Reports

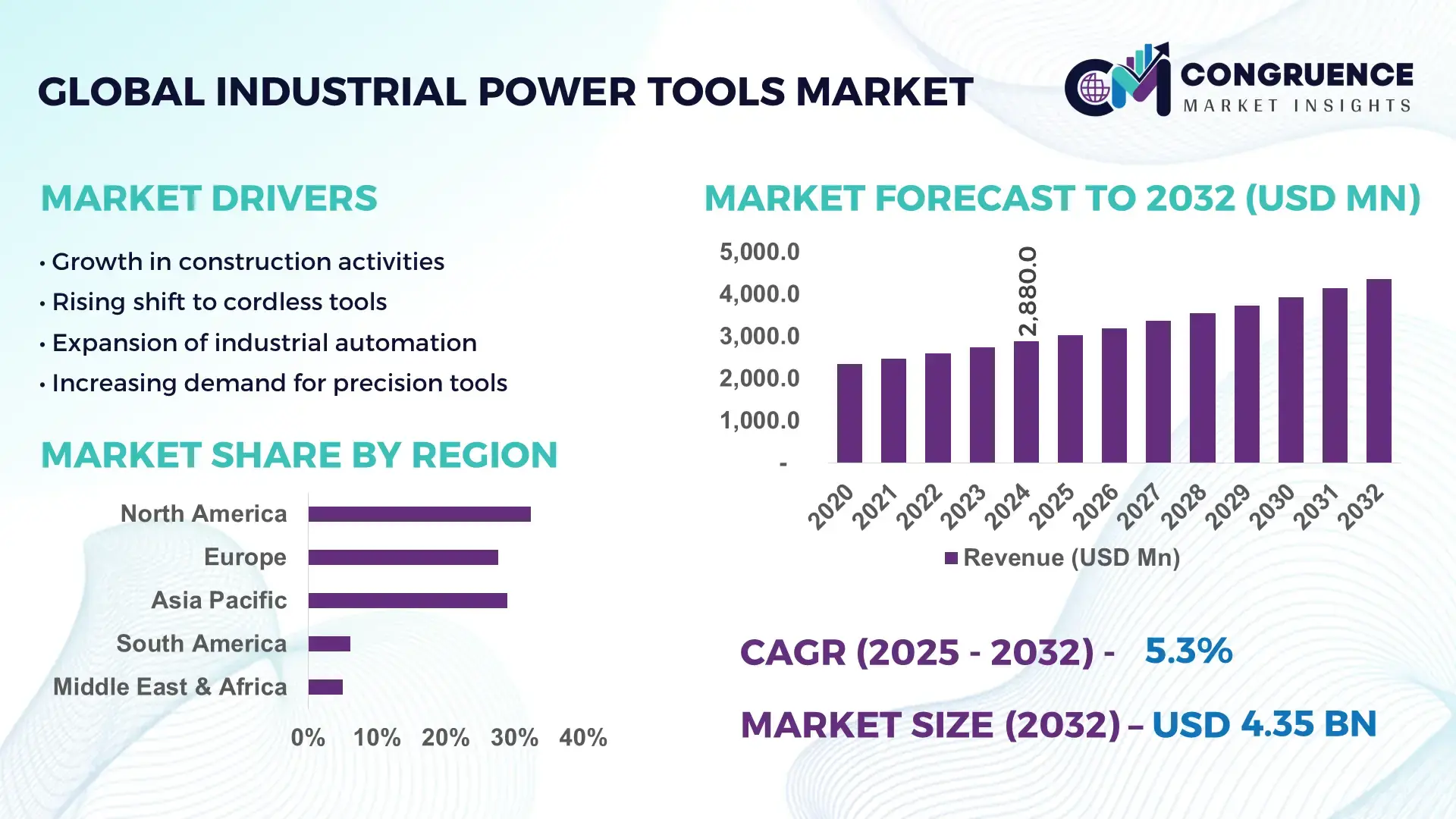

The Global Industrial Power Tools Market was valued at USD 2,880.0 Million in 2024 and is anticipated to reach a value of USD 4,353.3 Million by 2032, expanding at a CAGR of 5.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by accelerating industrial automation and rising adoption of high-precision tool systems.

The United States stands as the dominant country in the global Industrial Power Tools Market, supported by its advanced manufacturing capabilities and extensive investment in automated production systems. The country hosts over 250+ large-scale tool manufacturing and assembly facilities, with annual capital expenditure in industrial machinery surpassing USD 75 billion. High adoption in aerospace, automotive, and heavy engineering sectors drives demand for torque-controlled, battery-operated, and pneumatic tools. The U.S. also leads in robotics-enabled tool integrations, with more than 34% of industrial facilities deploying automated fastening and assembly systems.

Market Size & Growth: Valued at USD 2.88 billion in 2024, projected to reach USD 4.35 billion by 2032, expanding at 5.3% CAGR, supported by rising industrial automation.

Top Growth Drivers: 48% adoption in automated assembly, 32% efficiency improvement in manufacturing workflows, 41% rise in cordless tool utilization.

Short-Term Forecast: By 2028, engineered tools expected to deliver up to 27% reduction in operational downtime.

Emerging Technologies: AI-enabled torque monitoring and next-generation brushless motors accelerating precision and sustainability.

Regional Leaders: By 2032, North America projected at USD 1.21 billion, Europe at USD 1.09 billion, Asia Pacific at USD 1.58 billion—each driven by unique sectoral adoption patterns.

Consumer/End-User Trends: Strong uptake from automotive, aerospace, and energy sectors, with 52% preferring cordless solutions.

Pilot or Case Example: A 2027 automotive pilot integrated smart fastening tools, achieving 33% lower assembly errors.

Competitive Landscape: Market leader controls approx. 18% share, followed by five major competitors expanding portfolios in cordless and AI-integrated tools.

Regulatory & ESG Impact: Mandates for noise reduction and energy efficiency are shaping tool design and industrial adoption.

Investment & Funding Patterns: Over USD 3.2 billion recently invested in high-precision industrial tooling and automation systems globally.

Innovation & Future Outlook: Advancements in IoT-enabled tools and predictive maintenance are expected to shape next-generation manufacturing ecosystems.

Unique information about the Industrial Power Tools Market includes strong demand from auto-component, aerospace machining, heavy fabrication, and renewable infrastructure sectors, each contributing significantly to tool consumption patterns. Rapid innovations in brushless motors, ergonomic handling systems, and low-vibration tools are reshaping product design. Environmental regulations and energy-efficient standards are accelerating adoption of cordless electric platforms. Asia Pacific’s expanding manufacturing base and North America’s automation-led modernization continue to define near-term industry evolution.

The Industrial Power Tools Market plays a pivotal strategic role across manufacturing, construction, transportation, and energy sectors, driving measurable improvements in productivity, precision, and operational efficiency. As production environments increasingly shift toward automation, companies are prioritizing tool platforms that enhance process stability and reduce variability. New-generation brushless electric systems deliver up to 28% performance improvement compared to conventional brushed systems, demonstrating a clear evolutionary shift that supports long-term industrial modernization.

Regionally, Asia Pacific dominates in volume, driven by large-scale manufacturing, while North America leads in adoption, with over 46% of enterprises integrating smart or connected tool systems. This regional divergence highlights differentiated pathways for market expansion. By 2027, AI-driven predictive maintenance in tooling is expected to lower machine downtime by 22%, while digital torque management platforms will improve fastening accuracy by 18%.

Regulatory and ESG requirements are reshaping procurement, with firms committing to noise, vibration, and emission-related improvements, including up to 30% reductions in harmful occupational exposure by 2030. Micro-level transformations are already visible—for instance, in 2026, a major European aerospace facility achieved a 26% drop in assembly rework rates by integrating sensor-enabled industrial fastening systems.

Looking forward, the Industrial Power Tools Market is positioned as a core enabler of resilient manufacturing, compliant production ecosystems, and sustainable industrial advancement, underpinning the next phase of global industrial competitiveness.

The Industrial Power Tools Market is influenced by a combination of technological advancements, shifting industrial requirements, workforce skill optimization, and automation-driven transformation. Precision engineering, growth in modular and prefabricated construction, and an expanding manufacturing base in emerging economies are reinforcing demand. Industries such as automotive, aerospace, heavy machinery, and energy infrastructure are increasingly relying on torque-accurate, lightweight, and ergonomically engineered tools to meet modern production tolerances. Simultaneously, the integration of digital monitoring systems, IoT capabilities, and smart maintenance functionalities is reshaping how industrial facilities approach productivity, quality control, and safety. Collectively, these dynamics underscore a market transitioning towards high efficiency, reliability, and adaptability in diverse operational environments.

Automation-led modernization is significantly influencing the Industrial Power Tools Market as industries deploy advanced assembly systems requiring precision-driven equipment. Automated lines rely heavily on vibration-controlled drills, torque-driven fastening devices, and smart monitoring systems that can maintain tolerance levels within microns. Over 58% of automotive assembly operations now incorporate robotic-assisted power tools, reducing human error and improving standardization. Industries such as aerospace and electronics demand high-accuracy fastening, where misalignment or torque deviation rates must be kept below 1–2%, further boosting the adoption of intelligent industrial tools. The expansion of digital manufacturing ecosystems and the need for consistent quality outputs continue to reinforce automation as a primary driver.

The growing cost of advanced industrial power tools—especially smart, AI-integrated, and precision-driven systems—presents a significant restraint, particularly for small and mid-sized industrial firms. High-performance brushless motors and sensor-enabled torque systems can cost 25–40% more than conventional tools, increasing capital expenditure pressures. Maintenance and calibration requirements for high-precision manufacturing environments further add operational costs, while industries with thin operating margins struggle to justify upfront investments. Moreover, specialized tools require trained operators, and skill gaps in emerging economies slow adoption. These financial and capability-related barriers collectively restrict wider deployment of sophisticated tool systems.

The rapid development of smart factories presents substantial opportunities for the Industrial Power Tools Market. As industries transition toward interconnected, sensor-driven production systems, demand for digital torque tools, real-time usage monitoring, and predictive maintenance-enabled devices is accelerating. Over 43% of new manufacturing facilities are expected to incorporate IoT-enabled tooling technologies by the end of the decade. Integration with MES and ERP platforms creates opportunities for tool traceability, error-proofing, and automated quality assurance. Growing adoption of wireless diagnostics and cloud-based analytics across electronics, aerospace, and energy sectors opens pathways for innovative product lines and service-driven revenue models focused on industrial tool intelligence.

Industrial power tool usage comes with significant safety and compliance challenges, especially in environments with strict noise, vibration, and torque-consistency regulations. Incorrect torque levels can raise defect rates by up to 15%, while high vibration exposure contributes to occupational hazards, forcing industries to invest in additional safety gear and monitoring systems. Frequent tool misuse, inadequate calibration, and lack of operator training also disrupt productivity and increase accident risks. Furthermore, regulatory expectations around ergonomics and environmental emissions require constant product redesigns, adding complexity and cost for manufacturers. These operational risks continue to challenge seamless market expansion.

Expansion of Smart, Connected Tool Ecosystems: Industries are increasingly adopting connected tools equipped with torque sensors and wireless data monitoring. More than 40% of large manufacturing facilities now use digital tools to track performance and ensure fastening precision. These systems have led to measurable improvements, including 18% reductions in rework rates and 22% fewer assembly errors, strengthening tool reliability across automotive and aerospace applications.

Surge in Cordless and Battery-Optimized Tools: Cordless solutions continue to accelerate, driven by advances in lithium-ion batteries offering 35% longer runtime and 29% faster charging. Industrial users report up to 31% productivity gains with high-efficiency brushless motors. Demand is particularly strong in North America and Europe, where electric-powered platforms support energy efficiency mandates and ergonomic improvements.

Integration of AI and Predictive Maintenance: AI-integrated power tools capable of monitoring torque deviation, vibration levels, and usage anomalies are rapidly gaining traction. Early industrial use cases show 20–25% reductions in unexpected tool failures and 17% improvements in operational uptime. Predictive diagnostics are becoming critical in high-precision sectors such as aerospace machining and electronic assembly.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Power Tools Market. Research suggests that 55% of new projects experienced cost benefits with modular and prefabricated practices. Pre-bent and pre-cut elements minimize labor dependencies and accelerate timelines, increasing the need for high-precision tools. Europe and North America are witnessing strong uptake as developers aim for speed and efficiency in modern construction systems.

The Industrial Power Tools Market is segmented by type, application, and end-user categories, each demonstrating distinct adoption patterns and technological priorities. By type, demand varies across drilling tools, fastening tools, cutting tools, material removal tools, and sawing systems, with ergonomic designs and cordless innovations influencing user preferences. Application segmentation reflects strong penetration in manufacturing, construction, automotive assembly, aerospace operations, and energy-sector maintenance, each requiring tools with specific torque accuracy, durability, and operational reliability. End-user insights show that industrial manufacturing plants, automotive OEMs, metal fabrication facilities, and infrastructure developers represent the most significant consumer base, relying on precision-driven tools that enhance workflow efficiency and safety. Across all segments, cordless platforms, smart monitoring systems, and vibration-controlled technologies continue to gain prominence as industries move toward automation, lightweight handling, and digitally optimized production environments.

The Industrial Power Tools Market comprises drilling tools, fastening tools, cutting tools, grinding and material removal tools, sawing machines, and specialty industrial instruments. Fastening tools currently lead the segment, accounting for 34% share, supported by their essential role in automated assembly lines and torque-critical operations in automotive and aerospace manufacturing. Drilling tools follow with significant adoption driven by their versatility in metal, concrete, and composite fabrication. While traditional corded tools maintain utility, cordless electric variants are expanding rapidly due to improved battery density and reduced maintenance requirements. Cutting and material removal tools represent an important category, playing a major role in metalworking and fabrication environments where precision and speed are required. Together, these remaining tool types account for 41% combined share, reflecting their broad utility across sectors. The fastest-growing category is cordless fastening and drilling systems, expanding at an estimated 8.6% CAGR, driven by advancements in brushless motors, lightweight ergonomics, and integrated digital torque management.

The Industrial Power Tools Market spans manufacturing, construction, automotive assembly, aerospace production, energy infrastructure maintenance, and metal fabrication applications. Manufacturing leads the segment with 38% share, supported by increased automation, higher accuracy requirements, and rapid integration of programmable fastening and drilling systems. Construction applications hold substantial usage driven by rising modular building activity, sustained urban development, and increasing preference for cordless tools that reduce operator restrictions. Automotive assembly is accelerating quickly due to advanced torque-management needs and the proliferation of electric vehicle platforms requiring high-precision fastening at every stage. The fastest-growing application is aerospace manufacturing, expanding at an estimated 9.1% CAGR, supported by increased reliance on high-precision pneumatic and electric tools capable of maintaining extremely tight tolerance levels. Metal fabrication, energy-sector maintenance, and general industrial repair collectively represent 33% combined share, reflecting steady operational demand. In 2024, more than 39% of global enterprises reported implementing industrial tool automation pilots within their manufacturing lines. Surveys also show that 47% of skilled workers prefer cordless tool systems for efficiency and ergonomic comfort.

End-users in the Industrial Power Tools Market include industrial manufacturing facilities, automotive OEMs, aerospace companies, metal fabrication shops, energy-sector operators, and construction firms. Industrial manufacturing remains the leading end-user group with 36% share, driven by high-volume production environments requiring consistent accuracy, operational safety, and uptime reliability. Automotive OEMs follow closely due to increasing use of smart fastening systems and automated assembly workflows. Aerospace facilities exhibit the fastest growth, expanding at 9.4% CAGR, as lightweight, precision-controlled, digitally monitored tools become essential in aircraft component fabrication and structural assembly. Metal fabrication shops, energy utilities, and construction contractors collectively hold 35% combined share, driven by recurring equipment needs and modernization of infrastructure projects. Adoption rates across top industries show that more than 41% of fabrication facilities have transitioned to brushless-motor tools, while 45% of automotive plants are deploying AI-assisted torque verification. Workforce surveys indicate that over 52% of technicians prefer low-vibration tools to reduce fatigue and improve accuracy during long-duration operations.

North America accounted for the largest market share at 32.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

The global landscape shows strong performance across established and emerging economies, with Europe holding 27.6%, Asia-Pacific capturing 28.9%, South America contributing 6.1%, and the Middle East & Africa representing 5.0% of the total market in 2024. Variations in industrial maturity, construction output, government incentives, and digital adoption further shape regional competitiveness. Increasing automation, rising manufacturing investments, and ongoing technological modernization are expected to shift the market distribution gradually toward high-growth developing regions over the forecast period.

North America held a substantial 32.4% market share in 2024, supported by strong industrial output, advanced manufacturing clusters, and widespread adoption of cordless and digitally enabled power tools. Key industries such as automotive, aerospace, logistics, and construction continued to invest heavily in precision power tools to improve operational efficiency. Regulatory measures promoting workplace safety and energy-efficient equipment further strengthened market demand. Technological advancements, including smart torque systems and IoT-enabled diagnostics, have seen higher enterprise adoption in healthcare and finance-related facility management. A notable local player, Milwaukee Tool, expanded its cordless tool lineup across heavy-duty segments, reinforcing regional competitiveness. Consumer behavior in the region leans toward premium, durable, and performance-optimized power tools, reflecting high product awareness and technology readiness.

Europe accounted for 27.6% of the market in 2024, driven by strong demand in Germany, the United Kingdom, France, and Italy. The region continues to enforce stringent sustainability and workplace safety frameworks through regulatory bodies such as the European Committee for Standardization (CEN), which encourages manufacturers to adopt low-emission and energy-efficient equipment. Germany remains the dominant market due to its robust manufacturing sector, while France and the UK demonstrate strong adoption of automation-ready, sensor-integrated power tools. European consumers increasingly favor tools aligned with sustainability goals and compliance-oriented product designs. A key local player, Bosch Professional, actively invests in recyclable components and eco-efficient tool platforms, reinforcing green innovation across the region. Regulatory pressure has led to growing demand for explainable and traceable technology features within industrial environments.

The Asia-Pacific region captured 28.9% of the global market in 2024, ranking as the fastest-expanding volume-driven market. China, India, Japan, and South Korea remain the top-consuming countries due to large-scale construction activities, rapid industrialization, and expanding manufacturing ecosystems. The region is experiencing significant investment in infrastructure megaprojects, electronics production, and automotive assembly facilities, driving higher demand for cordless, automated, and ergonomic power tools. Technology hubs such as Shenzhen, Tokyo, and Bengaluru are fostering innovations in battery technologies, lightweight composite materials, and AI-enabled tool monitoring systems. Regional consumers show strong affinity for online purchasing, with e-commerce platforms influencing product selection and brand penetration. A notable regional player, HiKOKI, continues to expand its high-performance Li-ion tool range, strengthening the competitive landscape.

South America accounted for an estimated 6.1% market share in 2024, with Brazil and Argentina leading demand. The region’s growth is influenced by construction recovery, expansion of energy projects, and increased government-led infrastructure spending. Countries like Brazil are investing in hydroelectric and renewable energy initiatives, driving greater use of industrial fastening and drilling tools. Trade policies promoting industrial modernization have supported wider adoption across manufacturing and utilities. Regional consumer behavior shows a preference for cost-efficient and durable tools due to varying affordability levels. Local manufacturers are increasingly focusing on mid-range tool offerings to meet rising SME demand. The regional market also benefits from growing media and language localization needs, with higher use of digital platforms for procurement and service engagement.

The Middle East & Africa contributed 5.0% of the global market in 2024, driven by strong demand from the oil & gas sector, large-scale construction programs, and industrial modernization efforts. The UAE, Saudi Arabia, and South Africa remain the major growth countries, supported by infrastructure megaprojects and manufacturing diversification agendas. Adoption of technologically advanced and cordless power tools is increasing as industries focus on efficiency, safety, and reduced maintenance cycles. Regional regulators are encouraging trade partnerships and quality compliance, improving access to premium tool brands. A notable regional development includes UAE-based distributors expanding aftersales service networks to support rising demand for professional-grade equipment. Consumer preferences show inclination toward rugged, long-life tools suited for harsh working environments and heavy-duty applications.

United States – 21.2% Market Share: Dominance driven by advanced manufacturing capacity and high enterprise adoption of precision and digitally enabled tools.

China – 18.5% Market Share: Leadership supported by large-scale production ecosystems, expanding construction activity, and extensive domestic consumption across industrial sectors.

The competitive environment in the Industrial Power Tools Market remains moderately consolidated, with roughly 15–20 active global competitors dominating a substantial portion of volume and innovation cycles. The top 5 companies together hold approximately 48–55% of the total market share, reflecting a structure where a few established players lead while many smaller firms and niche manufacturers coexist, creating a balanced yet competitive ecosystem.

Major players are positioning themselves through aggressive product innovation, expansion of manufacturing capacity, and strategic investments. In 2023–2024, several leading firms launched new lines of high-performance cordless and brushless tools, integrating smart diagnostics, battery-management systems, and noise-reduction features to meet evolving industrial requirements. At the same time, there were notable manufacturing expansions and acquisitions to strengthen regional presence and supply chains. These strategic initiatives reflect an industry-wide shift toward energy-efficient, digitally enabled, ergonomic, and sustainable power tool solutions.

Competition is increasingly influenced by technological differentiation — companies that invest in battery technology, IoT connectivity, ergonomic design, and multi-functionality are gaining a competitive edge. At the same time, mid-range and regional players compete largely on price, service, and regional customization. The market thus exhibits a hybrid structure: consolidated at the top with global brands controlling a major share, but also fragmented beneath that level, giving room for agile, niche, or regional manufacturers to carve out specialized segments. Strategic alliances, R&D investments, and product diversification continue to drive competitive intensity.

Hilti

Techtronic Industries (Milwaukee Tool / AEG)

Festool

Snap-on

Metabo HPT

Ingersoll Rand

Atlas Copco

The Industrial Power Tools Market is currently undergoing a transformative technological evolution, shaped by advances in battery technology, digital integration, connectivity, and materials engineering. The widespread shift from corded to cordless lithium-ion battery systems has become a foundational change. Many new tools launched in 2023–2024 now deliver up to 30% longer runtime compared to previous generations, significantly enhancing mobility and operational flexibility in industrial and construction settings. At the same time, brushless motor technology has become standard in high-performance models, offering improved energy efficiency, longer lifespan, and reduced maintenance compared to traditional brushed motors.

Connectivity and smart diagnostics are emerging as differentiators. Increasingly, tools integrate Bluetooth or IoT-enabled modules that allow remote monitoring of usage patterns, torque calibration, maintenance scheduling, and predictive diagnostics. This digital layer aids enterprises in asset management, reduces unplanned downtime, improves safety compliance, and enhances lifecycle management of tools. Another notable trend is ergonomic and user-safety focused design: many new tools are significantly lighter, feature reduced vibration and noise levels, and use composite or recycled materials to meet environmental and occupational health standards.

Multi-functionality is also gaining traction — modular tools that combine drilling, cutting, fastening, and sanding functionalities are increasingly offered as space- and cost-efficient alternatives to maintaining multiple single-purpose tools. This trend is especially relevant for contractors and maintenance teams requiring flexibility on diverse job sites. In addition, some manufacturers are experimenting with smart battery management systems, auto-adjustable torque controls, and tool-user authentication systems to ensure secure, monitored usage in industrial environments.

Overall, the technology trajectory points toward a future where industrial power tools become part of connected, sustainable, and highly efficient manufacturing and construction workflows. Decision-makers are now evaluating tools not purely on power or torque, but on total cost of ownership, lifecycle sustainability, ergonomic safety, and integration within digital maintenance and asset-management platforms.

In April 2024, Stanley Black & Decker completed the sale of its Attachment Tools business to Epiroc AB, restructuring its portfolio to focus on core tooling and engineered fastening operations; the transaction closed on 1 April 2024, optimising the company’s strategic footprint. Source: www.stanleyblackanddecker.com

On 2 October 2024, Bosch Power Tools unveiled a major product rollout — introducing over 30 new tools and expanding its 18V cordless platform with brand-first category innovations designed for professional users and plumbers, strengthening its cordless and digital tool offerings. Source: us.bosch-press.com

In July 2024, Makita expanded its high-voltage XGT ecosystem, releasing new 40V Max XGT five-piece kits and increasing the XGT system to 125+ products during 2024, reinforcing its strategy to serve equipment-grade, battery-powered industrial applications. Source: www.makitatools.com

In H1 2024, Techtronic Industries (TTI) reported US$7.3 billion in first-half 2024 sales (up ~6.3%), noting that MILWAUKEE delivered double-digit sales growth, and the company highlighted balanced regional performance and continued investments in production and R&D. Source: www.ttigroup.com

This Industrial Power Tools Market Report provides a comprehensive analysis spanning multiple dimensions: product types, power sources, applications, end-user segments, and geographical regions. It covers drilling, fastening, cutting, grinding, sawing, and speciality industrial tools — both corded and cordless — with detailed insights into industry-grade and heavy-duty applications. The report examines usage across manufacturing, automotive assembly, aerospace, construction, metal fabrication, energy infrastructure maintenance, and general industrial repair.

Geographically, the report analyzes major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa — highlighting regional demand patterns, technological adoption rates, regulatory environments, and industrial infrastructure trends. It also addresses consumer behavior differences, such as enterprise adoption rates, preference for cordless vs corded tools, ergonomic and sustainability demands, and procurement practices across developed and emerging markets.

Technologically, the report includes analysis of brushless motor adoption, lithium-ion battery systems, IoT and connectivity integration, smart diagnostics, ergonomic design, vibration/noise reduction technologies, and modular multifunction tool trends. Emerging niches such as sensor-enabled tools, digitally monitored maintenance, and multi-function tool kits are explored. Industry focus areas include heavy manufacturing, automotive and aerospace production, renewable energy infrastructure, building and construction, maintenance and repair operations, and modular construction projects.

Furthermore, the report assesses competitive dynamics — including global market leaders, mid-tier and niche regional players — and strategic initiatives such as product launches, manufacturing expansions, R&D investments, and digital-service integration. The scope is designed to provide decision-makers and industry professionals with actionable insights on market segmentation, technological evolution, regional opportunities, end-user behavior, and competitive positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,880.0 Million |

| Market Revenue (2032) | USD 4,353.3 Million |

| CAGR (2025–2032) | 5.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Stanley Black & Decker, Bosch, Makita, Hilti Group, Techtronic Industries (Milwaukee Tool / AEG), Festool, Snap-on, Metabo HPT, Ingersoll Rand, Atlas Copco |

| Customization & Pricing | Available on Request (10% Customization Free) |