Reports

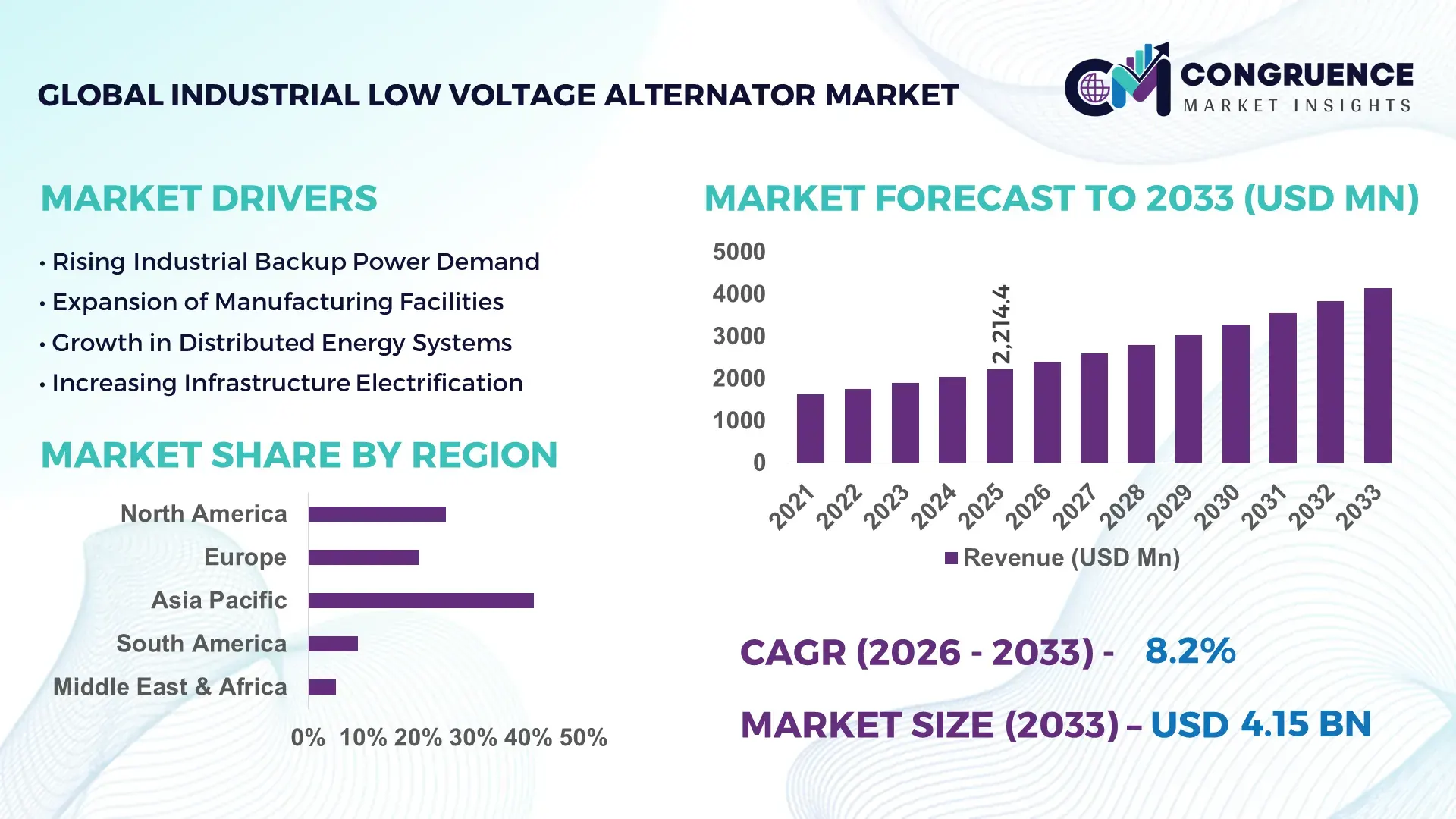

The Global Industrial Low voltage Alternator Market was valued at USD 2214.35 Million in 2025 and is anticipated to reach a value of USD 4147.43 Million by 2033 expanding at a CAGR of 8.16% between 2026 and 2033. Industrial electrification upgrades across manufacturing plants, distributed power systems, and backup energy infrastructure accelerated low voltage alternator installations by over 18% across heavy industrial facilities during 2025–2026.

China maintains dominant market influence with nearly 34% of global industrial low voltage alternator production capacity supported by more than USD 5.8 billion in electrical equipment modernization investments across industrial parks, petrochemical facilities, and export manufacturing zones. Advanced automation adoption in Chinese industrial plants exceeded 47% in 2026, strengthening demand for high-efficiency alternators integrated with digital voltage regulation and predictive monitoring systems. India and Southeast Asia recorded faster installation growth than Western Europe due to expanding captive power infrastructure and localized manufacturing expansion following Red Sea shipping disruptions and global supply chain realignment. Compared with conventional brushed systems, digitally regulated brushless low voltage alternators improved operational efficiency by nearly 14% while reducing maintenance intervals by 22%, particularly across mining, food processing, and industrial utility applications.

Manufacturers prioritizing localized component sourcing, smart monitoring integration, and high-efficiency industrial alternator platforms are strengthening competitive positioning across high-growth industrial economies.

Market Size & Growth: USD 2214.35 million in 2025 reaching USD 4147.43 million by 2033, driven by industrial backup power modernization and automated manufacturing expansion.

Top Growth Drivers: Industrial automation adoption increased 21%, distributed energy deployment rose 17%, and factory electrification projects expanded 19% globally.

Short-Term Forecast: By 2027, advanced low voltage alternators improve energy conversion efficiency by 13% while lowering maintenance downtime by 18%.

Emerging Technologies: AI-enabled predictive diagnostics, brushless rotor systems, and smart voltage regulation platforms improved operational reliability by over 16%.

Regional Leaders: Asia-Pacific exceeds USD 1.8 billion supported by manufacturing growth, Europe advances grid-resilient industrial systems, and North America strengthens data-driven power infrastructure deployment.

Consumer/End-User Trends: Nearly 44% of industrial operators shifted toward digitally monitored alternators for predictive maintenance and energy optimization.

Pilot/Case Example: In 2026, a Southeast Asian industrial cluster upgrade reduced unplanned equipment outages by 27% through smart alternator integration.

Competitive Landscape: Top manufacturers control approximately 39% market share, led by multinational electrical equipment suppliers and industrial power system specialists.

Regulatory & ESG Impact: High-efficiency alternator adoption lowered industrial energy losses by 11% under tightening energy efficiency compliance frameworks.

Investment & Funding: More than USD 3.2 billion supported factory automation partnerships, regional production expansion, and resilient supply chain localization initiatives.

Innovation & Future Outlook: Next-generation compact alternators with IoT-enabled monitoring and lightweight copper optimization are accelerating high-growth industrial deployment strategies.

Industrial manufacturing contributes nearly 41% of total demand for industrial low voltage alternators, followed by oil and gas processing and mining operations requiring continuous backup power reliability. Recent innovations include digitally controlled voltage stabilization systems and lightweight high-conductivity rotor materials improving operational efficiency by over 15%. Asia-Pacific continues leading installations due to expanding industrial infrastructure, while Europe prioritizes energy-efficient retrofits under tightening emissions regulations. Supply chain regionalization and localized component manufacturing are reshaping procurement strategies, with smart predictive maintenance integration emerging as a defining competitive trend for the next phase of industrial power infrastructure expansion.

The industrial low voltage alternator market is becoming strategically critical as manufacturers, utilities, and process industries prioritize uninterrupted power stability, localized production resilience, and energy-efficient electrical infrastructure. Industrial operators are replacing aging alternator systems with digitally regulated units to reduce downtime and improve operational continuity across automated production environments. Supply-chain restructuring after Red Sea shipping disruptions accelerated domestic sourcing initiatives in India, China, and Mexico, while industrial infrastructure modernization programs increased demand for compact high-efficiency alternators integrated with predictive maintenance systems.

Advanced brushless low voltage alternators deliver nearly 14% higher operational efficiency and reduce maintenance cycles by approximately 20% compared with legacy brushed systems widely used across older industrial facilities. China continues dominating large-scale deployment through high-volume manufacturing integration, while Germany emphasizes energy-efficient retrofits for precision engineering facilities. In the United States, industrial backup modernization projects within data-intensive manufacturing clusters increased smart alternator adoption by over 16% during 2025–2026. Over the next two years, digital monitoring integration across industrial power systems is expected to exceed 45% deployment penetration in newly commissioned facilities.

A 2026 petrochemical facility upgrade in Gujarat reduced unplanned operational stoppages by 24% through IoT-enabled alternator synchronization systems linked with automated load management platforms. Manufacturers are expanding regional assembly capabilities, securing copper supply agreements, and strengthening OEM partnerships to stabilize production efficiency and delivery timelines. Companies combining intelligent diagnostics, localized sourcing, and energy-efficient alternator platforms are establishing stronger competitive positioning across industrial modernization programs.

Industrial automation investments and rising captive power deployment across manufacturing-intensive economies are accelerating demand for industrial low voltage alternators. Factory automation penetration increased by nearly 21% across high-output industrial facilities during 2025–2026, while backup power integration within process industries expanded by approximately 18%. India’s industrial corridor expansion and China’s advanced manufacturing modernization programs intensified deployment of digitally regulated alternator systems supporting continuous operations. Industrial operators are prioritizing high-efficiency brushless configurations that reduce maintenance intervals by over 20% and improve voltage stability under fluctuating loads. In response, manufacturers are increasing regional production capacity, forming OEM supply partnerships, and integrating predictive diagnostics into alternator platforms. A notable operational shift involves companies redesigning alternators for modular industrial applications to shorten installation cycles and reduce equipment replacement downtime.

Copper price instability and dependency on imported electromagnetic components continue restricting scalability across the industrial low voltage alternator market. Copper winding material costs fluctuated by more than 15% during recent procurement cycles, directly impacting manufacturing margins and equipment pricing stability. Several industrial OEMs in Europe and Southeast Asia also faced delivery delays exceeding 12% due to semiconductor shortages affecting digital voltage regulation systems. High-efficiency alternator deployment remains constrained in smaller industrial facilities where modernization budgets remain limited despite rising operational energy costs. Companies are responding through localized component sourcing, long-term metal procurement agreements, and alternative conductor material development to reduce exposure to international supply-chain disruptions. A significant operational concern involves balancing lightweight alternator design requirements with thermal performance durability under high-load industrial environments.

Industrial electrification programs and smart monitoring integration are creating high-value opportunities across the industrial low voltage alternator ecosystem. Predictive maintenance deployment within industrial power systems increased by nearly 26% during 2026 as operators focused on reducing unscheduled downtime and maintenance labor intensity. Japan and South Korea are accelerating adoption of digitally synchronized alternators integrated with factory energy management software and automated diagnostics platforms. Emerging compact alternator designs using advanced insulation materials improved thermal efficiency by approximately 13% while lowering operational noise levels across precision manufacturing facilities. Companies are investing in IoT-enabled alternator platforms, AI-assisted fault analytics, and strategic partnerships with industrial automation firms to strengthen lifecycle service offerings. A non-obvious opportunity is developing alternator solutions optimized for hybrid industrial microgrids supporting renewable energy balancing and continuous power stabilization.

Integration complexity across digitally connected industrial power systems remains a major long-term challenge for industrial low voltage alternator deployment. Nearly 31% of industrial operators reported synchronization and compatibility issues when integrating advanced alternators with legacy electrical infrastructure and automated control architectures. Germany and the United States are facing skilled workforce shortages in industrial electrical maintenance, increasing commissioning timelines and operational dependency on specialized engineering contractors. Cybersecurity concerns surrounding connected monitoring systems also intensified as industrial facilities expanded remote diagnostics capabilities across energy infrastructure networks. Manufacturers must strengthen software interoperability, workforce training programs, and secure industrial communication protocols to maintain deployment consistency and operational reliability. A key strategic challenge involves scaling intelligent alternator ecosystems without increasing maintenance complexity or compromising long-term power quality performance across industrial facilities.

Smart Diagnostics Integration Rising Industrial operators increased deployment of IoT-enabled low voltage alternators by nearly 28% during 2025–2026 to strengthen predictive maintenance workflows and reduce unplanned shutdowns. Manufacturing plants in Germany and South Korea integrated cloud-based fault analytics with alternator monitoring systems, lowering maintenance response time by approximately 19%. Companies are restructuring service operations around remote diagnostics subscriptions and lifecycle monitoring contracts as labor shortages continue affecting industrial maintenance efficiency.

Localized Manufacturing Capacity Expansion Supply-chain disruptions and copper procurement volatility accelerated localized alternator assembly investments across India, Mexico, and Vietnam. Regional sourcing adoption increased by over 24% among industrial OEMs seeking shorter delivery cycles and reduced logistics exposure following Red Sea shipping instability. Manufacturers are expanding component partnerships and redesigning procurement networks to stabilize lead times, while modular alternator production reduced assembly turnaround by nearly 15% across high-volume industrial facilities.

Compact High-Efficiency Designs Advancing Demand for compact brushless alternators increased by approximately 22% as industrial facilities prioritized space optimization and lower thermal losses within automated environments. Advanced rotor cooling systems improved operational efficiency by nearly 13% compared with legacy industrial alternator platforms. Japanese industrial equipment manufacturers are scaling lightweight copper optimization technologies and automated winding systems to improve power density while reducing installation complexity across compact industrial machinery applications.

Hybrid Power Integration Accelerating Industrial microgrid deployment expanded by more than 18% as energy-intensive facilities integrated low voltage alternators with battery storage and renewable backup systems. Mining and oil processing operations in Australia and the United States adopted synchronized alternator platforms supporting hybrid load balancing and continuous operational stability during grid fluctuations. Companies are forming automation partnerships and investing in digital synchronization software to strengthen operational continuity while reducing fuel consumption across distributed industrial infrastructure.

Three Phase Alternators maintain dominant market share due to superior load handling capability, stable voltage output, and compatibility with high-capacity industrial equipment across manufacturing, mining, and utility operations. Nearly 48% of industrial installations during 2026 involved three-phase configurations because of their ability to support continuous heavy-load operations with lower transmission losses. Brushless Alternators represent the fastest-growing segment, with adoption increasing by approximately 23% as industrial operators prioritize reduced maintenance requirements and improved operational efficiency. Compared with traditional synchronous systems, advanced brushless designs lowered servicing frequency by nearly 20% in automated facilities. Diesel Generator Alternators continue holding strategic importance for remote industrial backup infrastructure, particularly across oil processing and construction applications. Single Phase Alternators remain relevant for smaller-scale industrial machinery and localized backup systems, while Synchronous Alternators are increasingly integrated into precision-controlled industrial environments requiring stable frequency management. Manufacturers are expanding smart alternator portfolios and investing in compact high-efficiency configurations to align with evolving industrial automation requirements.

Power Generation remains the leading application segment as industrial facilities increasingly depend on stable decentralized energy systems for continuous operations and voltage management. Nearly 42% of industrial low voltage alternator demand during 2026 originated from captive and distributed power generation infrastructure across manufacturing clusters and industrial parks. Backup Power Systems represent the fastest-growing application segment, expanding by approximately 25% due to rising concerns regarding grid instability, digital manufacturing continuity, and automated facility uptime requirements. Industrial Machinery applications continue expanding steadily as smart factories integrate digitally regulated alternators within robotic production systems and automated material handling equipment. Construction Equipment demand strengthened through infrastructure modernization projects in India and the Middle East, while Marine Applications increasingly adopted corrosion-resistant compact alternators supporting hybrid vessel operations. Oil and Gas Operations remain strategically important due to continuous-duty operational requirements across remote extraction and refining facilities. Companies are strengthening deployment capabilities through modular system integration, localized assembly, and predictive monitoring technologies.

Manufacturing remains the dominant end-user segment due to extensive deployment of industrial low voltage alternators across automated production facilities, process industries, and captive energy systems. Approximately 44% of total industrial alternator installations during 2026 were linked to manufacturing operations requiring continuous voltage regulation and operational redundancy. The Mining Sector is emerging as the fastest-growing end-user group, with deployment activity increasing by nearly 21% as mining operators modernize remote power infrastructure and hybrid energy systems. Oil and Gas companies continue prioritizing ruggedized alternator systems for high-load continuous-duty operations, while Utilities are expanding adoption within decentralized grid-support infrastructure and industrial substations. Construction companies increasingly favor compact high-output alternators supporting fuel-efficient heavy machinery operations, whereas the Marine Industry is integrating synchronized low voltage alternators into hybrid propulsion and onboard auxiliary power systems. Manufacturers are responding through application-specific product customization, long-term maintenance partnerships, and integrated digital monitoring solutions targeting industrial reliability and lower operational downtime.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Industrial Backup Modernization Strengthening Demand

North America represents a technologically advanced industrial low voltage alternator market driven by automated manufacturing infrastructure, industrial backup modernization, and smart power management integration. The region accounted for nearly 24% of global deployment activity during 2025, supported by high adoption across industrial processing facilities, logistics infrastructure, and utility-backed manufacturing operations. United States-based industrial operators increased predictive maintenance integration within alternator systems by approximately 18% during 2026 to reduce operational interruptions and energy losses. Industrial OEMs are strengthening domestic assembly capabilities and securing long-term component supply agreements to improve delivery stability amid semiconductor and copper procurement fluctuations. Investment momentum remains concentrated around digitally synchronized alternator systems supporting automated industrial facilities and resilient decentralized power infrastructure.

United States Market Outlook: The United States leads regional deployment through extensive industrial automation investments, advanced manufacturing infrastructure, and growing backup power integration across data-intensive industrial facilities. More than 46% of newly upgraded industrial power systems during 2026 incorporated digitally monitored low voltage alternators linked with predictive maintenance platforms. Domestic manufacturers are prioritizing localized production expansion and advanced rotor technology development to improve energy efficiency, shorten maintenance cycles, and strengthen operational resilience across industrial clusters in Texas, Ohio, and California.

Energy-Efficient Retrofitting Accelerating Industrial Adoption

Europe remains a strategically important market due to industrial energy-efficiency mandates, aging factory modernization programs, and advanced electrical engineering capabilities. The region contributed approximately 22% of global industrial low voltage alternator demand during 2025, with deployment concentrated across precision manufacturing, industrial utilities, and smart infrastructure projects. Germany, Italy, and France accelerated replacement of legacy alternator systems with digitally regulated brushless configurations capable of reducing thermal losses by nearly 12%. European manufacturers are increasingly integrating compact alternator architectures within automated production environments to align with stricter sustainability and operational reliability targets. Companies are also expanding regional engineering partnerships to strengthen localized servicing capabilities and improve lifecycle support efficiency across industrial facilities.

Germany Market Outlook: Germany dominates the European market through strong industrial automation penetration, precision engineering expertise, and large-scale factory modernization initiatives. Nearly 51% of industrial operators surveyed during 2026 prioritized energy-efficient electrical infrastructure upgrades linked with predictive maintenance integration. German manufacturers are investing in high-efficiency copper optimization technologies and intelligent synchronization platforms to support advanced manufacturing facilities, automotive production lines, and industrial robotics systems requiring uninterrupted power stability and precise voltage management.

Manufacturing Scale and Export Capacity Driving Leadership

Asia-Pacific leads the global industrial low voltage alternator market through large-scale manufacturing infrastructure, industrial electrification expansion, and competitive production economics. The region accounted for approximately 41% of global market activity during 2025, supported by rapid deployment across manufacturing corridors, mining facilities, and industrial backup systems. China and India increased industrial automation-linked alternator installations by more than 23% during 2026 as factories accelerated smart production upgrades and decentralized power integration. Regional manufacturers are expanding export-oriented production capacity and strengthening localized component ecosystems to reduce dependency on imported electromagnetic systems. Industrial clusters across Southeast Asia are also increasing adoption of compact brushless alternators supporting high-efficiency machinery and automated industrial workflows.

China Market Outlook: China remains the most influential market due to its extensive industrial manufacturing base, vertically integrated electrical equipment ecosystem, and strong infrastructure modernization investments. More than 34% of global industrial low voltage alternator production capacity is concentrated within Chinese manufacturing hubs. Domestic enterprises are accelerating deployment of digitally regulated alternators across petrochemical, heavy engineering, and export manufacturing facilities while increasing investment in automated winding technologies and intelligent monitoring systems to strengthen production efficiency and export competitiveness.

Industrial Infrastructure Upgrades Expanding Deployment

South America is experiencing rising industrial low voltage alternator demand driven by mining expansion, industrial backup modernization, and infrastructure rehabilitation programs. The region contributed nearly 7% of global industrial deployment activity during 2025, with Brazil and Chile representing the largest operational centers. Mining operators increased installation of ruggedized alternator systems by approximately 16% to support remote extraction facilities and hybrid energy integration projects. Industrial enterprises continue facing logistical bottlenecks and limited localized component manufacturing capacity, affecting delivery timelines and replacement cycles. Companies are responding through regional distribution partnerships, localized assembly investments, and deployment of modular alternator systems optimized for harsh industrial operating conditions and unstable grid environments.

Brazil Market Outlook: Brazil leads regional demand through large-scale mining operations, manufacturing activity, and infrastructure modernization initiatives supporting industrial electrification. Industrial backup power deployment across manufacturing facilities increased by approximately 14% during 2026 as operators prioritized operational continuity amid grid reliability concerns. Domestic engineering firms are expanding partnerships with international alternator manufacturers to strengthen technical servicing capabilities, improve equipment localization, and support long-duration industrial operations across mining, agriculture, and industrial processing sectors.

Energy Infrastructure Investments Accelerating Modernization

Middle East & Africa is emerging as the fastest-transforming industrial low voltage alternator market due to large-scale industrial infrastructure investments, oil processing modernization, and expanding decentralized power systems. The region accounted for nearly 6% of global market deployment during 2025, with strong demand concentrated across energy-intensive industrial operations and construction megaprojects. Gulf industrial operators increased deployment of digitally synchronized alternator systems by approximately 19% during 2026 to support continuous operations within petrochemical and utility facilities. Companies are investing in high-temperature-resistant alternator technologies and localized technical servicing networks to improve operational reliability under demanding environmental conditions. Industrial diversification programs across Saudi Arabia and the UAE are strengthening long-term deployment momentum.

Saudi Arabia Market Outlook: Saudi Arabia represents the region’s most strategically significant market due to extensive industrial diversification programs, refinery modernization, and large-scale infrastructure investment activity. More than 28% of newly commissioned industrial backup systems during 2026 incorporated smart low voltage alternators integrated with automated monitoring platforms. Industrial operators are expanding partnerships with international electrical equipment manufacturers to strengthen local assembly capabilities, improve maintenance responsiveness, and support continuous-duty industrial operations across energy, construction, and industrial manufacturing facilities.

Global electrical equipment leaders including Stamford, Mecc Alte, Leroy-Somer, Nidec, and Marathon Electric compete directly against regional alternator manufacturers and low-cost Asian OEM suppliers. The top five players collectively control nearly 44% of market activity through manufacturing scale, supply-chain integration, and advanced industrial power technologies. Competition increasingly centers on efficiency optimization, delivery speed, thermal performance, and predictive diagnostics integration, with digitally regulated alternators improving operational efficiency by nearly 14% compared with conventional systems. European manufacturers focus on precision-engineered high-efficiency systems, while Chinese suppliers compete aggressively on localized production and pricing advantages exceeding 12% cost reductions. Companies are expanding assembly facilities, securing copper procurement contracts, and integrating IoT-enabled monitoring platforms to strengthen lifecycle service offerings. Market consolidation accelerated through strategic industrial automation partnerships and vertically integrated component sourcing. High engineering certification requirements and electromagnetic component dependency remain significant entry barriers. Winning requires operational reliability, localized servicing strength, digital integration capability, and resilient industrial supply networks.

Stamford AvK

Mecc Alte

Leroy-Somer

Nidec Corporation

Marathon Electric

ABB

Siemens

Cummins Generator Technologies

WEG Industries

Kirloskar Electric Company

Caterpillar

Yanmar Holdings

Hyundai Electric

CG Power and Industrial Solutions

Industrial low voltage alternator technology is shifting toward digitally regulated brushless architectures integrated with predictive diagnostics and intelligent voltage control systems. Advanced digital AVR platforms improved voltage stability by nearly 15% compared with conventional analog regulation systems, while reducing maintenance intervention frequency by approximately 18%. More than 42% of newly deployed industrial alternators during 2026 incorporated IoT-enabled monitoring modules supporting real-time thermal analysis and remote fault detection. Manufacturing and utility operators benefit through reduced operational downtime, faster maintenance scheduling, and improved load management across automated industrial environments.

Emerging technologies between 2026 and 2028 include lightweight copper optimization, automated winding systems, and compact high-density rotor configurations designed for space-constrained industrial installations. Compared with legacy brushed alternators, modern brushless systems deliver nearly 14% higher operational efficiency and approximately 20% lower servicing requirements under continuous-duty conditions. Industrial OEMs in China, Germany, and India are accelerating adoption of synchronized alternator platforms integrated with industrial automation ecosystems and hybrid microgrid infrastructure.

Disruptive innovation is increasingly centered on AI-assisted diagnostics, QR-enabled service platforms, and hybrid-ready alternator synchronization technologies. Companies deploying digitally connected alternators gain stronger lifecycle service control, faster maintenance response, and improved energy optimization capabilities. Manufacturers investing early in intelligent monitoring integration and modular high-efficiency alternator systems are expected to strengthen competitive positioning across industrial modernization projects through 2028.

March 2025 – STAMFORD | AvK launched the AvK A7 alternator platform featuring over 20% size and weight reduction with enhanced digital AVR integration, improving operational flexibility and accelerating industrial deployment timelines. Source: STAMFORD | AvK

July 2025 – STAMFORD | AvK India shipped its first STAMFORD S9 LV alternator from the Ahilyanagar manufacturing plant, expanding local production capability up to 5600 kVA and strengthening export-focused industrial supply operations. Source: STAMFORD | AvK India

October 2025 – STAMFORD | AvK introduced QR-enabled alternators enabling instant maintenance access, product verification, and spare-part support, improving service efficiency and proactive maintenance management across newly deployed industrial systems.

March 2026 – Mecc Alte introduced its T-Type totally enclosed alternator range designed for harsh industrial environments, strengthening operational durability and expanding deployment suitability across dust-intensive manufacturing and energy applications. Source: Mecc Alte

The Industrial Low voltage Alternator Market report delivers detailed analysis across major alternator types including Brushless Alternators, Single Phase Alternators, Three Phase Alternators, Diesel Generator Alternators, and Synchronous Alternators. The study evaluates operational deployment trends across power generation, backup power systems, industrial machinery, marine applications, construction equipment, and oil and gas operations. More than 40% of market demand concentration is linked with manufacturing-intensive industrial environments requiring continuous power stability, automated monitoring integration, and high-efficiency electrical infrastructure modernization.

The report provides strategic regional assessment covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed country-level industrial insights. It analyzes emerging technologies including digital AVR systems, IoT-enabled diagnostics, hybrid microgrid synchronization, and predictive maintenance integration influencing deployment strategies between 2026 and 2033. The study supports competitive benchmarking, expansion planning, localization strategy development, supply-chain optimization, and industrial investment prioritization by examining operational shifts, enterprise adoption patterns, infrastructure modernization activity, and evolving industrial power management requirements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2214.35 Million |

|

Market Revenue in 2033 |

USD 4147.43 Million |

|

CAGR (2026 - 2033) |

8.16% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stamford AvK, Mecc Alte, Leroy-Somer, Nidec Corporation, Marathon Electric, ABB, Siemens, Cummins Generator Technologies, WEG Industries, Kirloskar Electric Company, Caterpillar, Yanmar Holdings, Hyundai Electric, CG Power and Industrial Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |