Reports

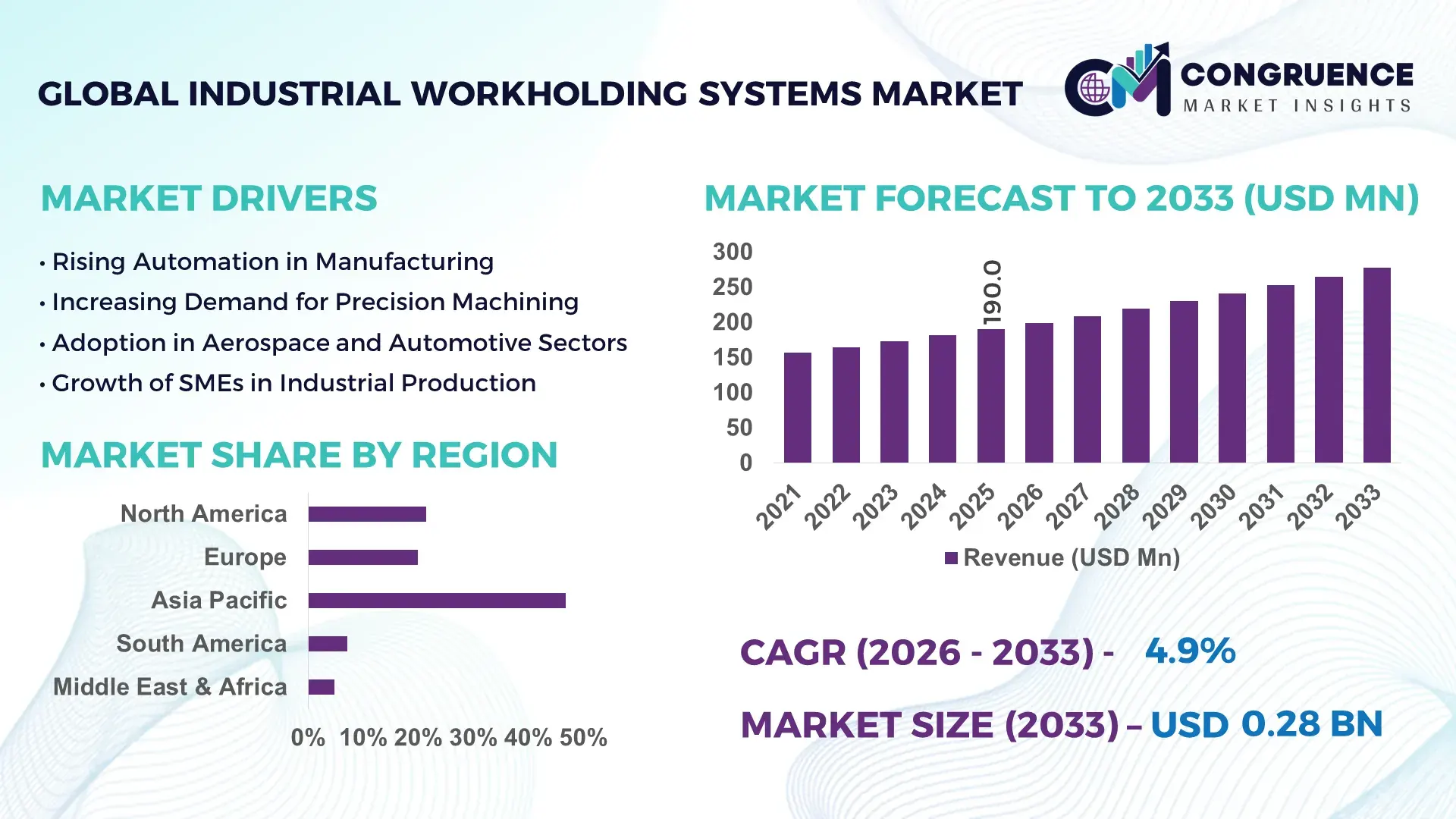

The Global Industrial Workholding Systems Market was valued at USD 190.0 Million in 2025 and is anticipated to reach a value of USD 277.7 Million by 2033 expanding at a CAGR of 4.86% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is supported by rising demand for precision machining, higher automation penetration in manufacturing plants, and increasing adoption of CNC-based production systems across heavy and light industries.

China represents the most influential national market within the Asia Pacific industrial workholding systems landscape, supported by its unmatched manufacturing scale and machine-tool production capacity. In 2024, China accounted for over 45% of global CNC machine tool installations, creating sustained demand for chucks, fixtures, vises, and modular workholding platforms. Annual investment in industrial automation equipment exceeded USD 38 billion, with automotive, general machinery, and electronics manufacturing as primary application areas. Chinese manufacturers increasingly deploy hydraulically actuated and quick-change workholding systems, improving machining throughput by over 20% in high-volume production lines.

Market Size & Growth: USD 190.0 Million in 2025, projected to reach USD 277.7 Million by 2033 at a CAGR of 4.86%, driven by rising CNC machining density and factory automation upgrades.

Top Growth Drivers: CNC machine penetration (+62%), machining accuracy improvement (+28%), production downtime reduction (+22%).

Short-Term Forecast: By 2028, advanced workholding adoption is expected to reduce setup time by approximately 25%.

Emerging Technologies: Smart sensor-enabled fixtures, modular zero-point clamping systems, hydraulically actuated workholding platforms.

Regional Leaders: Asia Pacific (USD 112.0 Million by 2033, high-volume manufacturing), Europe (USD 86.4 Million, precision engineering focus), North America (USD 63.3 Million, automation-led adoption).

Consumer/End-User Trends: Automotive and general machinery manufacturers account for nearly 58% of system deployments, emphasizing quick-change and repeatable setups.

Pilot or Case Example: In 2024, a German automotive plant achieved 18% machining efficiency gains through modular workholding retrofits.

Competitive Landscape: SCHUNK holds ~18% share, followed by SMW-Autoblok, Jergens Inc., Röhm GmbH, and Kitagawa Industries.

Regulatory & ESG Impact: Energy-efficient machining mandates drive adoption of lighter, recyclable alloy-based fixtures.

Investment & Funding Patterns: Over USD 1.1 billion invested globally since 2022 in tooling and precision manufacturing infrastructure.

Innovation & Future Outlook: Integration with digital twins and AI-driven setup optimization defines next-generation systems.

The Industrial Workholding Systems Market is shaped by automotive (34%), general machinery (29%), aerospace (16%), and electronics manufacturing (12%), with rapid growth in modular fixtures and zero-point clamping technologies. Regulatory emphasis on energy efficiency, regional production localization, and demand for high-mix low-volume manufacturing are reshaping consumption patterns, particularly in Asia Pacific and Europe.

The Industrial Workholding Systems Market plays a strategic role in enabling high-precision, high-throughput manufacturing across critical industrial sectors. As manufacturers pursue tighter tolerances and shorter production cycles, advanced workholding has become a foundational productivity lever. Smart modular clamping systems deliver up to 30% setup-time reduction compared to conventional fixed fixtures, directly improving machine utilization rates. Asia Pacific dominates in production volume, while Europe leads in advanced adoption, with over 42% of precision machining enterprises using sensor-enabled or quick-change workholding solutions.

By 2028, AI-assisted setup optimization is expected to cut machining errors by approximately 20%, improving first-pass yield across CNC operations. From an ESG standpoint, firms are committing to material efficiency improvements, including up to 15% reduction in steel usage per fixture by 2030 through lightweight alloys and modular reuse strategies. In 2024, Japan achieved a 17% reduction in machining downtime through automated clamping integration in automotive component manufacturing. Looking ahead, the Industrial Workholding Systems Market will remain a pillar of operational resilience, regulatory compliance, and sustainable industrial growth.

The Industrial Workholding Systems Market dynamics are shaped by accelerating industrial automation, growing CNC machine installations, and increasing demand for flexible manufacturing systems. Manufacturers are shifting toward modular and quick-change workholding to support high-mix production environments. Asia Pacific leads volume demand, while Europe and North America emphasize precision, automation compatibility, and digital integration. Material innovation, such as lightweight alloys and composite fixtures, is gaining traction as manufacturers target efficiency and sustainability improvements across machining operations.

Automation-driven factories require repeatable, high-accuracy workholding to maintain throughput consistency. Automated machining cells now account for over 48% of new CNC installations globally, significantly boosting demand for hydraulic and pneumatic workholding solutions that support unmanned operations and multi-axis machining.

Customized fixtures and precision systems involve higher initial investment, often 30–40% more than standard solutions, limiting adoption among small and mid-sized manufacturers operating on constrained capital budgets.

Modular fixtures enable reuse across product lines, reducing tooling changeover time by up to 35% and lowering lifecycle tooling costs, creating strong adoption potential in flexible manufacturing setups.

Limited availability of skilled operators for advanced fixturing and automation integration slows implementation, particularly in emerging manufacturing regions.

Shift Toward Modular Workholding Platforms: Modular systems now account for over 40% of new installations, enabling faster changeovers and up to 25% productivity improvement.

Integration with Automation Cells: More than 52% of newly installed workholding systems are designed for robotic loading and automated machining environments.

Adoption of Lightweight Materials: Aluminum and composite fixtures reduce fixture weight by 18–22%, improving machine energy efficiency.

Growth in High-Precision Applications: Aerospace and EV component machining demand tolerances below 5 microns, driving adoption of advanced hydraulic and zero-point clamping systems.

The Industrial Workholding Systems Market is segmented by type, application, and end-user, reflecting the diversity of machining requirements across modern manufacturing environments. Type-based segmentation highlights the balance between traditional mechanical systems and advanced hydraulic, pneumatic, and modular solutions designed for automation-ready production. Application segmentation is strongly influenced by machining intensity, tolerance requirements, and production volumes across sectors such as automotive, aerospace, general machinery, and electronics. End-user segmentation further reveals distinct adoption patterns between large-scale manufacturers, contract machining service providers, and small-to-medium enterprises, each prioritizing different performance metrics such as setup speed, repeatability, flexibility, and lifecycle cost efficiency. Together, these segmentation dimensions illustrate how demand is shifting toward flexible, high-precision, and automation-compatible workholding solutions aligned with evolving industrial production models.

The Industrial Workholding Systems Market by type includes mechanical workholding systems, hydraulic workholding systems, pneumatic workholding systems, modular/zero-point clamping systems, and magnetic workholding systems. Mechanical workholding systems remain the leading segment, accounting for approximately 38% of total adoption, due to their reliability, lower complexity, and widespread use in conventional machining and general-purpose CNC operations. Hydraulic workholding systems follow with around 27% adoption, driven by their ability to deliver consistent clamping force, improved surface finish, and suitability for high-precision and high-volume machining environments.

Modular and zero-point clamping systems, while currently representing about 19% of installations, are the fastest-growing type, expanding at an estimated 6.8% CAGR, supported by increasing demand for flexible manufacturing, reduced setup times, and frequent product changeovers. Pneumatic and magnetic workholding systems collectively account for roughly 16% of the market, serving niche applications such as lightweight component machining, thin-wall parts, and specialized grinding operations.

• In 2025, a national manufacturing technology institute reported the deployment of zero-point clamping systems in automotive machining lines, achieving setup time reductions exceeding 30% and improving machine utilization across multi-shift operations.

By application, the market spans automotive manufacturing, general machinery, aerospace, electronics and electrical equipment, and other industrial applications. Automotive manufacturing leads application demand with approximately 34% adoption, supported by high-volume production, strict dimensional accuracy requirements, and extensive use of CNC machining centers for powertrain, chassis, and structural components. General machinery applications account for nearly 26%, reflecting steady demand from industrial equipment, agricultural machinery, and heavy engineering segments.

Aerospace applications, currently at around 18% adoption, represent the fastest-growing application segment with an estimated 7.2% CAGR, driven by increasing aircraft production rates, lightweight material machining, and tolerance requirements below 10 microns. Electronics and electrical equipment manufacturing contributes close to 14%, supported by precision machining of housings, connectors, and thermal components. The remaining applications together represent roughly 8% of usage.

In 2025, over 41% of global automotive suppliers reported upgrading workholding systems to support automated machining cells, while 29% of aerospace manufacturers indicated increased adoption of hydraulic and modular fixtures for multi-axis machining.

• In 2024, a government-backed aerospace manufacturing program documented the use of advanced hydraulic workholding systems across multiple facilities, improving machining consistency for complex aluminum and titanium components.

End-user segmentation includes large manufacturing enterprises, contract machining and job shops, and small-to-medium manufacturing enterprises (SMEs). Large manufacturing enterprises dominate end-user adoption, accounting for approximately 46% of installed systems, supported by higher capital availability, large CNC machine fleets, and continuous production requirements. Contract machining and job shops represent about 32%, relying heavily on modular and quick-change workholding to accommodate diverse customer requirements and short production runs.

SMEs, currently contributing around 22%, form the fastest-growing end-user segment with an estimated 6.3% CAGR, driven by gradual automation adoption, falling costs of modular systems, and increased participation in global supply chains. Industry surveys indicate that 37% of job shops prioritize workholding upgrades to reduce setup time, while over 28% of SMEs report improved order turnaround after adopting modular fixtures.

In 2025, approximately 35% of manufacturing enterprises globally reported piloting automation-compatible workholding systems to improve machining flexibility and reduce operator dependency.

• In 2024, an industrial productivity agency reported that SME adoption of modular workholding systems enabled over 400 manufacturers to improve batch-change efficiency and reduce non-cutting time across CNC operations.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

The regional landscape of the Industrial Workholding Systems Market reflects strong disparities in industrial maturity, automation penetration, and manufacturing density. North America and Europe together accounted for over 41% of global demand in 2025, driven by precision engineering, aerospace, and automotive production. Asia-Pacific leads due to high-volume manufacturing, machine tool installations exceeding 55% of global CNC deployments, and rising automation investments. South America and the Middle East & Africa collectively contributed nearly 12%, supported by industrial diversification, energy-sector investments, and localized manufacturing expansion. Across regions, adoption of modular and hydraulic workholding systems has increased by over 30% since 2022, indicating a global shift toward flexible, automation-compatible machining infrastructure.

North America accounted for approximately 21.4% of the Industrial Workholding Systems Market in 2025, supported by strong demand from automotive, aerospace, defense, and industrial machinery sectors. The United States represents more than 78% of regional consumption, driven by large CNC machine fleets and a high concentration of automated machining cells. Federal incentives supporting smart manufacturing and reshoring initiatives have accelerated investments in advanced tooling and fixturing solutions. Over 44% of machining facilities in the region utilize hydraulically actuated or zero-point clamping systems. Digital transformation trends include integration of workholding with machine monitoring platforms to reduce setup errors by nearly 20%. A leading domestic tooling manufacturer expanded modular fixture production capacity in 2024 to support aerospace-grade precision machining. Regional consumer behavior shows higher enterprise adoption in capital-intensive industries, particularly aerospace and defense manufacturing.

Europe held close to 19.9% of global market demand in 2025, led by Germany, the United Kingdom, and France, which together represented nearly 67% of regional installations. Germany alone accounted for over 38% of European demand due to its advanced automotive and machine-tool industries. Sustainability initiatives under EU manufacturing efficiency frameworks have encouraged adoption of lightweight, reusable, and modular workholding systems, reducing material waste by up to 15%. Over 48% of European machining centers use quick-change or modular fixtures to comply with productivity and traceability requirements. Advanced sensor-enabled fixtures are increasingly adopted in aerospace and medical device manufacturing. A major European tooling supplier introduced digitally calibrated clamping systems in 2024, improving repeatability for high-precision applications. Regional behavior reflects regulatory pressure driving demand for transparent, standardized, and explainable manufacturing systems.

Asia-Pacific dominates global volume consumption and ranked first in overall growth contribution in 2025. China, Japan, and India collectively accounted for more than 72% of regional demand. China alone represents approximately 49% of Asia-Pacific installations, supported by machine tool output exceeding 1 million units annually. Japan contributes around 16%, driven by precision engineering and robotics integration, while India’s share surpassed 11%, supported by expanding automotive and industrial equipment manufacturing. Infrastructure investments and factory automation programs have increased CNC adoption by over 35% since 2021. Regional innovation hubs focus on smart fixtures, AI-assisted setup optimization, and hydraulically balanced systems. A major Japanese manufacturer deployed intelligent clamping platforms in 2024, achieving over 25% reduction in setup time. Consumer behavior shows strong growth driven by e-commerce manufacturing, electronics, and mobile-driven industrial automation.

South America accounted for approximately 7.1% of the global Industrial Workholding Systems Market in 2025. Brazil and Argentina together represented nearly 64% of regional demand, supported by automotive assembly, metal fabrication, and energy-sector equipment manufacturing. Infrastructure upgrades and renewable energy projects have increased demand for precision machining components, driving higher adoption of hydraulic and modular fixtures. Trade policies encouraging localized production have supported domestic tooling consumption, with industrial automation investments rising by over 22% since 2022. A Brazilian tooling firm expanded fixture production for automotive suppliers in 2024, improving domestic supply resilience. Regional consumer behavior reflects demand linked to localized manufacturing, media equipment fabrication, and language-specific industrial labeling requirements.

The Middle East & Africa region contributed approximately 4.8% of global demand in 2025. The UAE and South Africa accounted for more than 58% of regional installations, supported by oil & gas equipment manufacturing, construction machinery, and industrial repair services. Industrial diversification initiatives have driven increased investment in CNC machining centers, with adoption rising by 19% over three years. Technological modernization focuses on robust mechanical and hydraulic workholding systems suited for heavy-duty applications. Trade partnerships and free-zone manufacturing policies have supported tooling imports and localized assembly. A UAE-based industrial group implemented modular workholding systems in 2024 to improve machining throughput for energy-sector components. Regional consumer behavior emphasizes durability, long lifecycle performance, and compatibility with harsh operating environments.

China – 31.5% Market Share: High manufacturing output, extensive CNC machine installations, and large-scale industrial automation programs support dominance in the Industrial Workholding Systems Market.

United States – 18.7% Market Share: Strong aerospace, automotive, and defense manufacturing bases with high adoption of advanced and modular workholding technologies drive sustained leadership.

The Industrial Workholding Systems Market exhibits a moderately fragmented competitive structure, characterized by the presence of more than 70 active global and regional manufacturers offering mechanical, hydraulic, pneumatic, modular, and zero-point clamping solutions. Competition is driven by product precision, durability, automation compatibility, and customization capabilities rather than price alone. The top five companies collectively account for approximately 48–52% of global installations, reflecting a balanced mix of global leaders and strong regional specialists.

Market leaders focus heavily on R&D-led differentiation, with over 35% of leading players introducing modular or quick-change systems optimized for CNC automation and robotic machining cells. Strategic initiatives include cross-border distribution partnerships, localized manufacturing expansions, and co-development programs with machine tool OEMs. Product launch cycles have shortened, with new workholding platforms introduced every 18–24 months on average.

Innovation trends shaping competition include sensor-integrated fixtures, lightweight alloy designs reducing fixture mass by up to 20%, and digitally calibrated clamping systems improving repeatability below 5 microns. Mergers and acquisitions remain selective, primarily aimed at expanding geographic reach or acquiring niche precision technologies. Overall, the market rewards manufacturers that combine mechanical reliability with digital readiness and application-specific engineering depth.

Jergens, Inc.

Röhm GmbH

Carr Lane Manufacturing Co.

Kurt Manufacturing Company

OK-Vise Co., Ltd.

Te-Co Manufacturing

Chick Workholding Solutions

GRESSEL AG

LANG Technik GmbH

Positrol Workholding

Vektek LLC

Technological evolution in the Industrial Workholding Systems Market is closely aligned with automation, precision machining, and digital manufacturing trends. One of the most impactful developments is the widespread adoption of zero-point clamping systems, which enable fixture changeovers in under 60 seconds, compared to 10–15 minutes for conventional setups. These systems now represent over 40% of new installations in high-mix production environments.

Hydraulic workholding technology continues to advance, delivering consistent clamping forces exceeding 30 kN, ensuring improved surface finish and dimensional accuracy for complex parts. Pneumatic systems are increasingly optimized for lightweight components, offering faster actuation cycles below 0.5 seconds.

Digital integration is another key trend. Sensor-enabled fixtures capable of monitoring clamping force, vibration, and part presence are being integrated with CNC controllers and MES platforms. Such systems reduce setup-related errors by up to 22% and improve machine utilization rates. Material innovation also plays a role, with aluminum and composite-based fixtures reducing overall fixture weight by 15–25%, contributing to lower spindle load and energy consumption.

Looking forward, AI-assisted fixture design, digital twins for setup simulation, and robotics-compatible workholding are expected to become standard across advanced manufacturing facilities.

• In December 2025, Schunk showcased multiple innovations at EMO Hannover 2025, including a new internal hydraulic expansion clamping system for components up to 450 mm and the ROTA THW3 2+2 power chuck featuring a compensating clamping function and quick jaw change capability to enhance process reliability and versatility in complex workholding scenarios. Source: www.vdw.de

• In 2025, SMW Autoblok introduced automatic quick jaw change capability for its power chucks with the KNCS-matic series, enabling robotic conversion of chuck jaws and supporting digital factory requirements with automated handling and high-precision clamping. Source: www.geartechnology.com

• In December 2025, HWR Workholding expanded its portfolio with the INOFlex VF‑A hydraulic 4‑jaw chuck and the SOLIDPoint pneumatic coupler, designed to support automation‑ready workholding and simplify integration with SOLIDLine modular zero‑point systems for modern CNC environments. Source: www.geartechnology.com

• In January 2026, Schunk unveiled the ROTA THW3 2+2 power lathe chuck to the market, featuring independent jaw pairs with centrally compensating workpiece clamping that enhances safe, reliable holding of freeform and geometrically undefined parts in precision machining operations. Source: www.geartechnology.com

The Industrial Workholding Systems Market Report provides a comprehensive evaluation of the global market landscape, covering a broad spectrum of technologies, product types, applications, and end-user industries. The scope includes mechanical, hydraulic, pneumatic, magnetic, and modular/zero-point clamping systems used across CNC machining, turning, milling, grinding, and multi-axis operations. The report analyzes applications spanning automotive, aerospace, general machinery, electronics, energy equipment, and precision engineering sectors.

Geographically, the report assesses performance and adoption patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level insights for key manufacturing hubs such as China, the United States, Germany, Japan, and India. It evaluates technological integration trends, including automation compatibility, sensor-enabled fixtures, lightweight material adoption, and digital manufacturing alignment.

The scope further includes competitive benchmarking, innovation pipelines, regulatory and sustainability considerations, and evolving end-user requirements such as setup time reduction, repeatability enhancement, and lifecycle efficiency. Emerging segments such as robotics-compatible workholding and AI-assisted fixture optimization are also examined to provide decision-makers with forward-looking strategic clarity.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 190.0 Million |

| Market Revenue (2033) | USD 277.7 Million |

| CAGR (2026–2033) | 4.86% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SCHUNK GmbH & Co. KG; SMW-Autoblok Group; Kitagawa Corporation; Jergens, Inc.; Röhm GmbH; Carr Lane Manufacturing Co.; Kurt Manufacturing Company; OK-Vise Co., Ltd.; Te-Co Manufacturing; Chick Workholding Solutions; GRESSEL AG; LANG Technik GmbH; Positrol Workholding; Vektek LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |