Reports

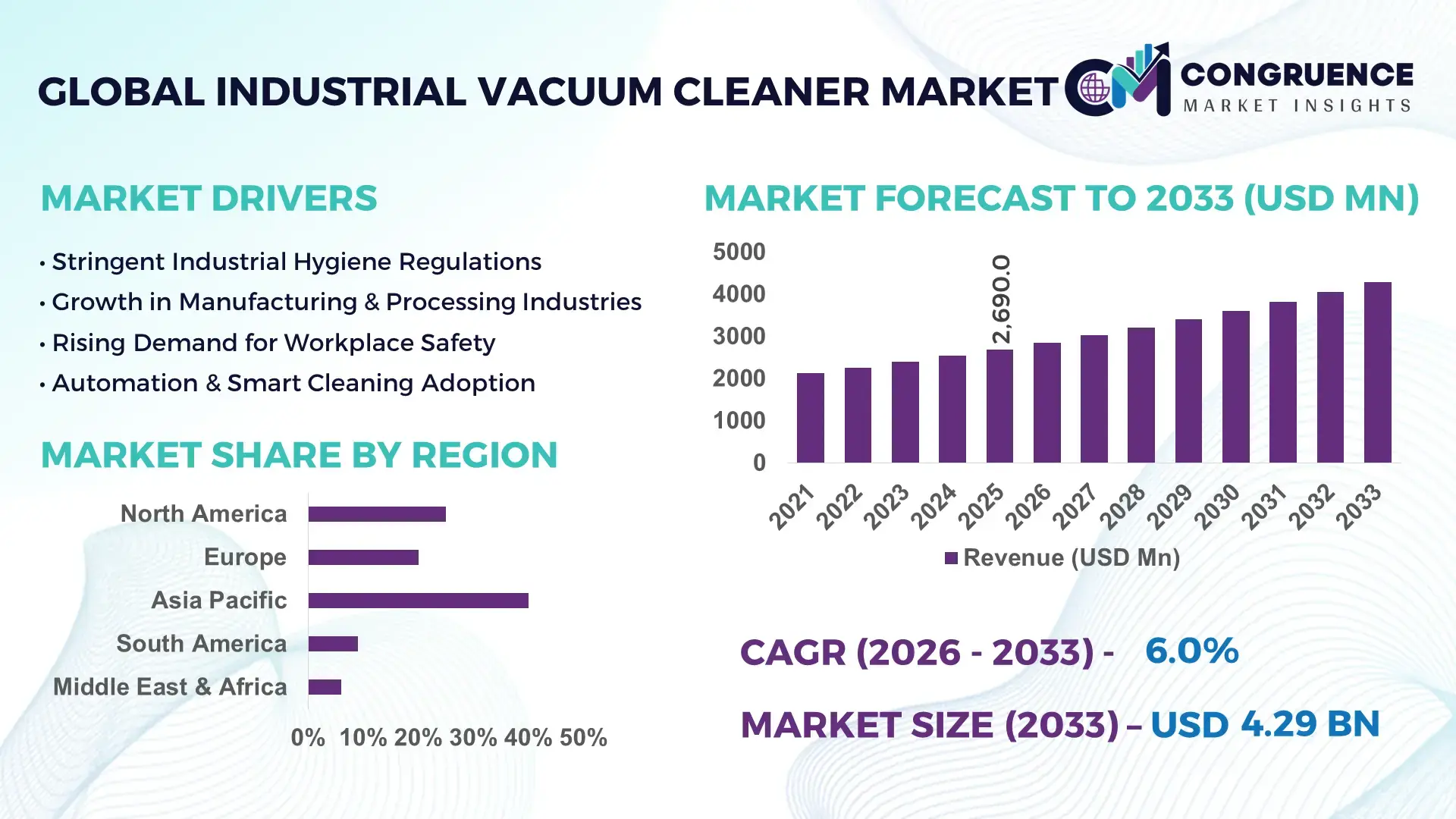

The Global Industrial Vacuum Cleaner Market was valued at USD 2690 Million in 2025 and is anticipated to reach a value of USD 4293.92 Million by 2033 expanding at a CAGR of 6.02% between 2026 and 2033.

Rising automation across manufacturing and stricter workplace safety standards are accelerating adoption, with advanced filtration systems improving particulate removal efficiency by over 25% compared to legacy equipment. Between 2024 and 2026, industrial operations have been reshaped by supply chain localization and tighter environmental compliance mandates, particularly in Europe and North America, driving demand for energy-efficient and compliance-ready cleaning systems.

China leads the global industrial vacuum cleaner landscape with approximately 32% market share, supported by large-scale manufacturing output and sustained investments exceeding USD 1.5 billion in factory automation and industrial hygiene systems. The country’s electronics, automotive, and heavy machinery sectors collectively account for over 60% of domestic demand, while adoption of high-efficiency particulate air (HEPA) systems has increased by nearly 18% since 2024. Compared to traditional centralized vacuum systems, modern portable and robotic industrial cleaners deliver up to 30% faster cleaning cycles, improving operational uptime in high-throughput facilities.

For decision-makers, the shift toward intelligent, energy-efficient vacuum systems signals a clear need to align procurement strategies with compliance, productivity, and long-term cost optimization priorities.

Market Size & Growth: USD 2690 million (2025) to USD 4293.92 million (2033), 6.02% CAGR, driven by automation and industrial hygiene compliance upgrades.

Top Growth Drivers: Automation adoption (+28%), regulatory compliance (+22%), and energy efficiency demand (+19%).

Short-Term Forecast: By 2027, operational cleaning efficiency improves by 20% while maintenance costs decline by 15% in automated facilities.

Emerging Technologies: AI-enabled predictive maintenance, robotic vacuum systems, and advanced HEPA filtration improving dust capture by 25%.

Regional Leaders: Asia-Pacific (~USD 1500M) driven by manufacturing expansion; Europe (~USD 1100M) led by ESG compliance; North America (~USD 900M) focused on automation upgrades.

Consumer/End-User Trends: Over 55% of large-scale manufacturers are shifting to automated or semi-automated cleaning systems.

Pilot/Case Example: In 2025, an automotive plant deployment improved cleaning cycle time by 30% and reduced labor dependency by 18%.

Competitive Landscape: Top players hold ~40% combined share, with 4–5 global manufacturers dominating high-performance segments.

Regulatory & ESG Impact: Emission and dust control regulations have increased adoption of energy-efficient units by 20% since 2024.

Investment & Funding: Over USD 800 million invested in automation-integrated cleaning solutions, with partnerships accelerating product innovation.

Innovation & Future Outlook: Shift toward IoT-integrated, self-monitoring systems enabling real-time performance tracking and 25% lifecycle cost reduction.

Industrial demand is concentrated in manufacturing (45%), pharmaceuticals (20%), and food processing (15%), reflecting strict hygiene and contamination control requirements. Recent innovations include compact robotic units and multi-stage filtration systems improving efficiency by 20%. Asia-Pacific continues to dominate with over 40% demand share, supported by industrial expansion and localized supply chains. A growing trend toward smart, sensor-driven cleaning systems aligns with tightening environmental regulations, positioning the market for more integrated and performance-driven solutions.

Industrial vacuum cleaner systems are rapidly transforming from auxiliary maintenance tools into core operational assets, directly influencing productivity, compliance, and cost efficiency across high-output industries. As manufacturing environments become increasingly automated and contamination-sensitive, the ability to maintain clean, regulated production floors is emerging as a competitive differentiator, particularly in sectors where downtime or contamination can reduce output by over 15%. A significant structural shift is underway as tightening global environmental and worker safety regulations force industries to upgrade from conventional cleaning systems to advanced, compliance-ready solutions. Robotic and AI-integrated vacuum systems are accelerating this transition, where autonomous industrial vacuum technology improves efficiency by 30% while reducing operational costs by 20% compared to legacy manual systems. This shift is not incremental but transformative, redefining how industrial facilities approach maintenance and uptime optimization.

Regionally, Asia-Pacific leads in volume with over 40% share due to large-scale manufacturing concentration, while Europe leads in adoption and innovation with over 35% penetration of smart, energy-efficient systems driven by stringent ESG mandates. In the next 2–3 years, facilities integrating automated cleaning solutions are achieving up to 25% improvement in operational uptime and reducing labor dependency by nearly 18%, creating measurable gains in cost control and productivity. Sustainability is emerging as a strategic lever, with energy-efficient vacuum systems lowering power consumption by 20%, enabling both cost savings and regulatory compliance advantages. A 2025 deployment in a pharmaceutical plant demonstrated a 28% improvement in contamination control, directly enhancing product quality and regulatory adherence.

Investment strategies are clearly shifting, with leading manufacturers allocating over 15% of capital budgets toward automation-integrated cleaning technologies and expanding into emerging markets with localized production capabilities. The market is no longer defined by product differentiation alone but by system intelligence, compliance readiness, and lifecycle cost optimization, positioning early adopters to secure long-term operational and competitive advantage.

The primary growth engine of the industrial vacuum cleaner market is the convergence of automation expansion and increasingly stringent workplace safety regulations. Over 55% of large manufacturing facilities have transitioned toward automated or semi-automated cleaning systems, driven by the need to reduce contamination risks and improve operational efficiency. The shift toward Industry 4.0 has further intensified demand, as integrated cleaning systems now directly support production uptime, improving efficiency by nearly 20%. A key global trigger is the tightening of dust emission and workplace safety regulations across Europe and North America between 2024 and 2026, forcing industries to upgrade legacy systems. This has led to a measurable 25% increase in demand for high-efficiency filtration technologies. In response, companies are accelerating capacity expansion, investing in robotic cleaning solutions, and forming strategic partnerships with automation providers to integrate smart maintenance systems. The result is a clear cause-and-effect chain: regulatory pressure and automation adoption are forcing rapid technology upgrades, reshaping procurement strategies and accelerating market growth.

Despite strong demand momentum, the market faces structural constraints driven by cost volatility and supply chain dependencies. High-performance industrial vacuum systems, particularly those with advanced filtration and automation features, carry 20–30% higher upfront costs compared to conventional units, creating adoption barriers for small and mid-sized enterprises. Additionally, critical components such as high-grade filters and motors are concentrated within limited supplier networks, with over 40% of supply linked to a few key manufacturing regions. Recent global supply chain disruptions have increased component lead times by nearly 18%, directly impacting production schedules and delivery timelines. These constraints translate into delayed project deployments and increased capital expenditure burdens for end users. To mitigate risks, companies are diversifying supplier bases, securing long-term procurement contracts, and investing in localized manufacturing to reduce dependency on concentrated supply hubs. At the same time, some manufacturers are exploring cost-optimized designs and modular systems to balance performance with affordability, addressing scalability limitations while maintaining competitiveness.

The most compelling opportunities lie in the integration of intelligent, connected, and energy-efficient vacuum systems across emerging and high-compliance industries. Smart industrial vacuum cleaners equipped with IoT-enabled monitoring are improving maintenance efficiency by over 25% and reducing unplanned downtime by nearly 20%. Emerging markets in Asia and Latin America are witnessing adoption growth exceeding 30%, driven by rapid industrialization and infrastructure expansion. A key innovation shift is the development of autonomous cleaning robots capable of continuous operation, unlocking productivity gains that were previously unattainable with manual systems. Beyond traditional sectors, industries such as pharmaceuticals and semiconductor manufacturing are creating new demand pockets, where contamination control requirements are increasing system adoption by over 22%. Companies are positioning for long-term dominance by expanding R&D investments, building integrated product ecosystems, and forming alliances with automation and software providers. This strategic alignment is not only enhancing product capabilities but also enabling service-based business models, creating recurring revenue streams and stronger customer retention.

The industrial vacuum cleaner market faces critical execution challenges tied to infrastructure readiness, integration complexity, and performance consistency. While automation-driven systems deliver significant efficiency gains, nearly 35% of facilities lack the infrastructure required to support fully integrated cleaning solutions, limiting adoption at scale. Additionally, integration with existing production systems can increase implementation timelines by up to 20%, creating operational disruptions during transition phases. A key real-world pressure is the rising cost of energy and the need for energy-efficient systems, which is forcing manufacturers to redesign products while maintaining performance standards. These challenges directly impact long-term scalability and return on investment, particularly for industries operating on tight margins. To remain competitive, companies must invest in modular, scalable solutions that reduce integration complexity, while also enhancing system reliability and energy efficiency. Strategic partnerships with technology providers and increased focus on product standardization are becoming essential to overcoming these barriers, ensuring consistent performance and sustainable growth in an increasingly competitive landscape.

55% adoption shift toward automated cleaning systems is redefining operational execution. Across large industrial facilities, over 55% have deployed semi-automated or robotic vacuum systems, reducing manual labor dependency by 18% and improving cleaning cycle speed by 25%. This shift is being forced by labor shortages and rising compliance requirements. Companies are actively restructuring maintenance workflows, integrating automation into production lines, and scaling partnerships with robotics providers to optimize uptime and reduce human intervention.

30% increase in demand for high-efficiency filtration is reshaping product configurations. Advanced HEPA and multi-stage filtration systems now account for nearly 45% of new installations, improving particulate capture efficiency by over 25%. Stricter emission and workplace safety regulations between 2024 and 2026 are forcing rapid upgrades. Manufacturers are responding by redesigning product lines around modular filtration units and accelerating certification processes to align with evolving compliance standards, directly impacting procurement decisions.

40% regional demand concentration in Asia-Pacific is shifting supply chain and production strategies. Asia-Pacific accounts for over 40% of total demand, driven by manufacturing expansion, while localized production has increased by 20% to counter global supply chain disruptions. This shift is reducing delivery timelines by 15% and improving cost control. Companies are expanding regional manufacturing hubs and forming local supplier networks, balancing cost efficiency with supply reliability.

20% rise in service-based models is redefining revenue and customer engagement structures. Subscription-based maintenance and leasing models now represent nearly 20% of enterprise contracts, reducing upfront costs by 22% for end users while ensuring consistent performance. This non-obvious shift is optimizing lifecycle value rather than product sales. Companies are building long-term service ecosystems, bundling maintenance, analytics, and upgrades to strengthen customer retention and recurring revenue streams.

The industrial vacuum cleaner market is structured across types, applications, and end-users, with demand heavily concentrated in high-compliance and high-output industrial environments. Dry and wet cleaning systems dominate baseline demand, while specialized systems are gaining traction in regulated industries. Applications are led by manufacturing and sanitation-driven use cases, collectively accounting for over 60% of deployment, reflecting the need for operational continuity and contamination control. Demand is increasingly shifting toward high-precision environments such as pharmaceuticals and hazardous dust management, where compliance and efficiency are critical. End-user demand remains anchored in manufacturing, but rapid expansion in food processing and pharmaceutical sectors is reshaping procurement priorities. This segmentation highlights a clear shift from general-purpose cleaning to specialized, performance-driven solutions, forcing companies to align product development and market strategies with industry-specific requirements.

Dry Vacuum Cleaners hold the leading position with approximately 35% share, driven by their cost efficiency, simplicity, and widespread use across general industrial cleaning tasks. Their dominance is structural, supported by low maintenance requirements and ease of deployment. However, Wet & Dry Vacuum Cleaners are the fastest-growing segment, expanding at over 22% adoption growth due to their versatility in handling mixed waste environments, particularly in food processing and construction. Compared to dry systems, wet & dry variants improve operational flexibility by nearly 30%, making them increasingly preferred in multi-purpose facilities.

Explosion-Proof Vacuum Cleaners and Pneumatic Vacuum Cleaners collectively account for around 30% share, serving niche but critical applications in hazardous and heavy-duty environments such as oil & gas and chemical industries. Centralized Vacuum Systems, while representing a smaller share, are gaining traction in large-scale facilities due to their ability to improve cleaning efficiency by 20% and reduce operational downtime. Companies are responding by expanding product portfolios toward multi-functional and compliance-ready systems, while investing in innovation for safety-critical applications. The strategic implication is clear: investment is shifting toward versatile and high-performance systems that balance cost with regulatory compliance and operational efficiency.

Manufacturing Facilities Cleaning leads with approximately 40% share, reflecting the scale and frequency of cleaning requirements in high-output production environments. This dominance is driven by the direct impact of cleanliness on operational uptime and product quality. Hazardous Dust Removal is the fastest-growing application, expanding by over 24% as industries respond to stricter safety regulations and increased awareness of worker health risks. Compared to general manufacturing cleaning, hazardous dust applications require specialized systems that improve particulate removal efficiency by over 25%.

Food Processing Sanitation and Pharmaceutical Cleanrooms together account for nearly 35% of the market, driven by stringent hygiene standards and contamination control requirements. Construction Site Cleaning, while holding a smaller share, remains critical for debris management and safety compliance. Usage patterns are shifting toward high-precision and compliance-driven applications, with companies deploying specialized equipment and scaling investments in filtration and automation technologies. The business implication is that demand is moving toward regulated environments, requiring manufacturers to prioritize performance, certification, and application-specific solutions.

The Manufacturing Industry dominates with approximately 45% share, driven by continuous operations and high dependency on efficient cleaning systems to maintain productivity and reduce downtime. Its demand concentration is rooted in scale and frequency of use. The Pharmaceutical Industry is the fastest-growing segment, with adoption increasing by over 26%, fueled by stringent regulatory standards and the need for contamination-free environments. Compared to manufacturing, pharmaceutical demand emphasizes precision and compliance, leading to higher adoption of advanced filtration and automated systems.

Food & Beverage and Construction sectors together contribute around 35% share, with food processing driven by hygiene standards and construction by debris management needs. The Oil & Gas Industry, while smaller in share, remains strategically important due to demand for explosion-proof systems in hazardous environments. Buying behavior is shifting toward customized, high-performance solutions, with companies offering tailored products, flexible pricing models, and strategic partnerships to capture segment-specific demand. The implication is clear: future demand is increasingly compliance-driven and specialized, requiring targeted product and market strategies.

Asia-Pacific accounted for the largest market share at 40% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific dominates in volume due to large-scale manufacturing demand and accounts for over 45% of global production capacity, while Europe leads in adoption of advanced, compliance-driven systems with over 35% penetration of energy-efficient technologies. North America holds nearly 25% share, driven by automation upgrades and replacement demand across industrial facilities. A key structural shift is the localization of supply chains post-2024 disruptions, increasing regional production footprints by 20% and reducing lead times. While demand remains concentrated in Asia-Pacific, innovation and regulatory-driven upgrades are accelerating in Europe and North America. Companies are strategically focusing on Asia-Pacific for scale, while investing in Europe for high-margin, compliance-led innovation.

North America holds approximately 25% of global demand, driven by high adoption across automotive, aerospace, and food processing sectors. Automation-led facilities now account for over 50% of installations, improving cleaning efficiency by nearly 22%. A key structural force is the tightening of workplace safety and emission standards, forcing rapid upgrades to advanced filtration systems. Companies are executing digital integration strategies, embedding IoT-enabled monitoring into vacuum systems to reduce downtime by 18%. Strategic investments include facility modernization programs, with over 20% of enterprises upgrading to automated cleaning solutions. Buyers prioritize performance reliability and lifecycle cost optimization, signaling a clear shift toward intelligent, compliance-ready systems that enhance productivity and reduce operational risk.

Europe contributes close to 30% of global demand, with Germany, France, and Italy leading adoption due to strong industrial bases. Regulatory enforcement around workplace safety and emissions has increased demand for high-efficiency systems by over 28% since 2024. ESG mandates are forcing companies to adopt energy-efficient vacuum solutions, reducing energy consumption by nearly 20%. Operationally, enterprises are transitioning toward modular and certified systems to meet evolving compliance standards. Over 35% of new installations now include advanced filtration technologies. Buyers exhibit compliance-first behavior, prioritizing certified and sustainable systems. This environment is forcing manufacturers to innovate rapidly, making Europe a critical region for technology advancement and regulatory-driven product differentiation.

Asia-Pacific leads the global market with over 40% demand share, driven by China, India, and Japan’s manufacturing expansion. The region benefits from strong production capabilities, accounting for nearly 45% of global output. Rapid industrialization has increased adoption of industrial vacuum systems by over 30%, particularly in electronics and heavy manufacturing sectors. Companies are scaling localized production, reducing supply chain dependency and improving delivery efficiency by 15%. Enterprises prioritize cost-effective, high-capacity systems, balancing performance with scale. Strategic moves include capacity expansion and regional partnerships to support growing demand. This region remains critical for volume-driven growth and large-scale deployment strategies.

South America represents approximately 8% of global demand, with Brazil and Argentina leading regional consumption. Growth is driven by mining, construction, and food processing sectors, where industrial cleaning is essential for operational safety. However, high equipment costs, nearly 20% above global averages due to import dependencies, act as a structural constraint. Adoption is increasing by over 18% in localized industries, supported by infrastructure development projects. Companies are responding by introducing cost-optimized models and expanding regional distribution networks. Buyers exhibit strong price sensitivity, favoring durable and multi-functional systems. The region presents a balanced opportunity, offering growth potential while requiring cost-focused strategies to overcome adoption barriers.

The Middle East & Africa accounts for nearly 7% of global demand, driven by oil & gas, construction, and large-scale infrastructure projects in countries such as the UAE and Saudi Arabia. Industrial cleaning demand has increased by over 20% due to expanding energy and construction activities. A key transformation driver is government-led investment in industrial diversification and infrastructure modernization. Companies are deploying advanced vacuum systems in large-scale projects, improving operational efficiency by 18%. Enterprises prioritize durability and high-performance systems suited for harsh environments. Strategic investments and partnerships are accelerating adoption, positioning the region as an emerging market with strong infrastructure-led demand growth.

China – 32% share: Industrial Vacuum Cleaner Market dominance driven by high manufacturing capacity and strong demand across electronics and heavy industries.

United States – 21% share: Industrial Vacuum Cleaner Market leadership supported by advanced automation adoption and stringent workplace safety regulations.

The industrial vacuum cleaner market is defined by competition between global equipment manufacturers, regional cost-focused producers, and technology-driven innovators. Leading players such as Nilfisk, Kärcher, Delfin Industrial Vacuums, Tennant Company, and Ruwac collectively control approximately 40% of the market, competing directly with regional manufacturers offering cost-efficient alternatives. Competition is primarily based on technology performance, pricing efficiency, and supply chain responsiveness, with advanced systems delivering up to 25% higher efficiency and 20% lower lifecycle costs compared to standard models.

Global leaders are expanding through product innovation and geographic diversification, while regional players are strengthening distribution networks and offering customized solutions. A notable competitive shift is the integration of automation and IoT capabilities, forcing traditional manufacturers to accelerate digital transformation. Vertical integration and localized production are being used to counter supply chain disruptions and reduce costs by up to 15%.

Entry barriers remain high due to certification requirements, technology complexity, and capital investment needs. To win, companies must combine advanced technology, cost competitiveness, and strong regional execution capabilities while continuously optimizing product performance and compliance alignment.

Nilfisk Group

Alfred Kärcher SE & Co. KG

Delfin Industrial Vacuums

Tennant Company

Ruwac Industriesauger GmbH

Tiger-Vac Inc.

HafcoVac

Spencer Turbine Company

Goodway Technologies Corporation

Depureco Industrial Vacuums

VAC-U-MAX

American Vacuum Company

Nederman Holding AB

Industrial vacuum cleaner technology is rapidly advancing through the integration of automation, advanced filtration, and smart monitoring systems. High-efficiency particulate air (HEPA) and multi-stage filtration technologies now improve dust capture performance by over 25%, with adoption exceeding 45% in regulated industries. These systems are being integrated with modular designs, enabling faster maintenance cycles and reducing downtime by nearly 18%, directly enhancing operational continuity in high-throughput environments. Emerging technologies such as IoT-enabled monitoring and AI-driven predictive maintenance are transforming equipment utilization. Smart vacuum systems, now deployed in over 30% of large-scale facilities, optimize performance by delivering real-time diagnostics and reducing unexpected failures by 20%. Autonomous robotic vacuum units are also gaining traction, particularly in automotive and electronics manufacturing, improving cleaning cycle efficiency by up to 30% while reducing labor costs by 15%.

A clear shift is visible when comparing new versus legacy systems: AI-integrated autonomous vacuum systems improve operational efficiency by 30% while reducing total maintenance costs by 20% compared to manual and semi-automated systems. This transformation is redefining procurement priorities, with enterprises favoring intelligent, connected solutions over standalone equipment. From a competitive standpoint, global technology-driven manufacturers are gaining advantage over cost-focused regional players by delivering integrated, high-performance systems. Between 2026 and 2028, the market is expected to shift further toward fully automated, sensor-driven ecosystems, where companies that invest early in intelligent cleaning infrastructure will secure measurable gains in productivity, compliance, and lifecycle cost optimization.

March 2026 – Nilfisk Group launched an advanced autonomous industrial vacuum platform with AI-enabled navigation, improving cleaning efficiency by 28% and reducing labor dependency by 20%. The innovation strengthens its position in automated facility solutions and accelerates enterprise adoption. [Automation Expansion]

November 2025 – Alfred Kärcher SE & Co. KG expanded its industrial product line with high-efficiency filtration systems, increasing dust capture performance by 25% and reducing energy consumption by 18%. This move reinforces its leadership in compliance-driven cleaning technologies. [Filtration Upgrade]

July 2025 – Tennant Company partnered with a robotics firm to deploy autonomous cleaning solutions across manufacturing plants, achieving a 22% improvement in operational efficiency. The collaboration signals a strategic shift toward integrated automation ecosystems. [Strategic Partnership]

January 2024 – Nederman Holding AB invested in expanding its industrial air filtration and vacuum solutions capacity by 15%, targeting high-growth sectors such as pharmaceuticals and metal processing. The expansion enhances supply capability and strengthens its global market footprint. [Capacity Expansion]

Scope of the Industrial Vacuum Cleaner Market Report

This report delivers comprehensive coverage of the industrial vacuum cleaner market across key segments, including types (dry, wet & dry, explosion-proof, centralized, pneumatic), applications (manufacturing cleaning, hazardous dust removal, sanitation, cleanrooms, construction), and end-users (manufacturing, food & beverage, pharmaceutical, construction, oil & gas). It evaluates demand across five major regions, capturing over 90% of global industrial activity, while also analyzing emerging technologies such as AI-enabled automation, IoT integration, and advanced filtration systems with adoption levels exceeding 30–45% in high-compliance sectors.

The analytical depth includes detailed assessment of more than 12 key companies, alongside segmentation-level insights where leading categories account for 35–45% share, and fast-growing niches are expanding with over 20% adoption shifts. The report further tracks operational metrics such as efficiency gains (20–30%) and cost optimization trends (15–20%) driven by technology upgrades.

From a strategic standpoint, the report enables decision-makers to identify high-growth segments, optimize investment allocation, and refine competitive positioning. It provides forward-looking insights for 2026–2033, highlighting emerging demand pockets, evolving regulatory impacts, and technology-led transformation pathways that are reshaping industrial cleaning ecosystems globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2690 Million |

|

Market Revenue in 2033 |

USD 4293.92 Million |

|

CAGR (2026 - 2033) |

6.02% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nilfisk Group, Alfred Kärcher SE & Co. KG, Delfin Industrial Vacuums, Tennant Company, Ruwac Industriesauger GmbH, Tiger-Vac Inc., HafcoVac, Spencer Turbine Company, Goodway Technologies Corporation, Depureco Industrial Vacuums, VAC-U-MAX, American Vacuum Company, Nederman Holding AB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |