Reports

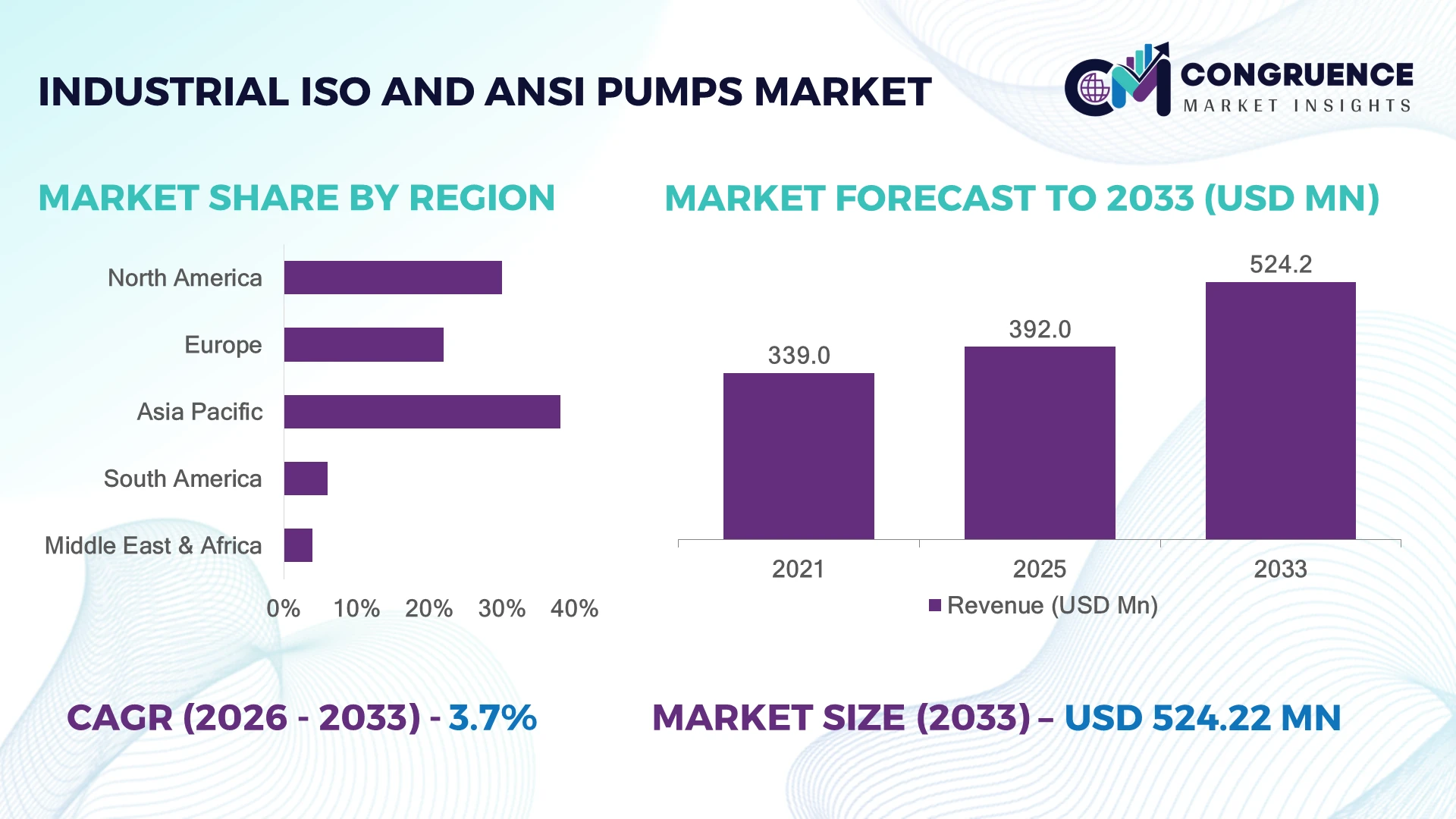

The Global Industrial ISO and ANSI Pumps Market was valued at USD 392.0 Million in 2025 and is anticipated to reach a value of USD 524.2 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is driven by rising adoption of energy-efficient centrifugal pumps, digital monitoring systems, and process optimization solutions across chemical, oil & gas, water treatment, and industrial manufacturing sectors.

China dominates the market landscape, accounting for approximately 28% of global industrial pump installations, supported by large-scale chemical processing, semiconductor, and water infrastructure investments. The country has deployed advanced pump automation across more than 60% of new industrial facilities, while the United States maintains strong demand through refinery modernization and manufacturing reshoring initiatives. Compared with Japan, China’s industrial pump capacity expansion is over 20% higher, reflecting rapid infrastructure upgrades following global supply-chain restructuring and energy security initiatives.

Strategic implication: Manufacturers prioritizing smart pumping solutions, energy efficiency, and localized production networks are positioned to capture long-term industrial demand.

Market Size & Growth: Valued at USD 392.0 Million in 2025 and projected at USD 524.2 Million by 2033, with 3.7% CAGR driven by energy-efficient pump upgrades and industrial automation.

Top Growth Drivers: Chemical processing modernization (35%), water infrastructure investment (28%), and digital pump monitoring adoption (22%) are the top growth contributors.

Short-Term Forecast: By 2028, advanced monitoring adoption is expected to reduce pump downtime by 15% and improve operational efficiency by 10%.

Emerging Technologies: AI-based predictive maintenance, IoT-enabled pump controls, and advanced corrosion-resistant materials are reshaping industrial pumping systems.

Regional Leaders: Asia Pacific is projected to exceed USD 220 Million with smart manufacturing adoption; North America is expected near USD 160 Million through refinery upgrades; Europe is forecast around USD 110 Million driven by energy-efficiency regulations.

Consumer/End-User Trends: Over 45% of industrial operators are integrating variable frequency drives and digital controls to optimize pump performance.

Pilot/Case Example: In 2024, industrial facilities implementing smart pump monitoring achieved up to 18% maintenance cost reduction through predictive analytics.

Competitive Landscape: Leading manufacturers hold significant global positions, including Flowserve Corporation, Sulzer Ltd., KSB SE & Co. KGaA, Grundfos, and Xylem Inc..

Regulatory & ESG Impact: Energy-efficiency standards and sustainability programs are pushing industries toward high-efficiency pumps, with optimized systems delivering 20–30% lower energy consumption.

Investment & Funding: More than USD 5 Billion in global industrial automation investments are supporting smart equipment partnerships, manufacturing expansion, and digital transformation initiatives.

Innovation & Future Outlook: Next-generation ISO and ANSI pumps will focus on AI diagnostics, modular designs, and connected industrial ecosystems to strengthen operational resilience.

Industrial ISO and ANSI pumps are experiencing increased demand from chemical plants, water treatment facilities, and process industries seeking reliable fluid-handling systems with lower operating costs. Recent innovations include sensor-integrated pump assemblies, magnetic drive technologies, and remote performance analytics, with digital monitoring adoption rising by nearly 25% across advanced industrial facilities. Global manufacturers are also strengthening regional supply chains amid equipment availability challenges and stricter efficiency standards.

Industrial ISO and ANSI pumps are becoming strategically important as manufacturers seek higher reliability, lower energy consumption, and improved process control across critical industries. The market is being reshaped by industrial automation, infrastructure modernization, and supply-chain localization strategies following global disruptions such as energy price volatility and manufacturing realignment.

Digitalized pump systems using IoT sensors and predictive analytics deliver measurable advantages over conventional equipment, reducing unplanned downtime by approximately 15% while improving maintenance planning. Compared with legacy fixed-speed pumps, variable-speed systems achieve energy savings of 20–30% in suitable industrial applications. North America and Europe are advancing through automation-focused upgrades and sustainability regulations, while Asia Pacific leads deployment scale due to expanding chemical, power, and manufacturing infrastructure.

Industrial operators are increasingly deploying smart ISO and ANSI pumps in applications such as water treatment networks and chemical processing plants to improve operational continuity. Leading manufacturers are expanding partnerships around connected equipment platforms, localized production, and lifecycle service models. Over the next few years, competitive advantage will depend on combining engineering reliability with digital intelligence, enabling companies to strengthen efficiency, resilience, and long-term industrial positioning.

Rising industrial automation and demand for energy-efficient fluid handling systems are accelerating ISO and ANSI pump adoption across chemical, pharmaceutical, and water-processing facilities. Smart pump installations are increasing by nearly 20%, while variable frequency drive integration is improving energy efficiency by 25–30% in optimized applications. China’s expansion of advanced manufacturing zones and the United States’ refinery modernization programs are strengthening replacement demand. Companies are responding through IoT-enabled pump platforms, predictive maintenance solutions, and localized manufacturing investments. The strategic shift toward lifecycle cost optimization is enabling manufacturers to compete beyond equipment sales through digital services and performance-based solutions.

Industrial ISO and ANSI pump manufacturers face pressure from fluctuating metal prices, specialized component shortages, and dependence on precision-engineered supply networks. Stainless steel and alloy material costs have experienced volatility exceeding 15% in recent supply cycles, while imported components account for over 30% of certain pump assemblies in developing manufacturing markets. Disruptions affecting machining hubs in Asia have increased lead times for critical components and impacted project execution schedules. Companies are mitigating these constraints through supplier diversification, regional sourcing agreements, and expanded inventory strategies. The key operational challenge remains maintaining competitive pricing while protecting manufacturing quality and delivery reliability.

The expansion of connected industrial infrastructure creates significant opportunities for advanced ISO and ANSI pump solutions integrated with sensors, analytics, and automation platforms. Digital monitoring adoption is growing across more than 40% of newly upgraded industrial facilities, enabling predictive maintenance and improved asset utilization. India’s chemical corridors and Southeast Asia’s manufacturing investments are creating new demand pockets for efficient pumping technologies. Companies are accelerating R&D partnerships around AI-based diagnostics, remote monitoring, and modular pump designs. A major strategic opportunity lies in transforming pumps from standalone mechanical assets into intelligent infrastructure components that generate operational insights and reduce total ownership costs.

The transition toward digitally connected ISO and ANSI pump systems faces execution challenges related to integration complexity, cybersecurity requirements, and limited technical expertise. Nearly 35% of industrial operators identify legacy equipment compatibility as a barrier to smart system deployment, while workforce shortages in industrial automation skills affect modernization timelines. Manufacturing facilities in countries such as Germany and Japan are addressing these issues through advanced training programs and automation partnerships. Companies must invest in interoperable platforms, cybersecurity frameworks, and technical support networks to ensure consistent deployment. Long-term competitiveness will depend on balancing mechanical reliability with digital capabilities across increasingly complex industrial environments.

Smart Pump Integration Shift Industrial operators are accelerating adoption of IoT-enabled ISO and ANSI pumps, with connected monitoring deployments rising by nearly 25% and predictive maintenance programs reducing unplanned downtime by 15–20%. Manufacturing plants in Germany and the United States are integrating real-time vibration, pressure, and flow analytics into pump workflows. Companies are responding by expanding digital service platforms and forming automation partnerships to convert traditional equipment sales into lifecycle management solutions.

Energy Optimization Focus High-efficiency pumping systems are gaining traction as industries prioritize energy reduction, with variable-speed pump adoption increasing by approximately 30% in upgraded facilities and energy savings reaching 20–35% in optimized operations. Stricter efficiency regulations in countries such as Japan are accelerating replacement of outdated equipment. Manufacturers are redesigning hydraulic systems and scaling premium-efficiency product lines to support lower operating costs.

Localized Manufacturing ExpansionSupply-chain restructuring is driving localized pump production, with industrial companies increasing regional sourcing by nearly 20% after component disruptions affected global equipment availability. India and Mexico are emerging as manufacturing hubs for industrial equipment supply networks. Pump manufacturers are expanding assembly capabilities, strengthening supplier ecosystems, and reducing dependency on single-source components to improve delivery reliability.

Advanced Materials Adoption Corrosion-resistant alloys, composite components, and improved sealing technologies are reshaping pump design, with advanced material usage increasing by over 15% in chemical and processing applications. The shift is particularly visible in aggressive fluid-handling environments where equipment lifespan is critical. Companies are investing in material innovation and customized engineering solutions to improve durability, reduce maintenance frequency, and support demanding industrial operations.

ANSI pumps represent the leading type segment due to their extensive use in North American chemical processing, refining, and general industrial applications. Their standardized dimensions, interchangeability, and broad aftermarket support make them attractive for facilities seeking simplified maintenance and reduced replacement complexity. ANSI pump installations account for nearly 55% of industrial pump deployments in applicable process industries, while manufacturers continue improving efficiency through upgraded impeller designs and smart monitoring compatibility. ISO pumps are emerging as the fastest-growing type as international manufacturers increasingly adopt standardized solutions for chemical, pharmaceutical, and water applications. Adoption is expanding by approximately 20% as global facilities prioritize modular equipment and cross-border engineering compatibility. Traditional pump categories continue serving specialized applications, but investment is shifting toward digitally integrated ISO and ANSI platforms. Companies are responding by expanding product portfolios, developing energy-efficient models, and strengthening regional service networks.

Chemical processing is the leading application segment due to continuous fluid transfer requirements, strict reliability standards, and demand for corrosion-resistant pumping solutions. Large-scale chemical facilities in China, the United States, and Germany are increasing investments in process optimization, with more than 40% of upgraded plants incorporating advanced monitoring systems. ANSI and ISO pumps remain essential for handling aggressive chemicals, improving operational continuity, and reducing maintenance interruptions. Water treatment and industrial utility applications represent the fastest-growing segment as governments and enterprises modernize infrastructure. Digital pump adoption in treatment facilities is increasing by nearly 25%, supported by automation initiatives and stricter resource-management policies. Oil & gas, power generation, and general manufacturing applications continue providing stable demand, but investment priorities are moving toward energy-efficient and remotely managed pumping systems. Companies are expanding integrated solutions combining hardware, analytics, and maintenance services.

Chemical and process industries remain the dominant end-user group because of intensive fluid-handling requirements, continuous operations, and demand for reliable pumping infrastructure. These industries contribute nearly 45% of advanced industrial pump usage across major manufacturing markets. Companies operating chemical plants are increasingly prioritizing corrosion-resistant materials, predictive maintenance, and customized pump configurations to improve asset performance. Water utilities and industrial infrastructure operators represent the fastest-growing end-user category as modernization programs expand across developing economies. Adoption of smart pumping technologies among utility operators is increasing by approximately 30%, driven by pressure to reduce energy consumption and improve operational visibility. Oil & gas companies, power producers, and manufacturing facilities continue upgrading legacy systems, while suppliers are developing service partnerships and application-specific solutions. Future competitiveness will depend on the ability to deliver reliable equipment combined with digital monitoring capabilities.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of4.2% between 2026 and 2033.

North America represents approximately 30% of global Industrial ISO and ANSI Pumps demand, supported by refinery upgrades, chemical processing investments, and manufacturing reshoring initiatives in the United States. The region has a high concentration of ANSI pump installations due to established process industries and extensive aftermarket networks. More than 50% of newly upgraded industrial facilities are integrating automation-enabled monitoring systems to improve equipment reliability. Companies are expanding service agreements, developing smart pump solutions, and strengthening domestic production capabilities to address supply-chain resilience requirements. The shift toward predictive maintenance and energy optimization is becoming a key differentiator among industrial equipment suppliers.

United States Market Outlook: The United States remains the dominant North American market due to its large chemical, pharmaceutical, and energy infrastructure base. More than 35% of industrial facilities adopting digital maintenance platforms are located within advanced manufacturing sectors across the country. Strong refinery modernization, semiconductor expansion, and industrial automation investments are supporting demand for high-performance ISO and ANSI pumping systems.

Europe accounts for nearly 22% of global Industrial ISO and ANSI Pumps adoption, driven by strict energy-efficiency standards, industrial decarbonization programs, and modernization of manufacturing facilities. Germany, Italy, and France represent major deployment centers due to strong chemical, automotive, and engineering industries. Approximately 40% of European industrial operators are prioritizing equipment upgrades that reduce energy consumption and improve lifecycle performance. Manufacturers are responding by introducing high-efficiency hydraulic designs, connected pump platforms, and sustainability-focused solutions aligned with European industrial policies. The region’s emphasis on operational efficiency is shifting purchasing decisions from initial equipment costs toward long-term asset performance.

Germany Market Outlook: Germany leads Europe through advanced engineering capabilities, industrial automation expertise, and a strong mechanical equipment manufacturing ecosystem. Over 45% of large manufacturing plants have adopted automation-driven equipment monitoring practices, supporting demand for intelligent ISO and ANSI pumps. Investments in industrial efficiency and smart factory infrastructure continue strengthening Germany’s position as a technology-focused market.

Asia-Pacific holds the largest market position with nearly 38% share, supported by extensive chemical production, water infrastructure projects, and manufacturing expansion in China, India, Japan, and South Korea. China contributes significantly through large-scale industrial capacity, accounting for more than 25% of regional pump installations across process industries. Rapid industrial automation adoption and infrastructure development are increasing demand for reliable fluid-handling systems. Companies are expanding local manufacturing facilities, forming technology partnerships, and improving supply-chain integration to serve growing industrial clusters. The region’s advantage comes from production scale combined with increasing adoption of digitally enabled pumping technologies.

China Market Outlook: China remains the key Asia-Pacific market due to its extensive chemical, power, and manufacturing infrastructure. More than 60% of newly developed industrial plants incorporate automated equipment management systems, creating strong demand for connected ISO and ANSI pumps. Domestic manufacturers are increasing production capabilities while international companies are establishing local partnerships to strengthen market access.

South America represents approximately 6% of global Industrial ISO and ANSI Pumps demand, supported by mining, oil processing, agriculture, and water infrastructure applications. Brazil and Chile account for major deployment activity due to resource-intensive industries requiring durable pumping systems. Around 30% of industrial facilities in major mining operations are upgrading equipment to improve reliability and reduce maintenance interruptions. However, infrastructure limitations and import dependency continue affecting project timelines. Companies are responding through regional service networks, local partnerships, and customized pump solutions designed for demanding operating environments. Resource-sector modernization remains the primary opportunity area for industrial pump suppliers.

Brazil Market Outlook: Brazil dominates the South American market due to its mining, energy, food processing, and industrial manufacturing base. The country’s industrial operators are increasingly adopting efficient pumping technologies, with approximately 20% growth in automation-focused equipment upgrades across large processing facilities. Local production partnerships are helping companies improve delivery capability and reduce dependence on imported components.

Middle East & Africa contributes nearly 4% of global Industrial ISO and ANSI Pumps demand, with adoption concentrated in oil & gas, desalination, petrochemicals, and infrastructure projects. Countries such as Saudi Arabia and the United Arab Emirates are investing heavily in industrial modernization and water security programs. More than 25% of new infrastructure projects are incorporating advanced pumping and monitoring technologies to improve efficiency and reliability. Companies are expanding regional service operations, forming engineering partnerships, and supplying customized pump systems for harsh operating environments. The region’s transition toward diversified industrial economies is creating new demand beyond traditional energy applications.

Saudi Arabia Market Outlook: Saudi Arabia represents the leading Middle Eastern market due to large-scale petrochemical facilities, desalination projects, and industrial diversification programs. Over 35% of major infrastructure developments include advanced fluid-handling requirements, supporting demand for reliable ISO and ANSI pumps. Industrial investment programs are encouraging suppliers to establish localized service capabilities and long-term maintenance partnerships.

The Industrial ISO and ANSI Pumps Market features competition between global OEM leaders such as Flowserve, Sulzer, KSB, Grundfos, and Xylem against regional manufacturers competing through cost efficiency and localized service networks. The top five players collectively account for approximately 45% of market presence, creating a moderately consolidated structure. Competition centers on pump efficiency, digital monitoring, customization, and supply-chain reliability, with advanced solutions improving operational efficiency by 15–25%. Global leaders are expanding smart pump portfolios, while regional suppliers focus on faster delivery and application-specific engineering. Companies are pursuing partnerships, manufacturing expansion, and vertical integration to strengthen lifecycle service capabilities. The competitive landscape is shifting toward connected pumping ecosystems, energy optimization, and resilient supply networks. High engineering expertise, certification requirements, and aftermarket infrastructure create significant entry barriers. Winning requires combining technological innovation, dependable supply chains, customization capability, and strong customer support.

Sulzer Ltd.

KSB SE & Co. KGaA

Grundfos

Xylem Inc.

Ebara Corporation

ITT Inc.

Pentair plc

Wilo SE

SPX FLOW, Inc.

Kirloskar Brothers Limited

ClydeUnion Pumps

Industrial ISO and ANSI pumps are increasingly adopting IoT sensors, digital twins, and predictive analytics to improve operational visibility. Smart monitoring platforms are reducing unplanned downtime by 15–20% and enabling condition-based maintenance. Deployment is expanding across chemical, water, and manufacturing facilities as companies prioritize asset optimization and remote diagnostics.

Advanced variable-speed drives, high-efficiency hydraulics, and corrosion-resistant materials are replacing conventional pump systems. Compared with fixed-speed legacy pumps, modern variable-speed solutions achieve 20–30% energy savings in suitable applications. Approximately 40% of industrial upgrades now include efficiency-focused pump technologies, giving manufacturers advantages through lower lifecycle costs and improved reliability.

From 2026 to 2028, AI-driven maintenance, connected pump ecosystems, and automated performance optimization will become major competitive differentiators. Global OEMs benefit from digital service models, while regional suppliers compete through customization and faster deployment. Companies acting now on intelligent pumping infrastructure will gain stronger operational resilience, reduced maintenance expenses, and improved industrial competitiveness.

March 2025 — Flowserve Corporation launched the INNOMAG® TB-MAG™ Dual Drive™ Pump, a sealless magnetic drive pump designed for hazardous chemical applications with enhanced containment protection. The innovation improves safety performance by eliminating leakage risks and strengthens Flowserve’s position in advanced chemical process pumping solutions. Source: www.ir.flowserve.com

March 2025 — Sulzer Ltd. introduced its Energy Optimization Service for centrifugal pumps, combining digital analysis, machine learning, and lifecycle monitoring. The solution targets energy-intensive industries and identifies efficiency improvement opportunities of up to 20–30% in selected pump systems, reducing energy costs and carbon impact. Source: www.sulzer.com

May 2025 — Grundfos expanded its production footprint in Brookshire, Texas, through a multi-million-dollar facility investment to increase manufacturing capacity and improve customer responsiveness in North America. The expansion supports shorter lead times and strengthens local supply capability for advanced pump solutions. Source: www.grundfos.com

February 2025 — Sulzer Ltd. expanded its Vadodara service center in India to strengthen support for oil & gas, power generation, and industrial customers. The upgraded facility enhances pump repair, retrofit, and lifecycle service capabilities, improving regional equipment reliability and maintenance responsiveness.

The Industrial ISO and ANSI Pumps Market Report provides comprehensive coverage across pump types, applications, end-users, regional markets, competitive positioning, and technology developments. The study evaluates ANSI pumps, ISO pumps, and emerging smart pumping solutions across chemical processing, water treatment, oil & gas, power generation, and industrial manufacturing sectors.

The report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into deployment trends, automation adoption, supply-chain dynamics, and enterprise investment priorities. Covering leading manufacturers and technology shifts, the report supports strategic decisions related to expansion planning, product development, partnerships, and competitive positioning. It highlights digital monitoring adoption, efficiency improvements, and evolving industrial requirements shaping market direction through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 392 Million |

| Market Revenue (2033) | USD 524.2 Million |

| CAGR (2026–2033) | 3.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Flowserve Corporation; Sulzer Ltd.; KSB SE & Co. KGaA; Grundfos; Xylem Inc.; Ebara Corporation; ITT Inc.; Pentair plc; Wilo SE; SPX FLOW, Inc.; Kirloskar Brothers Limited; ClydeUnion Pumps |

| Customization & Pricing | Available on Request (10% Customization Free) |