultra-thin decorative panel designs, app-controlled heating systems, and AI-based occupancy optimization tools. Demand is increasingly moving toward multifunctional intelligent heating ecosystems capable of balancing comfort, efficiency, and regulatory compliance across multiple infrastructure environments.

The commercial infrastructure sector leads the infrared heat panels market with approximately 41% demand share due to high heating intensity across office buildings, retail centers, warehouses, and institutional facilities. Large-scale facility operators prioritize infrared systems because they reduce maintenance requirements by nearly 20% while enabling precise thermal zoning and lower energy waste. Demand concentration is strongest in retrofit-driven urban environments where building owners face mounting efficiency and emission-compliance pressure. Healthcare and industrial end-users represent the fastest-growing adoption segment, with deployment increasing by nearly 25% as hospitals, laboratories, and manufacturing facilities prioritize controlled, targeted heating environments. Compared with established commercial buyers focused on operational efficiency, healthcare operators emphasize hygiene compatibility, silent operation, and rapid-response thermal management. This distinction is forcing manufacturers to diversify product engineering and customization strategies. Residential and hospitality users collectively contribute around 37% of market demand, driven by rising smart-home adoption and increasing preference for visually integrated low-noise heating systems. Companies are targeting these segments through subscription-based maintenance models, smart-device integration, and premium interior-compatible designs. Future demand is shifting toward intelligent multi-zone systems capable of integrating with broader home-energy ecosystems, making software compatibility and energy analytics increasingly important purchasing criteria.

Europe accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Europe leads in retrofit-driven demand and regulatory-backed electrification programs, with more than 42% of commercial building modernization projects incorporating low-emission heating technologies. Asia-Pacific is accelerating through manufacturing expansion, localized production, and rapid urban infrastructure deployment, while North America maintains strong adoption across smart residential and logistics applications with nearly 27% global demand contribution. South America and the Middle East & Africa collectively account for approximately 13% market share, supported by rising commercial construction and energy-efficiency initiatives. Supply-chain regionalization and building-decarbonization mandates are increasingly reshaping investment flows, with companies prioritizing localized manufacturing, AI-integrated heating systems, and strategic regional partnerships to secure long-term competitive positioning.

North America accounts for nearly 27% of global infrared heat panel demand, driven by strong adoption across smart homes, logistics facilities, and commercial retrofitting projects. Rising electricity-efficiency targets and warehouse modernization are accelerating demand for intelligent radiant heating systems capable of reducing operational energy consumption by approximately 25%. The region is also experiencing structural pressure from stricter building-performance standards and increasing winter energy-cost volatility. Commercial operators are rapidly deploying AI-enabled thermal zoning technologies, with smart infrared installations increasing by nearly 21% across industrial and office facilities during 2025. Several manufacturers expanded regional assembly and distribution capacity by over 18% to reduce delivery lead times and support retrofit demand. Enterprise buyers increasingly prioritize low-maintenance, digitally integrated heating infrastructure over conventional convection systems. This operational shift is positioning North America as a critical investment zone for intelligent heating ecosystem expansion and advanced energy-management integration.

Europe represents approximately 36% of the global infrared heat panels market, supported by aggressive decarbonization mandates, retrofit incentives, and high-efficiency building regulations. Germany, the United Kingdom, and France remain the dominant deployment hubs due to large-scale modernization of residential and commercial infrastructure. More than 44% of commercial energy-efficiency retrofit projects now prioritize electric radiant heating systems to reduce fossil-fuel dependency and improve carbon compliance. The region is experiencing rapid operational transformation through IoT-connected thermal management and AI-based energy optimization, improving heating efficiency by nearly 30% across smart-building deployments. Manufacturers are increasing localized production capacity and expanding premium ultra-thin product portfolios to comply with stricter energy-performance standards. European buyers increasingly favor long-lifecycle, compliance-driven heating solutions over low-cost alternatives. This environment is forcing continuous product innovation, making Europe a defining region for technology leadership and regulatory-driven competitive differentiation.

Asia-Pacific is emerging as the fastest-scaling infrared heat panels market, supported by rapid urbanization, manufacturing expansion, and rising smart-infrastructure deployment across China, Japan, South Korea, and India. The region contributes nearly 24% of global demand while accounting for over 45% of production capacity due to cost-efficient manufacturing ecosystems and strong electronics supply-chain integration. Localized production of advanced infrared panels increased by approximately 28% during 2025 as manufacturers expanded regional assembly operations to meet accelerating infrastructure demand. Smart residential adoption and modular commercial construction are driving rapid deployment of lightweight and AI-enabled heating systems. Enterprise buyers prioritize scalability, cost optimization, and fast installation cycles, forcing suppliers to accelerate automation and regional distribution capabilities. Asia-Pacific is becoming strategically critical for both global supply resilience and high-volume deployment, positioning the region as the industry’s primary scale and expansion engine.

South America accounts for nearly 7% of global infrared heat panel demand, led primarily by Brazil, Chile, and Argentina where commercial infrastructure upgrades and energy-efficiency initiatives are gradually increasing adoption. Rising electricity optimization needs across hospitality, retail, and industrial facilities are driving deployment of localized radiant heating systems capable of reducing operational heating waste by nearly 19%. However, infrastructure limitations and import dependency continue constraining market scalability, with installation costs remaining approximately 16% higher than conventional systems in several regional markets. Companies are responding through localized distribution partnerships and modular product offerings designed for lower installation complexity. Commercial buyers remain highly price-sensitive, prioritizing operational savings and long-term durability over premium smart features. Despite structural constraints, increasing commercial modernization and energy-efficiency awareness are positioning South America as a selective but strategically emerging expansion opportunity for globally diversified heating manufacturers.

The Middle East & Africa region contributes approximately 6% of global infrared heat panel demand, supported by expanding commercial construction, healthcare modernization, and industrial infrastructure development across the UAE, Saudi Arabia, and South Africa. Demand is increasingly concentrated in premium hospitality, logistics, and industrial projects requiring energy-optimized thermal systems for controlled indoor environments. Infrastructure modernization programs and smart-building investments are accelerating adoption of digitally controlled radiant heating technologies, with commercial deployment activity increasing by nearly 18% during 2025. Several regional construction projects integrated centralized smart thermal systems capable of improving heating efficiency by over 20%. Enterprise buyers prioritize durability, centralized control, and operational efficiency as large-scale infrastructure spending continues expanding. The region is emerging as a strategically important long-term opportunity where modernization, construction growth, and technology partnerships are reshaping heating-system procurement priorities.

Germany – 24% Market share: Strong building-efficiency regulations, large-scale retrofit activity, and advanced smart-building integration continue driving Germany’s dominance.

China – 19% Market share: Massive manufacturing capacity, rapid urban infrastructure expansion, and cost-efficient production ecosystems position China as a critical scale leader.

The infrared heat panels market is characterized by intense competition between European technology leaders, Asian cost-efficient manufacturers, and smart-heating innovators focused on intelligent energy optimization. Key players including Herschel Infrared, Frico, Königshaus, ThermoUp, Ecaros, and Sundirect compete across premium efficiency-focused systems, while regional manufacturers target price-sensitive commercial and residential retrofit segments. The top five players collectively control nearly 48% of global market share, with competition increasingly centered on thermal efficiency, installation flexibility, smart-control integration, and supply-chain responsiveness.

Advanced AI-enabled heating systems improve operational energy efficiency by approximately 30%, forcing traditional manufacturers to accelerate product innovation and IoT integration. Premium suppliers are investing heavily in graphene-based heating elements, modular installation systems, and localized assembly operations to shorten delivery cycles by nearly 20%. Meanwhile, cost-focused regional producers are competing aggressively through manufacturing scale and lower installation pricing.

The competitive landscape is shifting toward vertically integrated smart-heating ecosystems where software compatibility, predictive thermal analytics, and regulatory compliance are becoming decisive differentiators. Rising certification standards and electrical-infrastructure requirements are increasing entry barriers, making technology integration capability, supply resilience, and execution speed essential to compete effectively against established market leaders.

Frico AB

Königshaus GmbH

Sundirect Technology Ltd.

Ecaros GmbH

Infrared Heating Supplies Ltd.

Welltherm GmbH

Redwell Manufaktur GmbH

Heat4All

Veito

Tansun Ltd.

Infralia

Ecosun

Advanced carbon-crystal and graphene-based heating technologies are redefining performance standards across the infrared heat panels market. Compared with conventional metallic heating elements, graphene-enabled systems improve thermal conductivity by nearly 33% while reducing panel thickness by approximately 25%. These innovations are enabling faster heat response, lower operational energy consumption, and easier integration into smart-building infrastructure. More than 38% of newly deployed premium commercial infrared systems now incorporate advanced conductive materials to improve efficiency and lifecycle durability.

AI-enabled thermal optimization and IoT-integrated control systems are rapidly becoming core competitive differentiators. Intelligent occupancy-based zoning systems reduce unnecessary heating consumption by nearly 27% while improving real-time thermal precision across commercial and residential environments. Smart integration is particularly accelerating across logistics facilities, healthcare infrastructure, and energy-efficient residential projects where predictive energy management directly impacts operational expenditure.

Ultra-thin modular panel systems are also reshaping installation economics and deployment scalability. New-generation modular infrared systems reduce installation time by nearly 22% compared to legacy convection-based electric heating infrastructure. Manufacturers benefiting most are those capable of combining lightweight engineering, wireless connectivity, and advanced thermal analytics into scalable integrated solutions.

Between 2026 and 2028, software-driven heating ecosystems, self-learning thermal automation, and intelligent energy-balancing platforms will increasingly determine competitive positioning. Companies that invest early in AI-based optimization, regional manufacturing automation, and interoperable smart-building integration will secure stronger margins, faster deployment cycles, and higher enterprise retention rates in the evolving intelligent heating landscape.

August 2025 – Frico completed the full integration of Burda infrared patio heaters into its branded portfolio, strengthening its radiant heating ecosystem across Europe. The move expanded Frico’s infrared product coverage and streamlined international order management through Sweden-based operations. [Portfolio Integration] Source: www.frico.net

July 2025 – Infratech partnered with Bond to launch Wi-Fi-enabled Smart Wall Switch and Smart Wall Dimmer systems for outdoor infrared heaters. The integration enabled app-based and voice-controlled heating management, accelerating smart outdoor heating adoption across residential and commercial installations. [Smart Heating Control]

October 2025 – Mito Red Light introduced the MitoADAPT 4.0 multi-wavelength infrared panel with 11 operating modes and app-connected controls. The launch strengthened demand for intelligent infrared wellness systems while improving personalization and operational flexibility for advanced light-therapy applications. [Multi-Wavelength Expansion]

October 2025 – Toyotomi launched the POWER HEAT PH-R19 far-infrared heating system capable of heating spaces up to 64 tatami units with 4-way airflow distribution. The product expansion strengthened the company’s high-capacity commercial and residential infrared heating positioning in Japan. [High-Capacity Launch]

The Infrared Heat Panels Market Report delivers comprehensive coverage of the global industry across product types, applications, end-user industries, regional demand centers, and emerging intelligent heating technologies. The report evaluates ceiling-mounted, wall-mounted, portable, and hybrid infrared heating systems while analyzing deployment trends across commercial buildings, residential infrastructure, industrial facilities, healthcare environments, and hospitality sectors. It also covers critical enabling technologies including AI-enabled thermal optimization, graphene heating materials, IoT-integrated controls, and smart zoning systems shaping next-generation energy-efficient heating ecosystems.

The analysis spans five major regions and multiple country-level markets, providing detailed assessment of demand concentration, manufacturing dynamics, retrofit adoption patterns, and operational efficiency trends. More than 40% of analyzed commercial infrastructure projects now prioritize intelligent electric heating integration, while premium smart-heating adoption across urban residential environments exceeds 30% in several advanced economies. The report profiles key market participants, competitive positioning strategies, supply-chain developments, and execution-level innovation trends influencing industry transformation.

The study also delivers forward-looking strategic intelligence covering 2026–2033 deployment direction, infrastructure modernization priorities, regional manufacturing expansion, and evolving energy-management integration models. Decision-makers benefit from detailed insight into investment opportunities, competitive risks, technology positioning, and operational optimization pathways critical for long-term market expansion and strategic differentiation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 370 Million |

| Market Revenue (2033) | USD 603.2 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Herschel Infrared Ltd; Frico AB; ThermoUp; Königshaus GmbH; Sundirect Technology Ltd.; Ecaros GmbH; Infrared Heating Supplies Ltd.; Welltherm GmbH; Redwell Manufaktur GmbH; Heat4All; Veito; Tansun Ltd.; Infralia; Ecosun |

| Customization & Pricing | Available on Request (10% Customization Free) |