Reports

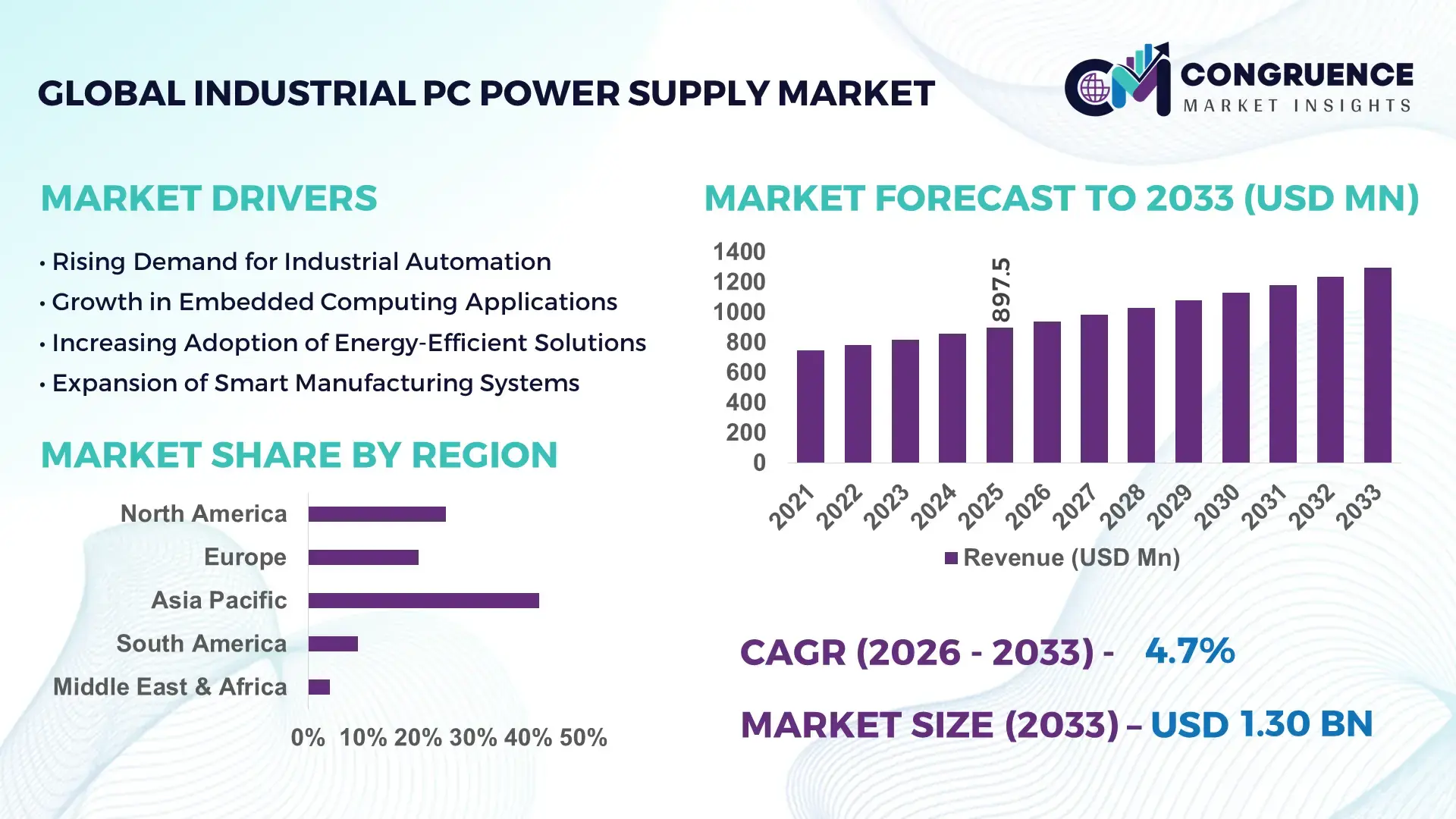

The Global Industrial PC Power Supply Market was valued at USD 897.52 Million in 2025 and is anticipated to reach a value of USD 1296.04 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. Growth is driven by rising automation intensity and demand for reliable power architectures in harsh industrial environments.

China represents the most influential country-level ecosystem within the Industrial PC Power Supply market due to its extensive electronics manufacturing base and large-scale industrial automation deployment. The country hosts more than 30,000 industrial automation manufacturing facilities, with industrial electronics output exceeding USD 2.1 trillion annually. Over 65% of new factory installations integrate industrial PCs with dedicated power supply units designed for high-temperature and vibration tolerance. Annual investments in smart manufacturing infrastructure surpassed USD 180 billion, accelerating adoption of high-efficiency DIN-rail, ATX, and redundant power supplies. Key application clusters include automotive production lines, semiconductor fabs, energy control systems, and logistics automation hubs, where power supplies with MTBF ratings above 500,000 hours and efficiency levels exceeding 92% are increasingly standardized.

Market Size & Growth: USD 897.52 Million (2025) to USD 1296.04 Million (2033) at 4.7% CAGR, supported by rapid industrial digitalization.

Top Growth Drivers: Factory automation adoption +38%, energy efficiency upgrades +26%, industrial IoT integration +31%.

Short-Term Forecast: By 2028, system downtime reduction of 18% through high-reliability power designs.

Emerging Technologies: Wide-input voltage power modules, fanless power supplies, intelligent power monitoring.

Regional Leaders: Asia Pacific USD 512 Million (2033) driven by smart factories; Europe USD 364 Million with energy-efficient retrofits; North America USD 298 Million led by industrial edge computing.

Consumer/End-User Trends: Strong uptake from manufacturing, energy utilities, and transportation automation users.

Pilot or Case Example: 2024 automotive plant upgrade achieved 22% maintenance cost reduction using redundant IPC power systems.

Competitive Landscape: Delta Electronics ~18% share; followed by Mean Well, TDK-Lambda, Siemens, and Phoenix Contact.

Regulatory & ESG Impact: IEC 62368-1 compliance and efficiency mandates accelerating product replacement cycles.

Investment & Funding Patterns: Over USD 1.1 billion invested globally in industrial power electronics modernization since 2023.

Innovation & Future Outlook: Integration of AI-enabled power diagnostics and modular redundancy architectures.

The Industrial PC Power Supply market is shaped by strong demand from manufacturing, energy, transportation, and process industries, with manufacturing contributing approximately 42% of total consumption, followed by energy and utilities at 21% and transportation systems at 17%. Technological advancements such as wide-temperature operation, high-efficiency (>94%) designs, and real-time power health monitoring are redefining product differentiation. Regulatory emphasis on energy efficiency, electromagnetic compatibility, and operational safety is influencing procurement standards globally. Asia Pacific leads consumption growth due to rapid factory automation, while Europe focuses on power-efficient retrofits and North America emphasizes reliability for edge computing environments. Emerging trends include redundant power architectures, compact high-wattage units, and predictive maintenance integration, positioning the market for steady long-term expansion.

The Industrial PC Power Supply Market holds strategic relevance as a foundational enabler of industrial automation, digital manufacturing, and mission-critical computing across factories, energy infrastructure, and transportation systems. Reliable power delivery directly impacts uptime, system lifespan, and operational safety in environments where failure costs can exceed USD 100,000 per hour in high-value manufacturing lines. The shift from conventional ATX power supplies to wide-input, high-efficiency industrial-grade power units illustrates this importance; wide-input DC power architectures deliver up to 28% higher voltage stability compared to legacy fixed-input ATX standards, reducing system faults in fluctuating grid conditions.

From a regional perspective, Asia Pacific dominates in shipment volume due to dense manufacturing clusters, while Europe leads in adoption intensity, with over 62% of industrial enterprises deploying energy-efficient or redundant IPC power supplies aligned with automation upgrades. Strategically, vendors are aligning product roadmaps with AI-enabled diagnostics and predictive maintenance. By 2028, AI-driven power monitoring is expected to reduce unplanned IPC downtime by 20% through early fault detection and load optimization.

Compliance and ESG considerations are becoming central to procurement strategies. Firms are committing to energy efficiency and material sustainability improvements, such as achieving 30% reduction in power losses and 25% recyclable component usage by 2030. In 2024, Germany-based industrial manufacturers achieved a 17% reduction in power-related failures by integrating intelligent power supplies with real-time health analytics across smart factories. Looking ahead, the Industrial PC Power Supply Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term digital transformation across global industries.

Accelerating industrial automation is a primary driver of the Industrial PC Power Supply Market, as automated production lines require continuous, stable power to avoid costly interruptions. Over 70% of new industrial machinery installations now integrate industrial PCs for control, visualization, and data processing, each dependent on high-reliability power supplies. Automated facilities operate with higher equipment density, increasing thermal loads and power quality sensitivity, which elevates demand for fanless, wide-temperature, and high-efficiency power supplies. In automotive and electronics manufacturing, even a 1% reduction in power-related downtime can translate into productivity gains exceeding 3%. The proliferation of robotics, machine vision, and AI-enabled inspection systems further intensifies the need for low-noise, stable power outputs, reinforcing sustained demand for advanced Industrial PC Power Supply solutions.

Higher upfront costs associated with advanced Industrial PC Power Supply systems present a notable restraint, particularly for small and mid-sized manufacturers. Industrial-grade power supplies with redundancy, intelligent monitoring, and extended temperature tolerance can cost 35–50% more than standard commercial-grade alternatives. For cost-sensitive facilities operating legacy equipment, the return on investment horizon may exceed internal budget cycles, delaying upgrades. Additionally, customized power configurations required for specific industrial PCs increase engineering and validation expenses. In regions with less stringent regulatory enforcement, some operators continue using non-industrial power units, despite higher failure risks. These cost pressures slow replacement rates and limit penetration of next-generation power supply technologies in price-competitive industrial environments.

The rapid expansion of industrial edge computing presents significant opportunities for the Industrial PC Power Supply Market. Edge systems deployed near machines and sensors require compact, high-efficiency power supplies capable of operating reliably in harsh conditions. By 2027, more than 55% of industrial data processing is expected to occur at the edge, increasing demand for low-profile, DIN-rail, and DC-DC power supplies with intelligent load management. Energy utilities, smart grids, and logistics hubs are adopting edge-enabled industrial PCs to reduce latency by up to 40%, creating demand for power supplies with built-in surge protection and remote diagnostics. This shift opens new avenues for suppliers offering modular, scalable, and digitally enabled power solutions tailored to decentralized industrial architectures.

Regulatory complexity and thermal management requirements pose ongoing challenges for the Industrial PC Power Supply Market. Compliance with multiple regional standards—including IEC safety norms, EMC directives, and energy efficiency requirements—extends product development and certification timelines by 6–12 months. Simultaneously, increasing power density in compact industrial PCs generates higher thermal stress, particularly in fanless designs. Managing heat dissipation without compromising reliability requires advanced materials and design optimization, raising development costs. Failure to meet thermal and regulatory thresholds can limit market access or result in costly redesigns. These challenges necessitate continuous investment in engineering and compliance capabilities, impacting margins and time-to-market for power supply manufacturers.

• Accelerated Shift Toward Modular and Prefabricated Industrial Systems

The increasing adoption of modular and prefabricated industrial systems is reshaping demand patterns in the Industrial PC Power Supply market. Around 55% of newly commissioned industrial automation and smart factory projects report measurable cost and deployment benefits from modular system designs. Pre-assembled control cabinets and prefabricated automation units require standardized, modular Industrial PC Power Supply configurations to enable faster installation and scalability. Deployment timelines have shortened by nearly 30%, while on-site labor requirements declined by approximately 25%, particularly across Europe and North America. This shift is driving higher demand for plug-and-play, hot-swappable power supplies compatible with modular industrial PC architectures.

• Growing Adoption of High-Efficiency and Wide-Input Voltage Power Supplies

Industrial facilities are increasingly prioritizing energy efficiency and power stability, accelerating the adoption of high-efficiency Industrial PC Power Supply units. More than 60% of newly installed industrial PCs now integrate power supplies rated above 92% efficiency, compared to less than 40% five years ago. Wide-input voltage ranges (typically 9–36V DC or 90–264V AC) are being specified in over 48% of new deployments to mitigate grid instability and voltage fluctuations. These upgrades have demonstrated up to 18% reductions in power-related equipment failures and improved system availability across continuous-process industries.

• Expansion of Fanless and High-Temperature Power Supply Designs

Fanless Industrial PC Power Supply designs are gaining traction due to maintenance reduction and reliability improvements in harsh environments. Approximately 46% of industrial PCs deployed in manufacturing plants now utilize fanless power supplies, up from 31% in recent years. These systems support operating temperature ranges exceeding 70°C, reducing dust ingress and mechanical wear. Field data indicates maintenance intervals extending by nearly 40%, while mean time between failures improves by over 20%. This trend is particularly pronounced in automotive, metal processing, and energy infrastructure applications.

• Integration of Intelligent Monitoring and Predictive Diagnostics

The integration of intelligent monitoring features within Industrial PC Power Supply units is emerging as a critical trend. Around 34% of new industrial power supplies now include built-in voltage, temperature, and load monitoring capabilities. Predictive diagnostics enabled through embedded sensors and digital interfaces have reduced unexpected power-related shutdowns by approximately 22%. In digitally mature factories, real-time power analytics have improved asset utilization rates by 15% and enabled faster fault isolation. This trend reflects growing alignment between power infrastructure and data-driven industrial operations.

The Industrial PC Power Supply market is segmented based on type, application, and end-user, each reflecting distinct demand drivers and usage patterns across industrial environments. By type, the market is shaped by differences in form factor, power redundancy, and efficiency requirements aligned with specific industrial PC architectures. Applications vary widely, ranging from factory automation and process control to energy management and transportation systems, with power reliability and environmental tolerance acting as key differentiators. From an end-user perspective, manufacturing enterprises dominate adoption due to high automation intensity, while energy utilities, transportation operators, and logistics providers are accelerating uptake as digital infrastructure expands. Segmentation insights reveal that buyers increasingly prioritize long lifecycle support, compliance readiness, and modular scalability when selecting Industrial PC Power Supply solutions, indicating a shift from commodity components to strategic infrastructure elements within industrial systems.

The Industrial PC Power Supply market by type includes DIN-rail power supplies, ATX power supplies, redundant power supplies, DC-DC converters, and embedded power modules. DIN-rail power supplies currently account for approximately 38% of total adoption, driven by their compact design, ease of installation, and widespread use in control cabinets for factory automation and energy systems. ATX power supplies follow with nearly 27% adoption, primarily supporting legacy industrial PC platforms and cost-sensitive deployments. However, redundant power supplies represent the fastest-growing type, expanding at an estimated 7.1% annually, as industries prioritize zero-downtime operations in critical environments such as semiconductor fabs and data-driven manufacturing. Growth in this segment is fueled by rising deployment of dual-input and hot-swappable architectures that improve system availability by over 20%. Other types, including DC-DC converters and embedded modules, collectively contribute around 35% of the market, serving niche requirements such as mobile machinery, transportation systems, and compact edge devices.

By application, factory automation represents the leading segment in the Industrial PC Power Supply market, accounting for roughly 41% of total usage. This dominance is supported by high industrial PC density on production lines, where continuous power stability directly influences throughput and quality consistency. Process control applications hold close to 24% adoption, particularly in chemicals, oil and gas, and food processing, where power fluctuations can disrupt safety-critical operations. Transportation and logistics systems are emerging as the fastest-growing application area, expanding at an estimated 6.5% annually, driven by smart rail systems, automated ports, and warehouse robotics requiring ruggedized power supplies. Other applications, including energy management, utilities, and building automation, collectively represent about 35% of demand, benefiting from grid modernization and distributed control systems.

From an end-user perspective, manufacturing enterprises lead the Industrial PC Power Supply market with approximately 46% share, reflecting extensive use of industrial PCs in robotics, machine control, and quality inspection systems. Energy and utilities follow with nearly 21% adoption, driven by substation automation, renewable energy monitoring, and grid control platforms. The fastest-growing end-user segment is logistics and warehousing, expanding at an estimated 6.9% annually, fueled by rapid deployment of automated storage, sorting, and autonomous material handling systems. Transportation authorities and smart city operators, along with healthcare and research facilities, collectively contribute around 33% of total demand, with adoption rates in transportation automation exceeding 28% in digitally advanced regions.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

Asia-Pacific leads due to its dense manufacturing base, with over 60% of global industrial automation equipment installations concentrated across China, Japan, and South Korea. Europe follows closely in value-driven adoption, supported by strict energy efficiency and safety compliance frameworks impacting more than 70% of industrial facilities. North America holds approximately 26% share, driven by high penetration of industrial PCs in manufacturing, healthcare, and critical infrastructure. South America and the Middle East & Africa collectively account for nearly 14%, supported by industrial modernization, energy projects, and logistics automation. Regional disparities are also visible in adoption patterns, with over 58% of enterprises in developed regions prioritizing high-efficiency and redundant Industrial PC Power Supply systems, compared to 34% in emerging markets. These variations underline region-specific regulatory, industrial, and digital transformation dynamics shaping the market.

How is digital industrial resilience shaping power infrastructure investments?

This region accounts for nearly 26% of the Industrial PC Power Supply market, supported by strong demand from manufacturing, healthcare systems, energy utilities, and data-intensive industries. Over 65% of large industrial enterprises operate advanced automation systems requiring high-reliability power supplies. Regulatory initiatives emphasizing equipment safety, cybersecurity, and energy efficiency have accelerated replacement of legacy power units, particularly in pharmaceuticals and critical infrastructure. Digital transformation trends include adoption of edge computing and AI-enabled diagnostics, with more than 40% of new industrial PC installations integrating smart power monitoring. A prominent local player expanded production of fanless, high-efficiency power supplies optimized for harsh environments, reducing maintenance cycles by 30%. Consumer behavior reflects higher enterprise adoption in healthcare and finance-linked industrial operations, where system uptime and compliance are prioritized.

Why is compliance-driven modernization accelerating industrial power upgrades?

Europe holds approximately 24% of the Industrial PC Power Supply market, led by Germany, the UK, and France, which together represent over 68% of regional demand. Regulatory pressure from safety, energy efficiency, and sustainability frameworks has influenced procurement strategies, with nearly 72% of industrial buyers prioritizing certified, high-efficiency power supplies. Sustainability initiatives have driven adoption of power units with efficiency ratings above 93% and recyclable materials exceeding 25%. Emerging technologies such as redundant power architectures and intelligent load balancing are increasingly deployed in smart factories. A leading regional manufacturer introduced modular power platforms aligned with green manufacturing goals, achieving a 15% reduction in power losses. Consumer behavior reflects regulatory-led demand for transparent, compliant, and explainable Industrial PC Power Supply systems.

How is large-scale manufacturing automation sustaining volume leadership?

Asia-Pacific ranks first globally by volume, accounting for around 42% of the Industrial PC Power Supply market. China, Japan, and India are the top consuming countries, collectively representing more than 75% of regional installations. Manufacturing expansion, smart factory programs, and electronics production clusters are key drivers, with over 55% of new factories integrating industrial PCs. Regional innovation hubs focus on compact, cost-efficient, and wide-input voltage power supplies to support high-density deployments. A major regional supplier increased output of DIN-rail power supplies by 20% to meet automation demand from automotive and semiconductor plants. Consumer behavior shows growth driven by e-commerce logistics, robotics, and mobile AI-enabled industrial applications.

What role does infrastructure modernization play in industrial power adoption?

South America accounts for approximately 9% of the Industrial PC Power Supply market, with Brazil and Argentina leading regional demand. Infrastructure upgrades in energy, mining, and transportation are increasing industrial PC deployments, particularly in grid monitoring and process automation. Government incentives targeting industrial modernization and trade facilitation have supported equipment imports and local assembly. Over 38% of new industrial projects incorporate upgraded power infrastructure to address grid instability. A regional electronics manufacturer partnered with automation integrators to supply rugged power units for mining operations, improving system reliability by 18%. Consumer behavior indicates demand tied to localized industrial content, language-specific interfaces, and media-driven logistics operations.

How are industrial diversification and energy projects shaping demand patterns?

The Middle East & Africa region holds close to 5% of the Industrial PC Power Supply market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Oil & gas, construction, and utilities dominate adoption, accounting for over 60% of installations. Industrial diversification initiatives and smart infrastructure investments are driving upgrades to automation-ready power systems. Technological modernization includes integration of industrial PCs in refineries and smart grids, where power reliability improvements of 20% have been recorded. A regional systems integrator deployed redundant power supplies across digital oilfield projects, reducing operational disruptions by 16%. Consumer behavior emphasizes durability and tolerance to extreme environmental conditions.

China – 28% market share: Dominance driven by high industrial production capacity, extensive automation deployment, and large-scale smart factory investments in the Industrial PC Power Supply market.

United States – 21% market share: Strong position supported by advanced industrial digitization, high enterprise adoption of reliable power systems, and regulatory emphasis on operational safety in the Industrial PC Power Supply market.

The Industrial PC Power Supply market exhibits a moderately fragmented competitive structure, characterized by the presence of more than 45 active global and regional manufacturers competing across standardized and customized product segments. The top five companies collectively account for approximately 52% of total market presence, indicating moderate consolidation driven by brand reputation, compliance capabilities, and long-term supply contracts with industrial OEMs. Market leaders maintain strong positioning through broad product portfolios covering DIN-rail, ATX, redundant, and wide-input voltage power supplies, while mid-tier players compete on customization, regional proximity, and cost efficiency.

Strategic initiatives are a defining feature of competition. Over 38% of leading players launched new or upgraded power supply models between 2023 and 2025, focusing on efficiency levels above 93%, fanless designs, and intelligent monitoring features. Partnerships between power supply manufacturers and industrial PC OEMs have increased by nearly 25%, enabling tighter system integration and faster deployment cycles. Mergers and capacity expansions remain selective, with most investments directed toward automation of manufacturing lines, improving output consistency by up to 20%. Innovation trends center on redundant architectures, digital diagnostics, and compliance-ready designs, reinforcing differentiation in reliability-critical industrial environments.

Delta Electronics

Mean Well Enterprises

TDK-Lambda

Siemens

Phoenix Contact

Advanced Energy Industries

Artesyn Embedded Power

Cosel

FSP Group

Murata Power Solutions

XP Power

Weidmüller

Technological advancements are redefining the Industrial PC Power Supply market as power units evolve from basic electrical components into intelligent, high-reliability subsystems integral to industrial digital infrastructure. One of the most impactful developments is the widespread adoption of high-efficiency power conversion technologies, with over 62% of newly deployed industrial PC power supplies now exceeding 92% efficiency. This shift directly reduces thermal losses by nearly 18% and extends component lifecycles, particularly in continuous-operation environments. Wide-input voltage designs, supporting ranges such as 9–36V DC and 90–264V AC, are now specified in approximately 48% of industrial deployments to address grid instability and fluctuating power conditions.

Fanless and conduction-cooled architectures represent another major technological shift, accounting for nearly 46% of new installations. These designs support operating temperatures above 70°C and reduce mechanical failure points, improving mean time between failures by more than 20%. Redundant and hot-swappable power supply technologies are increasingly integrated into mission-critical systems, with dual-input configurations improving system availability by up to 99.99% in automation and energy applications.

Digitalization is further influencing technology adoption through intelligent monitoring and communication interfaces. Around 34% of modern Industrial PC Power Supply units include embedded sensors for voltage, current, and temperature tracking, enabling predictive maintenance and reducing unexpected shutdowns by roughly 22%. Integration with industrial communication protocols allows real-time diagnostics and remote management across distributed facilities. Emerging technologies such as silicon carbide–based components and compact high-density power modules are enabling smaller footprints while supporting higher wattage outputs. Collectively, these technological advancements position Industrial PC Power Supply solutions as strategic enablers of resilient, efficient, and future-ready industrial computing systems.

• In March 2025, TDK-Lambda expanded its industrial power supply lineup with the launch of a 960W DIN-rail mount programmable DC-UPS designed for mission-critical applications, offering enhanced reliability and flexibility for industrial automation systems. (us.lambda.tdk.com)

• In October 2025, TDK-Lambda introduced a 1U high, 13-output modular industrial power supply capable of delivering up to 1500 W with ultra-low acoustic noise, improving configurability and application breadth in compact industrial installations. (us.lambda.tdk.com)

• In November 2025, TDK-Lambda expanded its compact industrial power supply series with new 600 W and 1000 W models optimized for factory automation, semiconductor fabrication, and broadcast equipment, featuring efficiencies up to 95 % and low-noise operation. (us.lambda.tdk.com)

• In December 2024, TDK-Lambda enhanced its 50 W to 150 W HWS-A family with push-in wire terminations, simplifying cable harnessing and increasing installation efficiency for automated manufacturing environments. (us.lambda.tdk.com)

The Industrial PC Power Supply Market Report covers a comprehensive assessment of product, application, and end-user dimensions across global industrial ecosystems. It includes segmentation by product types such as DIN-rail power supplies, redundant supplies, ATX and embedded formats, and DC-DC converters, highlighting performance attributes like efficiency, form factor, temperature tolerance, and digital monitoring capabilities. The report also addresses application areas such as factory automation, process control, transportation systems, energy infrastructure, and edge computing nodes, detailing deployment characteristics and system requirements.

Geographically, the report profiles key regions including Asia-Pacific, North America, Europe, South America, and Middle East & Africa, offering insights into volume consumption, regional priorities, regulatory influences, and infrastructure trends. It includes metrics related to installation densities, enterprise adoption patterns, and technology uptake across primary markets and emerging industrial clusters. The scope extends to technological innovations influencing product design, such as modular architectures, wide-input voltage support, intelligent power monitoring protocols, and ruggedized assemblies for harsh environments.

Additionally, the report examines industry focus areas such as compliance with safety and electromagnetic standards, industrial IoT integration, and digital transformation enablers that shape procurement strategies. Emerging and niche segments—such as power solutions tailored for AI-driven automation, multi-output platforms for complex control systems, and fanless high-temperature units—are also evaluated to provide strategic context for decision-makers. The content is designed to support business professionals in understanding market complexity, competitive positioning, and technology-driven value propositions across the Industrial PC Power Supply landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 4.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Delta Electronics, Mean Well Enterprises, TDK-Lambda, Siemens, Phoenix Contact, Advanced Energy Industries, Artesyn Embedded Power, Cosel, FSP Group, Murata Power Solutions, XP Power, Weidmüller |

Customization & Pricing | Available on Request (10% Customization is Free) |