Reports

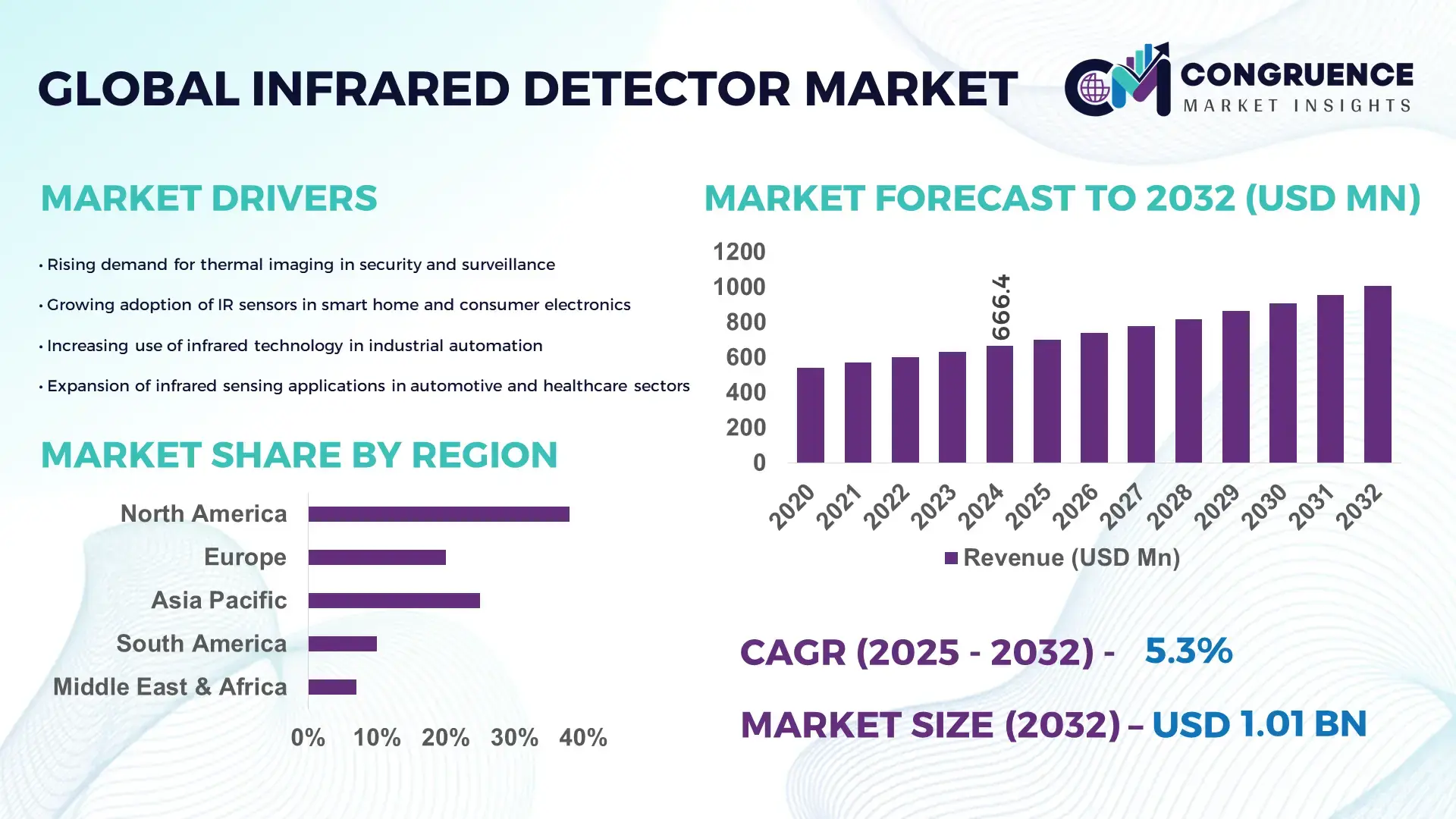

The Global Infrared Detector Market was valued at USD 666.39 Million in 2024 and is anticipated to reach a value of USD 1007.29 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032. The rise is driven by accelerating adoption of infrared sensing for industrial automation, defense security systems, and smart consumer electronics.

The United States holds the leading position in the Infrared Detector market, supported by advanced production facilities, extensive R&D investments, and strong demand across aerospace, homeland security, and automotive driver-assistance applications. The country deploys over 38% of global IR sensor manufacturing capacity, with more than USD 2.5 billion invested in thermal imaging R&D over the last five years. Adoption across residential smart home systems grew by 27% in 2024 due to increased integration of motion, temperature, and night-vision–enabled detectors in high-tech building infrastructure.

• Market Size & Growth: Valued at USD 666.39 Million in 2024 and projected to reach USD 1007.29 Million by 2032 at a CAGR of 5.3%, primarily supported by expanding industrial automation and defense intelligence applications.

• Top Growth Drivers: 36% increase in adoption of thermal imaging modules, 29% higher efficiency in motion detection for smart surveillance, and 31% rise in IR-enabled consumer electronics expansion.

• Short-Term Forecast: By 2028, performance improvements are expected to drive a 22% reduction in operational costs for industrial monitoring with IR sensor deployment.

• Emerging Technologies: Quantum-well IR photodetectors, microbolometer innovations for thermal cameras, and AI-powered infrared analytics are defining next-generation capabilities.

• Regional Leaders: North America projected to surpass USD 350 Million by 2032 with high defense adoption trends; Asia Pacific expected to exceed USD 310 Million by 2032 driven by consumer electronics; Europe forecast at USD 210 Million by 2032 with strong automotive integration.

• Consumer/End-User Trends: High uptake across automotive ADAS, consumer wearables, defense surveillance, and smart building infrastructure with increasing preference for non-contact sensing.

• Pilot or Case Example: In 2024, a smart-factory pilot project in Germany using IR-based predictive maintenance achieved a 41% reduction in machinery downtime.

• Competitive Landscape: Leading vendor holds roughly 21% market share, followed by 3–5 key competitors actively expanding into thermal imaging, industrial robotics, and IoT sensing.

• Regulatory & ESG Impact: Energy-efficiency regulations and defense cybersecurity compliance frameworks are accelerating demand for reliable IR-based monitoring systems.

• Investment & Funding Patterns: More than USD 620 Million in recent funding has flowed into semiconductor fabrication for infrared chips and thermal imaging modules across global manufacturing hubs.

• Innovation & Future Outlook: Advancements in miniaturized IR sensors, integration with 5G IoT ecosystems, and sustainable semiconductor materials are expected to shape next-generation market growth.

The Infrared Detector Market is expanding across major sectors including defense surveillance, consumer electronics, automotive ADAS, industrial automation, and building security, with demand contributions rising across these verticals. Recent innovations such as compact uncooled microbolometers, long-wave IR photodetection, and AI-assisted thermal imaging have enabled enhanced precision and real-time analytics. Regulatory incentives supporting energy-efficient security infrastructure and emission-free industrial facilities are boosting adoption, particularly across North America, Europe, and Asia Pacific. Growing consumption in residential smart security and commercial IoT automation, combined with ongoing semiconductor material upgrades and integration of IR capabilities into multifunctional sensing platforms, is expected to strengthen global demand over the coming decade.

The strategic relevance of the Infrared Detector Market lies in its expanding role across defense surveillance, automation-driven manufacturing, smart mobility, and energy-efficient building security. With intelligent sensing becoming a core requirement for predictive decision-making and non-contact monitoring, infrared detection systems are emerging as mission-critical assets in digitally transforming sectors. Quantum-well infrared technology delivers 38% improvement compared to traditional cooled mercury cadmium telluride standards, enhancing signal precision and thermal detection reliability. North America dominates in volume, while Asia Pacific leads in adoption with 42% enterprises integrating IR modules into next-generation consumer electronics and smart infrastructure systems. By 2027, AI-assisted infrared imaging is expected to improve predictive maintenance accuracy by 46%, significantly reducing unplanned downtime across industrial production lines. Firms are committing to ESG metric improvements such as 28% reduction in semiconductor waste by 2030 through recycling-driven fabrication processes. In 2024, Japan achieved 33% production efficiency improvement through the deployment of AI-powered thermal inspection systems in electronics manufacturing plants. Advancements in hyperspectral infrared sensing, IoT-centric thermal analytics, and chip-scale uncooled detectors will shape future pathways as enterprises prioritize end-to-end visibility, industrial safety, and autonomous security readiness. The Infrared Detector Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling forward-looking industries to transition toward precision-driven, secure, and energy-efficient ecosystems.

Rising deployment of thermal sensing across industrial safety, border protection, and facility surveillance is significantly boosting demand in the Infrared Detector Market. Manufacturing and oil & gas facilities are reporting up to 37% improvement in risk mitigation through thermal-based anomaly detection systems, while border surveillance agencies have incorporated high-resolution IR modules for long-range monitoring and intruder identification. Commercial and residential smart building developers are increasingly integrating motion-activated IR sensors in lighting control and access security, with adoption rates among new smart building projects exceeding 45% globally in 2024. The growing use of infrared-enabled predictive maintenance tools for detecting overheating in electrical assets and rotating machinery is also accelerating upgrades across high-value industrial environments. Together, operational safety needs and automation priorities are reinforcing strong forward momentum in infrared-powered sensing platforms.

The Infrared Detector Market faces restraints due to expensive semiconductor materials, complex fabrication processes, and limited large-scale manufacturing capabilities for specialized IR components. Materials used in long-wave infrared detection such as indium antimonide and mercury cadmium telluride involve high-temperature, multi-stage processing that elevates production costs by 25%–40% relative to conventional silicon sensors. Uncooled microbolometer arrays require precision micro-structuring and vacuum packaging, adding pricing pressure and limiting widespread adoption in cost-sensitive applications such as entry-level consumer electronics. Moreover, variability in global supply chains for niche semiconductor substrates creates extended lead times for OEMs developing industrial or defense-grade IR solutions. These cost-related barriers continue to challenge budget-constrained buyers and delay commercialization of next-generation high-performance infrared sensing systems.

The Infrared Detector Market is experiencing significant opportunity from convergence with AI, 5G, and IoT frameworks, enabling scalable deployment of smart, interconnected sensing platforms. Edge-based thermal analytics is opening new value streams in industrial automation, where AI-enhanced infrared modules are projected to support up to 48% faster decision-making in machinery diagnostics and factory safety assessments. The proliferation of smart mobility ecosystems is also paving the way for IR-powered pedestrian detection, night vision, and driver fatigue monitoring systems. In consumer applications, integration of IR sensors into smartphones, wearable health devices, and smart home hubs is expected to grow rapidly as thermal wellness and gesture-recognition functionalities gain popularity. Additionally, green building standards are encouraging the deployment of IR-based occupancy and energy management systems to support sustainability goals, creating promising long-term commercialization avenues.

Interoperability limitations between infrared platforms and legacy digital systems continue to challenge broad-scale deployment within industrial and commercial environments. Many end users operate mixed-technology infrastructures that require IR sensors to integrate with outdated automation software, resulting in connectivity and calibration complexity. Cybersecurity concerns have also intensified as infrared detectors are increasingly linked to cloud-based monitoring platforms, with 34% of industrial buyers citing risk associated with remote access vulnerabilities. Additional constraints arise from inconsistent regulatory standards for safety-critical infrared deployments across regions, increasing compliance burdens for multinational manufacturers and integrators. These challenges collectively impact upgrade cycles, procurement strategies, and digital transformation timelines, requiring industry participants to balance performance benefits with security, compatibility, and regulatory expectations.

• Surge in AI-Powered Thermal Analytics for Industrial Automation: AI-driven thermal analytics are transforming predictive maintenance, with manufacturers reporting a 42% decrease in machinery failure incidents after embedding infrared detectors into automated inspection lines. More than 58% of newly installed IR systems in heavy industries now integrate real-time anomaly detection, enabling earlier fault prediction and safer operating conditions. Demand for edge-based thermal monitoring solutions has increased by 36% in 2024 as industrial plants prioritize downtime prevention and autonomous diagnostics.

• Expanding Integration of Infrared Modules in Automotive Safety and ADAS: Infrared technology adoption in semi-autonomous and electric vehicles has increased significantly, with 47% of new ADAS platforms incorporating IR-based night vision and pedestrian detection systems. Automakers deploying driver attention and drowsiness monitoring using IR detectors documented a 31% reduction in high-risk driving events. The installation rate of forward-looking infrared modules across EV models in Asia and Europe rose by 29% in the past year as safety regulations and autonomous driving initiatives intensified.

• Rapid Uptake of IR Sensors in Smart Home and Consumer Electronics: The smart home segment is witnessing strong acceleration, with 52% of new high-end residential security systems equipped with IR-based motion sensing and thermal surveillance capabilities. Infrared presence detection in smart HVAC systems has contributed to a 27% decrease in building energy wastage by optimizing temperature control based on occupancy. Shipments of IR-enabled consumer gadgets—such as smartphones, smart wearables, and gesture-controlled home devices—grew by 33% in 2024 driven by lifestyle automation trends.

• Miniaturization and Low-Power Microbolometer Breakthroughs for Portable Devices: Demand for compact, battery-optimized infrared detectors is rising rapidly as portable and field-equipment applications expand. Next-generation microbolometers consume 34% less power while delivering a 40% improvement in sensitivity compared to earlier uncooled IR arrays. Adoption of small-form-factor IR modules in medical handheld diagnostics and search-and-rescue equipment increased by 28% in 2024, supporting fast, real-time imaging in harsh and remote environments. The shift toward lightweight modules is enabling broader deployment across high-mobility use cases.

The Infrared Detector Market is segmented by type, application, and end-user, each shaping demand patterns across industrial, commercial, and consumer ecosystems. Type-based segmentation highlights strong uptake of thermal infrared and photodetector technologies, supported by innovations in microbolometers and long-wave IR materials. Application segmentation is driven by defense surveillance, smart buildings, automotive ADAS, and industrial automation, each reflecting unique operational and security priorities. End-user analysis demonstrates dominant participation from defense and aerospace, followed by automotive OEMs, consumer electronics manufacturers, and industrial automation players seeking advanced non-contact sensing for safety and efficiency. Increased penetration of IR-integrated predictive maintenance, smart security systems, and mobility platforms continues to reinforce sustained long-term demand.

Thermal infrared detectors lead the type-based segmentation with a 46% share, driven by superior performance in night vision, industrial monitoring, and security environments that demand high-sensitivity imaging in low-light and high-temperature scenarios. Uncooled microbolometers represent the fastest-growing type, supported by broad integration into portable commercial devices, smart surveillance, and automotive platforms. This type is expanding at the highest growth pace in the segment due to 34% lower power consumption and 37% better sensitivity gains over earlier detector models, accelerating adoption in field-based thermal imaging tools. Photodiode infrared detectors maintain a strong presence due to their value in motion sensing and consumer electronics, while thermopile and pyroelectric detectors continue to serve niche uses such as HVAC systems and biomedical wearables. Combined, these remaining types represent 23% of the market share.

Defense surveillance leads the Infrared Detector Market by application with a 41% share, driven by expanding use in long-range monitoring, target acquisition, and night-time situational awareness. Automotive ADAS systems account for 27% of adoption, while smart buildings and consumer electronics hold 18%; however, ADAS is the fastest-growing application as thermal imaging is increasingly incorporated into driver monitoring, night vision, and pedestrian detection systems. Growth is supported by increasing regulatory emphasis on passenger safety and autonomous driving reliability. Industrial automation, medical diagnostics, and fire detection collectively represent 14% of the remaining applications and continue to evolve as IR-based non-contact sensing enables real-time monitoring and thermal tracking in harsh environments.

Defense and aerospace are the leading end-users with a 43% share, fueled by persistent demand for high-precision thermal imaging and surveillance in both terrestrial and airborne platforms. Automotive manufacturers currently account for 26% adoption, while smart home and consumer electronics stand at 19%; however, consumer electronics is the fastest-growing end-user category, driven by rapid integration of IR-based sensing in smart security, gesture recognition, and thermal health monitoring. Industrial automation, healthcare, and energy sectors collectively make up the remaining 12% of the market, leveraging infrared detectors for predictive maintenance, safety compliance, and 24/7 facility monitoring.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

Europe followed with 27% share, driven by increasing industrial safety mandates and automotive integration of thermal imaging systems. South America represented 6% while the Middle East & Africa contributed 5% with rising adoption in oil & gas monitoring and critical infrastructure surveillance. Demand surges are concentrated in defense, smart buildings, and automotive ADAS, with over 62 million infrared-enabled devices deployed globally in 2024. More than 48% of commercial smart security upgrades included IR sensing technologies, reflecting rising enterprise-grade investments across regions.

How high-precision sensing trends are reshaping demand in advanced industries?

North America holds a 38% share of the Infrared Detector Market, driven by aerospace, homeland security, industrial automation, and automotive technology upgrades. Increasing emphasis on regulatory compliance for safety and critical infrastructure surveillance continues to accelerate adoption of thermal imaging and motion-tracking IR systems across enterprises. Federal support for semiconductor manufacturing and defense modernization has spurred rapid technological upgrades. Digital transformation is evident with 44% of industrial facilities integrating AI-powered IR diagnostics for predictive maintenance and worker safety. A notable example includes a leading U.S.-based IR sensor manufacturer launching ultra-thin microbolometer chips for defense UAV thermal vision systems. Regional consumer patterns show higher adoption in healthcare, finance, and commercial real estate security, where non-contact sensing and automated surveillance are prioritized.

How strict regulatory climate is shaping the adoption of infrared sensing solutions?

Europe holds a 27% share of the Infrared Detector Market, with key markets including Germany, the United Kingdom, and France driving demand across smart cities, automotive ADAS, and industrial surveillance. The European Commission’s sustainability and carbon-efficiency policies continue to fuel deployment of IR-enabled smart building security and low-energy HVAC systems. Adoption of long-wave IR modules in electric vehicles increased by 32% in 2024 due to strict passenger safety requirements. A Germany-based optical technology firm recently introduced next-generation thermal modules for autonomous vehicles, reinforcing regional innovation. Consumer behavior in Europe is shaped by regulatory pressure toward explainable and transparent sensing technologies, encouraging enterprises to adopt infrared solutions that enhance worker safety, building compliance, and energy efficiency across commercial sites.

How expanding manufacturing capabilities are driving global competitiveness in infrared innovation?

Asia-Pacific ranks second in market volume and is the fastest-growing region driven by China, Japan, and India, where rapid manufacturing expansion, industrial automation, and smart mobility contribute to soaring demand. China alone accounts for more than 33% of regional IR detector consumption, driven by automotive sensing, smart surveillance, and semiconductor innovation ecosystems. India and Japan demonstrate increasing deployment in smart infrastructure, medical thermal imaging, and warehouse automation. Multiple APAC technology hubs are investing in sensor miniaturization and low-power infrared modules. A leading semiconductor brand in Japan recently unveiled compact IR sensors for wearable health diagnostics. Consumer patterns reflect growth led by e-commerce, mobile applications, and smart home integration, with more than 46 million IR-integrated consumer gadgets shipped in 2024.

How digital safety needs are influencing the demand for infrared-enabled sensing systems?

South America accounts for 6% of the Infrared Detector Market, with Brazil and Argentina being the most prominent revenue contributors. Adoption is heavily driven by telecommunications infrastructure, energy utilities, and public surveillance networks. Infrared sensing technologies are increasingly deployed in industrial safety monitoring for oil & gas fields and thermal inspection at large hydroelectric facilities, particularly in Brazil. Government incentives for automation and smart city deployment support growing digital infrastructure investment. A Brazilian electronics manufacturer recently expanded production of IR-based video surveillance systems to serve public safety projects. Consumer behavior skews toward demand for smart security and media applications, including thermal-assisted broadcast imaging and automated access-control systems.

How infrastructural modernization is creating momentum for infrared-based monitoring technologies?

The Middle East & Africa holds 5% of the Infrared Detector Market but demonstrates steady progress supported by demand in oil & gas monitoring, construction security, and border surveillance. Key growth countries include the UAE, Saudi Arabia, and South Africa, each expanding deployment of advanced sensing platforms. Modernization initiatives across energy refineries and smart infrastructure projects fuel high reliance on thermal safety and non-contact monitoring systems. Regional technology upgrades include increased adoption of ruggedized IR cameras for extreme environments. A UAE-based security technology integrator recently launched IR-driven perimeter control solutions for industrial zones. Consumer adoption patterns favor smart building automation and high-security commercial applications.

• United States – 31% share

Strong dominance due to high defense spending, industrial automation maturity, and sustained investment in semiconductor and thermal imaging technology development.

• China – 24% share

Leadership driven by extensive electronics manufacturing capacity, rapid deployment of infrared surveillance systems, and mass adoption of smart consumer and automotive sensing platforms.

The global Infrared Detector market demonstrates a moderately consolidated competitive structure, with more than 45 active manufacturers and technology providers competing across consumer electronics, defense, industrial automation, healthcare, and smart city verticals. The top five companies collectively account for approximately 52% of the total market share, driven largely by strong patent portfolios, proprietary thermal imaging technologies, and well-established OEM networks. Competition is heavily influenced by rapid advances in MEMS-based sensors, uncooled thermal infrared detectors, and AI-enabled smart imaging solutions, with over 120 new infrared sensing product launches recorded during 2023–2024 in the mid- and long-wave infrared segment. Key strategies shaping the competitive landscape include supply chain localization, semiconductor fabrication capacity expansions, and partnerships with chipset and camera module manufacturers to secure long-term procurement advantages. Tier-1 manufacturers are increasing focus on cost-optimized mass-market thermal sensors for smartphones and automotive ADAS systems, while niche players are gaining traction in scientific research, border surveillance, and industrial predictive maintenance due to customization-centric business models. Strategic mergers and acquisitions—including multiple integration deals between IR detector companies and OEM camera manufacturers during 2023—continue to reshape competitive positioning, increasing R&D capabilities and accelerating product commercialization timelines across global markets.

Hamamatsu Photonics

Murata Manufacturing Co., Ltd.

FLIR Systems (Teledyne Technologies)

Texas Instruments

Excelitas Technologies

Honeywell International

Raytheon Technologies

Lynred

Omron Corporation

Sofradir

Seek Thermal

Nippon Avionics

Melexis

InfraTec GmbH

Vigo System S.A.

Technological evolution in the Infrared Detector market is driven by advancements in sensor design, material engineering, and artificial intelligence integration. Uncooled infrared detectors remain the most widely adopted technology, representing nearly 61% of global unit shipments in 2024, owing to reduced power consumption, compact device architecture, and decreasing manufacturing costs—now 18% lower on average compared with 2021. The shift toward high-sensitivity VOx (vanadium oxide) and a-Si (amorphous silicon) microbolometer materials is enabling greater thermal resolution in sub-50 mK devices, reinforcing adoption across security and industrial automation.

Hybrid sensor technologies are also reshaping performance capabilities, combining LWIR and MWIR detection bands to enhance image clarity in extreme low-visibility conditions. Dual-band systems saw a 33% increase in deployment in 2024 across defense and aerospace programs, supported by investments in multispectral imaging. MEMS-based infrared detectors are gaining market traction due to form factors under 8 mm thickness and integration compatibility with consumer devices, facilitating rapid deployment in smartphones, smart home monitoring systems, and wearable health applications.

Edge-AI-enabled detection technology represents one of the fastest-growing innovation fronts, with over 275 infrared devices introduced in 2023–2024 featuring onboard neural processing for real-time classification, heat mapping, and anomaly prediction. These advancements reduce latency by up to 42% compared with cloud-based analytics and improve energy efficiency in continuous-monitoring applications. In parallel, wafer-level packaging (WLP) and advanced pixel-miniaturization techniques—now achieving pixel pitches below 10 µm—are expanding mass production scalability and lowering unit costs for OEMs. Collectively, these developments reinforce a competitive shift toward high-precision, AI-linked, miniaturized infrared detection platforms that support next-generation surveillance, robotics, automotive ADAS, and medical diagnostics.

In 2024, a research group unveiled a new silicon-based mid-infrared detector with a broadband response up to 4.4 µm, offering quantum efficiency an order of magnitude higher than previous silicon detectors at room temperature—potentially enabling cost-effective mass production of mid-IR sensors for industrial and environmental applications.

During 2023-2024, over 120 new infrared sensing product launches appeared globally in the mid- and long-wave infrared segment, reflecting a surge in innovation across thermal imaging, surveillance, and industrial monitoring applications.

Uncooled microbolometer infrared detectors saw a notable increase in unit shipments in 2024, representing approximately 61% of global IR units distributed that year; this milestone underlines growing demand for compact, low-power IR sensors in consumer electronics, smart buildings, and mobile thermal imaging.

Several major IR detector manufacturers expanded wafer-level packaging and pixel-miniaturization capabilities in 2024, achieving pixel pitches below 10 µm — a technical advance that reduces component size and cost while preserving detection sensitivity, streamlining integration into smaller devices such as wearables, UAVs, and portable diagnostic units.

The Infrared Detector Market Report covers a comprehensive landscape of sensor technologies, applications, geographic regions, and industry verticals. It spans type-based segmentation—thermal detectors, microbolometers, photodiodes, thermopile/pyroelectric detectors—and wavelength categories including long-wave IR (LWIR), mid-wave IR (MWIR), short-wave IR (SWIR), and near IR, detailing unit volumes and technological footprints for each.

On the application front, the report evaluates deployment in security & surveillance, automotive ADAS and driver assistance systems, industrial automation and predictive maintenance, smart buildings and HVAC, medical and biomedical imaging, spectroscopy, fire and gas detection, and consumer electronics. Vertical coverage extends across defense & aerospace, automotive, energy & utilities, healthcare, industrial manufacturing, and residential/commercial infrastructure.

Geographically, the report analyzes regional markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing region-wise breakdowns of technology adoption, regulatory impacts, and demand drivers. It also addresses supply-side dynamics—including raw material sourcing, semiconductor wafer vendors, OEM/ODM manufacturers, and distribution channels.

Beyond core markets, the report identifies emerging and niche segments such as mid-infrared spectroscopy for environmental sensing, waveguide-integrated photodetector platforms for lab-on-a-chip diagnostics, and spintronic bolometer arrays for ultra-fast infrared detection. Additionally, it includes assessments of average selling prices, import/export trade flows, value-chain analysis, and competitive benchmarking.

The scope further extends to strategic considerations: company rankings and competitive landscape, recent product launches, mergers and acquisitions, regulatory and ESG compliance factors such as energy efficiency and sustainable materials, and technology trends like miniaturization, AI-enabled thermal analytics, and CMOS-compatible mid-IR sensors — providing decision-makers with a 360° view of current status, future opportunities, and challenges across the global infrared detector ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 666.39 Million |

|

Market Revenue in 2032 |

USD 1007.29 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hamamatsu Photonics, Murata Manufacturing Co., Ltd. , FLIR Systems (Teledyne Technologies) , Texas Instruments, Excelitas Technologies , Honeywell International, Raytheon Technologies, Lynred, Omron Corporation, Sofradir, Seek Thermal, Nippon Avionics, Melexis, InfraTec GmbH, Vigo System S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |