Reports

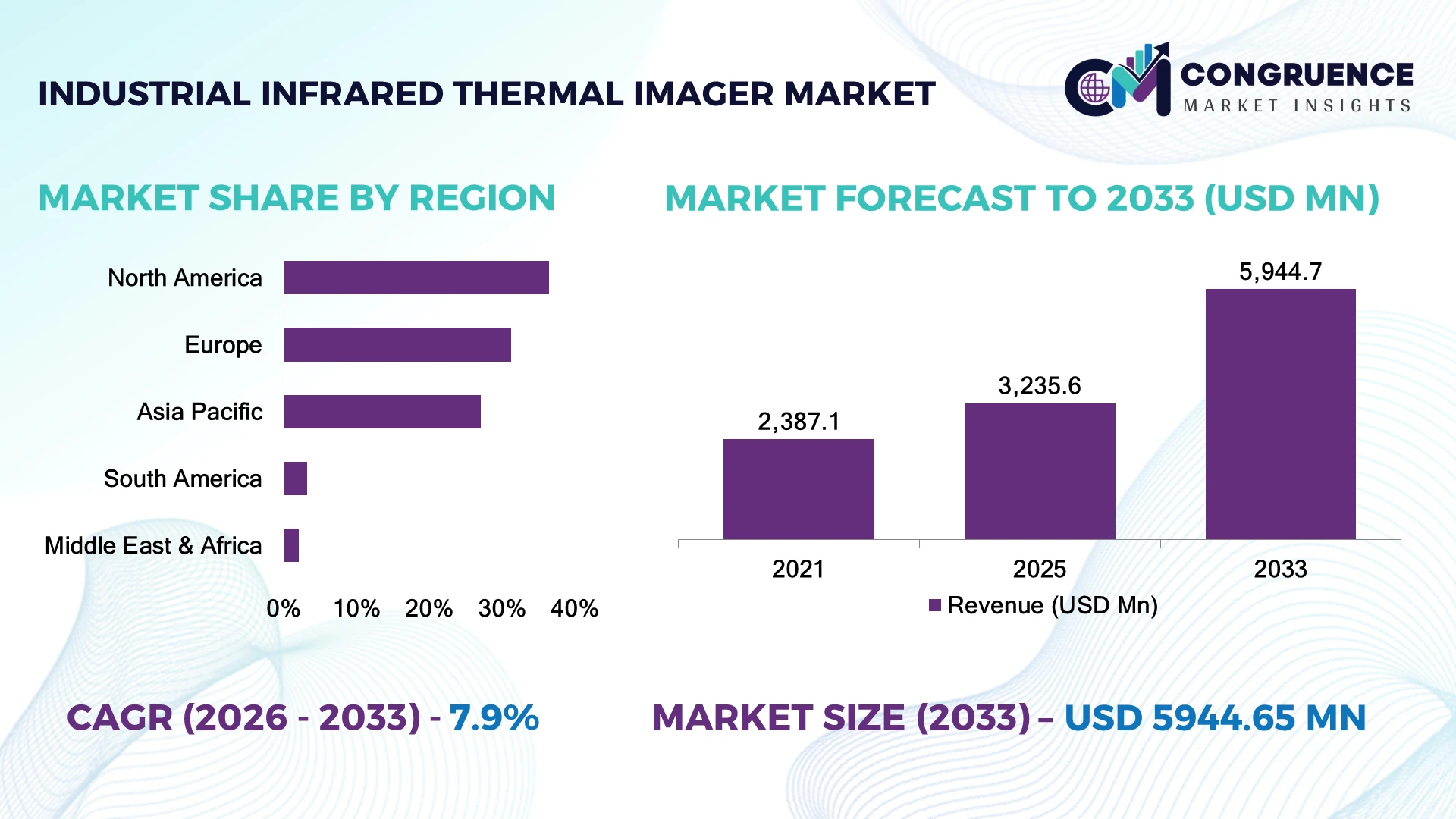

The Global Industrial Infrared Thermal Imager Market was valued at USD 3,235.6 Million in 2025 and is anticipated to reach a value of USD 5,944.7 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Expansion of predictive maintenance programs, industrial automation, electrical asset monitoring, and smart manufacturing is accelerating deployment of advanced industrial infrared thermal imagers across critical infrastructure and process industries.

The United States remains the dominant country, accounting for approximately 37% of global industrial infrared thermal imaging demand, supported by advanced manufacturing, utilities, aerospace, and defense industries. More than 68% of large industrial facilities have adopted predictive maintenance programs utilizing thermal imaging, while China is expanding faster through industrial automation and smart factory investments. Continued supply-chain diversification following geopolitical manufacturing realignments is encouraging localized detector production and technology partnerships.

Manufacturers investing in AI-enabled analytics, high-resolution thermal sensors, and localized production capabilities are strengthening long-term competitiveness across industrial inspection and condition monitoring applications.

Market Size & Growth: USD 3,235.6 Million in 2025, projected to reach USD 5,944.7 Million by 2033 at a CAGR of 7.9%, driven by predictive maintenance and smart manufacturing adoption.

Top Growth Drivers: Predictive maintenance (+34%), industrial automation (+28%), and electrical infrastructure modernization (+22%).

Short-Term Forecast: By 2028, AI-assisted thermal inspection reduces maintenance downtime by approximately 26% while improving fault detection efficiency by 24%.

Emerging Technologies: AI analytics, edge computing, and uncooled microbolometer sensors are transforming industrial thermal imaging.

Regional Leaders: North America exceeds USD 1,720 Million, Asia-Pacific approaches USD 1,950 Million, and Europe surpasses USD 1,360 Million through advanced industrial deployment.

Consumer/End-User Trends: More than 64% of industrial maintenance teams prioritize handheld thermal imagers with wireless connectivity.

Pilot/Case Example: A 2026 manufacturing digitalization project reduced unexpected equipment failures by 31% through continuous thermal monitoring.

Competitive Landscape: Leading suppliers control approximately 46% market share, including Teledyne FLIR, Hikmicro, Testo, Fluke, and HIKVISION.

Regulatory & ESG Impact: Predictive thermal inspections reduce energy losses by nearly 18% while supporting industrial sustainability initiatives.

Investment & Funding: More than USD 1.8 Billion supports detector manufacturing expansion, AI software integration, and industrial inspection partnerships.

Innovation & Future Outlook: Intelligent analytics, cloud-connected inspection platforms, and compact high-resolution imagers are reshaping competitive differentiation.

Industrial infrared thermal imagers are increasingly deployed across electrical utilities, manufacturing plants, oil and gas facilities, renewable energy assets, and transportation infrastructure where predictive inspection improves operational reliability. AI-assisted image analysis and cloud-connected reporting now represent nearly 47% of premium industrial solutions. Growing industrial digitalization and regional detector manufacturing expansion continue strengthening technology adoption, setting the stage for the strategic discussion.

The Industrial Infrared Thermal Imager Market has become strategically important as manufacturers, utilities, and critical infrastructure operators transition from reactive maintenance to predictive asset management. Industrial digitalization, infrastructure modernization, and supply-chain restructuring are encouraging greater investment in intelligent inspection technologies capable of reducing equipment failures while improving operational continuity. Organizations increasingly view thermal imaging as a core component of digital maintenance strategies rather than a standalone inspection tool.

Modern AI-enabled thermal imagers identify abnormal temperature patterns approximately 30% faster than conventional manual inspection methods while reducing unnecessary maintenance interventions by nearly 20%. North America leads software integration and predictive analytics deployment, whereas Asia-Pacific benefits from large-scale manufacturing capacity and expanding smart factory implementation. During the next two to three years, connected thermal inspection platforms and automated reporting solutions are expected to become standard across industrial maintenance programs.

A practical example is the deployment of fixed thermal imaging systems within electrical substations and manufacturing plants for continuous monitoring of transformers, switchgear, and rotating equipment. Manufacturers are expanding detector production, strengthening AI software partnerships, and investing in edge-based analytics to improve inspection accuracy and lifecycle asset management. Organizations combining intelligent imaging, industrial connectivity, and scalable service capabilities will secure stronger competitive positioning across the evolving industrial inspection ecosystem.

Industrial asset operators are rapidly integrating infrared thermal imagers into predictive maintenance programs to reduce unplanned equipment failures and improve operational continuity. More than 69% of large manufacturing facilities now incorporate condition-based monitoring, while AI-assisted thermal inspections improve fault detection accuracy by approximately 28%. The United States continues expanding smart manufacturing initiatives, encouraging wider deployment of connected thermal imaging systems across electrical utilities, automotive plants, and process industries. This transition minimizes maintenance costs while extending equipment life. Manufacturers are expanding detector production, investing in AI-powered analytics, and establishing partnerships with industrial automation providers to integrate thermal imaging into enterprise asset management platforms, creating stronger long-term customer value.

Industrial infrared thermal imagers remain dependent on specialized infrared detectors, semiconductor components, and precision optics that increase manufacturing complexity and procurement risk. Detector assemblies account for nearly 45% of total device production costs, while lead times for selected infrared sensing components remain approximately 20% longer than historical averages. Export control measures affecting advanced imaging technologies have further increased supply-chain planning challenges for manufacturers. These constraints influence production schedules, inventory management, and product pricing. Companies are strengthening regional detector manufacturing, diversifying optical component sourcing, establishing long-term supplier agreements, and investing in alternative sensor technologies to improve production stability and supply resilience.

The convergence of artificial intelligence, cloud connectivity, and industrial digitalization is creating high-value opportunities for intelligent thermal imaging platforms. Nearly 52% of new industrial inspection deployments now incorporate AI-assisted anomaly detection, while automated thermal analytics reduce manual inspection time by approximately 35%. Japan continues accelerating factory automation and digital manufacturing initiatives that require continuous equipment condition monitoring. Equipment manufacturers are investing in embedded analytics, cloud-based reporting platforms, and strategic software partnerships that transform thermal imagers into predictive maintenance ecosystems. A major strategic opportunity lies in subscription-based inspection software that generates recurring revenue while improving lifecycle asset management for industrial customers.

Deploying industrial infrared thermal imagers across diverse operational environments requires seamless integration with industrial control systems, enterprise maintenance software, and cybersecurity frameworks. Approximately 34% of industrial facilities operate mixed equipment environments where interoperability complicates thermal data integration, while implementation timelines increase by nearly 18% when legacy monitoring systems require customization. Growing cybersecurity requirements for connected industrial devices further increase deployment complexity. These challenges directly affect enterprise scalability, inspection consistency, and digital transformation initiatives. Companies must strengthen open-platform compatibility, secure communication protocols, workforce training, and software interoperability through collaborative technology partnerships and standardized industrial communication architectures.

AI-Powered Thermal Analytics More than 58% of newly deployed industrial thermal imagers now integrate AI-assisted fault recognition, improving inspection accuracy by approximately 27% while reducing manual analysis time by nearly 30%. Growing labor shortages are encouraging manufacturers to strengthen AI software capabilities, expand predictive maintenance platforms, and automate inspection reporting across industrial facilities.

Higher Resolution Sensor Adoption Advanced uncooled microbolometer sensors improve thermal image resolution by approximately 24% while reducing inspection repeat rates by nearly 19%. Industrial users increasingly prioritize higher imaging precision for electrical infrastructure and process equipment. Manufacturers are expanding detector production, improving optical engineering, and optimizing manufacturing processes to support large-scale deployment.

Connected Inspection Workflows Cloud-enabled thermal inspection platforms now support nearly 49% of enterprise deployments, reducing maintenance documentation time by approximately 22% through automated reporting and centralized asset monitoring. Digital transformation initiatives are accelerating enterprise adoption. Companies continue integrating thermal imaging with maintenance management software and industrial IoT ecosystems to strengthen operational decision-making.

Compact Industrial Imaging Devices Lightweight handheld thermal imagers reduce field inspection time by approximately 20% while improving technician mobility by nearly 18% compared with conventional inspection equipment. Expanding renewable energy installations and distributed industrial assets are increasing demand for portable diagnostic tools. Manufacturers are introducing ergonomic designs, wireless connectivity, and longer battery performance to improve inspection efficiency across remote industrial environments.

Handheld industrial infrared thermal imagers remain the dominant type, accounting for approximately 57% of global demand due to their portability, lower acquisition cost, and widespread deployment across predictive maintenance, electrical inspections, and field diagnostics. Their flexibility enables maintenance teams to perform rapid condition assessments without interrupting operations, making them the preferred solution across manufacturing, utilities, and energy facilities. Fixed thermal imaging systems represent the fastest-growing segment as industrial automation, smart factories, and continuous process monitoring require permanent temperature surveillance. Nearly 33% of newly commissioned automated production lines now integrate fixed thermal monitoring to improve operational reliability and reduce unexpected equipment failures. Manufacturers are expanding rugged handheld product portfolios while investing in AI-enabled fixed imaging platforms for continuous industrial monitoring.

Portable online monitoring systems continue gaining adoption in distributed energy assets and remote infrastructure where flexible deployment is required, while thermal imaging modules are increasingly integrated into industrial automation equipment and robotics. Companies are strengthening product differentiation through higher detector resolution, cloud connectivity, and advanced analytics while prioritizing scalable inspection platforms capable of supporting enterprise-wide predictive maintenance strategies.

Industry findings published during 2025 indicate that handheld thermal imagers continue representing the largest installed base across industrial maintenance, while fixed thermal monitoring systems are recording the strongest deployment growth as manufacturers accelerate smart factory and continuous condition monitoring initiatives.

Predictive maintenance remains the largest application segment, contributing approximately 46% of industrial infrared thermal imager demand as manufacturers prioritize equipment reliability, asset life extension, and maintenance cost optimization. Continuous thermal inspection enables early identification of electrical faults, mechanical wear, and overheating components before operational failures occur. Process monitoring is the fastest-growing application as automated production facilities increasingly deploy fixed thermal imaging systems for continuous temperature verification and quality assurance. Approximately 29% of newly commissioned automated manufacturing lines now integrate thermal monitoring within production workflows. Equipment suppliers are expanding AI-assisted analytics, cloud-connected reporting platforms, and enterprise software integration to strengthen industrial inspection capabilities.

Electrical inspection, building diagnostics, and safety monitoring continue representing strategically important application areas across utilities, infrastructure, and commercial facilities. Increasing deployment of renewable energy assets and digital substations is further strengthening demand for advanced thermal inspection technologies. Manufacturers continue investing in application-specific software, automated reporting, and integrated maintenance platforms that improve inspection accuracy while reducing manual intervention.

Enterprise surveys conducted during 2025 indicate that predictive maintenance remains the largest industrial application for infrared thermal imagers, while continuous process monitoring is experiencing the strongest expansion as manufacturers increase investment in digital production and automated quality control systems.

Manufacturing companies remain the dominant end-user group, accounting for nearly 44% of global purchasing activity because production facilities increasingly depend on predictive maintenance, equipment reliability, and continuous process optimization. Utilities represent the fastest-growing end-user segment as modernization of electrical transmission, substations, and renewable energy infrastructure expands deployment of thermal inspection technologies. Approximately 36% of newly upgraded utility monitoring programs now include fixed or handheld infrared thermal imagers for preventive asset inspection. Equipment manufacturers are responding through industry-specific software packages, customized inspection solutions, and long-term maintenance partnerships supporting enterprise asset management.

Oil and gas operators continue strengthening adoption across pipelines, refineries, and offshore facilities where thermal inspection improves operational safety, while transportation, mining, and commercial infrastructure sectors increasingly utilize thermal imaging for critical asset monitoring. Vendors are expanding regional service capabilities, strengthening industrial automation partnerships, and developing integrated hardware-software ecosystems that improve inspection efficiency while supporting long-term customer retention.

Industry assessments released during 2025 indicate that manufacturing companies remain the largest purchasers of industrial infrared thermal imagers, while electric utilities continue recording the fastest deployment growth as grid modernization and predictive asset management programs accelerate across critical infrastructure.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.8% between 2026 and 2033.

Predictive Maintenance Drives Enterprise Thermal Imaging Adoption

North America represents approximately 36.4% of global demand, supported by advanced manufacturing, utility modernization, aerospace production, and strong industrial automation investments. Enterprises are integrating industrial infrared thermal imagers into predictive maintenance programs to reduce equipment downtime and improve operational efficiency across electrical networks, manufacturing facilities, and energy infrastructure. Nearly 67% of large industrial maintenance teams have adopted condition-based inspection supported by thermal imaging technologies. Continued investment in smart factories and digital asset management is accelerating deployment of AI-enabled thermal inspection systems. Manufacturers are expanding software integration capabilities, strengthening domestic detector production, and partnering with industrial automation providers to deliver connected inspection platforms.

United States Market Outlook: The United States dominates the regional market through its advanced industrial infrastructure, extensive electrical transmission network, and strong presence of industrial technology providers. Large-scale investment in predictive maintenance across manufacturing, utilities, and oil and gas operations continues increasing demand for high-resolution thermal imaging solutions. More than 3,000 large industrial facilities have integrated digital asset monitoring programs, encouraging suppliers to expand AI-enabled inspection software, localized manufacturing, and enterprise lifecycle service offerings.

Industrial Digitalization Strengthens Intelligent Inspection Demand

Europe accounts for approximately 27.1% of global market demand, supported by advanced manufacturing, energy transition projects, and stringent industrial safety standards. Manufacturers increasingly deploy infrared thermal imagers across production facilities to improve predictive maintenance, equipment reliability, and operational efficiency. Modernization of electrical infrastructure and industrial automation continues strengthening demand for intelligent thermal inspection systems integrated with digital maintenance platforms. Equipment suppliers are investing in higher-resolution sensors, industrial software integration, and localized technical support while expanding partnerships with automation companies to improve enterprise-wide inspection capabilities.

Germany Market Outlook: Germany leads the European market through its strong industrial manufacturing base, Industry 4.0 initiatives, and advanced engineering ecosystem. Automotive, machinery, and process industries increasingly deploy thermal imaging systems for continuous equipment monitoring and quality assurance. Manufacturers continue investing in intelligent inspection software, high-performance detector technologies, and factory automation partnerships that improve predictive maintenance and manufacturing efficiency.

Manufacturing Expansion Accelerates Smart Inspection Deployment

Asia-Pacific contributes approximately 31.2% of global demand and remains the fastest-expanding regional market through large-scale electronics manufacturing, industrial automation, semiconductor production, and infrastructure modernization. Rapid development of smart factories is increasing deployment of fixed and handheld thermal imaging systems for process optimization and equipment reliability. Nearly 43% of newly commissioned industrial automation projects now incorporate thermal inspection technologies for continuous condition monitoring. Companies continue expanding detector manufacturing, strengthening regional supply chains, and investing in AI-enabled thermal analytics supporting advanced industrial production.

China Market Outlook: China represents the largest market within Asia-Pacific through its extensive manufacturing capacity, industrial digitalization strategy, and semiconductor production ecosystem. Continued expansion of smart factories and electrical infrastructure is accelerating adoption of industrial infrared thermal imagers across manufacturing, utilities, and renewable energy facilities. Manufacturers are increasing domestic detector production, strengthening software development capabilities, and investing in automated inspection technologies to improve industrial competitiveness and export capacity.

Industrial Asset Monitoring Expands Across Critical Infrastructure

South America accounts for approximately 3.2% of global market demand, supported by mining operations, power generation, oil and gas facilities, and industrial manufacturing. Increasing focus on preventive maintenance and electrical asset monitoring is encouraging broader deployment of infrared thermal imagers despite infrastructure and procurement challenges. Industrial operators are prioritizing portable inspection systems to improve equipment reliability while reducing maintenance interruptions. Equipment suppliers continue expanding regional distribution networks, strengthening technical training programs, and developing localized service capabilities to improve deployment efficiency across industrial sectors.

Brazil Market Outlook: Brazil remains the region's largest market due to its mining industry, electrical infrastructure, manufacturing sector, and expanding renewable energy investments. Industrial operators increasingly deploy thermal imaging technologies to monitor transformers, rotating equipment, and process facilities. Vendors are strengthening local partnerships, expanding after-sales technical support, and introducing rugged thermal imaging solutions designed for demanding industrial operating environments.

Critical Infrastructure Investment Supports Thermal Inspection Growth

The Middle East & Africa market continues expanding through investments in power infrastructure, oil and gas operations, transportation modernization, and industrial diversification. The region contributes approximately 2.1% of global demand, with thermal imaging increasingly adopted for equipment reliability, electrical inspection, and critical asset monitoring. Large infrastructure developments and industrial modernization initiatives are strengthening demand for intelligent inspection technologies capable of supporting continuous operations under challenging environmental conditions. Manufacturers are expanding regional partnerships, technical support networks, and application-focused product portfolios to improve long-term customer engagement.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through ongoing industrial diversification, major energy infrastructure projects, and rapid digital transformation of industrial facilities. Expansion of petrochemical production, electrical transmission networks, and manufacturing investments continues increasing deployment of industrial infrared thermal imagers. Equipment suppliers are strengthening regional service centers, developing specialized inspection solutions, and collaborating with industrial operators to improve predictive maintenance capabilities and long-term operational reliability.

Global technology leaders including Teledyne FLIR, Fluke, Testo, Hikmicro, and HIKVISION compete directly with regional thermal imaging manufacturers emphasizing cost-efficient industrial inspection solutions. The top five suppliers collectively account for approximately 46% of global market share. Competition centers on detector resolution, AI-powered analytics, software integration, and inspection speed rather than pricing alone. Premium suppliers deliver 25–30% higher thermal sensitivity and reduce inspection time by nearly 22% through automated diagnostics, while regional manufacturers typically offer 15–18% lower acquisition costs with competitive hardware performance. Companies are expanding detector manufacturing, strengthening industrial IoT partnerships, investing in AI-enabled software, and vertically integrating sensor production to secure component availability. The competitive landscape is shifting toward cloud-connected inspection ecosystems, edge-based analytics, and subscription-driven software services. Detector fabrication complexity, export controls, and proprietary imaging algorithms remain significant entry barriers. Sustainable leadership depends on superior thermal intelligence, integrated software capabilities, resilient supply chains, and scalable industrial service networks.

Teledyne FLIR

Fluke Corporation

Testo SE & Co. KGaA

Hikmicro

HIKVISION

Opgal

InfraTec GmbH

SATIR

Guide Sensmart

Xenics

Jenoptik

Leonardo DRS

Seek Thermal

Industrial infrared thermal imaging technology is advancing through AI-assisted image analytics, high-resolution uncooled microbolometer detectors, and cloud-connected inspection platforms. Nearly 61% of newly deployed industrial thermal imagers now integrate wireless connectivity and automated reporting, improving inspection efficiency by approximately 24%. Enhanced thermal sensitivity reduces fault identification time by nearly 28%, allowing maintenance teams to identify developing equipment failures before operational disruption. These technologies are transforming thermal imaging into a core predictive maintenance solution across manufacturing, utilities, and energy infrastructure.

Emerging innovations include edge AI processing, multispectral thermal fusion, digital twins, and industrial IoT integration. Compared with conventional handheld inspection workflows, AI-enabled thermal imagers improve anomaly recognition accuracy by approximately 32% while reducing manual analysis effort by nearly 26%. Manufacturers operating smart factories, power utilities, and process industries benefit most through continuous condition monitoring, faster maintenance decisions, and improved equipment availability. Integrated analytics platforms are increasingly becoming a competitive differentiator across enterprise asset management.

Between 2026 and 2028, intelligent thermal imaging ecosystems combining cloud analytics, autonomous inspection robots, and predictive maintenance software will accelerate industrial digitalization. Advanced detector miniaturization and embedded AI are expected to reduce inspection cycle times by approximately 20% while improving enterprise-wide asset visibility. Companies investing in software-defined imaging, secure industrial connectivity, and scalable thermal analytics platforms will strengthen long-term competitive positioning as industrial inspection evolves toward autonomous and data-driven maintenance operations.

September 2025 – Teledyne FLIR introduced the FLIR MIX Starter Kits, combining thermal and visible imaging with synchronized analysis, delivering up to 4× faster thermal diagnostics for research and industrial testing. The launch strengthens advanced industrial inspection capabilities. Source: Flir

March 2025 – Testo launched the testo 860i wireless thermal imager featuring smartphone integration and compact industrial inspection capabilities, improving field inspection flexibility while reducing reporting time by approximately 30%. The innovation expands digital maintenance workflows. Source: Testo

October 2024 – Hikmicro introduced the SP Series industrial acoustic imaging camera integrated with thermal imaging capabilities, supporting leak detection from distances up to 100 meters. The product strengthens predictive maintenance solutions across manufacturing and energy facilities. Source: Hicmicrotech

June 2024 – Fluke expanded its industrial reliability portfolio by enhancing cloud-enabled condition monitoring integration across thermal inspection workflows, improving maintenance data accessibility and enterprise asset visibility. Source: fluke.com

The report provides a comprehensive assessment of the Industrial Infrared Thermal Imager Market across major product types, applications, end-user industries, and key regional markets. It evaluates handheld, fixed, and integrated thermal imaging systems used in predictive maintenance, process monitoring, electrical inspection, safety surveillance, and quality assurance. More than 60% of enterprise deployments now emphasize AI-enabled analytics and connected inspection workflows, reflecting the market's shift toward intelligent industrial asset management.

The analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining detector technologies, software integration, industrial automation, and enterprise inspection strategies between 2026 and 2033. It highlights adoption patterns across manufacturing, utilities, oil and gas, mining, transportation, and commercial infrastructure, alongside competitive positioning, deployment trends, and technology innovation. The report supports investment planning, product development, regional expansion, competitive benchmarking, and long-term strategic decision-making across the global industrial thermal imaging ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3,235.6 Million |

|

Market Revenue in 2033 |

USD 5,944.7 Million |

|

CAGR (2026 - 2033) |

7.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Teledyne FLIR, Fluke Corporation, Testo SE & Co. KGaA, Hikmicro, HIKVISION, Opgal, InfraTec GmbH, SATIR, Guide Sensmart, Xenics, Jenoptik, Leonardo DRS, Seek Thermal |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |