Reports

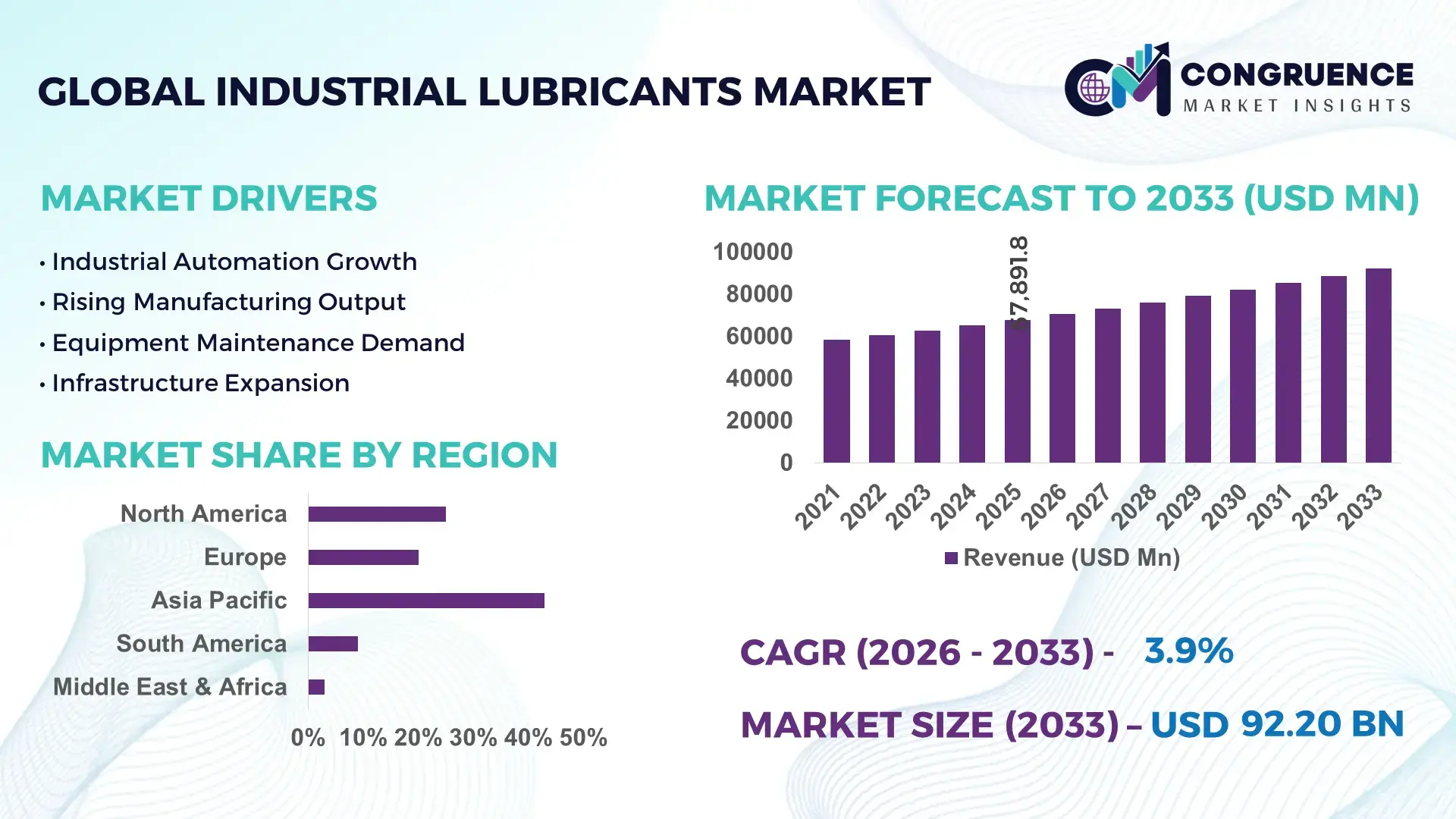

The Global Industrial Lubricants Market was valued at USD 67891.79 Million in 2025 and is anticipated to reach a value of USD 92202.28 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. Growth is being driven by higher deployment of automated manufacturing systems, expanding wind energy installations, and rising demand for high-performance synthetic lubricants that extend equipment life by 15–25% in heavy industrial operations.

China remains the dominant country in the industrial lubricants landscape, accounting for approximately 31% of global manufacturing output and supported by multi-billion-dollar investments in advanced industrial production, metals processing, and renewable energy infrastructure. Industrial lubricant consumption intensity in China exceeds that of Germany by more than 2x, while smart factory adoption across key industrial clusters has surpassed 40%. Ongoing supply-chain diversification following Red Sea trade disruptions has further reinforced localized production and lubricant demand across strategic industrial sectors.

For industry participants, prioritizing high-performance formulations, regional manufacturing footprints, and application-specific lubrication solutions is becoming essential to capture long-term industrial asset maintenance spending.

Market Size & Growth: USD 67,891.79 million in 2025, projected to reach USD 92,202.28 million by 2033 at 3.9% CAGR, supported by automation expansion and synthetic lubricant adoption.

Top Growth Drivers: Synthetic lubricant penetration (+22%), industrial automation deployment (+18%), and renewable energy equipment installations (+16%) drive market expansion.

Short-Term Forecast: By 2028, predictive lubrication programs are expected to reduce maintenance costs by 12% and improve equipment uptime by 10%.

Emerging Technologies: AI-based lubricant monitoring, IoT sensors, and advanced synthetic base oils improve lubrication efficiency by 15–20%.

Regional Leaders: Asia-Pacific exceeds USD 38 billion, Europe approaches USD 21 billion, and North America surpasses USD 18 billion, supported by smart manufacturing investments.

Consumer/End-User Trends: More than 45% of large industrial facilities are integrating condition-based lubrication management systems.

Pilot/Case Example: In 2026, a large steel production modernization project achieved a 14% reduction in lubricant consumption through digital monitoring integration.

Competitive Landscape: Top players collectively control approximately 38% of global share, with major competition centered on advanced synthetic and specialty lubricant portfolios.

Regulatory & ESG Impact: Low-emission lubricant adoption has increased over 20%, supporting industrial sustainability targets and reduced waste generation.

Investment & Funding: Global capacity expansions and strategic partnerships exceed USD 5 billion, targeting regional supply resilience and specialty product development.

Innovation & Future Outlook: Bio-based lubricants, AI-driven maintenance platforms, and high-performance formulations are accelerating next-generation industrial asset optimization.

Industrial lubricants play a critical role across manufacturing, mining, power generation, metals processing, and renewable energy operations where equipment reliability directly affects productivity. Recent innovations in synthetic formulations, condition-monitoring technologies, and bio-based products have improved lubricant performance by approximately 15% while supporting sustainability objectives. Increasing localization of industrial supply chains and stricter operational efficiency requirements are accelerating demand for application-specific lubrication solutions, creating a strong foundation for the strategic market developments discussed in the following sections.

Industrial lubricants are becoming strategically important as manufacturers prioritize asset reliability, energy efficiency, and production continuity amid supply-chain restructuring and infrastructure modernization. The market has evolved from a maintenance consumables segment into a critical operational performance category influencing equipment lifespan, downtime management, and sustainability objectives. Rising investments in advanced manufacturing facilities, renewable energy assets, and automated production systems are increasing demand for specialized lubrication solutions capable of supporting higher operating loads and precision equipment requirements.

Technology adoption is reshaping competitive dynamics. Synthetic lubricants typically deliver 20–30% longer drain intervals and reduce maintenance interventions by nearly 15% compared with conventional mineral-based products. China continues to lead in industrial-scale deployment through extensive manufacturing capacity, while Germany demonstrates stronger adoption of high-performance and condition-monitoring lubrication systems across advanced engineering sectors. In the United States, digital lubricant monitoring programs are being integrated into industrial maintenance strategies, with predictive maintenance adoption exceeding 35% among large manufacturing facilities.

A practical example is the deployment of sensor-enabled lubrication systems in steel and cement plants, where operators have achieved double-digit reductions in unplanned equipment stoppages. Over the next two to three years, companies are expected to increase investments in localized production, specialty formulations, and strategic technology partnerships. Organizations that combine performance-driven product portfolios with digital lubrication capabilities will strengthen competitive positioning and secure long-term operational advantages.

Industrial automation expansion and increasing focus on equipment uptime remain the strongest demand catalysts for industrial lubricants. Automated manufacturing facilities now account for more than 40% of production capacity additions in major industrial economies, while predictive maintenance adoption has increased by approximately 35% among large-scale operators. As machinery utilization rates rise, demand is shifting toward synthetic and application-specific lubricants capable of extending component life by 15–25%. China's continued investment in advanced manufacturing and India's industrial corridor development are increasing lubricant consumption across metals, power generation, and heavy engineering sectors. In response, suppliers are expanding specialty product lines, investing in performance-enhancing formulations, and forming technology partnerships to support high-load industrial environments. The strategic advantage increasingly lies in delivering measurable uptime improvements rather than simply supplying lubrication products.

Base oil price volatility and feedstock dependency continue to constrain profitability across the industrial lubricants value chain. Raw material costs can represent over 55% of total lubricant production expenses, while fluctuations in crude-derived feedstocks have generated periodic procurement uncertainty. Supply disruptions linked to major shipping routes have extended lead times by 10–20% for selected industrial inputs, creating inventory planning challenges. Germany and Japan, which depend significantly on imported feedstock streams, remain particularly exposed to global supply fluctuations. The direct impact includes compressed margins, delayed product deliveries, and reduced pricing flexibility for manufacturers. To mitigate risk, companies are increasing localized sourcing, securing long-term supply agreements, and diversifying base oil procurement strategies. Operational resilience has become as important as production capacity in sustaining market competitiveness.

The emergence of intelligent lubrication management presents a significant opportunity beyond traditional product sales. Sensor-integrated lubrication systems can improve maintenance efficiency by approximately 20% while reducing lubricant waste by nearly 15%. Industrial operators in China and South Korea are accelerating investments in connected manufacturing environments where lubrication performance data is integrated into broader asset management platforms. Bio-based and high-performance synthetic lubricants are also gaining traction as industrial facilities target lower emissions and improved energy efficiency. Companies are expanding R&D programs, forming digital technology partnerships, and developing application-specific formulations for wind turbines, electric manufacturing equipment, and automated production assets. A notable strategic opportunity lies in combining lubricant products with predictive maintenance services, creating higher-value recurring business models rather than relying solely on volume-based sales.

The primary long-term challenge is the integration and scaling of advanced lubrication technologies across diverse industrial environments. More than 60% of industrial facilities continue to operate mixed fleets containing both legacy and modern equipment, complicating lubricant standardization and monitoring deployment. Workforce shortages in maintenance engineering have increased by approximately 12% in several manufacturing-intensive economies, limiting effective implementation of sophisticated lubrication programs. In the United States and Japan, aging industrial infrastructure further increases maintenance complexity and operational risk. Companies must address system compatibility, workforce training, and digital integration requirements while maintaining production continuity. Investments in workforce development, condition-monitoring infrastructure, and collaborative technology ecosystems will be essential. Organizations that successfully standardize lubrication practices across complex asset networks will gain a durable operational and competitive advantage.

• Predictive Lubrication Gains Momentum Industrial facilities are increasingly integrating sensor-enabled lubrication systems, with predictive maintenance deployment rising by nearly 35% since 2024. Equipment failure rates have declined by 12–18% in facilities using real-time lubricant monitoring, while maintenance scheduling accuracy has improved by approximately 20%. In response to labor shortages and uptime pressures, manufacturers are partnering with industrial software providers to automate lubrication workflows and asset condition tracking.

• Synthetic Formulations Replace Conventional Oils Advanced synthetic lubricants now account for over 40% of lubricant usage in high-load industrial applications across Germany, Japan, and the United States. Drain intervals are extending by 20–30%, while lubricant consumption per operating hour has declined by nearly 15%. Stricter equipment performance requirements and energy-efficiency targets are encouraging suppliers to expand specialty product portfolios and invest in performance-focused formulation technologies.

• Localized Supply Networks Expand Following shipping disruptions and procurement volatility, industrial lubricant producers have increased regional blending and storage capacity by approximately 18% since 2025. Lead times for critical lubricant categories have improved by nearly 10%, reducing operational risk for heavy industries. A notable shift is the relocation of inventory closer to industrial hubs, enabling manufacturers to improve service reliability while strengthening supply-chain resilience.

• Sustainability Standards Influence Procurement Industrial buyers are increasingly evaluating lubricant performance through lifecycle efficiency metrics rather than product cost alone. Adoption of bio-based and low-emission lubricant solutions has increased by roughly 22%, while waste lubricant generation has declined by nearly 12% in monitored facilities. Companies are responding through certification programs, sustainability partnerships, and product redesign initiatives that align operational performance with evolving environmental compliance requirements.

Hydraulic Oils remain the leading segment, accounting for an estimated 32–35% of industrial lubricant demand due to their extensive deployment across manufacturing equipment, construction machinery, and industrial automation systems. Their dominance is supported by scalability, operational versatility, and compatibility with modern hydraulic systems. Equipment operators increasingly prioritize high-performance hydraulic formulations capable of reducing wear rates by 15–20% while improving system efficiency. Meanwhile, Gear Oils continue to maintain strong demand in heavy industrial equipment, mining assets, and power transmission systems where reliability requirements remain critical.

Compressor Oils represent the fastest-growing segment as compressed-air systems become increasingly important within automated production facilities. Adoption has accelerated by approximately 18% in advanced manufacturing environments seeking energy optimization and reduced maintenance intervals. Metalworking Fluids continue to benefit from precision machining growth in China and India, while Greases maintain strategic importance in heavy-duty and high-temperature applications where contamination resistance is essential. Suppliers are expanding specialty formulations, investing in synthetic technologies, and strengthening industrial partnerships to address evolving equipment performance requirements and application-specific demand.

Machinery Lubrication remains the dominant application, representing approximately 38% of total industrial lubricant consumption due to its direct impact on equipment reliability, uptime, and maintenance efficiency. Industrial operators increasingly use advanced lubrication programs to reduce unexpected downtime by 10–15% while extending equipment service life. Manufacturing Equipment applications continue to generate significant demand as automation investments increase across industrial facilities. The operational priority has shifted from reactive maintenance toward continuous asset performance optimization.

Power Generation is emerging as the fastest-growing application segment, supported by expanding renewable energy installations and modernization of conventional power assets. Lubricant requirements for turbines, generators, and auxiliary equipment have increased by nearly 17% as operators seek higher reliability and extended maintenance intervals. Mining Operations continue to require specialized high-load lubrication solutions, while Metal Processing applications benefit from increasing precision manufacturing activity. Companies are responding through targeted product development, digital monitoring integration, and deployment support services designed to improve operational continuity across critical industrial environments.

Manufacturing remains the dominant end-user segment, accounting for roughly 40% of industrial lubricant consumption due to extensive deployment across production lines, machine tools, robotics, and processing equipment. High operating intensity and continuous production schedules create sustained demand for hydraulic oils, compressor oils, and metalworking fluids. Manufacturers adopting predictive maintenance programs have reported maintenance cost reductions of approximately 15%, reinforcing lubricant performance as a strategic operational factor. Companies are increasingly offering customized lubrication programs and technical support services tailored to specific production environments.

Power Generation is the fastest-growing end-user segment, driven by investments in renewable energy assets, grid modernization, and turbine reliability programs. Lubricant demand in power applications has increased by nearly 16% as operators focus on asset longevity and maintenance optimization. Mining, Construction, Oil and Gas, and Marine Industry segments continue to generate substantial demand due to harsh operating environments and heavy equipment utilization. Suppliers are strengthening partnerships with equipment manufacturers, expanding application-specific product portfolios, and implementing value-based pricing strategies to secure long-term customer relationships in these performance-critical sectors.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Advanced Manufacturing and Predictive Maintenance Expansion

North America represents a mature but technologically advanced industrial lubricants market, supported by extensive manufacturing, power generation, mining, and logistics infrastructure. The region accounts for approximately 24% of global industrial lubricant consumption, with demand increasingly linked to automation and asset reliability initiatives. Predictive maintenance adoption has surpassed 35% among large industrial operators, accelerating demand for premium synthetic lubricants and condition-monitoring solutions. Industrial modernization programs across the United States and Canada have increased deployment of sensor-enabled lubrication systems by nearly 20% since 2024. Suppliers are strengthening technical service capabilities and expanding specialized product portfolios to support advanced production environments and uptime-focused maintenance strategies.

United States Market Outlook: The United States remains the regional leader due to its large manufacturing base, extensive industrial automation deployment, and advanced maintenance practices. More than 40% of large industrial facilities utilize predictive asset management programs incorporating lubricant monitoring technologies. Growing investments in semiconductor manufacturing, energy infrastructure, and industrial reshoring initiatives continue to support demand for high-performance hydraulic oils, compressor oils, and specialty lubricants designed for precision equipment and continuous production environments.

Efficiency-Driven Industrial Modernization

Europe maintains a strong position through advanced engineering industries, stringent operational standards, and widespread adoption of energy-efficient industrial processes. The region contributes nearly 22% of global industrial lubricant demand, with growth increasingly driven by specialty lubricants and sustainability-focused formulations. Industrial operators have improved lubricant lifecycle efficiency by approximately 15% through synthetic product deployment and digital maintenance integration. Modernization of manufacturing assets and process optimization initiatives continue to increase demand for application-specific lubrication solutions. Companies are investing in lower-emission product technologies and strengthening partnerships with industrial equipment manufacturers to support long-term operational performance objectives.

Germany Market Outlook: Germany serves as the region's strategic industrial hub, supported by its leadership in machinery manufacturing, automotive production, and industrial engineering. Smart factory adoption exceeds 40% across major manufacturing sectors, creating sustained demand for advanced lubrication solutions capable of supporting automated production systems. The country's focus on precision engineering and equipment reliability encourages the use of premium synthetic lubricants and integrated maintenance programs designed to maximize operational efficiency and reduce equipment downtime.

Manufacturing Scale and Infrastructure Expansion

Asia-Pacific remains the largest industrial lubricants market due to its dominant manufacturing footprint, expanding industrial infrastructure, and rising equipment deployment across multiple sectors. The region accounts for approximately 44% of global demand and benefits from large-scale production activity in China, India, Japan, and South Korea. Industrial machinery installations have increased by more than 18% over recent years, supporting strong consumption of hydraulic oils, gear oils, and metalworking fluids. Infrastructure investment programs, export-oriented manufacturing expansion, and growing automation deployment continue to reinforce lubricant demand. Producers are expanding blending facilities and strengthening regional supply networks to improve service responsiveness and operational reliability.

China Market Outlook: China remains the most influential market due to its unmatched manufacturing capacity, extensive industrial ecosystem, and ongoing industrial upgrading initiatives. The country contributes more than 30% of global manufacturing output and continues to expand smart manufacturing deployment across strategic industrial clusters. Demand is particularly strong in metals processing, machinery manufacturing, renewable energy equipment production, and industrial automation applications. Suppliers are increasing localized innovation efforts and specialized product development to support evolving equipment performance requirements.

Mining and Industrial Recovery Support Demand

South America continues to strengthen its industrial lubricants market through mining expansion, infrastructure investment, and manufacturing recovery initiatives. The region contributes approximately 6% of global lubricant demand, with consumption concentrated in mining operations, construction equipment, and industrial processing facilities. Mining-sector equipment utilization rates have increased by nearly 12% in key resource-producing countries, driving demand for heavy-duty lubrication solutions. However, logistics constraints and uneven infrastructure development continue to influence deployment efficiency. Market participants are addressing these challenges through localized distribution networks, strategic inventory management, and targeted partnerships supporting industrial customers operating in remote environments.

Brazil Market Outlook: Brazil dominates regional demand through its diversified industrial base, large mining sector, and expanding manufacturing activities. Industrial equipment modernization programs and infrastructure investments continue to strengthen lubricant consumption across construction, metals processing, and production industries. The country's growing focus on operational efficiency has encouraged broader adoption of premium lubrication products, while expanding domestic industrial activity supports stable long-term demand for maintenance and reliability solutions.

Industrial Diversification and Infrastructure Investment

Middle East & Africa is emerging as a high-priority market supported by industrial diversification strategies, energy infrastructure projects, and manufacturing expansion programs. The region contributes approximately 5% of global demand but is recording some of the strongest industrial deployment momentum. Large-scale infrastructure developments and industrial zone investments have increased equipment deployment activity by nearly 20% across several strategic markets. Demand remains concentrated in construction, power generation, mining, and industrial processing operations. Lubricant suppliers are expanding regional blending capabilities, distribution infrastructure, and technical service networks to capitalize on growing industrial activity and equipment maintenance requirements.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through large-scale industrial diversification initiatives, manufacturing investments, and infrastructure expansion programs. Industrial cities and energy-related projects continue to drive demand for hydraulic oils, gear oils, and heavy-duty industrial lubricants. The country has increased investment in industrial capacity development and advanced manufacturing initiatives, creating significant opportunities for suppliers capable of supporting complex industrial operations with specialized lubrication solutions and technical performance services.

The industrial lubricants market is led by global lubricant specialists including Shell, ExxonMobil, BP Castrol, TotalEnergies, Chevron, and FUCHS, competing against regional manufacturers and application-focused specialty suppliers. The top five players collectively control approximately 45–50% of market share, creating a moderately consolidated structure where scale and technical expertise determine competitive strength. Global leaders compete through product performance, supply reliability, and technical service capabilities, while regional suppliers focus on cost efficiency and localized distribution. Synthetic lubricant portfolios typically command 15–25% pricing premiums, while advanced formulations can extend lubricant life by more than 20%, strengthening value-based competition. Companies are expanding blending capacity, forming OEM partnerships, investing in condition-monitoring technologies, and pursuing vertical integration to secure feedstock availability. Competitive pressure is shifting toward digital maintenance ecosystems and application-specific formulations. Regulatory compliance, technical validation, and industrial service capabilities remain significant entry barriers. Winning requires performance differentiation, dependable supply networks, and strong industrial customer integration.

Shell plc

Exxon Mobil Corporation

BP Castrol

TotalEnergies SE

Chevron Corporation

FUCHS SE

Valvoline Inc.

Petro-Canada Lubricants

Idemitsu Kosan Co., Ltd.

ENEOS Corporation

Phillips 66 Lubricants

LUKOIL Lubricants Company

Petronas Lubricants International

Indian Oil Corporation Limited (Servo Lubricants)

Industrial lubricant technology is increasingly centered on synthetic base oils, advanced additive packages, and condition-monitoring systems that improve equipment reliability and maintenance efficiency. Synthetic lubricants now account for more than 40% of usage in high-load industrial applications, extending drain intervals by 20–30% and reducing component wear by approximately 15%. Compared with conventional mineral-based lubricants, next-generation synthetic formulations deliver up to 25% longer service life and improved thermal stability under continuous operating conditions. Manufacturers benefit through reduced downtime, lower maintenance frequency, and improved asset utilization across production-intensive environments.

Emerging technologies are transforming lubrication from a consumables function into a data-driven operational process. IoT-enabled lubricant sensors and predictive maintenance platforms are deployed in nearly 35% of large industrial facilities, helping reduce unplanned equipment failures by 12–18%. AI-assisted lubricant analytics improve maintenance planning accuracy by approximately 20%, while automated monitoring enables real-time contamination detection and performance optimization. Industrial operators are integrating lubrication data directly into enterprise asset management systems to strengthen operational visibility and lifecycle management.

Disruptive innovation is increasingly focused on bio-based formulations, smart lubrication ecosystems, and digital service models. Between 2026 and 2028, adoption of intelligent lubrication platforms is expected to exceed 45% among advanced manufacturing facilities. Global leaders with integrated digital monitoring capabilities, specialty formulations, and application-specific engineering support are positioned to outperform cost-focused competitors as industrial maintenance strategies become increasingly predictive and performance-driven.

If you want clickable links in the report, the correct format is:

April 2025 – FUCHS SE acquired IRMCO Advanced Metalforming Lubricant Technologies to strengthen its industrial metalworking lubricants portfolio and expand specialty manufacturing capabilities. The acquisition added more than 100 years of application expertise, improving FUCHS' position in precision metal-forming solutions.

July 2025 – Shell Lubricants completed the acquisition of Raj Petro Specialities, securing full ownership and expanding its specialty lubricants presence across industrial and power transmission applications in India. The transaction enhanced regional supply capabilities and broadened specialty product coverage. Source: shell.in

October 2025 – FUCHS SE acquired ASEOL SUISSE AG, integrating a long-standing Swiss distribution partner serving industrial, semiconductor, and medical technology customers. The combined operation includes approximately 40 employees, strengthening customer support and local market penetration. Source: fuchs.com

March 2025 – ENEOS Corporation announced restructuring of lubricant production operations at its Yokohama facility with annual lubricant production capacity of 126,000 kiloliters. The optimization program is designed to improve manufacturing efficiency and production network utilization. Source: reuters.com

This report provides comprehensive analysis of the industrial lubricants market across key product categories including Hydraulic Oils, Gear Oils, Compressor Oils, Metalworking Fluids, and Greases. It evaluates demand patterns across Machinery Lubrication, Metal Processing, Power Generation, Mining Operations, and Manufacturing Equipment applications while assessing purchasing behavior among Manufacturing, Mining, Power Generation, Construction, Oil and Gas, and Marine Industry end-users. The study covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, representing more than 95% of global industrial activity influencing lubricant consumption.

The report examines technology adoption trends including synthetic lubricants, predictive maintenance platforms, sensor-enabled monitoring systems, and advanced additive technologies. More than 40% adoption levels in premium lubricant applications and increasing deployment of digital asset management tools are assessed for their operational impact. Strategic insights include competitive positioning, supply-chain restructuring, industrial modernization programs, sustainability initiatives, investment priorities, and emerging application opportunities. The analysis supports expansion planning, product development, market entry decisions, partnership evaluation, and long-term competitive strategy development through 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 67891.79 Million |

|

Market Revenue in 2033 |

USD 92202.28 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shell plc, Exxon Mobil Corporation, BP Castrol, TotalEnergies SE, Chevron Corporation, FUCHS SE, Valvoline Inc., Petro-Canada Lubricants, Idemitsu Kosan Co., Ltd., ENEOS Corporation, Phillips 66 Lubricants, LUKOIL Lubricants Company, Petronas Lubricants International, Indian Oil Corporation Limited (Servo Lubricants) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |