Reports

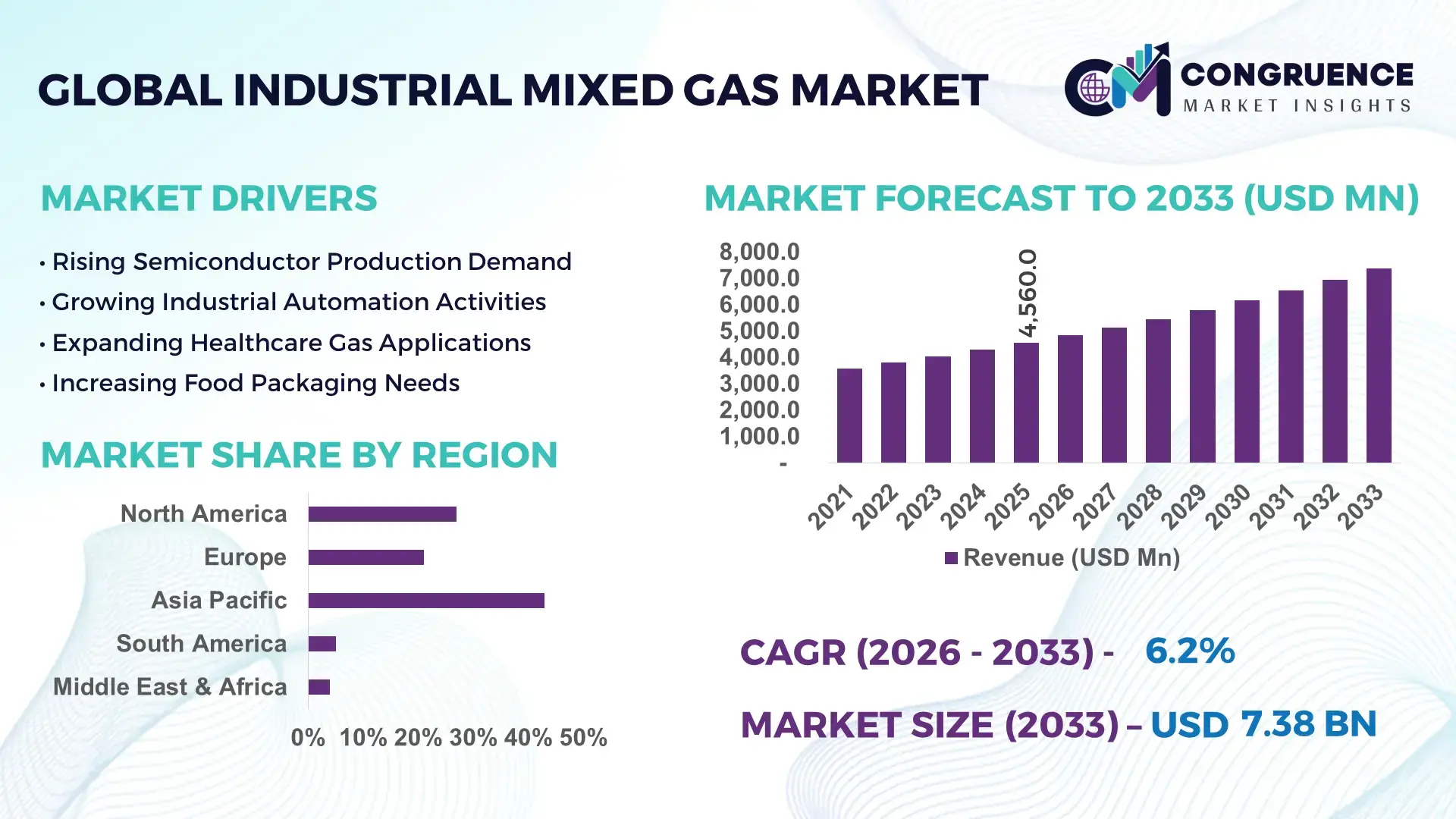

The Global Industrial Mixed Gas Market was valued at USD 4,560.0 Million in 2025 and is anticipated to reach a value of USD 7,378.4 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. The market is accelerating due to rapid adoption of precision gas blending systems across semiconductor fabrication, automated welding, pharmaceutical processing, and hydrogen-based manufacturing, where advanced mixed-gas integration improves process consistency by over 27% while reducing material wastage by nearly 18%. Between 2024 and 2026, industrial gas supply chains experienced major restructuring following the Russia–Ukraine conflict and tightening European emissions regulations, forcing manufacturers to regionalize production, secure long-term helium and argon sourcing contracts, and invest aggressively in localized gas storage infrastructure.

China dominates the global Industrial Mixed Gas Market with approximately 35% of global production capacity, supported by large-scale investments in semiconductor manufacturing, steel processing, and electronics assembly. More than 48 industrial gas separation and blending projects were expanded across China during 2024–2025, while high-purity specialty gas demand in the country increased by 32% due to domestic chip fabrication expansion. Compared with Europe, where energy-intensive gas operations face higher operating costs and stricter carbon controls, China maintains nearly 20% lower production costs through vertically integrated manufacturing ecosystems and stable feedstock access. Meanwhile, the United States leads in advanced industrial mixed gas innovation for aerospace and healthcare applications, accounting for nearly 29% of global specialty gas technology deployments.

As advanced manufacturing, clean-energy infrastructure, and automated industrial processing continue transforming global production ecosystems, companies investing in high-purity gas blending technologies, resilient regional supply networks, and AI-enabled process optimization are securing stronger long-term industrial competitiveness.

Market Size & Growth: USD 4,560.0 million in 2025 reaching USD 7,378.4 million by 2033, driven by semiconductor and precision manufacturing expansion.

Top Growth Drivers: Semiconductor gas demand rose 32%, automated welding adoption increased 24%, and hydrogen-processing integration expanded 19%.

Short-Term Forecast: By 2028, AI-enabled gas systems will reduce operational waste by 26% and improve blending accuracy by 21%.

Emerging Technologies: Smart sensors, automated gas mixing, and membrane separation systems improved purity efficiency by over 18%.

Regional Leaders: Asia-Pacific holds 43% demand share, North America leads specialty gas innovation, while Europe accelerates low-emission industrial adoption.

Consumer/End-User Trends: Over 41% of manufacturers shifted toward customized mixed-gas solutions for precision operations and energy optimization.

Pilot/Case Example: In 2025, automated gas deployment in automotive welding reduced downtime by 22% and improved weld consistency by 29%.

Competitive Landscape: Top five companies control nearly 54% share, led by Linde, Air Liquide, Air Products, Messer, and Nippon Sanso.

Regulatory & ESG Impact: Emission-focused gas optimization programs lowered industrial carbon intensity by nearly 16% across European facilities.

Investment & Funding: More than USD 1.4 billion was allocated toward regional gas infrastructure and specialty gas expansion projects during 2025.

Innovation & Future Outlook: Hydrogen-compatible mixed gases and AI-controlled purity systems are reshaping advanced global industrial processing ecosystems.

Electronics manufacturing contributes nearly 34% of total Industrial Mixed Gas Market demand, followed by metal fabrication at 26% and healthcare processing at 14%. Recent innovations include AI-driven gas blending systems and ultra-high-purity specialty gas cylinders that improve operational precision by over 20%. Asia-Pacific accounts for approximately 43% of global demand due to large-scale manufacturing concentration, while North America leads aerospace-grade gas innovation. Tightening emission regulations and post-pandemic supply-chain restructuring are accelerating localized production strategies and strategic storage investments. The market is steadily shifting toward intelligent, low-emission, and highly customized industrial gas ecosystems that will define the next phase of competitive industrial manufacturing.

The Industrial Mixed Gas Market has become a critical competitive layer for advanced manufacturing, semiconductor fabrication, clean-energy processing, aerospace engineering, and pharmaceutical production because industrial performance increasingly depends on precision-controlled gas environments rather than conventional bulk gas delivery. Manufacturers are aggressively optimizing production lines through customized mixed-gas systems capable of improving process stability, reducing contamination risks, and enhancing automation efficiency across high-value industrial operations.

Global supply-chain fragmentation, export-control policies, and tightening emissions standards are accelerating regional gas infrastructure investments and forcing companies to redesign sourcing strategies for helium, argon, hydrogen, and specialty gas blends. AI-enabled gas blending technology improves operational efficiency by 28% while reducing calibration and wastage costs by 19% compared to legacy manual gas control systems. Asia-Pacific leads in production volume due to large-scale electronics and heavy manufacturing concentration, while North America leads in advanced adoption and innovation with nearly 31% share of specialty gas automation deployments. Over the next three years, automated industrial gas management systems are projected to reduce production downtime by 24% and improve precision manufacturing throughput by 22%. ESG-driven gas recycling and recovery systems are also becoming a competitive advantage, lowering industrial gas losses by nearly 17% while helping manufacturers comply with stricter carbon-efficiency frameworks and cross-border procurement standards.

A major automotive fabrication facility in South Korea improved robotic welding efficiency by 26% after integrating AI-assisted mixed-gas optimization across its assembly operations. Simultaneously, leading industrial gas companies are shifting capital allocation toward semiconductor-grade specialty gases, localized storage hubs, and hydrogen-ready blending infrastructure to secure strategic supply resilience. The Industrial Mixed Gas Market is no longer operating as a supporting industrial utility segment; it is transforming into a strategic manufacturing control layer where companies that secure supply stability, advanced purity technologies, and intelligent blending capabilities will dominate future industrial competitiveness and operational scalability.

The Industrial Mixed Gas Market is undergoing rapid structural transformation as industrial automation, precision manufacturing, and clean-energy processing redefine gas utilization standards across global production ecosystems. Industrial mixed gases are increasingly integrated into semiconductor fabrication, metal processing, electronics assembly, healthcare sterilization, food preservation, and hydrogen-based industrial applications where operational precision and purity consistency directly affect output quality and manufacturing efficiency. The market is being reshaped by tighter environmental regulations, regional supply-chain restructuring, and rising investments in localized gas blending infrastructure. Manufacturers are aggressively deploying AI-enabled gas monitoring systems, automated blending platforms, and high-purity specialty gas solutions to improve production reliability and reduce process inefficiencies. Asia-Pacific continues dominating large-scale industrial consumption, while North America and Europe are accelerating innovation in low-emission and specialty-grade gas technologies. Simultaneously, geopolitical supply constraints surrounding helium and rare gas sourcing are forcing companies to diversify procurement strategies and secure long-term supply agreements. Industrial mixed gas providers are increasingly competing through customization capabilities, purity control, delivery speed, and integrated digital monitoring solutions, reshaping the competitive structure of the global industrial gas ecosystem.

The rapid expansion of advanced manufacturing and automated production systems is becoming the primary growth engine for the Industrial Mixed Gas Market. Semiconductor fabrication facilities increased specialty gas consumption by nearly 32% during 2024–2025, while robotic welding operations using argon-based mixed gases expanded by approximately 24% across automotive and heavy engineering sectors. Industrial manufacturers are increasingly demanding customized gas compositions capable of improving precision, lowering contamination rates, and optimizing thermal performance during high-speed automated production processes. Global supply-chain diversification following geopolitical disruptions and export-control restrictions has accelerated regional manufacturing investments, particularly across Asia-Pacific and North America. This shift is forcing industrial gas suppliers to expand localized blending facilities and secure stable sourcing partnerships for helium, argon, nitrogen, and hydrogen-based gas mixtures. In response, major industrial gas companies are increasing capital deployment toward AI-enabled blending systems, modular storage infrastructure, and integrated digital monitoring platforms. The direct impact is measurable: manufacturers deploying automated gas management systems are reducing operational waste by nearly 18% while improving production consistency by more than 25%. Companies are responding through strategic partnerships with semiconductor, aerospace, and automotive manufacturers to secure long-term supply agreements and strengthen operational resilience across critical industrial sectors.

The Industrial Mixed Gas Market faces significant structural constraints due to volatile raw material availability, energy-intensive production requirements, and concentrated global sourcing networks for specialty gases such as helium and neon. More than 55% of global helium supply remains concentrated within a limited number of production regions, exposing industrial gas manufacturers to geopolitical instability, transportation bottlenecks, and sudden pricing fluctuations. Energy costs for cryogenic gas separation and purification processes increased by nearly 21% across parts of Europe during recent energy market disruptions, directly pressuring industrial operating margins. These limitations are constraining scalability for smaller industrial gas suppliers and increasing procurement complexity for semiconductor and healthcare manufacturers that depend on uninterrupted high-purity gas availability. Infrastructure gaps in emerging economies are also slowing advanced gas distribution and storage deployment, extending industrial project timelines by approximately 14% in several high-growth manufacturing regions. To mitigate these risks, companies are aggressively diversifying sourcing channels, signing multi-year supply agreements, and investing in gas recycling technologies capable of reducing fresh gas dependency by nearly 16%. Industrial gas providers are also accelerating localized storage development and alternative sourcing partnerships to reduce vulnerability to supply concentration and transportation disruptions.

The integration of AI-driven gas management systems and hydrogen-compatible industrial infrastructure is creating high-impact opportunities across the Industrial Mixed Gas Market. Smart gas blending platforms equipped with real-time monitoring and automated calibration capabilities are improving industrial process accuracy by nearly 27% while lowering gas consumption inefficiencies by approximately 19%. These technologies are rapidly gaining traction across semiconductor fabrication, pharmaceutical sterilization, and advanced metal processing environments where precision control directly affects operational profitability. Hydrogen-based industrial transformation is also unlocking new demand pockets for customized mixed gases used in fuel processing, energy storage, and low-emission manufacturing systems. Industrial facilities transitioning toward hydrogen-ready operations increased by nearly 23% during 2025, particularly across Europe and East Asia where emission reduction mandates are accelerating clean-energy industrialization. A non-obvious competitive advantage is emerging through gas recovery and recycling ecosystems, where manufacturers are reducing procurement dependency while improving compliance performance simultaneously. Industrial gas companies are positioning for long-term dominance through R&D investments, regional expansion strategies, and ecosystem partnerships focused on intelligent blending infrastructure, digital gas analytics, and modular specialty gas distribution systems capable of supporting future high-purity industrial operations.

The Industrial Mixed Gas Market faces critical execution challenges related to infrastructure scalability, specialty gas transportation, regulatory compliance complexity, and advanced purity-control requirements. High-purity industrial applications now require contamination thresholds below 10 parts per million in semiconductor and aerospace environments, significantly increasing operational complexity and quality-control costs. At the same time, specialized cryogenic transportation and storage systems can raise logistics expenses by nearly 18% across geographically fragmented supply chains. Power-intensive gas separation operations are also encountering pressure from energy grid instability and carbon-reduction mandates, particularly in Europe and parts of Asia where industrial facilities are being forced to modernize production systems rapidly. Delays in permitting and industrial infrastructure expansion have slowed gas facility deployment timelines by approximately 15% in several emerging manufacturing zones. These pressures are directly affecting long-term scalability and operational consistency for industrial gas suppliers attempting to meet rapidly evolving demand from semiconductor, healthcare, and clean-energy sectors. To remain competitive, companies must accelerate investment in digital monitoring systems, energy-efficient purification technologies, and regionalized production networks while simultaneously building strategic partnerships that strengthen supply resilience and advanced manufacturing integration.

34% Increase in AI-Controlled Gas Blending Deployments Across Precision Manufacturing Facilities: Industrial manufacturers are rapidly replacing manual gas calibration systems with AI-enabled blending platforms capable of improving mixture accuracy by 27% and reducing process downtime by 18%. Semiconductor and aerospace producers are integrating predictive monitoring tools directly into production lines, while industrial gas suppliers are restructuring service models around automated purity optimization and remote diagnostics capabilities.

22% Shift Toward Regionalized Gas Storage and Distribution Networks Following Supply-Chain Disruptions: Industrial gas companies are accelerating localized storage hub development and decentralized blending operations to minimize transportation risk and delivery volatility. Europe and North America expanded regional specialty gas reserves by nearly 19% during 2025, while manufacturers prioritized dual-sourcing contracts to stabilize helium and argon supply continuity under geopolitical and logistics pressure.

29% Growth in Hydrogen-Compatible Mixed Gas Integration Across Heavy Industrial Operations: Steel processing, energy infrastructure, and automotive facilities are increasingly adopting hydrogen-ready gas mixtures to support lower-emission industrial processing. Industrial operators deploying advanced hydrogen-compatible systems improved thermal efficiency by approximately 16% while reducing process-related emissions by 14%, forcing suppliers to scale specialized blending and storage capabilities rapidly.

18% Expansion in Subscription-Based Industrial Gas Management Contracts Reshaping Commercial Models: Industrial buyers are shifting from conventional bulk purchasing toward long-term performance-based gas supply agreements that bundle monitoring, analytics, maintenance, and purity optimization services. This transition is reducing unexpected supply interruptions by 21% and improving operational planning accuracy, while industrial gas providers strengthen customer retention through integrated digital infrastructure and predictive service ecosystems.

The Industrial Mixed Gas Market is segmented across type, application, and end-user categories, with demand distribution increasingly shifting toward high-purity and application-specific gas mixtures designed for advanced industrial precision. Semiconductor manufacturing, metal fabrication, healthcare processing, chemicals, and electronics production continue driving large-scale mixed gas adoption due to strict operational purity and efficiency requirements. Customized industrial gas solutions now account for nearly 44% of industrial processing demand as manufacturers prioritize automation compatibility and lower process variability. Demand concentration remains strongest in high-volume manufacturing sectors, while growth is accelerating across clean-energy processing and semiconductor applications where specialized gas compositions directly improve operational consistency and contamination control. Companies are strategically repositioning product portfolios toward intelligent gas blending systems, AI-enabled monitoring platforms, and localized distribution infrastructure to capture rising demand for precision-driven industrial operations. Simultaneously, industrial buyers are shifting toward long-term supply partnerships focused on supply resilience, purity assurance, and integrated technical support, reshaping procurement strategies and competitive positioning across the global Industrial Mixed Gas Market.

High-purity industrial mixed gases dominate the Industrial Mixed Gas Market with approximately 46% share due to their critical role in semiconductor fabrication, aerospace engineering, pharmaceutical sterilization, and advanced electronics manufacturing. Their structural dominance is driven by superior contamination control, consistent chemical stability, and compatibility with automated production systems where even minor purity deviations can disrupt manufacturing output. In contrast, specialty reactive gas mixtures are emerging as the fastest-growing category, expanding adoption by nearly 24% due to rising hydrogen-processing applications, advanced welding systems, and precision chemical manufacturing requirements. The market is increasingly witnessing a transition from standard inert gas mixtures toward customized specialty blends optimized for industry-specific operational requirements. Compared with conventional argon-nitrogen blends used in traditional fabrication, high-purity reactive mixtures deliver nearly 21% better thermal efficiency and significantly lower process defect rates in precision manufacturing environments. Meanwhile, calibration gases, medical gas mixtures, and food-grade gas blends collectively account for around 32% of total market demand, maintaining strong niche relevance across healthcare, laboratory, and packaging operations. Industrial gas providers are aggressively expanding specialty gas blending facilities, investing in automated purification technologies, and developing AI-enabled gas composition systems to strengthen competitive positioning. Demand is clearly shifting toward premium, application-specific gas solutions, making advanced purity-control technologies and localized production infrastructure the most strategic investment focus areas.

Metal fabrication and welding applications continue dominating the Industrial Mixed Gas Market with nearly 38% share due to extensive usage across automotive manufacturing, shipbuilding, aerospace assembly, and heavy engineering operations. Demand concentration remains high because mixed gases significantly improve welding penetration, arc stability, and production consistency while lowering material wastage during automated fabrication processes. Semiconductor and electronics manufacturing represent the fastest-growing application segment, with adoption increasing by approximately 28% as advanced chip fabrication facilities require ultra-high-purity gas mixtures for precision etching, deposition, and contamination-sensitive operations. Traditional fabrication processes using standard shielding gases are increasingly being replaced by intelligent mixed-gas systems capable of optimizing thermal performance and automated production accuracy. Compared with mature welding applications, semiconductor gas deployments require significantly stricter purity thresholds and integrated digital monitoring systems, driving higher-value infrastructure investments. Chemical processing, healthcare sterilization, and food packaging applications collectively contribute nearly 34% of market demand, supported by rising industrial automation and process safety requirements. Industrial gas companies are repositioning operational strategies around high-purity specialty gas production, integrated logistics systems, and customized industrial service agreements to capture evolving application demand. The strongest market momentum is shifting toward precision-driven applications where operational consistency, emission optimization, and contamination control directly influence industrial productivity and regulatory compliance.

Manufacturing industries remain the leading end-user segment in the Industrial Mixed Gas Market, accounting for approximately 49% of global demand due to continuous consumption across automotive, electronics, heavy engineering, and metal processing operations. Demand concentration is strongest among high-volume industrial manufacturers that rely on stable gas compositions to maintain welding precision, thermal control, and automated production consistency. Meanwhile, the healthcare and pharmaceutical sector is emerging as the fastest-growing end-user group, with adoption increasing by nearly 22% as sterilization systems, laboratory processing, and medical gas applications expand globally.mCompared with mature industrial manufacturing demand, healthcare-focused gas applications require higher regulatory compliance standards, specialized packaging systems, and advanced purity verification technologies. Energy, chemicals, food processing, and research institutions collectively represent nearly 33% of total market consumption, driven by rising investments in hydrogen infrastructure, controlled-atmosphere processing, and advanced analytical operations.mIndustrial gas providers are increasingly targeting end-users through customized supply agreements, predictive maintenance services, and sector-specific blending technologies designed to improve operational reliability and reduce downtime. Companies prioritizing specialized gas solutions, integrated monitoring capabilities, and localized technical support are capturing stronger long-term customer retention across rapidly evolving industrial ecosystems.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Asia-Pacific continues leading global industrial mixed gas consumption due to large-scale semiconductor fabrication, electronics manufacturing, automotive production, and expanding industrial infrastructure across China, Japan, South Korea, and India. North America accounts for nearly 27% of total market demand and leads in advanced specialty gas innovation, AI-enabled blending technologies, and aerospace-grade gas applications. Europe holds approximately 21% share, driven by low-emission industrial transformation and strict industrial compliance standards. Meanwhile, South America and the Middle East & Africa collectively contribute 9% of global demand as industrial modernization and energy-sector expansion accelerate. Regional competition is increasingly shaped by supply-chain localization, strategic storage investments, and high-purity gas production capabilities, pushing global companies toward regionalized expansion strategies.

North America accounts for approximately 27% of global Industrial Mixed Gas Market demand, supported by strong aerospace, semiconductor, healthcare, and automated manufacturing activity across the United States and Canada. Semiconductor fabrication expansion and advanced welding automation increased specialty mixed gas consumption by nearly 24% during 2025. The region is also benefiting from reshoring strategies and supply-chain diversification policies aimed at strengthening domestic industrial resilience following geopolitical trade disruptions. Industrial operators are aggressively integrating AI-driven gas monitoring systems and automated purity-control platforms, improving operational precision by approximately 21%. Major industrial gas providers expanded localized specialty gas infrastructure and storage capacity by nearly 18% to support semiconductor and defense manufacturing requirements. Enterprise buyers increasingly prioritize reliability, purity assurance, and digital monitoring integration over low-cost procurement models. Companies continue prioritizing North America because of its high-value industrial demand base, advanced innovation ecosystem, and accelerating investment in strategic manufacturing independence.

Europe represents approximately 21% of the global Industrial Mixed Gas Market, with Germany, France, and the Netherlands leading industrial gas consumption across automotive, healthcare, chemicals, and advanced engineering sectors. The region’s demand is strongly shaped by stringent emissions policies, industrial decarbonization targets, and carbon-efficiency mandates that are forcing manufacturers to optimize gas utilization and reduce process-related emissions. More than 36% of large industrial facilities across Western Europe integrated low-emission gas management systems during 2025 to improve compliance and operational efficiency simultaneously. Industrial gas companies are deploying energy-efficient separation technologies and gas recycling systems capable of lowering industrial gas losses by approximately 17%. European enterprises increasingly adopt compliance-driven procurement strategies prioritizing certified low-carbon gas solutions and supply transparency. The region continues forcing innovation in advanced purification systems, sustainable gas recovery infrastructure, and intelligent process optimization technologies that redefine industrial competitiveness under tightening regulatory pressure.

Asia-Pacific dominates the Industrial Mixed Gas Market with approximately 43% global share, driven by large-scale electronics production, semiconductor fabrication, automotive manufacturing, and industrial infrastructure expansion across China, Japan, South Korea, and India. China alone contributes nearly 35% of regional industrial mixed gas consumption due to aggressive investments in semiconductor self-sufficiency and precision manufacturing ecosystems. Industrial gas deployment across automated manufacturing operations increased by approximately 29% during 2025 as regional manufacturers accelerated smart factory adoption and localized specialty gas production. Companies are rapidly expanding cryogenic storage infrastructure, AI-enabled blending facilities, and regional distribution hubs to strengthen supply resilience and reduce logistics dependence. Industrial buyers prioritize scalability, delivery speed, and cost-efficient customized gas solutions to support high-volume manufacturing environments. Asia-Pacific remains strategically critical because it combines unmatched industrial scale, strong manufacturing integration, and rapidly expanding high-purity gas demand across future-focused production sectors.

South America accounts for nearly 5% of global Industrial Mixed Gas Market demand, led by Brazil and Argentina where automotive manufacturing, mining operations, food processing, and steel production continue driving industrial gas consumption. Industrial mixed gas adoption across regional metal fabrication operations increased by approximately 16% during 2025 as manufacturers upgraded automated welding and industrial processing capabilities. However, infrastructure limitations, transportation costs, and inconsistent energy availability remain major structural constraints affecting large-scale industrial gas deployment. Logistics costs for specialty gas transportation are nearly 14% higher compared with mature industrial markets, directly impacting operational scalability. In response, industrial gas suppliers are investing in localized storage hubs, regional blending facilities, and flexible supply agreements to improve delivery reliability. Enterprise buyers remain highly price-sensitive and prioritize operational continuity, making South America strategically attractive for long-term industrial expansion while simultaneously presenting execution and infrastructure risks.

The Middle East & Africa region contributes approximately 4% of global Industrial Mixed Gas Market demand, supported by large-scale oil and gas operations, infrastructure development, petrochemical processing, and industrial diversification programs across Saudi Arabia, the UAE, and South Africa. Industrial gas utilization in energy and heavy engineering projects increased by nearly 18% during 2025 as governments accelerated industrial modernization and manufacturing localization initiatives. Regional investment in industrial infrastructure and strategic partnerships is reshaping gas deployment capabilities, particularly across petrochemical and hydrogen-processing operations. Industrial operators are increasingly adopting automated gas management systems and advanced purification technologies capable of improving operational efficiency by approximately 15%. Enterprise procurement behavior is shifting toward long-term supply security, localized production, and scalable gas delivery solutions. The region is becoming strategically important because industrial diversification agendas and infrastructure expansion programs are creating sustained demand for advanced industrial mixed gas solutions.

China – 35% Market Share: Driven by massive semiconductor manufacturing expansion, integrated electronics production ecosystems, and large-scale industrial gas infrastructure investments.

United States – 27% Market Share: Supported by advanced aerospace manufacturing, specialty gas innovation leadership, and rapid adoption of AI-enabled industrial gas management systems.

The Industrial Mixed Gas Market is highly competitive, with global industrial gas leaders competing aggressively against regional specialty gas suppliers, technology-driven purity solution providers, and cost-focused local distributors. Major companies including Linde plc, Air Liquide, Air Products and Chemicals, Inc., Messer Group, and Nippon Sanso are competing through high-purity gas technologies, localized infrastructure expansion, integrated logistics systems, and long-term industrial partnerships. The top five players collectively control nearly 54% of global market share, supported by strong supply-chain integration and advanced purification capabilities.

Competition is increasingly defined by delivery reliability, gas purity consistency, digital monitoring integration, and customized blending performance rather than pricing alone. AI-enabled gas management systems improve operational efficiency by approximately 21%, while advanced recycling technologies reduce gas wastage by nearly 17%, giving innovation-focused players a measurable competitive edge. Companies are aggressively pursuing vertical integration strategies, semiconductor partnerships, regional storage expansion, and hydrogen-ready gas infrastructure investments to secure supply resilience and customer retention.

The competitive landscape is rapidly shifting toward technology-led differentiation and localized supply control. Winning in this market now requires advanced purity engineering, resilient regional infrastructure, intelligent gas optimization capabilities, and the ability to deliver customized industrial solutions at scale under increasingly complex regulatory and operational conditions.

Air Liquide

Air Products and Chemicals, Inc.

Messer Group GmbH

Nippon Sanso Holdings Corporation

Taiyo Nippon Sanso Corporation

Matheson Tri-Gas, Inc.

SOL Group

Gulf Cryo

Ellenbarrie Industrial Gases Ltd.

INOX Air Products

Praxair Technology, Inc.

Yingde Gases Group Company Limited

AI-enabled gas blending and automated purity-control technologies are becoming central to industrial mixed gas operations. Advanced digital blending platforms improve gas composition accuracy by nearly 27% while reducing calibration downtime by approximately 19% compared with conventional manual systems. More than 38% of semiconductor and aerospace manufacturing facilities now deploy real-time gas analytics and predictive monitoring tools to maintain contamination-sensitive production environments and optimize operational consistency.

Membrane separation technologies and energy-efficient cryogenic purification systems are also reshaping industrial gas production. Compared with legacy gas separation infrastructure, next-generation membrane-based systems improve energy efficiency by approximately 22% and lower maintenance intensity significantly. Industrial gas suppliers adopting integrated purification and recycling systems are reducing gas losses by nearly 17%, strengthening both operational efficiency and regulatory compliance performance across emission-sensitive industries.

Hydrogen-compatible industrial mixed gas systems are rapidly emerging across steel manufacturing, energy processing, and advanced transportation sectors. Automated hydrogen blending technologies improve thermal process efficiency by approximately 16% while supporting lower-emission industrial operations. Companies positioned within hydrogen infrastructure ecosystems are gaining competitive advantages through early deployment capabilities and specialized gas management expertise.

Between 2026 and 2028, intelligent industrial gas ecosystems integrating AI diagnostics, remote monitoring, digital twins, and automated recovery systems are expected to redefine industrial process optimization. Manufacturers investing early in smart gas infrastructure, localized specialty gas production, and high-purity analytics platforms will secure stronger supply resilience, operational precision, and long-term industrial competitiveness.

April 2025 – Linde plc announced expansion of ultra-high-purity industrial gas supply to Samsung’s semiconductor complex in South Korea through an eighth on-site air separation unit. The project strengthens nitrogen, argon, and hydrogen supply reliability for advanced chip production and supports operations beginning mid-2026. [Semiconductor Capacity Expansion] Source: www.linde.com

July 2025 – Air Liquide committed more than EUR 250 million to build three advanced gas production units and hydrogen facilities in Germany’s Silicon Saxony semiconductor hub. The investment strengthens ultra-pure gas availability while reducing transport-related emissions through localized production infrastructure. [Localized Supply Integration]

July 2025 – Air Liquide started operations at the world’s largest molybdenum manufacturing plant in South Korea to support next-generation semiconductor materials. The facility enables large-scale ultra-high-purity material production and strengthens advanced industrial gas integration for semiconductor fabrication ecosystems. [Advanced Materials Scale-Up]

July 2025 – Air Liquide announced a USD 50 million investment to construct an advanced industrial gas production facility supporting U.S. semiconductor manufacturing. The new plant will supply ultra-pure nitrogen and oxygen directly to a major chip manufacturer, reinforcing localized specialty gas resilience. [U.S. Semiconductor Support]

The Industrial Mixed Gas Market Report delivers comprehensive analysis across industrial gas types, applications, end-user industries, regional demand patterns, and emerging technology ecosystems shaping advanced manufacturing operations. The report evaluates high-purity industrial gas mixtures, specialty reactive gas systems, calibration gases, and customized industrial blending solutions used across semiconductor fabrication, metal processing, healthcare, chemicals, food packaging, aerospace, and hydrogen-processing applications. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, enabling detailed comparison of production concentration, industrial adoption trends, infrastructure investments, and supply-chain transformation strategies.

The report provides deep analytical coverage across more than 15 strategic market segments, profiling over 12 major industrial gas companies and evaluating operational trends influencing industrial competitiveness between 2026 and 2033. Asia-Pacific accounts for approximately 43% of global demand concentration, while customized high-purity gas solutions represent nearly 44% of advanced industrial processing deployments. Additionally, over 38% of semiconductor and aerospace manufacturing facilities have integrated AI-enabled gas monitoring and purity optimization technologies, reshaping operational efficiency standards globally.

The study also assesses future-focused themes including hydrogen-compatible industrial gas systems, AI-driven blending technologies, localized supply infrastructure, digital gas analytics, and energy-efficient purification systems. The report supports strategic decision-making for manufacturers, investors, industrial suppliers, and technology providers seeking expansion opportunities, operational optimization pathways, competitive benchmarking insights, and resilient long-term positioning within the rapidly transforming global Industrial Mixed Gas Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,560.0 Million |

| Market Revenue (2033) | USD 7,378.4 Million |

| CAGR (2026–2033) | 6.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Linde plc; Air Liquide; Air Products and Chemicals, Inc.; Messer Group GmbH; Nippon Sanso Holdings Corporation; Taiyo Nippon Sanso Corporation; Matheson Tri-Gas, Inc.; SOL Group; Gulf Cryo; Ellenbarrie Industrial Gases Ltd.; INOX Air Products; Yingde Gases Group Company Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |