Reports

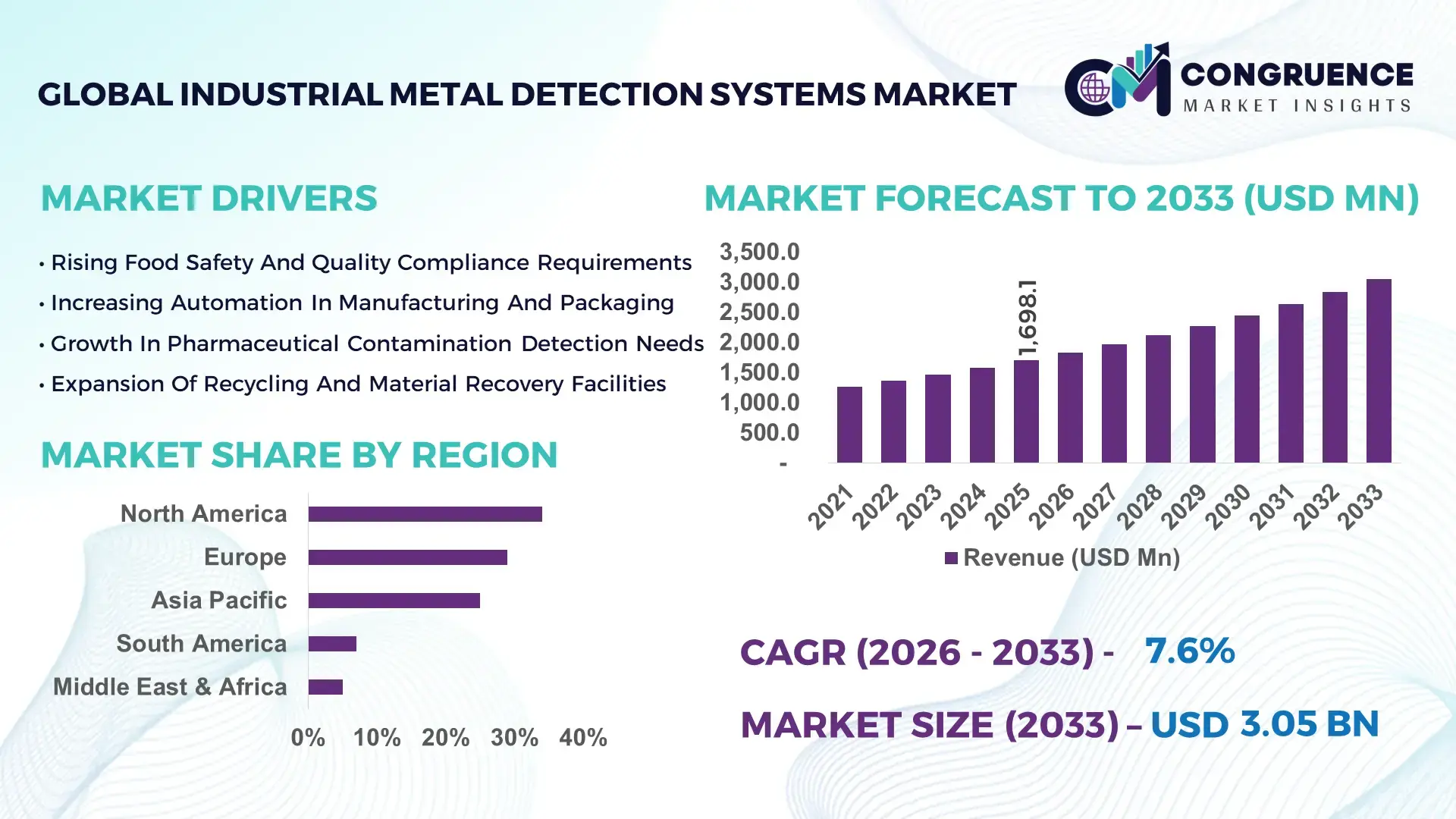

The Global Industrial Metal Detection Systems Market was valued at USD 1,698.1 Million in 2025 and is anticipated to reach a value of USD 3,051.1 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by tightening product safety regulations and rising automation across food, pharmaceutical, and mining industries.

In the United States, which leads in advanced industrial automation deployment, more than 68% of large-scale food processing plants have integrated inline Industrial Metal Detection Systems within high-speed conveyor lines. Annual capital investment in food safety and quality inspection technologies exceeded USD 2.5 billion in 2025, with over 14,000 manufacturing facilities deploying digital inspection and contaminant detection solutions. The country also hosts more than 120 specialized manufacturers and system integrators focusing on multi-frequency detection coils, AI-enhanced signal filtering, and real-time reject mechanisms capable of detecting ferrous particles as small as 0.3 mm in packaged goods.

Market Size & Growth: USD 1,698.1 Million in 2025, projected to reach USD 3,051.1 Million by 2033 at 7.6% CAGR, supported by stringent industrial safety mandates.

Top Growth Drivers: 42% rise in automated food inspection lines; 35% efficiency improvement in quality control; 28% reduction in product recalls.

Short-Term Forecast: By 2028, AI-enabled detection analytics expected to reduce false rejects by 18%.

Emerging Technologies: Multi-spectrum frequency scanning; AI-based noise discrimination; IoT-enabled remote calibration systems.

Regional Leaders: North America projected above USD 1,050 Million by 2033; Europe above USD 820 Million; Asia-Pacific above USD 780 Million, driven by manufacturing automation.

Consumer/End-User Trends: Over 61% of packaged food manufacturers prioritize inline contaminant detection integration.

Pilot Case Example: In 2025, a dairy processor reduced contamination incidents by 32% after upgrading to high-sensitivity Industrial Metal Detection Systems.

Competitive Landscape: Leading player holds approximately 17% share, followed by four major global competitors with strong OEM partnerships.

Regulatory & ESG Impact: 100% compliance required under updated food safety modernization guidelines; 24% energy-efficient system upgrades adopted.

Investment Patterns: More than USD 900 Million invested globally in automated inspection technologies during 2024–2025.

Innovation & Outlook: Predictive diagnostics and smart conveyor integration shaping next-generation Industrial Metal Detection Systems.

Industrial Metal Detection Systems are primarily adopted across food & beverage (44%), pharmaceuticals (21%), mining (15%), and plastics & packaging (11%). Increasing automation in emerging Asia-Pacific manufacturing hubs, coupled with digital quality assurance mandates in Europe, is accelerating demand. Smart reject mechanisms and compact tunnel detectors are gaining traction in high-speed production environments exceeding 300 units per minute.

The Industrial Metal Detection Systems Market plays a pivotal role in safeguarding supply chains, enhancing brand protection, and ensuring regulatory compliance. As global food production exceeds 4 billion metric tons annually, manufacturers are integrating advanced inline contaminant detection to minimize recall risks and maintain consumer trust. Modern multi-frequency Industrial Metal Detection Systems deliver 25% higher detection sensitivity compared to traditional single-frequency systems.

North America dominates in installed base volume, while Asia-Pacific leads in new facility adoption with over 46% of recently commissioned processing plants integrating automated inspection systems. By 2028, AI-driven signal processing is expected to reduce downtime by 20% and improve detection accuracy by 15%. Firms are committing to ESG-driven efficiency targets, including 18% energy consumption reduction by 2030 through low-power detection coils.

In 2025, a European food manufacturer achieved a 29% reduction in product waste by deploying AI-calibrated Industrial Metal Detection Systems across 12 production lines. With predictive maintenance, digital twin calibration, and integrated IoT dashboards, the Industrial Metal Detection Systems Market is emerging as a pillar of operational resilience, regulatory alignment, and sustainable industrial growth.

The Industrial Metal Detection Systems Market is shaped by regulatory enforcement, automation trends, and rising quality assurance expectations across manufacturing industries. More than 70 countries enforce mandatory contaminant detection standards for packaged food exports, compelling manufacturers to upgrade legacy inspection systems. Increased automation in high-speed production lines operating above 250 packs per minute has necessitated real-time detection with millisecond response capability.

Technological advancements in coil design and digital filtering have improved detection thresholds by up to 30% over the past five years. Simultaneously, global recall incidents linked to foreign object contamination have increased by 12%, emphasizing preventive quality control. Integration with Industry 4.0 ecosystems enables centralized monitoring across multi-site operations, strengthening compliance and traceability.

Global food and pharmaceutical regulations mandate contaminant-free production lines, directly boosting demand for Industrial Metal Detection Systems. Over 61% of multinational food manufacturers upgraded inspection infrastructure between 2023 and 2025. Advanced conveyor-based systems detect metallic fragments as small as 0.3 mm in dry products and 0.5 mm in wet applications.

In pharmaceutical production, compliance audits increased by 19%, pushing companies to adopt high-sensitivity metal detectors integrated with automated rejection units. Quality control automation has reduced recall-related financial losses by approximately 28%, reinforcing the value proposition of Industrial Metal Detection Systems in regulated sectors.

Despite technological benefits, upfront costs for advanced Industrial Metal Detection Systems range between USD 15,000 and USD 45,000 per unit, limiting adoption among small-scale processors. Installation and calibration expenses add approximately 12% to total project budgets.

Additionally, false rejection rates averaging 2–3% in poorly calibrated systems can result in production inefficiencies. Smaller facilities with throughput below 50 units per minute often delay modernization due to budget constraints and limited technical expertise.

The rise of smart factories presents significant growth avenues. Over 48% of new manufacturing plants incorporate IoT-enabled inspection systems capable of remote diagnostics and predictive maintenance. Integration with centralized dashboards allows performance tracking across multiple facilities.

AI-based signal differentiation reduces false rejects by up to 18%, improving yield efficiency. Emerging economies investing in automated food processing infrastructure—particularly in Asia-Pacific—offer substantial deployment potential for scalable Industrial Metal Detection Systems.

The increased use of metallized films and aluminum packaging complicates metal detection performance. Approximately 22% of packaged goods now utilize composite materials that interfere with electromagnetic detection fields.

High-moisture or high-salt content products generate conductive signals, increasing calibration complexity. Manufacturers must invest in multi-frequency and phase-sensitive Industrial Metal Detection Systems to maintain detection precision in challenging environments.

• AI-Enhanced Signal Filtering and False Reject Reduction: Modern Industrial Metal Detection Systems incorporating AI-driven algorithms have reduced false reject rates by 18% while improving detection sensitivity by 22%. Facilities processing over 300 units per minute report productivity gains of 15% following AI integration.

• Compact and Modular Conveyor-Based Systems: Over 57% of newly installed detection systems in 2025 feature modular designs, reducing installation time by 25%. Compact tunnel detectors enable seamless integration into existing high-speed packaging lines without structural modifications.

• IoT-Enabled Remote Monitoring: Approximately 46% of large manufacturing enterprises now utilize IoT-connected Industrial Metal Detection Systems, enabling remote calibration and predictive maintenance. Downtime has decreased by 17% in plants using cloud-based monitoring dashboards.

• Multi-Frequency and High-Sensitivity Coil Advancements: Advanced multi-spectrum detection coils improve contaminant detection accuracy by 30% compared to legacy systems. Mining and recycling facilities deploying these technologies have enhanced metal fragment recovery efficiency by 21%.

The Industrial Metal Detection Systems Market is segmented by type, application, and end-user. By type, conveyor-based systems dominate high-speed manufacturing environments, while pipeline and gravity-fed detectors serve bulk and liquid applications. By application, food & beverage leads due to regulatory mandates, followed by pharmaceuticals, mining, and plastics.

End-user segmentation highlights large-scale manufacturers accounting for the majority of installations, while SMEs represent growing adoption driven by export compliance requirements. Technological sophistication, detection sensitivity, and integration capability remain key purchase criteria for decision-makers.

Conveyor-based Industrial Metal Detection Systems account for approximately 49% of total installations due to widespread adoption in packaged food production lines. Pipeline metal detectors hold around 23%, primarily used in dairy and liquid processing. Gravity-fed detectors represent 17%, serving powder and grain processing industries.

Conveyor-based systems remain dominant due to compatibility with automated reject units and throughput exceeding 300 units per minute. However, pipeline detectors are the fastest-growing segment with a projected CAGR of 8.9%, driven by liquid food and beverage expansion. Remaining niche systems, including handheld and customized inspection units, collectively contribute 11% share.

Food & Beverage accounts for approximately 44% of Industrial Metal Detection Systems usage, followed by pharmaceuticals at 21% and mining at 15%. Packaging and plastics collectively represent 10%.

Food processing leads due to mandatory contaminant detection requirements across export markets. Pharmaceutical production lines increasingly adopt high-sensitivity systems capable of detecting stainless steel fragments under 0.4 mm. Mining applications use heavy-duty detectors for ore and aggregate screening.

In 2025, more than 41% of enterprises globally reported upgrading inspection systems within customer-facing supply chains. Additionally, 38% of automated processing facilities integrated Industrial Metal Detection Systems within digital quality assurance platforms.

Large-scale food processors represent 46% of end-user installations, reflecting high compliance obligations and export standards. Pharmaceutical manufacturers account for 22%, while mining and recycling industries contribute 18%. SMEs and contract manufacturers represent 14%.

Large enterprises dominate due to multi-line production capacity and global distribution networks. However, SMEs represent the fastest-growing end-user segment with an expected CAGR of 8.4%, supported by increasing export compliance requirements.

In 2025, over 39% of enterprises globally reported piloting Industrial Metal Detection Systems integration within broader smart factory initiatives. Furthermore, 34% of packaging plants implemented automated rejection and data logging capabilities.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America’s dominance is supported by over 18,000 large-scale food and beverage processing facilities and more than 6,500 pharmaceutical manufacturing plants operating under mandatory contaminant control frameworks. Europe followed with approximately 29% market share, driven by stringent product safety regulations across Germany, the UK, France, and Italy, collectively representing over 11,000 regulated food production sites. Asia-Pacific held nearly 25% share in 2025, supported by rapid industrial automation in China, India, and Japan, where manufacturing output accounts for more than 30% of regional GDP in key economies. South America contributed close to 7%, while Middle East & Africa represented around 5%, reflecting expanding packaged food production capacity exceeding 120 million metric tons annually across emerging economies. Increased cross-border food exports, which grew by 14% year-over-year in 2025, continue to reinforce the global adoption of Industrial Metal Detection Systems across regulated supply chains.

How Are Advanced Food Safety Regulations Reshaping High-Sensitivity Detection Adoption?

North America represents approximately 34% of the global Industrial Metal Detection Systems market, supported by highly regulated food, pharmaceutical, and packaging industries. The United States accounts for the majority of installations, with over 70% of large food processing plants operating inline conveyor-based metal detectors. Canada contributes significantly through export-driven meat and dairy processing, handling more than 25 million metric tons annually.

Regulatory modernization initiatives have strengthened compliance audits, increasing inspection frequency by 19% over the past three years. Digital transformation trends are evident, with nearly 48% of large manufacturers integrating IoT-enabled Industrial Metal Detection Systems into centralized monitoring dashboards. A leading regional manufacturer has introduced multi-frequency systems capable of detecting ferrous contaminants as small as 0.3 mm, improving accuracy by 22%. Consumer behavior reflects strong preference for certified contaminant-free packaged goods, with over 63% of consumers prioritizing product safety labeling in purchasing decisions.

Is Regulatory Pressure Driving Precision Detection Upgrades in Manufacturing Lines?

Europe holds approximately 29% of the global Industrial Metal Detection Systems market, with Germany, the United Kingdom, and France accounting for more than 60% of regional demand. Germany alone operates over 4,000 medium-to-large food processing facilities, many requiring high-sensitivity inspection systems under strict compliance frameworks.

Sustainability initiatives emphasize waste reduction, leading to 21% of manufacturers upgrading to energy-efficient detection coils. Adoption of emerging technologies such as AI-driven calibration tools has improved detection precision by nearly 18% in pilot deployments. A prominent European equipment manufacturer recently launched compact gravity-fed detectors optimized for powdered dairy products, reducing false rejects by 15%. Regional consumer behavior demonstrates heightened demand for traceability and documented inspection processes, with 58% of retailers requiring certified inspection logs before product acceptance.

How Is Rapid Industrial Automation Accelerating Inline Inspection Integration?

Asia-Pacific ranks third in total market volume but leads in new installation growth, accounting for nearly 25% of global demand. China, India, and Japan collectively operate more than 20,000 food and beverage manufacturing units requiring contaminant screening. China alone contributes over 35% of regional installations due to high packaged food output exceeding 300 million metric tons annually.

Infrastructure modernization and automation investment exceeding USD 50 billion across manufacturing upgrades have accelerated the integration of conveyor-based and pipeline Industrial Metal Detection Systems. A major regional equipment supplier introduced AI-enhanced phase-sensitive detection units in 2025, improving detection rates by 20% in high-moisture environments. Consumer behavior trends show increasing packaged food consumption, with urban households rising by 12% year-over-year, reinforcing demand for automated inspection technologies.

Can Expanding Food Exports Strengthen Compliance-Driven Detection Adoption?

South America accounts for approximately 7% of the global Industrial Metal Detection Systems market, with Brazil and Argentina representing nearly 65% of regional installations. Brazil processes over 40 million metric tons of meat annually, creating substantial demand for inline contaminant detection.

Government export incentives supporting agricultural shipments have increased inspection requirements by 16% over the past two years. Energy and mining sectors also contribute to adoption, particularly in mineral screening operations. A regional manufacturer introduced heavy-duty tunnel detectors designed for bulk grain export terminals, improving throughput by 14%. Consumer behavior reflects growing awareness of international safety standards, particularly among export-focused producers complying with global food safety protocols.

Are Infrastructure Modernization and Export Compliance Driving Detection System Deployment?

Middle East & Africa contribute approximately 5% of global Industrial Metal Detection Systems demand, led by the UAE and South Africa. The UAE’s food re-export industry handles more than 10 million metric tons annually, requiring strict inspection compliance. South Africa supports over 3,500 regulated food processing units.

Industrial modernization initiatives linked to oil & gas diversification strategies have boosted automation investments by 18% since 2023. A regional supplier introduced stainless-steel IP69K-rated detectors for harsh environments, improving operational durability by 25%. Trade partnerships with European markets have increased compliance-driven installations. Consumer purchasing patterns indicate rising preference for packaged goods with certified quality inspection credentials, particularly in urban retail sectors expanding at 9% annually.

United States – 28% Market Share: Industrial Metal Detection Systems adoption driven by over 18,000 regulated food and pharmaceutical manufacturing facilities.

Germany – 11% Market Share: Strong Industrial Metal Detection Systems demand supported by advanced manufacturing automation and strict EU food safety regulations.

The Industrial Metal Detection Systems market is moderately consolidated, with approximately 45 active global and regional competitors. The top five companies collectively account for nearly 54% of total market share, reflecting strong brand positioning and established OEM partnerships. Leading players maintain competitive advantage through multi-frequency technology portfolios, integrated conveyor systems, and global service networks operating in more than 80 countries.

Strategic initiatives between 2024 and 2025 included over 12 product launches focusing on AI-enabled calibration and IoT connectivity. More than 18 strategic distribution agreements were signed to expand presence in Asia-Pacific and Latin America. Companies are investing heavily in R&D, allocating an average of 6–8% of annual budgets toward advanced coil design and signal filtering innovation. Competitive differentiation increasingly centers on detection sensitivity thresholds, false reject reduction rates below 2%, and predictive maintenance capabilities. The market continues to witness partnerships between equipment manufacturers and food processing automation providers to deliver integrated quality control ecosystems.

Sesotec GmbH

CEIA S.p.A.

Loma Systems

Anritsu Corporation

Eriez Manufacturing Co.

Fortress Technology Inc.

Cassel Messtechnik GmbH

Bunting Magnetics Co.

Multivac Group

Mesutronic Gerätebau GmbH

Nikka Densok Ltd.

Technological advancement is central to the evolution of the Industrial Metal Detection Systems market. Multi-frequency detection technology now enables simultaneous scanning across 3–5 frequency bands, enhancing detection accuracy by up to 30% compared to single-frequency systems. Phase-sensitive detection algorithms differentiate between product effect and metal contaminants, reducing false rejects by approximately 18%.

AI-driven signal analytics improve calibration speed by 22%, while predictive maintenance systems decrease unexpected downtime by 17%. IoT-enabled detectors transmit real-time performance metrics, supporting centralized monitoring across multi-plant operations. Stainless-steel IP69K-rated enclosures enhance durability in washdown environments, extending equipment life by nearly 25%.

Integration with Industry 4.0 frameworks allows synchronization with automated reject arms operating within milliseconds. Advanced coil geometry improves sensitivity to non-ferrous and stainless-steel contaminants smaller than 0.4 mm. Emerging compact tunnel detectors designed for high-speed packaging lines exceeding 350 packs per minute are gaining adoption. These innovations collectively strengthen operational efficiency, regulatory compliance, and product safety assurance across global manufacturing ecosystems.

• In March 2025, Mettler-Toledo launched an upgraded Profile Advantage metal detection system featuring enhanced multi-simultaneous frequency technology, improving contaminant detection sensitivity in challenging wet and conductive products by up to 20%. Source: www.mt.com

• In October 2024, Thermo Fisher Scientific introduced advanced Sentinel metal detector models integrating improved signal processing algorithms to reduce false reject rates in packaged food lines operating above 300 packs per minute. Source: www.thermofisher.com

• In May 2025, Minebea Intec unveiled a compact Vistus metal detection system optimized for space-constrained production facilities, delivering improved stainless-steel detection capability below 0.4 mm. Source: www.minebea-intec.com

• In January 2024, Sesotec expanded its INTUITY metal detector portfolio with AI-supported evaluation software designed to enhance signal differentiation accuracy by approximately 15% in high-moisture food applications. Source: www.sesotec.com

The Industrial Metal Detection Systems Market Report provides comprehensive coverage across product types, applications, end-user industries, and geographic regions. The scope includes conveyor-based systems, pipeline detectors, gravity-fed units, and heavy-duty industrial models designed for mining and recycling operations. Detection sensitivity parameters ranging from 0.3 mm to 2.5 mm across ferrous, non-ferrous, and stainless-steel contaminants are evaluated in detail.

Application coverage spans food & beverage processing exceeding 4 billion metric tons annually, pharmaceutical production lines operating under global compliance mandates, mining operations processing over 7 billion metric tons of ore, and plastics & packaging sectors requiring inline contaminant control. The report examines regional demand across North America (34%), Europe (29%), Asia-Pacific (25%), South America (7%), and Middle East & Africa (5%).

Technological scope includes AI-driven calibration systems, IoT connectivity, predictive diagnostics, multi-frequency scanning, and compact modular designs. The study also analyzes installation trends in facilities operating above 300 units per minute, compliance-driven inspection mandates across more than 70 countries, and integration within Industry 4.0 manufacturing ecosystems. Emerging niche segments such as portable inspection units and high-hygiene washdown-certified detectors are also evaluated, providing strategic insights for manufacturers, investors, and industrial automation stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,698.1 Million |

|

Market Revenue in 2033 |

USD 3,051.1 Million |

|

CAGR (2026 - 2033) |

7.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Mettler-Toledo International Inc., Thermo Fisher Scientific Inc., Minebea Intec GmbH, Sesotec GmbH, CEIA S.p.A., Loma Systems, Anritsu Corporation, Eriez Manufacturing Co., Fortress Technology Inc., Cassel Messtechnik GmbH, Bunting Magnetics Co., Multivac Group, Mesutronic Gerätebau GmbH, Nikka Densok Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |