Reports

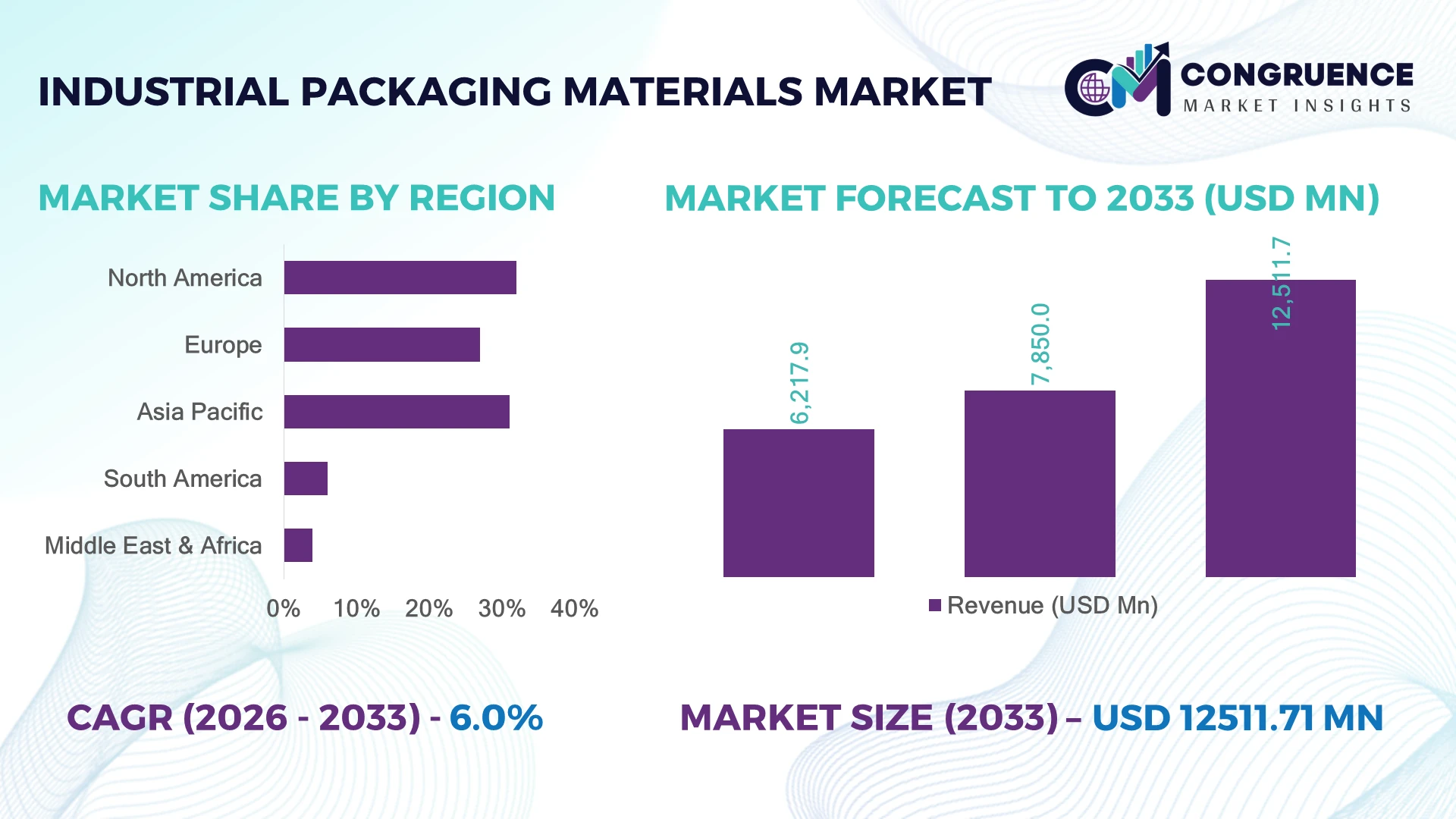

The Global Industrial Packaging Materials Market was valued at USD 7,850.0 Million in 2025 and is anticipated to reach a value of USD 12,511.7 Million by 2033 expanding at a CAGR of 6.0% between 2026 and 2033. Growth is driven by lightweight packaging innovations, automated material handling systems, recycled polymer adoption, and advanced bulk packaging solutions across manufacturing and logistics operations.

The United States holds a leading position with nearly 28% market share, supported by strong chemical, automotive, food processing, and logistics industries, alongside investments of over USD 10 billion in packaging automation and sustainable material infrastructure. China contributes approximately 25% of global production capacity through large industrial manufacturing hubs. Following the supply-chain disruptions after the Russia-Ukraine conflict, companies increased regional packaging resilience investments, with U.S. automation adoption exceeding China by nearly 12%.

Strategic implication: Businesses investing in sustainable materials, digital packaging technologies, and localized production networks will secure stronger operational advantages.

Market Size & Growth: USD 7.85 Billion (2025) to USD 12.51 Billion (2033) at 6.0% CAGR, driven by sustainable packaging innovation and automation.

Top Growth Drivers: 35% recyclable material adoption, 30% supply-chain optimization, 25% industrial automation expansion.

Short-Term Forecast: By 2028, smart packaging systems reduce material waste by 15% and improve efficiency by 20%.

Emerging Technologies: AI-based inspection, IoT tracking, robotics, and advanced bio-materials accelerate industrial packaging transformation.

Regional Leaders: Asia Pacific USD 4.0B with manufacturing expansion, North America USD 3.5B with automation adoption, Europe USD 2.8B with circular packaging initiatives.

Consumer/End-User Trends: 45% of manufacturers prioritize recyclable and reusable industrial packaging formats.

Pilot/Case Example: 2024 automated packaging projects delivered 18% labor reduction and 22% throughput improvement.

Competitive Landscape: Leading suppliers account for ~35% share, including Greif, Amcor, Mondi, International Paper, and Mauser Packaging Solutions.

Regulatory & ESG Impact: Sustainability policies target 30%+ packaging waste reduction through recycling and reuse programs.

Investment & Funding: Over USD 15 billion invested in recycling facilities, automation partnerships, and packaging innovation.

Innovation & Future Outlook: Next-generation materials, smart containers, and circular supply-chain models redefine industrial packaging strategies.

Industrial Packaging Materials Market solutions are gaining momentum across chemical, automotive, pharmaceutical, food, and logistics sectors due to increasing requirements for durable and sustainable packaging formats. Manufacturers are introducing recyclable plastics, fiber-based containers, lightweight bulk packaging, and connected tracking solutions. Around 40% of industrial companies are shifting toward greener packaging systems as global supply chains adapt to stricter environmental standards and operational efficiency requirements.

The Industrial Packaging Materials Market is becoming strategically important as industries prioritize supply-chain resilience, sustainable operations, and efficient material management. Global manufacturing shifts, regional production expansion, and stricter environmental regulations are accelerating investments in recyclable packaging formats and advanced industrial handling solutions.

Technology transformation is creating measurable operational benefits, with automated packaging systems improving throughput by approximately 20% compared with conventional manual processes while lowering labor-related costs by nearly 15%. North America leads in automation-driven packaging deployment, while Asia Pacific maintains stronger production capacity through expanding manufacturing ecosystems. Europe continues to influence innovation through circular economy policies and sustainability-focused packaging standards.

Over the next 2–3 years, companies are expanding investments in smart packaging, reusable transport systems, and digitally connected supply networks. Automotive manufacturers and chemical producers are deploying IoT-enabled containers to improve tracking accuracy and reduce packaging losses. Strategic partnerships between material producers, automation providers, and logistics companies are reshaping industry priorities. Organizations that integrate sustainability, technology, and regional supply-chain strategies will achieve stronger competitive positioning and long-term operational efficiency.

The shift toward sustainable industrial packaging and automated handling systems is accelerating market transformation, with recyclable material usage increasing by nearly 35% and automated packaging adoption reaching over 40% among large manufacturers. Regulatory pressure in countries such as the United States and Germany is driving companies to replace conventional materials with lightweight polymers, fiber-based solutions, and reusable containers. Supply-chain disruptions after the Russia-Ukraine conflict further increased demand for localized packaging production. Companies are responding through recycling facility investments, automation partnerships, and material innovation programs. The strategic advantage lies in reducing waste costs while improving operational consistency across complex manufacturing networks.

Industrial packaging manufacturers face pressure from fluctuating raw material prices, supply dependency, and recycling infrastructure limitations. Polymer and metal packaging inputs have experienced price volatility exceeding 20% in recent years, while recycled material availability remains below 50% in several developing markets. Countries dependent on imported resins and specialty materials face higher production risks during global logistics disruptions. These constraints impact profitability, pricing stability, and expansion timelines for packaging suppliers. Companies are mitigating risks through supplier diversification, regional production facilities, long-term procurement contracts, and investments in alternative materials. The key operational challenge remains balancing sustainable material adoption with cost-efficient manufacturing scalability.

The market is opening new opportunities through smart packaging technologies, advanced materials, and circular economy models. IoT-enabled industrial containers are improving tracking accuracy by more than 25%, while automated packaging platforms deliver efficiency improvements of nearly 20% across high-volume operations. Countries such as India and Vietnam are emerging as attractive manufacturing hubs due to expanding industrial infrastructure and export-oriented production. Policy initiatives supporting recycled materials and waste reduction are encouraging investment in bio-based polymers and reusable packaging systems. Companies are strengthening their positions through R&D partnerships, technology integration, and ecosystem development. A major opportunity lies in combining digital visibility with sustainable packaging design to optimize industrial logistics.

Industrial packaging companies face execution challenges related to technology integration, workforce capability, and inconsistent recycling infrastructure. Approximately 30% of manufacturers report difficulties integrating smart tracking systems with existing logistics platforms, while skilled automation workforce shortages affect deployment speed in emerging industrial markets. Countries with fragmented recycling networks continue to experience challenges in achieving circular packaging targets. These barriers influence scalability, sustainability performance, and long-term competitiveness. Companies are addressing these issues through workforce training, strategic technology partnerships, and investment in localized recycling ecosystems. The critical requirement is building interoperable packaging platforms that support efficiency, environmental compliance, and reliable global supply-chain operations.

Smart Packaging Integration Growth Industrial packaging is shifting toward IoT-enabled containers, digital tracking, and connected logistics systems, with adoption rising by nearly 25% among large-scale manufacturers. Companies are deploying RFID, sensors, and cloud-based monitoring to improve asset visibility, reduce losses by around 15%, and strengthen inventory control. Supply-chain disruptions after 2022 accelerated investments in real-time packaging intelligence, especially across automotive and chemical industries.

Circular Material Transformation Sustainable packaging models are expanding as manufacturers increase recycled polymer, fiber-based, and reusable material usage by nearly 35%. Regulations targeting packaging waste reduction in countries such as Germany and Japan are accelerating material redesign and closed-loop systems. Companies are restructuring procurement strategies, partnering with recycling providers, and expanding low-carbon packaging portfolios to meet environmental compliance requirements.

Automation-Driven Production Scaling Industrial packaging facilities are increasing automation deployment, with robotic handling and automated filling systems improving throughput by approximately 20% and reducing labor dependency by nearly 15%. Manufacturing hubs in the United States and China are prioritizing automated packaging lines to address workforce shortages and improve production consistency. Companies are investing in robotics partnerships and smart factory integration.

Lightweight Material Innovation Shift Packaging producers are adopting lightweight plastics, composite materials, and advanced fiber solutions to reduce material consumption by nearly 18% while maintaining durability. Rising transportation costs and sustainability targets are encouraging industries to redesign bulk containers and protective packaging formats. Companies are expanding R&D programs to develop high-strength materials that improve logistics efficiency and reduce environmental impact.

Flexible packaging materials represent the leading segment due to their lightweight structure, cost efficiency, and adaptability across chemicals, food processing, pharmaceuticals, and logistics applications. Flexible industrial packaging accounts for nearly 40% of material usage, supported by reduced transportation costs and improved storage efficiency. Rigid packaging materials, including drums, containers, and crates, maintain strong demand due to durability requirements in heavy industries. The fastest-growing type is sustainable and recyclable packaging materials, driven by corporate ESG targets and regulatory pressure. Adoption of recycled polymers and bio-based materials is increasing by approximately 30%, while manufacturers are investing in advanced barrier technologies to improve performance. Metal and wooden packaging continue serving specialized industrial applications where strength and reuse capability remain critical. Companies are shifting product strategies toward hybrid materials, recyclable designs, and customized solutions to balance performance, compliance, and operational costs.

Chemical packaging is the leading application segment due to strict safety requirements, hazardous material handling standards, and high-volume industrial usage. Drums, intermediate bulk containers, and specialized containers represent nearly 35% of industrial packaging demand in chemical supply chains. Food and beverage applications continue expanding through improved protective packaging, while pharmaceutical usage is increasing through secure and traceable packaging solutions. The fastest-growing application is logistics and transportation packaging, supported by warehouse automation, e-commerce supply networks, and reusable transport systems. Adoption of smart tracking solutions in logistics packaging is increasing by approximately 25%, enabling better asset management and reducing packaging losses. Automotive manufacturers are also increasing investment in returnable packaging systems to improve supply-chain efficiency. Companies are adapting through automation integration, customized packaging designs, and partnerships with logistics providers to strengthen operational reliability.

Manufacturing industries represent the leading end-user segment due to extensive requirements across automotive, chemicals, machinery, and industrial goods transportation. Large manufacturers contribute nearly 45% of industrial packaging consumption as they require durable, standardized, and high-volume packaging solutions. Chemical producers and automotive suppliers maintain strong demand because of safety compliance, component protection, and global distribution requirements. The fastest-growing end-user group is logistics and warehousing companies, driven by automation, inventory optimization, and expanding cross-border supply networks. Adoption of smart packaging solutions among logistics operators is increasing by nearly 25%, enabling improved tracking and reduced handling inefficiencies. Small and medium enterprises are also increasing usage of flexible and cost-efficient packaging formats. Companies are targeting these segments through customized solutions, digital services, long-term supply agreements, and integrated packaging-management platforms.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America captured approximately 32% of the global market share in 2025, supported by advanced manufacturing, chemical processing, automotive production, and logistics infrastructure. The United States represents the regional core, with high adoption of automated packaging systems and sustainable material solutions across enterprise operations. More than 40% of large industrial facilities have integrated automated packaging workflows to improve efficiency and reduce handling costs. Companies are expanding recycling facilities, investing in smart packaging technologies, and forming partnerships with logistics providers to improve operational reliability.

United States Market Outlook: The United States remains the dominant national market due to its extensive industrial base, strong packaging innovation ecosystem, and advanced automation infrastructure. The country accounts for nearly 28% of global industrial packaging demand, driven by chemical, automotive, and food manufacturing sectors. Enterprises are increasingly adopting reusable containers, digital tracking systems, and lightweight materials to optimize industrial supply chains.

Europe accounted for approximately 27% of the global market share in 2025, supported by strict sustainability regulations, advanced recycling infrastructure, and strong industrial manufacturing capabilities. Countries including Germany, France, and Italy are accelerating adoption of recyclable polymers, fiber-based packaging, and reusable transport systems. Nearly 35% of industrial packaging users are prioritizing sustainable materials due to environmental compliance requirements. Companies are restructuring packaging portfolios through circular economy initiatives, recycling partnerships, and material innovation programs to meet evolving regulatory expectations.

Germany Market Outlook: Germany leads the European market through its strong automotive, chemical, and engineering industries. The country’s industrial sector has increased investment in automated packaging systems and resource-efficient materials, with more than 30% of large manufacturers adopting sustainable packaging practices. Strong industrial infrastructure and technology-focused production facilities continue to support market expansion.

Asia-Pacific represents approximately 31% of the global market share in 2025, driven by large-scale manufacturing, expanding export activities, and rapid industrial infrastructure development. China, India, Japan, and South Korea remain key contributors due to strong automotive, electronics, chemical, and logistics sectors. China contributes nearly 25% of global production capacity, while India is expanding packaging manufacturing through industrial corridor development and supply-chain investments. Companies are increasing investments in automation, local production facilities, and sustainable packaging technologies to support high-volume operations.

China Market Outlook: China maintains a leading position through its extensive manufacturing ecosystem, export-oriented industries, and established packaging production capabilities. The country supports nearly one-quarter of global industrial packaging output, with strong demand from chemicals, machinery, and consumer goods manufacturing. Companies are upgrading factories with robotics, smart logistics systems, and recyclable material solutions to improve production efficiency.

South America accounts for approximately 6% of the global market share in 2025, supported by mining, agriculture, food processing, and manufacturing activities. Brazil represents the regional hub due to its large industrial base and growing logistics requirements. Packaging modernization is increasing as companies improve transportation efficiency and adopt more durable industrial containers. Nearly 20% of major industrial operators are investing in improved packaging processes to reduce material losses and operational inefficiencies. Businesses are strengthening local partnerships and improving supply networks to address infrastructure limitations.

Brazil Market Outlook: Brazil leads South America through its agricultural exports, mining operations, and industrial manufacturing base. The country is experiencing increased adoption of bulk packaging solutions and reusable transport systems, particularly across food and chemical industries. Companies are investing in localized production capabilities to improve supply reliability and reduce dependence on imported packaging materials.

The Middle East & Africa region represents approximately 4% of the global market share in 2025, supported by infrastructure development, energy-sector activity, manufacturing expansion, and logistics investments. Countries across the region are improving industrial packaging capabilities to support chemical, construction, food, and export industries. Packaging automation adoption is increasing by nearly 15% among large industrial facilities as companies focus on productivity improvement. Businesses are expanding local manufacturing partnerships and investing in sustainable packaging solutions to support industrial diversification strategies.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a significant industrial packaging market due to investments in petrochemicals, manufacturing, and logistics infrastructure under economic diversification initiatives. The country’s industrial expansion is increasing demand for bulk containers, drums, and specialized packaging formats. Companies are adopting advanced packaging systems and sustainable materials to support growing domestic production and export activities.

The Industrial Packaging Materials Market features competition between global packaging leaders such as Amcor, International Paper, Mondi, Greif, and regional manufacturers specializing in cost-efficient production. The top five players collectively control approximately 35% of market activity, creating a moderately consolidated structure. Competition is driven by material innovation, pricing efficiency, supply reliability, customization, and sustainability capabilities. Leading companies invest heavily in recycled materials, automation, and digital tracking, with sustainable packaging adoption increasing by nearly 30% across industrial buyers. Global leaders compete through acquisitions, recycling infrastructure expansion, and integrated supply networks, while regional suppliers compete through lower costs and faster customization. The competitive landscape is shifting toward circular packaging models, smart containers, and localized manufacturing following supply-chain disruptions. High capital requirements, technical expertise, and customer qualification processes create entry barriers. Winning companies will combine scalable production, advanced materials, and resilient supply-chain capabilities.

International Paper Company

Mondi Group

Greif, Inc.

Mauser Packaging Solutions

Berry Global Group, Inc.

Smurfit Westrock plc

Sonoco Products Company

DS Smith plc

Schütz GmbH & Co. KGaA

Huhtamaki Oyj

Nefab Group

Packaging Corporation of America

Orora Limited

Industrial packaging technology is shifting toward automation, smart monitoring, and sustainable material engineering. Automated packaging lines using robotics and AI-based inspection improve production efficiency by nearly 20% compared with conventional manual processes. IoT-enabled containers and RFID tracking systems are gaining adoption among logistics-intensive industries, improving asset visibility by approximately 25% and reducing handling losses.

Advanced materials are becoming a competitive differentiator as manufacturers introduce lightweight polymers, recyclable composites, and fiber-based alternatives. Compared with traditional packaging materials, lightweight solutions reduce material consumption by nearly 15% while maintaining industrial durability. Companies benefiting most are integrated suppliers combining material science with digital manufacturing capabilities.

Between 2026 and 2028, smart packaging platforms, predictive analytics, and circular material systems will become central to industrial operations. Large manufacturers are increasing deployment of connected packaging solutions to improve inventory accuracy, reduce waste, and strengthen supply-chain control. Companies adopting these technologies early will gain advantages through lower operating costs, faster logistics coordination, and stronger sustainability performance.

October 2025, Amcor plc released its FY25 sustainability update highlighting progress after completing its combination with Berry Global. The company strengthened circular packaging capabilities, expanded responsible material solutions, and positioned its larger global platform to accelerate recyclable packaging innovation. Source: www.amcor.com

April 2025, Mondi Group completed the acquisition of Schumacher Packaging’s Western Europe operations, expanding its corrugated packaging portfolio and production footprint. The transaction strengthened regional capacity and improved its ability to serve customers through integrated sustainable packaging solutions.

May 2025, International Paper Company began construction of its Waterloo, Iowa corrugated box plant, its largest greenfield box facility. The project introduced advanced manufacturing capabilities focused on sustainable packaging production, strengthening North American supply-chain capacity for industrial customers.

May 2025, International Paper Company announced facility alignment initiatives in the Rio Grande Valley, including investments to modernize operations and improve regional capabilities. The restructuring enhanced production efficiency and supported a more competitive packaging network across North America.

The Industrial Packaging Materials Market Report provides comprehensive coverage across major material types, including flexible packaging, rigid containers, metal packaging, paper-based solutions, and sustainable alternatives. The analysis evaluates applications across chemicals, food and beverage, pharmaceuticals, automotive, logistics, and manufacturing sectors, while assessing end-user adoption patterns across industrial enterprises. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level insights.

The report examines automation, smart packaging, recyclable materials, IoT-enabled tracking, and advanced manufacturing technologies shaping industry transformation. It highlights competitive positioning, strategic investments, supplier capabilities, and emerging opportunities. Covering market developments from 2026 to 2033, the study supports investment decisions, expansion planning, partnership strategies, and long-term competitive positioning for companies operating across industrial packaging ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 7,850 Million |

| Market Revenue (2033) | USD 12,511.7 Million |

| CAGR (2026–2033) | 6.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Amcor plc; International Paper Company; Mondi Group; Greif, Inc.; Mauser Packaging Solutions; Berry Global Group, Inc.; Smurfit Westrock plc; Sonoco Products Company; DS Smith plc; Schütz GmbH & Co. KGaA; Huhtamaki Oyj; Nefab Group; Packaging Corporation of America; Orora Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |