Reports

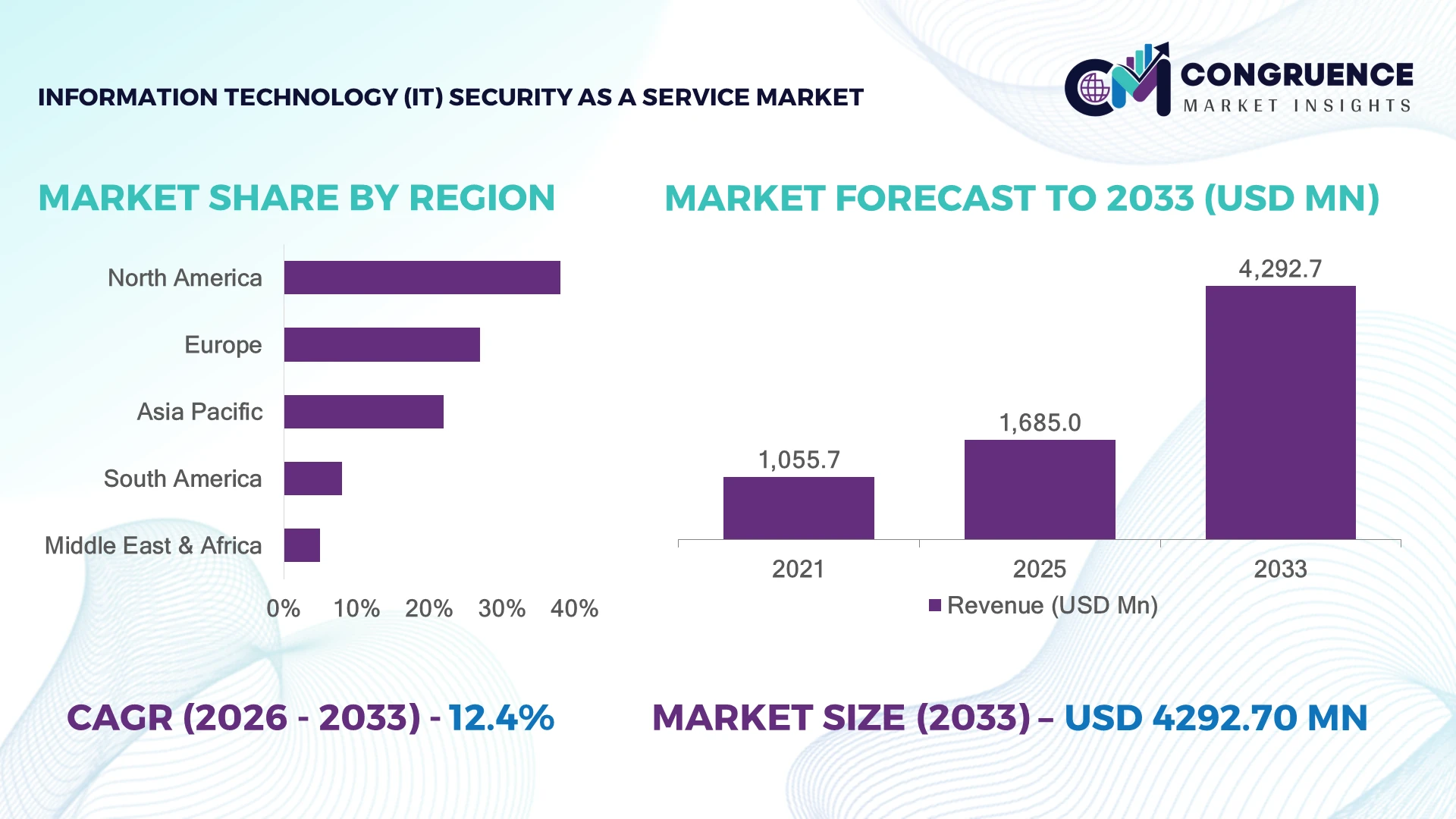

The Global Information Technology (IT) Security as a Service Market was valued at USD 1,685.0 Million in 2025 and is anticipated to reach a value of USD 4,292.7 Million by 2033 expanding at a CAGR of 12.4% between 2026 and 2033. Growth is driven by rising adoption of cloud-native security platforms, AI-based threat detection, zero-trust architectures, and managed cybersecurity services replacing fragmented in-house security operations.

The United States dominated the market with approximately 38% share in 2025, supported by high cybersecurity spending, federal initiatives following the U.S. Cybersecurity Executive Order, and widespread adoption across BFSI, healthcare, and technology sectors. More than 70% of large U.S. enterprises integrate managed security solutions, while Germany and Japan show stronger industrial security adoption through smart manufacturing and critical infrastructure protection.

Strategic investments in scalable security platforms will determine competitive advantage as organizations prioritize resilient digital ecosystems.

Market Size & Growth: Valued at USD 1.68 billion in 2025 and forecast to reach USD 4.29 billion by 2033 at a 12.4% CAGR, driven by AI-powered cybersecurity automation and cloud migration.

Top Growth Drivers: Cloud security adoption (35%), ransomware protection demand (28%), and zero-trust implementation (25%) represent the strongest market accelerators.

Short-Term Forecast: By 2028, enterprises using managed security services are expected to reduce incident response costs by 30% and improve threat detection efficiency by 45%.

Emerging Technologies: AI threat analytics, automated security orchestration, extended detection and response (XDR), and identity-based security frameworks are reshaping deployments.

Regional Leaders: North America is projected to exceed USD 1.6 billion, Europe USD 1.1 billion, and Asia Pacific USD 1.0 billion by 2033, supported by cloud-first security adoption.

Consumer/End-User Trends: Over 65% of enterprises prioritize outsourced cybersecurity services due to skill shortages and increasing compliance requirements.

Pilot/Case Example: In 2024, financial institutions deploying AI-driven managed security platforms achieved approximately 40% faster threat investigation cycles.

Competitive Landscape: Major providers include Microsoft, IBM, Cisco, Palo Alto Networks, and CrowdStrike, with leading vendors collectively controlling over 45% of enterprise security service deployments.

Regulatory & ESG Impact: Global cybersecurity regulations are increasing compliance investments, with over 60% of enterprises upgrading security frameworks to meet data protection standards.

Investment & Funding: More than USD 20 billion has flowed into cybersecurity technology investments, emphasizing AI security, cloud protection, and strategic partnerships.

Innovation & Future Outlook: Next-generation security services are shifting toward autonomous defense platforms, predictive analytics, and integrated digital risk management ecosystems.

The Information Technology (IT) Security as a Service Market is witnessing increased adoption across banking, healthcare, government, and manufacturing sectors as organizations modernize security operations. Recent innovations include AI-driven managed detection platforms, automated compliance monitoring, and cloud-based security analytics, with approximately 60% of enterprises prioritizing security automation initiatives. Growing regulatory pressure after global cyber incidents and increasing third-party risk management requirements are accelerating partnerships between technology providers and enterprises, creating new opportunities for scalable cybersecurity models.

The Information Technology (IT) Security as a Service Market is becoming strategically important as organizations shift cybersecurity from a reactive function into a continuous business protection framework. Increasing cyberattacks, complex supply chains, and stricter data protection regulations are pushing enterprises toward outsourced security models that provide faster response capabilities and specialized expertise.

The transition from traditional security infrastructure to AI-enabled managed platforms is improving operational efficiency. Modern security-as-a-service solutions can reduce threat investigation time by nearly 40% compared with manual monitoring systems while lowering infrastructure maintenance requirements. North America maintains leadership through mature cloud adoption and enterprise cybersecurity spending, whereas Asia Pacific is expanding rapidly due to digital transformation programs, industrial automation, and increasing regulatory focus on data protection.

Over the next 2–3 years, enterprises will prioritize integrated platforms combining threat intelligence, identity protection, and automated response capabilities. Financial institutions, healthcare providers, and government agencies are increasingly forming technology partnerships to strengthen cyber resilience. Organizations investing in adaptive security ecosystems will gain stronger operational continuity, reduced risk exposure, and a more competitive position in an increasingly digital economy.

The rapid migration toward cloud infrastructure is driving adoption of Information Technology (IT) Security as a Service solutions as enterprises seek scalable threat management capabilities. Over 70% of large organizations globally are increasing cybersecurity automation investments, while AI-enabled security tools improve incident detection speed by nearly 45%. The expansion of zero-trust frameworks following cybersecurity mandates in countries such as the United States is reshaping enterprise security strategies. Companies including Microsoft, IBM, and Cisco are expanding managed security portfolios through AI integration and strategic partnerships. The key operational shift is the transition from fragmented security teams toward continuous, outsourced protection models.

Complex integration with legacy IT environments remains a significant barrier for enterprises adopting security-as-a-service platforms. Nearly 40% of organizations report interoperability challenges between existing security systems and cloud-based solutions, while around 35% cite data migration and compliance requirements as deployment obstacles. In Germany and Japan, highly regulated industries face additional challenges due to strict data governance frameworks and localized infrastructure requirements. Companies are addressing these limitations through hybrid deployment models, customized service agreements, and investments in API-driven security platforms. The primary business impact is slower implementation cycles, increasing operational costs, and reduced scalability across multi-cloud environments.

Advancements in artificial intelligence, machine learning, and autonomous threat response are creating new opportunities for security-as-a-service providers. AI-based cybersecurity platforms are improving threat analysis efficiency by over 50%, while more than 65% of enterprises are prioritizing automated security operations to address workforce shortages. Countries such as India and Singapore are emerging as innovation hubs through digital infrastructure expansion and cybersecurity ecosystem development. Companies are increasing R&D investments, forming technology alliances, and launching managed detection and response solutions. A strategic opportunity lies in delivering predictive security services for small and medium enterprises that lack specialized cybersecurity teams.

The shortage of skilled cybersecurity professionals and increasing multi-cloud complexity continue to challenge long-term market expansion. Industry assessments indicate that over 50% of enterprises experience cybersecurity talent shortages, while approximately 60% operate across multiple cloud environments requiring advanced security coordination. Rapid adoption of connected technologies in sectors such as healthcare and manufacturing increases exposure to sophisticated cyber threats. Companies must strengthen automation capabilities, expand cybersecurity training programs, and develop integrated security ecosystems to maintain service reliability. The major operational challenge is achieving consistent protection across diverse digital environments while managing evolving compliance requirements and increasing threat sophistication.

AI Security Automation Growth Enterprises are rapidly integrating AI-driven threat detection, with over 60% of large organizations adopting automated security analytics and nearly 45% reporting faster incident response workflows. The shift is changing security operations from manual monitoring toward predictive defense models. U.S. financial institutions and technology companies are scaling AI-powered managed security platforms, while vendors are expanding automation partnerships to address cybersecurity workforce shortages. A key operational shift is the use of autonomous response systems to reduce analyst workload and improve continuous protection.

Zero-Trust Deployment Expansion Zero-trust security frameworks are becoming standard enterprise architecture, with more than 65% of global organizations prioritizing identity-based access controls and approximately 50% increasing investment in authentication technologies. Regulatory pressure from cybersecurity frameworks in the United States and Europe is accelerating adoption. Companies are restructuring security workflows around continuous verification, micro-segmentation, and privileged access management. This transition improves compliance readiness and reduces exposure from increasingly distributed hybrid work environments.

Managed Detection Evolution Managed detection and response services are gaining traction as enterprises address cybersecurity skill shortages, with nearly 55% of organizations outsourcing at least part of their security operations. Companies in healthcare and manufacturing are expanding partnerships with specialized providers to maintain 24/7 monitoring capabilities. The non-obvious market shift is the movement toward outcome-based security contracts, where enterprises prioritize measurable threat reduction rather than standalone technology purchases.

Cloud Security Consolidation Enterprises are consolidating fragmented security tools as multi-cloud adoption increases, with around 70% of organizations operating multiple cloud environments and over 40% seeking integrated security platforms. Supply-chain disruptions and increasing third-party cyber risks are accelerating platform consolidation. Technology providers are responding by developing unified cloud security ecosystems that improve operational visibility, reduce management complexity, and support faster enterprise expansion.

Cloud-based security services represent the leading type segment due to scalability, flexible deployment models, and integration capabilities across distributed enterprise environments. Organizations increasingly prefer cloud security platforms because they eliminate extensive infrastructure investment and enable centralized threat monitoring. More than 70% of large enterprises are adopting cloud-based security solutions, while approximately 55% prioritize integrated security management across multiple cloud environments. Traditional managed security models continue supporting industries with strict compliance requirements, but their growth is constrained by infrastructure dependency and slower customization cycles. AI-powered security services are emerging as the fastest-growing type as enterprises seek automated threat intelligence, predictive analytics, and faster response capabilities. Around 60% of organizations are increasing automation adoption within cybersecurity workflows, encouraging providers to expand AI-driven offerings and strategic collaborations. Companies are shifting investments toward intelligent security platforms that combine cloud flexibility with automated decision-making capabilities.

Threat management represents the leading application segment as enterprises prioritize continuous monitoring, vulnerability detection, and rapid incident response. Rising cyberattack frequency across banking, healthcare, and government sectors is increasing demand for managed threat intelligence solutions. Nearly 65% of enterprises consider real-time threat detection a critical cybersecurity capability, while more than 50% are expanding investments in automated monitoring tools. Compliance management, data protection, and identity security applications remain important as organizations strengthen regulatory readiness and protect sensitive information. Identity and access management applications are experiencing the fastest adoption growth due to increasing hybrid work environments and zero-trust implementation. Approximately 60% of enterprises are upgrading identity security frameworks, particularly in countries such as the United States and Singapore where digital infrastructure modernization is accelerating. Companies are expanding partnerships with identity security providers and integrating automated authentication solutions to improve workforce access control and reduce unauthorized access risks.

Large enterprises represent the leading end-user segment due to extensive digital infrastructure, higher cybersecurity requirements, and greater exposure to complex threats. Banking, healthcare, manufacturing, and technology companies are major adopters because they require continuous monitoring across interconnected systems. More than 75% of large organizations maintain dedicated cybersecurity improvement programs, while over 60% are increasing reliance on external security specialists to address internal skill gaps. Small and medium enterprises are adopting security-as-a-service solutions gradually due to affordability and simplified management benefits. Small and medium enterprises represent the fastest-growing end-user group as subscription-based security models reduce entry barriers and provide access to advanced cybersecurity capabilities. Approximately 50% of smaller businesses are increasing cybersecurity investments due to rising ransomware concerns and regulatory expectations. Providers are responding with scalable packages, customized pricing models, and industry-specific solutions to expand adoption among underserved businesses.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

North America maintains market leadership due to advanced cloud adoption, strong cybersecurity investment, and widespread enterprise deployment of managed security platforms. The region contributes approximately 38% of global adoption, supported by large-scale implementation across banking, healthcare, government, and technology sectors. More than 70% of large enterprises in the United States utilize cloud-based security frameworks, while federal cybersecurity initiatives are accelerating zero-trust deployment. Major technology providers are expanding managed security capabilities through AI integration, strategic alliances, and automated threat response platforms. The region’s mature digital ecosystem enables faster adoption of advanced security services, creating stronger operational resilience for enterprises managing complex cyber risks.

United States Market Outlook: The United States represents the primary growth engine within North America due to high cybersecurity spending, advanced cloud infrastructure, and strong enterprise demand. More than 75% of large U.S. organizations operate hybrid or multi-cloud environments requiring integrated security management. Financial services, healthcare, and government agencies are increasing partnerships with cybersecurity providers to strengthen compliance, threat intelligence, and continuous monitoring capabilities.

Europe is experiencing strong adoption of security-as-a-service platforms as enterprises respond to stricter data protection regulations and increasing cyber resilience requirements. The region accounts for approximately 27% of global market activity, supported by digital transformation across manufacturing, financial services, and public infrastructure sectors. The implementation of cybersecurity regulations such as NIS2 is accelerating enterprise investment in managed security solutions. Over 60% of European organizations are prioritizing automated security monitoring and compliance management capabilities. Companies are expanding partnerships with local cybersecurity providers and strengthening cloud security ecosystems to support operational continuity. Germany, the United Kingdom, and France remain key deployment centers due to industrial digitization and critical infrastructure protection initiatives.

Germany Market Outlook: Germany leads European adoption through its advanced industrial base, manufacturing automation, and strong cybersecurity requirements. More than 65% of large industrial enterprises are increasing investment in digital security solutions to protect connected production environments. The country’s Industry 4.0 ecosystem is encouraging demand for integrated security platforms supporting smart factories, supply-chain protection, and operational technology networks.

Asia-Pacific represents the fastest-growing market due to rapid digital transformation, expanding cloud infrastructure, and increasing cybersecurity awareness among enterprises. The region contributes nearly 22% of global adoption, with significant deployment activity across China, India, Japan, and Singapore. More than 60% of enterprises in major Asian economies are accelerating cybersecurity modernization programs as digital services expand. Government-led cybersecurity initiatives and increasing investment in data centers are strengthening regional infrastructure capabilities. Technology companies are scaling managed security offerings through partnerships, localized solutions, and AI-powered platforms. The region’s large enterprise base and growing online economy create strong demand for flexible security services.

China Market Outlook: China remains a strategically important market due to extensive digital infrastructure, industrial automation, and large-scale enterprise technology adoption. Over 70% of large Chinese organizations are investing in advanced cybersecurity frameworks to support cloud migration and connected industrial systems. Domestic technology providers are expanding security ecosystems through AI analytics, cloud protection services, and enterprise-focused cybersecurity platforms.

South America is gradually expanding adoption of security-as-a-service solutions as organizations modernize digital operations and address rising cyber threats. The region contributes approximately 8% of global market activity, with Brazil, Argentina, and Chile representing major deployment centers. Financial services, telecommunications, and government sectors are leading adoption due to increasing requirements for data protection and operational security. Around 45% of enterprises in key markets are strengthening cybersecurity investments through cloud-based solutions. However, infrastructure limitations and cybersecurity skill shortages continue affecting deployment speed. Companies are responding through managed service partnerships, localized support models, and scalable subscription-based security offerings.

Brazil Market Outlook: Brazil dominates regional adoption due to its large digital economy, expanding financial technology sector, and growing cybersecurity requirements. More than 50% of Brazilian enterprises are increasing spending on cloud security and threat monitoring solutions. Regulatory developments around data protection are encouraging organizations to adopt managed security services for compliance improvement and operational risk reduction.

The Middle East & Africa market is expanding through government digital transformation programs, smart infrastructure investments, and increasing enterprise cybersecurity requirements. The region represents nearly 5% of global adoption, with the United Arab Emirates, Saudi Arabia, and South Africa driving deployment activity. More than 50% of organizations in major markets are prioritizing cybersecurity modernization as cloud adoption and digital public services increase. Large-scale smart city initiatives and critical infrastructure protection programs are accelerating demand for managed security platforms. Companies are forming technology partnerships and expanding regional security operations centers to support enterprise resilience and compliance requirements.

United Arab Emirates Market Outlook: The United Arab Emirates is a leading regional adopter due to advanced digital infrastructure, government cybersecurity initiatives, and strong investment in smart technologies. Over 60% of large organizations are implementing advanced security monitoring capabilities to protect cloud environments and digital services. The country’s focus on artificial intelligence and smart city development continues to create demand for integrated cybersecurity solutions.

The Information Technology (IT) Security as a Service Market features intense competition between global cybersecurity leaders including Microsoft, IBM, Cisco, Palo Alto Networks, CrowdStrike, and regional managed security providers. Global platforms compete through AI capabilities, cloud integration, threat intelligence, and ecosystem partnerships, while regional players compete through customization, pricing flexibility, and localized compliance expertise. The top five vendors collectively account for approximately 45% of enterprise security service deployments. Competition centers on automation, response speed, platform consolidation, and service scalability, with AI-driven solutions improving operational efficiency by nearly 40% and reducing manual security workload by over 30%. Companies are expanding through acquisitions, cloud partnerships, and integrated security platforms. The competitive landscape is shifting toward autonomous security operations, creating higher entry barriers around AI models, threat intelligence databases, and enterprise trust. Winning requires continuous innovation, global service capability, and the ability to deliver measurable cybersecurity outcomes.

IBM

Cisco Systems

Palo Alto Networks

CrowdStrike

Fortinet

Check Point Software Technologies

Broadcom

Trend Micro

Sophos

Zscaler

Rapid7

CyberArk

SentinelOne

Artificial intelligence and machine learning are transforming security-as-a-service platforms by enabling automated threat detection, predictive analysis, and faster incident response. AI-driven security assistants improve investigation efficiency by approximately 40% compared with traditional analyst-led workflows, while more than 60% of large enterprises are adopting automation capabilities. Companies such as Microsoft, IBM, and Cisco are integrating generative AI into managed security operations to improve response speed and reduce analyst workload.

Cloud-native security architecture is replacing legacy appliance-based protection models as enterprises operate hybrid and multi-cloud environments. Modern cloud security platforms improve visibility and deployment speed by nearly 35% compared with fragmented legacy systems, enabling organizations to consolidate security controls. Extended detection and response (XDR), identity security, and security orchestration technologies are becoming competitive differentiators as vendors expand integrated platforms.

Between 2026 and 2028, autonomous security operations, AI governance, and zero-trust frameworks will shape market positioning. Organizations adopting intelligent security platforms gain faster response cycles, improved compliance readiness, and lower operational complexity. Vendors investing in AI security partnerships and ecosystem integration will benefit most as enterprises move from reactive protection toward continuous cyber resilience.

August 2024 — IBM introduced a generative AI-powered Cybersecurity Assistant for its managed Threat Detection and Response Services, using watsonx capabilities to accelerate investigation workflows. The solution improved analyst efficiency and strengthened AI-enabled security operations. Source: www.newsroom.ibm.com

January 2025 — Cisco launched AI Defense to secure enterprise AI applications, protecting against AI misuse and data leakage risks. The platform strengthened AI governance capabilities and supported safer enterprise AI deployment strategies across digital environments. Source: www.newsroom.cisco.com

April 2025 — Palo Alto Networks introduced Cortex XSIAM 3.0 with AI-driven security operations enhancements, adding exposure management and advanced email security capabilities. The platform surpassed $1 billion in cumulative bookings, highlighting strong enterprise adoption momentum. Source: www.paloaltonetworks.com

April 2025 — Cisco and ServiceNow expanded their partnership to simplify secure AI adoption by integrating Cisco AI Defense with ServiceNow Security Operations. The collaboration targeted enterprise-scale AI security management and reduced complexity in governance workflows.

The Information Technology (IT) Security as a Service Market Report covers comprehensive segmentation by type, application, and end-user, including cloud-based security services, managed security solutions, threat management, identity protection, enterprises, SMEs, and industry-specific deployments. The report evaluates adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The study analyzes emerging technologies such as artificial intelligence security, zero-trust frameworks, automation, XDR platforms, and cloud-native protection models. It provides strategic insights into competitive positioning, technology adoption, deployment trends, and investment priorities. With analysis of leading market participants and evolving enterprise requirements, the report supports expansion planning, partnership strategies, operational decisions, and long-term cybersecurity market positioning through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,685.0 Million |

| Market Revenue (2033) | USD 4,292.7 Million |

| CAGR (2026–2033) | 12.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Microsoft Corporation; IBM Corporation; Cisco Systems, Inc.; Palo Alto Networks, Inc.; CrowdStrike Holdings, Inc.; Fortinet, Inc.; Check Point Software Technologies Ltd.; Broadcom Inc.; Trend Micro Incorporated; Sophos Ltd.; Zscaler, Inc.; Rapid7, Inc.; CyberArk Software Ltd.; SentinelOne, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |