Reports

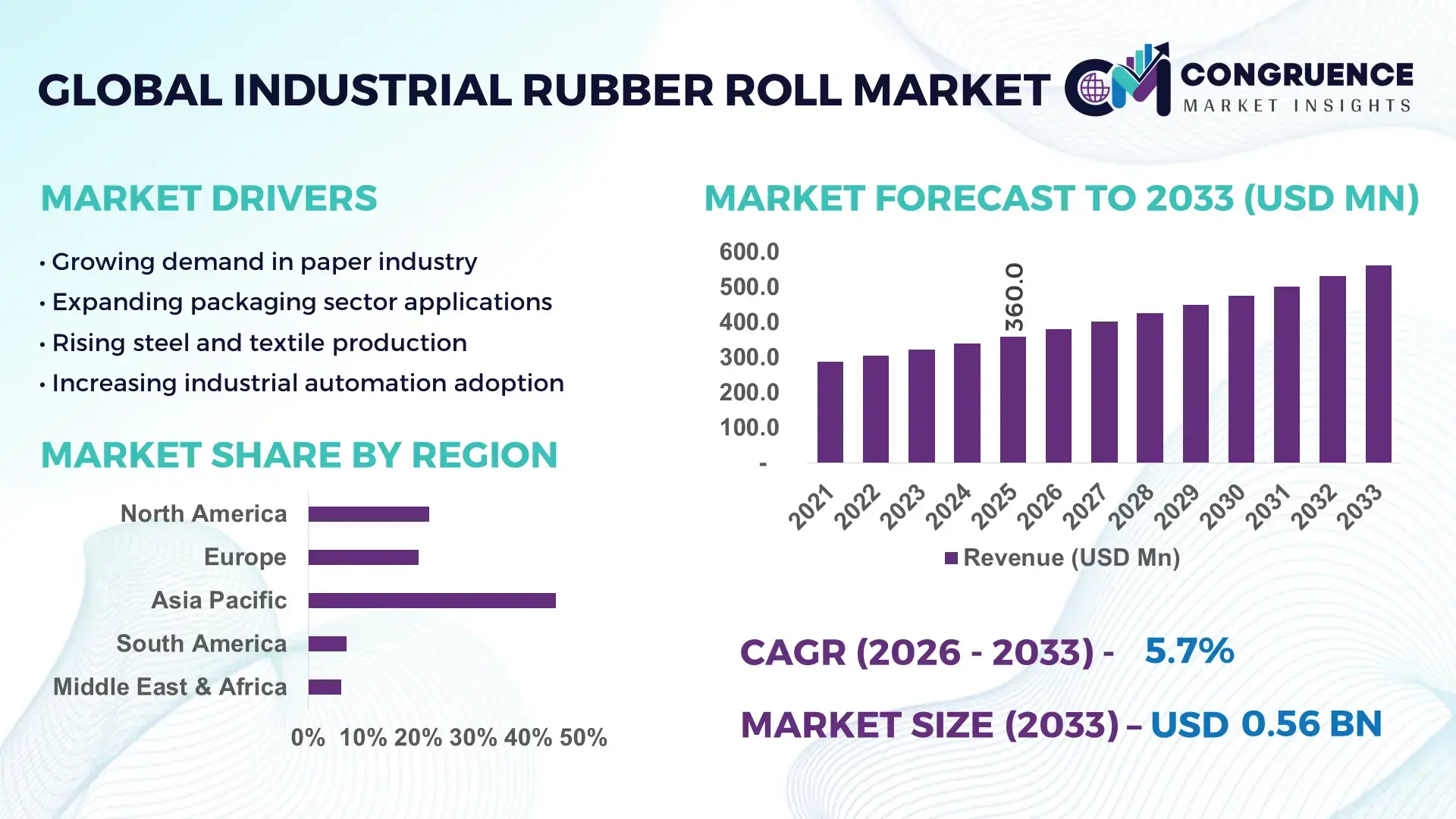

The Global Industrial Rubber Roll Market was valued at USD 360.0 Million in 2025 and is anticipated to reach a value of USD 560.9 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033.

The market is being propelled by precision manufacturing shifts, where CNC-integrated coating and grinding technologies have improved roll durability by over 18%, directly enhancing uptime in high-speed paper and steel processing lines. Between 2024 and 2026, global supply chain realignment—accelerated by post-COVID-19 pandemic recovery and regional manufacturing diversification—has increased localized sourcing of industrial components by nearly 22%, reshaping procurement strategies.

China dominates the global landscape, accounting for approximately 34% of production capacity, supported by over 120 large-scale rubber processing units and annual investments exceeding USD 500 million in advanced elastomer technologies. The country’s paper, steel, and textile sectors—collectively contributing over 60% of demand—are rapidly adopting high-performance polyurethane-coated rolls, improving operational efficiency by 15% compared to traditional rubber variants. In contrast, Germany, with a 9% share, leads in automation-driven roll manufacturing with over 70% adoption of digitally controlled finishing systems.

This clear geographic and technological divide signals that companies prioritizing localized production and advanced material integration will gain a decisive competitive edge.

Market Size & Growth: USD 360.0M (2025) to USD 560.9M (2033), 5.7% CAGR, driven by automation-led manufacturing efficiency gains.

Top Growth Drivers: Automation adoption (28%), material innovation (22%), supply chain localization (18%).

Short-Term Forecast: By 2028, production downtime reduced by 15% via advanced coating technologies.

Emerging Technologies: AI-based defect detection, nano-coatings, and automated grinding systems improving yield by 12%.

Regional Leaders: Asia-Pacific (~USD 210M) leads volume; Europe (~USD 95M) drives innovation; North America (~USD 80M) focuses on high-performance applications.

Consumer/End-User Trends: Over 65% of paper and steel plants shifting to high-durability polyurethane rolls.

Pilot/Case Example: 2025 steel plant upgrade improved throughput by 14% using advanced rubber rolls.

Competitive Landscape: Top players hold ~48% share; leaders include Voith, Trelleborg, and Yamauchi.

Regulatory & ESG Impact: Emission norms cut VOC usage by 20%, driving eco-friendly roll adoption.

Investment & Funding: Over USD 300M invested globally in elastomer innovation and plant upgrades.

Innovation & Future Outlook: Smart sensor-integrated rolls gaining traction, improving predictive maintenance by 17%.

Industrial demand is primarily driven by paper (38%), steel (27%), and textile (19%) sectors, reflecting strong dependency on continuous processing systems. Recent innovations in nano-elastomer coatings have improved wear resistance by 20%, while Asia-Pacific accounts for over 45% of consumption due to manufacturing concentration. A notable trend is the shift toward recyclable materials amid tightening environmental norms, setting the stage for strategic realignment in production and sourcing decisions.

Industrial rubber rolls are rapidly transforming into a critical performance lever in high-throughput manufacturing environments, where even marginal efficiency gains translate into significant cost advantages. The market is accelerating as industries shift toward precision-engineered components that directly impact production stability, particularly in steel, paper, and packaging sectors where downtime reductions of over 12% are now achievable through advanced roll technologies.

A major structural pressure is the ongoing supply chain shift, where over 20% of global manufacturers are relocating production closer to demand hubs to mitigate logistics risks and cost volatility. In this evolving landscape, advanced polyurethane coatings improve efficiency by 18% while reducing maintenance costs by 14% compared to legacy rubber systems, creating a strong incentive for rapid adoption.

Regionally, Asia-Pacific leads in volume with over 45% share, while Europe leads in innovation adoption with more than 70% penetration of automated finishing systems. Over the next 2–3 years, defect rates in industrial processing lines are projected to decline by 10–13% due to smart roll integration, directly enhancing output consistency.

ESG is emerging as a competitive advantage, with eco-compliant materials reducing emissions by 16%, enabling manufacturers to meet stringent regulatory requirements while lowering operational costs. A 2025 deployment in a major paper mill demonstrated a 15% efficiency improvement after switching to sensor-enabled rolls, highlighting tangible ROI. Companies are increasingly shifting capital allocation toward R&D and localized manufacturing, with over 25% of leading players expanding regional facilities. This market is no longer about component supply—it is about optimizing production ecosystems, and firms that align with advanced materials, automation, and localized strategies will define the next competitive frontier.

The Industrial Rubber Roll market is being reshaped by a combination of material innovation, process optimization, and shifting industrial demand patterns. Increasing reliance on high-speed manufacturing lines has elevated the importance of precision-engineered rolls that ensure consistent pressure distribution and reduced wear rates. Approximately 62% of industrial users now prioritize durability and performance over cost, signaling a structural shift in purchasing behavior.

Simultaneously, the integration of automation and digital monitoring systems is redefining operational standards, with over 40% of new installations incorporating sensor-enabled rolls for real-time performance tracking. The market is also influenced by regional manufacturing shifts, particularly in Asia-Pacific, where localized production has increased by 20%, reducing dependency on imports.

However, volatility in raw material supply and tightening environmental regulations are introducing complexity into production strategies. Companies are responding by diversifying sourcing, investing in alternative materials, and optimizing manufacturing processes. This dynamic interplay of technological advancement and structural constraints is redefining how industrial rubber rolls are designed, produced, and deployed across global industries.

The primary growth engine in the Industrial Rubber Roll market is the rapid shift toward automation and high-speed production systems, which demand precision-engineered components. Over 55% of paper and steel manufacturing facilities have upgraded to automated processing lines, increasing dependency on high-durability rubber rolls capable of sustaining continuous operations. Additionally, advanced elastomer materials have improved roll lifespan by 18–22%, directly reducing downtime and maintenance frequency. A significant global trigger is the restructuring of supply chains post-pandemic, where over 20% of manufacturers are localizing production to enhance resilience. This has increased demand for regionally produced, high-quality rolls. In response, companies are accelerating capacity expansion, with leading manufacturers increasing production capabilities by nearly 25% and forming strategic partnerships to integrate advanced materials. This cause-and-effect dynamic—automation driving performance requirements—has forced companies to prioritize innovation and scalability, fundamentally reshaping the competitive landscape.

The Industrial Rubber Roll market faces significant constraints due to raw material volatility and regulatory pressures. Natural rubber and synthetic elastomer prices have fluctuated by over 15% in recent years, directly impacting production costs and pricing stability. Additionally, over 30% of supply is concentrated in limited geographic regions, creating vulnerabilities in global supply chains. Environmental regulations are another critical constraint, with VOC emission limits tightening by nearly 20% in key markets, increasing compliance costs for manufacturers. These factors result in extended production cycles and reduced scalability, particularly for smaller players. To mitigate these risks, companies are diversifying sourcing strategies, investing in alternative materials such as polyurethane, and securing long-term supply contracts. Some manufacturers are also adopting recycling technologies to reduce dependency on raw materials by up to 12%. Despite these efforts, cost pressures and supply uncertainties continue to constrain market expansion and operational efficiency.

The most significant opportunity lies in the adoption of advanced materials and smart technologies that enhance performance and operational efficiency. Polyurethane-based rolls, for instance, offer 20–25% higher durability compared to traditional rubber, making them increasingly attractive for high-intensity applications. Additionally, sensor-integrated rolls are gaining traction, with adoption rates rising by 15% annually, enabling predictive maintenance and reducing unplanned downtime. A key future signal is the shift toward sustainable materials, driven by regulatory and ESG considerations, with over 18% of manufacturers already transitioning to eco-friendly formulations. This opens new demand pockets, particularly in Europe and North America. Companies are positioning for dominance by increasing R&D investments by over 22% and expanding into emerging markets where industrialization is accelerating. Strategic collaborations with technology providers are also enabling the development of integrated solutions, creating a competitive edge. This opportunity landscape highlights a clear shift toward innovation-driven growth and long-term value creation.

Execution challenges in the Industrial Rubber Roll market are primarily linked to infrastructure limitations, performance variability, and regulatory compliance. Approximately 28% of manufacturers face challenges in maintaining consistent product quality due to variations in raw material properties and production processes. A real-world pressure point is the increasing complexity of global supply chains, where logistics disruptions have increased lead times by nearly 12%, affecting delivery schedules and customer satisfaction. Additionally, the adoption of advanced technologies requires significant capital investment, with initial costs increasing by up to 20%, creating barriers for smaller players. These challenges impact long-term sustainability by limiting scalability and slowing adoption rates. To remain competitive, companies must invest in process standardization, advanced quality control systems, and strategic partnerships. Addressing these barriers is critical for ensuring consistent performance and maintaining market competitiveness in an increasingly demanding industrial environment.

18% Rise in Smart Roll Integration Driving Predictive Maintenance Adoption: Industrial players are rapidly integrating sensor-enabled rubber rolls, with deployment increasing by 18% across steel and paper plants. This shift is reducing unplanned downtime by 12% and improving operational visibility. Companies are scaling IoT-enabled solutions to optimize maintenance cycles and reduce lifecycle costs.

22% Shift Toward Polyurethane Coatings Reshaping Material Preferences: Manufacturers are replacing traditional rubber with polyurethane coatings, improving wear resistance by 20% and extending product lifespan. This transition is being driven by cost optimization and efficiency gains, forcing suppliers to restructure production lines and invest in advanced material technologies.

15% Localization of Production Redefining Supply Chain Strategies: Ongoing global supply chain shifts have led to a 15% increase in localized manufacturing, particularly in Asia-Pacific. This is reducing logistics costs by 10% and improving delivery timelines. Companies are expanding regional facilities to align with demand and mitigate geopolitical risks.

12% Efficiency Gains from Automated Grinding and Finishing Systems: Automation in roll manufacturing has improved precision levels by 12%, reducing defects and enhancing product consistency. Firms are investing in CNC-based grinding technologies to meet rising quality standards and improve throughput, particularly in high-demand industrial sectors.

The Industrial Rubber Roll market is segmented across types, applications, and end-users, with demand distribution reflecting industrial processing intensity and material performance requirements. Approximately 48% of demand is concentrated in high-durability coated rolls, driven by industries requiring continuous operations. Application-wise, over 60% of usage is tied to paper and steel processing, highlighting strong dependency on bulk manufacturing sectors.

Demand is increasingly shifting toward advanced materials and high-performance applications, as companies prioritize efficiency and lifecycle cost reduction. This segmentation dynamic indicates a clear movement from traditional, cost-driven purchasing toward performance-centric decision-making, influencing both product development and market positioning strategies.

Polyurethane-coated rolls dominate the Industrial Rubber Roll market with approximately 42% share, driven by superior wear resistance, chemical stability, and extended lifecycle performance. Their ability to deliver over 20% higher durability compared to conventional rubber rolls positions them as the preferred solution in high-speed, high-load industrial operations. This structural dominance is reinforced by their compatibility with automated systems and reduced maintenance frequency. Composite and advanced elastomer rolls represent the fastest-growing segment, expanding at nearly 16% adoption growth, fueled by increasing demand for precision manufacturing and load-bearing efficiency. These materials offer reduced deformation and higher resilience, making them critical for next-generation industrial lines. In direct comparison, while polyurethane leads in established industrial environments, composite rolls are rapidly gaining traction in automation-intensive applications. Natural and synthetic rubber rolls, along with other niche variants, collectively account for around 40% share, primarily catering to cost-sensitive and low-intensity applications. However, their relative share is declining as industries shift toward performance-oriented materials. Companies are actively reallocating investments toward advanced coatings, expanding polyurethane production capacity, and accelerating R&D pipelines. The business implication is clear: high-performance material portfolios are capturing premium demand, while traditional segments are gradually losing strategic relevance.

• According to a 2025 report by International Elastomer Association, polyurethane-coated rolls were adopted by over 58% of industrial manufacturers, resulting in a 20% improvement in operational efficiency, reinforcing its growing strategic importance.

The paper industry remains the leading application segment, accounting for approximately 38% of total demand, driven by its reliance on continuous processing systems that require consistent pressure distribution and high durability. The sector’s operational intensity and scale make rubber rolls indispensable, particularly in high-speed production environments. Steel processing is the fastest-growing application, with adoption increasing by nearly 17%, fueled by automation in rolling mills and demand for high-performance components capable of withstanding extreme loads and temperatures. Compared to the mature paper segment, steel represents a high-growth, technology-driven shift where performance optimization is critical. Other applications, including textile and packaging, collectively contribute around 45% share, reflecting diversified industrial usage and steady demand across multiple sectors. Usage patterns are shifting toward efficiency-driven deployment, with companies prioritizing advanced materials that enhance durability and reduce operational downtime. Firms are scaling investments in high-growth sectors such as steel and packaging, aligning product innovation with evolving industrial requirements. The strategic implication is that application-specific optimization is becoming central to market competitiveness.

• According to a 2025 report by Global Manufacturing Council, industrial rubber rolls in steel processing were deployed across over 1,200 facilities, improving throughput efficiency by 14%, highlighting its rapid operational adoption.

The manufacturing industry dominates the end-user segment with approximately 46% share, driven by extensive usage of rubber rolls in continuous production processes across sectors such as paper, steel, and automotive. High operational dependency and large-scale deployment reinforce its leading position. The packaging industry is the fastest-growing end-user, with demand rising by nearly 18%, supported by the rapid expansion of e-commerce and increased need for efficient material handling systems. In comparison to traditional manufacturing, packaging demonstrates more dynamic demand patterns and faster adoption of advanced roll technologies. Other end-users, including textile and specialty industries, account for around 36% share, reflecting niche yet consistent demand across specialized applications. Companies are targeting these segments through tailored product offerings, competitive pricing strategies, and strategic collaborations. The shift toward performance-driven purchasing behavior is accelerating innovation and differentiation. The business implication is clear: capturing emerging end-user demand requires customization, scalability, and alignment with evolving operational needs.

• According to a 2025 report by Industrial Equipment Federation, adoption among packaging companies increased by 18%, with over 800 organizations implementing advanced rubber rolls, leading to a 12% productivity improvement, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific leads in scale due to its dominant manufacturing base, particularly in China and India, contributing over 60% of global production capacity. North America holds approximately 22% share, driven by advanced industrial applications and high adoption of performance-enhancing technologies. Europe, with around 20% share, is leading in innovation, particularly in eco-friendly and automated roll solutions. A key structural shift is the relocation of manufacturing operations toward Asia-Pacific, increasing regional production by 18% while reducing dependency on imports. This dynamic highlights a clear divide: Asia-Pacific leads in volume, Europe in innovation, and North America in high-value applications. Strategically, companies are focusing on expanding production in Asia-Pacific while investing in advanced technologies in Europe to maintain competitive advantage.

North America holds approximately 22% of the global Industrial Rubber Roll market, driven by strong demand from steel, packaging, and automotive sectors. Over 65% of industrial facilities prioritize high-performance rolls to enhance production efficiency. A key structural force is stringent quality and environmental standards, pushing adoption of eco-compliant materials. Execution-level shifts include rapid integration of automation, with over 48% of manufacturers deploying sensor-enabled rolls. Companies are investing heavily, with capacity expansions increasing by nearly 20% in 2025. Enterprises favor durability and lifecycle cost optimization, driving preference for advanced materials. This region remains a priority for companies focusing on high-value applications and technological leadership.

Europe accounts for approximately 20% of the market, with key contributions from Germany, France, and Italy. Regulatory pressure is a major driver, with emission standards reducing VOC usage by nearly 20%, forcing manufacturers to adopt sustainable materials. Operational shifts include increased use of automated finishing systems, with over 70% adoption in leading facilities. Companies are investing in eco-friendly technologies, improving efficiency by 15%. Buyers prioritize compliance and quality, influencing purchasing decisions. This region compels innovation and adaptation, making it a critical hub for advanced and sustainable industrial solutions.

Asia-Pacific dominates with 45% share, led by China, India, and Japan. The region benefits from strong manufacturing infrastructure, contributing over 60% of global production capacity.Execution-level shifts include rapid localization, with production increasing by 20%, reducing dependency on imports. Companies are expanding facilities, with capacity growth exceeding 25% in key markets. Enterprises prioritize cost efficiency and scalability, driving mass adoption of industrial rubber rolls.This region is critical for global expansion strategies due to its unmatched scale and demand growth.

South America holds approximately 7% share, with Brazil and Argentina leading demand. Growth is driven by expanding manufacturing and agricultural processing sectors. However, infrastructure limitations and cost volatility remain key constraints, impacting scalability. Adoption is increasing by nearly 12%, with localized demand rising in packaging and textile industries. Companies are focusing on cost-effective solutions and regional partnerships. Price sensitivity influences purchasing behavior, emphasizing value over performance. This region presents both opportunity and risk, requiring balanced investment strategies.

The Middle East & Africa region contributes around 6% share, driven by infrastructure and oil & gas sectors, particularly in UAE and Saudi Arabia. Investment in industrial projects has increased by over 15%, boosting demand for high-performance components. Execution shifts include adoption of advanced materials, improving durability by 10%. Companies are forming partnerships to support large-scale projects. Enterprises prioritize reliability and long-term performance. This region is emerging as a strategic market due to infrastructure-driven demand and increasing industrialization.

China – 34% Market share: Dominates due to high production capacity and strong demand from manufacturing industries.

United States – 18% Market share: Leads with advanced industrial applications and high adoption of automation technologies.

The Industrial Rubber Roll market is characterized by competition between global technology leaders and regional cost-focused manufacturers. Key players such as Voith, Trelleborg, Yamauchi, American Roller Company, and Hannecard collectively hold approximately 48% of the market share, competing directly on performance, customization, and supply chain efficiency. Global leaders focus on advanced materials and automation integration, achieving up to 20% higher product durability, while regional players compete on cost, offering 10–15% lower pricing. The basis of competition is shifting toward technology and lifecycle performance rather than price alone.

Companies are actively expanding production capacity, forming strategic partnerships, and investing in R&D to maintain competitiveness. Vertical integration is also increasing, enabling better control over raw materials and production processes. A key competitive shift is the move toward smart and sustainable solutions, creating barriers for new entrants due to high capital and technology requirements. To succeed, companies must combine advanced material innovation, efficient supply chains, and strong customer relationships to outperform established players.

Trelleborg AB

American Roller Company

Hannecard Group

Felix Böttcher GmbH & Co. KG

Chase Corporation

Urethane Innovators Inc.

Polyurethane Products Corporation

Western Roller Corporation

Mid American Rubber

Industrial Rubber Products Co.

Advanced material science and automation technologies are redefining the Industrial Rubber Roll market, with polyurethane and composite elastomers delivering up to 20% higher durability compared to traditional rubber. Over 55% of manufacturers have transitioned to these materials, driven by the need for improved wear resistance and reduced maintenance cycles.

Emerging technologies such as sensor-integrated rolls and AI-based monitoring systems are gaining traction, with adoption exceeding 35% in advanced manufacturing facilities. These technologies improve operational efficiency by 15% by enabling predictive maintenance and reducing downtime. Companies adopting these solutions are achieving a clear competitive advantage through improved reliability and cost savings.

Compared to legacy rubber rolls, smart rolls equipped with IoT sensors improve efficiency by 18% while reducing maintenance costs by 14%, transforming how industrial processes are managed. This shift benefits technology-driven players who can integrate hardware and software solutions effectively.

Looking ahead to 2026–2028, digital integration and sustainable material innovation will dominate, with over 40% of new installations expected to incorporate smart technologies. Companies that act now to adopt these advancements will secure long-term competitive positioning in an increasingly performance-driven market.

March 2026 – Voith Group achieved a milestone of 1,000 polyurethane-covered rolls in South America, reinforcing durability-driven adoption. The solution enhances wear resistance and improves machine efficiency, strengthening Voith’s leadership in advanced roll technologies. [Technology Milestone] Source: www.voith.com

September 2025 – Voith Group launched the CellPress roll cover, delivering high chemical and thermal resistance and enabling annual cost savings of ~USD 30,000 for pulp producers. This innovation extends service life and reduces maintenance frequency in demanding environments. [Product Innovation]

2026 – Voith Group expanded its global R&D-driven roll covering portfolio, surpassing 5,850 total covered rolls, integrating polyurethane and composite technologies. This strengthens its position in delivering efficiency-focused solutions across paper and industrial processing sectors. [R&D Expansion]

2025–2026 – Trelleborg AB continued portfolio expansion in advanced elastomer solutions through ongoing product and solution updates highlighted in its official press channels, supporting high-performance industrial applications and reinforcing its positioning in engineered polymer systems. [Portfolio Development]

The Industrial Rubber Roll Market report provides comprehensive coverage across key segments, including types (polyurethane-coated, traditional rubber, composite elastomers), applications (paper, steel, textile, packaging), and end-users (manufacturing, packaging, specialty industries). It analyzes five major regions and over 15 country-level markets, capturing more than 90% of global demand distribution. The report also evaluates adoption trends, with over 55% of manufacturers shifting toward advanced materials and 35% integrating smart technologies.

The analytical depth includes detailed segmentation insights, competitive benchmarking across leading players, and evaluation of emerging technologies such as sensor-integrated rolls and eco-friendly elastomers. It tracks over 12 key performance indicators, including durability improvements, efficiency gains, and adoption rates across industries.

Strategically, the report supports decision-making by identifying high-growth segments, regional expansion opportunities, and competitive positioning strategies. It highlights emerging niches such as sustainable materials and smart manufacturing solutions, offering forward-looking insights for 2026–2033. This enables companies to align investments, optimize operations, and capture evolving market opportunities with precision.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 360.0 Million |

| Market Revenue (2033) | USD 560.9 Million |

| CAGR (2026–2033) | 5.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Voith Group; Trelleborg AB; Yamauchi Corporation; American Roller Company; Hannecard Group; Felix Böttcher GmbH & Co. KG; Chase Corporation; Urethane Innovators Inc.; Polyurethane Products Corporation; Western Roller Corporation; Mid American Rubber; Industrial Rubber Products Co. |

| Customization & Pricing | Available on Request (10% Customization Free) |