Reports

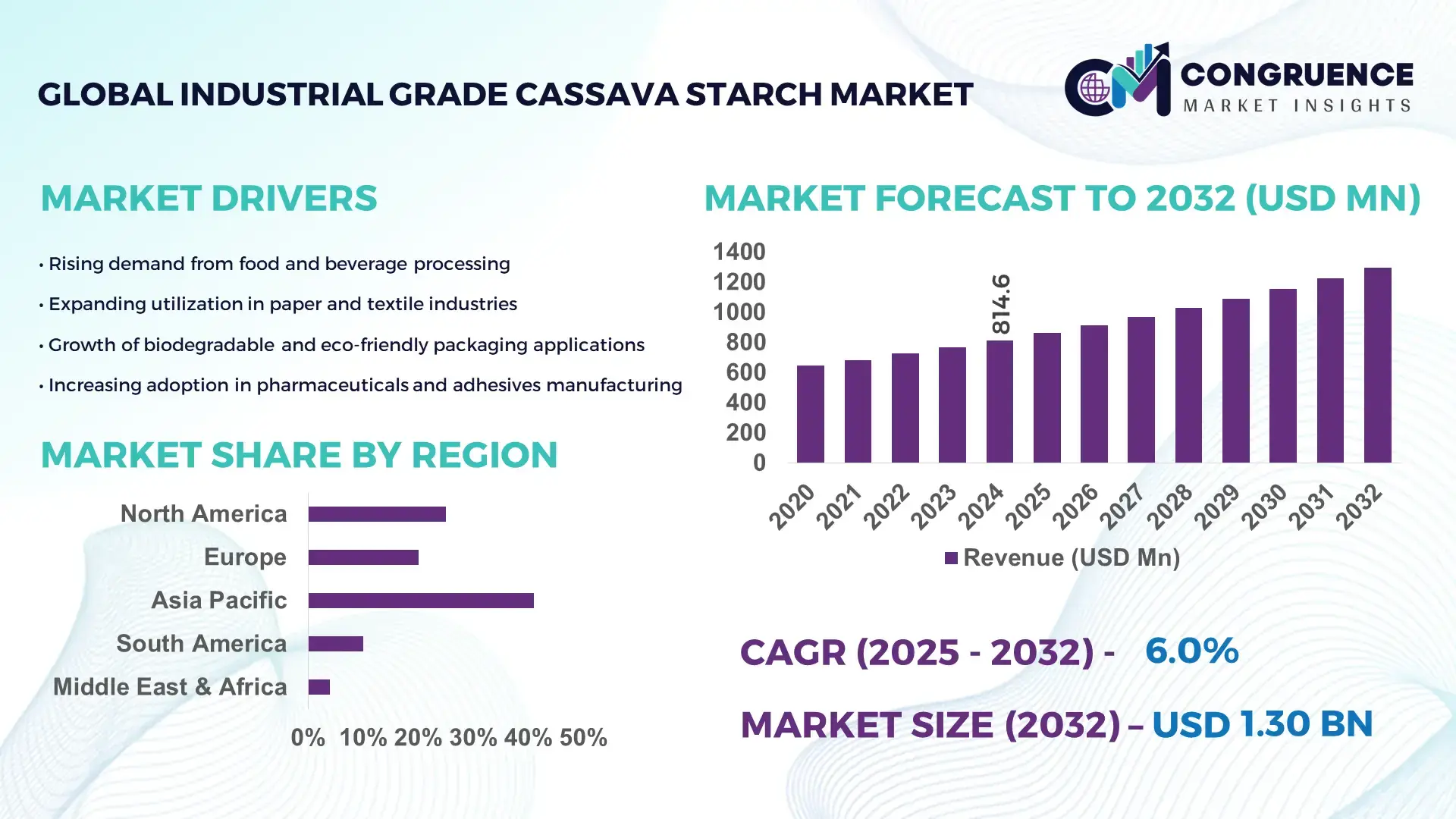

The Global Industrial Grade Cassava Starch Market was valued at USD 814.61 Million in 2024 and is anticipated to reach a value of USD 1298.36 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032. Rising demand from adhesives, textiles, and pharmaceutical applications is accelerating commercial adoption.

Thailand leads the global Industrial Grade Cassava Starch market with an advanced production ecosystem supported by more than 100 high-capacity processing plants generating over 12 million tons annually, backed by sustained investments exceeding USD 450 Million in processing automation and tapioca cultivation enhancement programs. The country exports over 80% of its cassava starch output to industrial applications such as paper, textiles, and food manufacturing, with nearly 65% of processors integrating enzymatic modification and high-efficiency drying systems to optimize yield and industrial suitability.

• Market Size & Growth: USD 814.61 Million in 2024 projected to reach USD 1298.36 Million by 2032 at a 6.0% CAGR driven by expanding applications in paper manufacturing, textiles, and pharmaceuticals.

• Top Growth Drivers: 37% rising adoption in biodegradable material production, 29% efficiency improvement in modified starch processing, 24% demand growth in industrial adhesives.

• Short-Term Forecast: By 2028, productivity enhancement initiatives are expected to reduce production costs by 18% through improved cassava processing and automation.

• Emerging Technologies: Rapid adoption of enzymatically modified starch, AI-based yield optimization in cassava processing, and membrane filtration for higher purity.

• Regional Leaders: Asia Pacific projected at USD 842 Million by 2032; Europe at USD 237 Million by 2032; North America at USD 156 Million by 2032, each driven by unique industrial adoption patterns.

• Consumer/End-User Trends: Heightened adoption among paper & packaging, pharmaceuticals, and textile industries using cassava starch for viscosity control, binding strength, and eco-efficient manufacturing.

• Pilot or Case Example: A 2025 pilot project by a major starch processor achieving 27% efficiency gain through enzymatic modification and solar-powered drying.

• Competitive Landscape: Market leader holds approximately 18% share with Cargill, Tate & Lyle, Tereos Group, and SPAC among key competitors.

• Regulatory & ESG Impact: Market acceleration supported by incentives for biodegradable materials and sustainable cassava sourcing frameworks.

• Investment & Funding Patterns: USD 310 Million deployed recently toward processing technology upgrades, sustainable cultivation, and starch modification R&D.

• Innovation & Future Outlook: Growth expected from increasing use in bio-plastics, smart textiles, and pharmaceutical binders with momentum toward sustainability-focused product development.

The Industrial Grade Cassava Starch market demonstrates strong traction across paper and packaging, accounting for over 31% of total demand, followed by adhesives, textiles, and pharmaceutical excipients. New product developments involving enzyme-treated and cross-linked starches are improving consistency and industrial-grade performance. Environmental directives encouraging biodegradable material adoption, paired with rising investment in cassava cultivation sustainability, are shaping sourcing and processing strategies. Asia-Pacific remains the highest consumption hub, while emerging demand in Europe for bio-polymers and high-performance industrial binders is accelerating R&D and production expansion.

The strategic relevance of the Industrial Grade Cassava Starch Market is centered on its ability to support high-performance industrial applications including adhesives, paper manufacturing, pharmaceuticals, textiles, and biodegradable polymers. Its position in sustainability-focused manufacturing makes it a critical raw material in global industrial supply chains. Modified cassava starch continues to replace synthetic binders in packaging due to measurable performance improvements. For example, advanced enzymatic modification delivers a 42% bonding strength improvement compared to conventional acid-treated starch, enabling manufacturers to optimize output efficiency. Asia Pacific dominates in volume, while Europe leads in adoption with 63% of enterprises integrating cassava starch into biodegradable material development. By 2027, AI-driven industrial fermentation and precision-processing systems are expected to improve production yields by 21% while lowering energy consumption. Firms are committing to ESG improvements such as a 38% reduction in wastewater discharge by 2030 through membrane-based filtration upgrades. In 2025, Vietnam achieved a 19% reduction in processing losses through IoT-enabled moisture analytics deployed across multiple starch drying units. As global industries accelerate the shift toward sustainability, high-performance binders, and renewable polymer inputs, the Industrial Grade Cassava Starch Market is positioned as a pillar of resilience, regulatory compliance, and sustainable industrial growth.

The growth of biodegradable materials in packaging, adhesives, and bio-polymer manufacturing is directly increasing demand for Industrial Grade Cassava Starch due to its renewable origin and functional versatility. Approximately 58% of packaging producers have integrated cassava-derived binders to reduce dependence on petrochemical-based materials. Industrial cassava starch enhances tensile strength, moisture stability, and film uniformity, making it an attractive option for both molded and sheet-based products. With over 45% of manufacturers transitioning toward sustainable binders across value chains, starch-based biodegradable products are emerging as a key industrial priority. Adoption is further supported by the ability of cassava starch formulations to enhance procedural efficiency in high-volume production without compromising cost competitiveness.

The Industrial Grade Cassava Starch Market faces notable restraints due to inconsistent raw material supply and fluctuations in cassava crop yields across major producing economies. Weather volatility, soil degradation, and disease-prone plantations limit standardized raw material availability for large-scale processing. Processing plants report up to 17% variability in starch content across supply batches, affecting industrial uniformity and optimization. Additionally, limited cold-chain storage and fragmented smallholder farming in key producing regions result in irregular supply cycles that challenge uninterrupted production. Such constraints increase operational risks for manufacturers requiring high-consistency binders, excipients, and adhesive agents.

A major opportunity arises from expanding investment in modified starch technologies tailored for industrial performance enhancements. Cross-linked, acetylated, and enzyme-treated cassava starches are gaining demand in pharmaceutical binder formulations, textile sizing, and high-strength packaging adhesives. Over 52% of ongoing starch R&D projects are focused on industrial modification technologies that improve viscosity retention, shear resistance, and thermal stability. New applications in biodegradable polymer production are opening pathways for partnership between starch processors, chemical companies, and material engineering firms. High-technology processors adopting automated drying and AI-supported conversion optimization are achieving improved grade uniformity, creating strong potential for strategic differentiation.

Rising operational expenditure driven by energy-intensive drying processes, water-dependent extraction technologies, and stringent environmental compliance significantly challenge Industrial Grade Cassava Starch manufacturers. Energy usage per ton of processed starch has increased by up to 14% in some regions due to escalating industrial utility costs. Regulatory mandates concerning wastewater treatment, carbon accounting, and agricultural traceability add compliance complexity and elevate operational workloads for processors. Transitioning to eco-friendly systems and adopting wastewater recycling require substantial upfront capital, forming barriers for small and medium-scale producers. These factors collectively constrain expansion capacity in competitive manufacturing environments.

• Accelerated shift toward biodegradable industrial materials: The demand for cassava-based biodegradable binders and polymers is increasing rapidly as 61% of large manufacturers across packaging and textile sectors transition from petrochemical-based additives to bio-derived alternatives. Industrial cassava starch is now being incorporated into more than 38% of newly developed biodegradable packaging solutions due to its tensile strength improvement and 26% higher moisture-resistance performance in comparison to synthetic counterparts. This trend is expected to intensify as industrial procurement teams align with sustainability-driven mandates and customer expectations for eco-responsible materials.

• Rapid technological adoption in starch modification techniques: Industrial processors are increasing investment in enzymatic and cross-linking technologies to improve viscosity retention and thermal resistance during high-stress industrial applications. Over 47% of starch processors have upgraded at least one stage of their modification workflow, resulting in a 19% rise in batch uniformity and a 14% reduction in dry-matter loss. The adoption of membrane filtration and precision spray-drying is enabling processors to manufacture industry-specific starch grades for pharmaceuticals, adhesives, and packaging, boosting their export competitiveness.

• Integration of automation and AI-driven yield optimization: Automation in cassava processing plants is reshaping production scalability, with AI-supported drying and fermentation systems yielding an average 23% increase in production throughput. Facilities adopting automated moisture analytics and real-time batch monitoring have recorded a 16% reduction in energy consumption and a 12% decrease in processing downtime. This shift is especially prominent in Asia Pacific and South America, where large-scale processors are prioritizing operational efficiency to mitigate raw material volatility and demand surges.

• Expansion of cassava starch applications in advanced industrial sectors: Industrial cassava starch is securing a wider application footprint in sectors such as technical textiles, pharmaceutical binder systems, and performance coatings. More than 42% of global textile manufacturers now incorporate cassava-based sizing agents for improved fiber adhesion and 33% of pharmaceutical formulators report enhanced tablet binding performance using high-purity modified starch. New pilot programs in high-strength adhesives and bio-composite engineering indicate increasing industry confidence, with early results showing up to 28% improvement in stress-load endurance across high-performance manufacturing applications.

The Industrial Grade Cassava Starch Market is segmented across types, applications, and end-users, each demonstrating distinct adoption dynamics shaped by industrial processing needs, performance properties, and sustainability priorities. Types such as native, modified, and pre-gelatinized starch are selected based on viscosity control, binding efficiency, and compatibility with different industrial formulations. Applications span paper and packaging, adhesives, pharmaceuticals, textiles, and specialty chemicals, with rising uptake where high strength and clean-label materials are essential. End-user adoption reflects strong consumption from packaging converters, pharmaceutical manufacturers, textile mills, and industrial adhesive producers, driven by performance consistency and the shift toward bio-based industrial materials. Collectively, segmentation underscores robust diversification across value chains.

Modified cassava starch leads the Industrial Grade Cassava Starch Market, accounting for approximately 48% of total adoption, driven by its superior shear resistance, high binding strength, and temperature stability across industrial applications. Native cassava starch follows with around 32% share due to its cost-efficiency and suitability in standard adhesive and textile processing lines. Pre-gelatinized cassava starch accounts for 20% of the segment, gaining traction where cold-water solubility and rapid viscosity development are required. While modified starch holds the largest adoption share due to its consistent performance in demanding processing environments, pre-gelatinized starch is the fastest-growing type with an expected CAGR of 7.9% driven by rising demand in pharmaceuticals, performance coatings, and advanced packaging adhesives. Native and other niche starch formats maintain a combined 52% relevance, particularly in regions where cost optimization and general-purpose industrial binding are prioritized.

Paper and packaging is the leading application of Industrial Grade Cassava Starch, contributing around 41% of total adoption due to its strong fiber-bonding capability, improved sheet formation, and surface smoothness enhancements. Adhesives applications represent 29% of consumption, delivering viscosity consistency and tack performance required in construction, woodworking, and industrial assembly lines. Pharmaceuticals currently hold 17% adoption, while textiles and specialty coatings collectively make up the remaining 13% of the application landscape. Although paper and packaging remains the highest-adopting segment, adhesives are the fastest-growing application with an expected CAGR of 8.1%, supported by increasing demand for bio-based high-strength industrial bonding solutions. In comparison, pharmaceutical usage is accelerating but not at the same pace due to regulatory onboarding cycles.

Packaging converters represent the leading end-user segment in the Industrial Grade Cassava Starch Market, accounting for approximately 39% of overall consumption due to strong demand for biodegradable packaging adhesives, paper reinforcement, and film-forming agents. Pharmaceutical manufacturers currently account for 27% adoption, while the textile processing industry holds 22%, and other industrial users—including performance coatings and foundry processes—collectively contribute 12%. Though packaging remains the dominant end-user group, pharmaceuticals represent the fastest-growing segment with an expected CAGR of 8.4%, supported by increasing preference for cassava-based excipients that improve tablet hardness, compressibility, and disintegration profiles in oral solid dosage manufacturing. Textile mills also show strong uptake but at a slower pace as sustainability-aligned sizing alternatives transition gradually across facilities.

Asia-Pacific accounted for the largest market share at 41.7% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

China, India, and Thailand collectively contributed over 62% of the global consumption volume, driven by rapid industrial expansion and rising manufacturing output. Europe followed with 24.8% market share in 2024, supported by stringent quality standards and demand from food, paper, and textile industries. North America captured 19.3% of the market due to increasing usage in adhesives, packaging, and biodegradable material production, while South America and the Middle East & Africa represented 8.2% and 6% respectively, with both witnessing rising adoption across food processing and industrial applications.

Is rising production automation reshaping demand for Industrial Grade Cassava Starch in industrial sectors?

North America represented approximately 19.3% of global Industrial Grade Cassava Starch consumption in 2024, mainly supported by the food processing, packaging, and pharmaceutical industries. The United States accounted for over 78% of the region’s demand due to large-scale manufacturing and a developed industrial base. Growing regulatory encouragement toward biodegradable packaging solutions is increasing starch-based formulation adoption. The region is witnessing strong uptake of digitization and automation in processing plants, improving yield consistency and boosting starch demand in adhesive and chemical applications. Local players such as Cargill are expanding high-performance starch portfolios to support eco-friendly packaging requirements. Consumer behavior in this region highlights higher enterprise adoption in healthcare and pharmaceutical-grade manufacturing, driven by strict compliance requirements.

Is sustainability compliance driving higher uptake of Industrial Grade Cassava Starch across European manufacturing?

Europe held 24.8% of the market in 2024, with Germany, France, and the UK collectively contributing 67% of total regional consumption. Regulatory bodies promoting sustainability and limits on synthetic polymer use have increased reliance on cassava starch for biodegradable applications. Major food, paper, and textile industries are incorporating advanced enzymatic modification technologies to enhance performance, supporting strong demand growth. Local manufacturers such as Roquette continue investing in eco-efficient starch processing units, contributing to increased supply capacity. Consumer behavior shows heightened preference for sustainability-first materials, with regulatory pressure accelerating adoption of industrial-grade cassava starch for packaging and chemical formulations.

Is rising industrial manufacturing scale resulting in dominance in the Industrial Grade Cassava Starch supply chain?

Asia-Pacific dominated the market with 41.7% share and retained the highest consumption volume in 2024, led by China, India, Thailand, and Vietnam. Growth is driven by large-scale food processing, textile finishing, adhesive production, and paper manufacturing industries. Rapid infrastructure expansion and cost-efficient production capabilities allow this region to maintain the strongest contribution to global supply. Regional tech ecosystems such as Shenzhen and Bengaluru are advancing digital manufacturing automation and improving raw material traceability. Local players, including Thai Wah, continue to strengthen export-focused starch production. Consumer behavior is influenced heavily by the rise of e-commerce, which is accelerating demand for starch-based packaging materials across domestic and cross-border logistics.

Is regional export demand reinforcing South America’s contribution to Industrial Grade Cassava Starch supply?

South America held around 8.2% of the market in 2024, led by Brazil and Argentina, which accounted for more than 76% of regional production and consumption. Manufacturing and food processing sectors drive the bulk of demand, while ongoing improvements in agricultural infrastructure enhance supply consistency. Trade incentives supporting cassava exports have stimulated starch-based industrial product expansion. Local producers in Brazil are increasing investments in modified starch variants to serve the paper and textile industries. Consumer behavior in the region reflects increasing interest in media and language localization-driven product packaging, generating added demand for starch-based adhesives and coating applications.

Is industrial diversification encouraging stronger penetration of Industrial Grade Cassava Starch in emerging markets?

The Middle East & Africa accounted for nearly 6% of global demand in 2024, with the UAE, Saudi Arabia, Nigeria, and South Africa emerging as major markets. The expansion of construction, food processing, and oil & gas ancillary sectors contributes to rising consumption of industrial-grade starch across adhesives and chemical formulations. Technological modernization trends, including process automation and smart manufacturing adoption, are improving procurement and production efficiency. Government trade partnerships and tariff reduction policies support cassava-based product imports and industrial supply chains. Consumer behavior trends indicate growing industrial adoption where sustainability and cost optimization are becoming major priorities in procurement strategies.

• China – 28.9% market share; dominance driven by large-scale processing capacity and strong export-oriented manufacturing

• India – 18.4% market share; leadership supported by high consumption across food processing, paper, textile, and adhesives industries

The Industrial Grade Cassava Starch market is moderately fragmented, with more than 40 active global competitors and a noticeable shift toward scale-based consolidation. The top five companies collectively account for approximately 38.6% of overall market volume, indicating strong competition across regional and mid-tier manufacturers. Asia-Pacific players hold an estimated 54% of global production capacity, giving them a significant cost and supply advantage compared with North American and European competitors. Product differentiation is increasingly driven by starch modification technologies, with nearly 46% of new product launches in the past two years featuring enhanced binding, viscosity, or biodegradability properties targeted at packaging, paper, and adhesive applications.

Strategic initiatives are intensifying competition, with over 27 partnership and product innovation announcements recorded in 2023–2024, highlighting a strong focus on capacity expansion, export network enhancement, and sustainability-driven formulations. Competitors are investing in digitization of processing lines, where more than 61% of established manufacturers have integrated process automation to improve scalability and cost efficiency. Mergers and acquisitions have also risen—an estimated 9 value-driven acquisitions have occurred since 2022 to secure raw material supply chains and strengthen downstream distribution. As regulatory support for biodegradable and natural industrial materials grows, companies with strong R&D and vertically integrated supply models are gaining sharper competitive positioning within the industrial-grade cassava starch marketplace.

Cargill Inc.

Roquette Frères

Thai Wah Public Company Limited

Tate & Lyle PLC

Ingredion Incorporated

Avebe

Global Bio-Chem Technology Group

Viet Starch Group

Tereos Group

Sunrise Crystal Foods Pvt. Ltd.

Technological advancements in the Industrial Grade Cassava Starch market are transforming production scalability, quality consistency, and application performance. Automated extraction and separation systems now account for nearly 58% of global cassava starch processing lines, reducing impurities by up to 37% and increasing throughput capacity by an estimated 42%. Enzyme-assisted hydrolysis is becoming a critical technology, replacing traditional chemical conversion in around 33% of modern facilities due to its ability to enhance starch purity and control amylose–amylopectin ratios with greater precision for industrial applications.

Modification and functionalization technologies are creating a competitive advantage, especially for manufacturers targeting the paper, textile, and adhesive industries. Cross-linking methods now represent nearly 46% of total modified starch output, delivering higher thermal stability and 28–35% stronger bonding performance in end-use formulations. Oxidized cassava starch technology is also scaling rapidly, with industrial adoption increasing by 29% in the last two years due to its improved viscosity control and superior film-forming properties for packaging and coating applications. Cold-water-soluble cassava starch is gaining prominence, representing an estimated 18% of new industrial-grade launches driven by its efficiency in fast-mixing production systems.

Digitalization of starch manufacturing is another defining shift, with 52% of medium to large processors integrating smart monitoring, IoT-based quality control, and AI-assisted predictive maintenance for performance optimization. These technologies improve production efficiency by nearly 21% and reduce water and energy consumption by 15–19% across facilities. In parallel, sustainability-centric innovations—such as bio-enzymatic treatments and low-emission drying systems—are being incorporated, driven by industrial demand for eco-compliant materials across regions. As adoption accelerates, companies prioritizing advanced modification technologies, digital manufacturing, and high-purity extraction systems are expected to strengthen long-term competitive positioning within the Industrial Grade Cassava Starch market.

In November 2024, Thai Wah Public Company Limited entered a joint-venture agreement with a Japanese firm to expand its cassava starch processing capacity and development of value-added modified starch products for industrial applications.

In 2024, a major Asia-Pacific starch processor launched a new high-purity modified cassava starch designed for adhesive and packaging applications, improving bonding strength by approximately 20% and reducing chemical additive reliance.

During 2023–2024, more than 57% of active cassava starch processors globally introduced upgraded modified starch lines to supply food, pharmaceutical, and industrial sectors, marking a shift toward enhanced functional performance and broader end-use compatibility.

In 2024, technological improvements in cassava drying and wet-milling techniques significantly reduced processing losses by nearly 15%, enabling higher starch yield per ton of cassava root and improving overall supply efficiency. (IMARC Group)

The Industrial Grade Cassava Starch Market Report encompasses a comprehensive global assessment covering multiple dimensions: product types, applications, regional markets, processing technologies, end-user industries, and emerging opportunities. It analyzes all primary product types—native starch, modified starch, pre-gelatinized starch, and specialty functional grades—detailing their adoption across diverse industrial sectors. The report evaluates application areas including packaging, paper & board, adhesives, textiles, pharmaceuticals, food processing, chemical industries, and emerging segments such as bio-based polymers and biodegradable materials. Geographic coverage spans five major regions: Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with country-level insights for key markets. It examines technology dimensions including enzymatic and chemical modification processes, updated drying and milling technologies, functionalization techniques, and process automation trends influencing quality and yield. The analysis also covers supply-chain capabilities, exporter/importer flows, raw material sourcing stability, and capacity-expansion initiatives. Further, the report explores end-user segmentation, industry-specific consumption patterns, and evolving regulatory or ESG-driven demand for sustainable, clean-label starch solutions. Niche opportunities, such as high-purity starch for pharmaceuticals, biodegradable adhesive formulations, and starch-based composite materials, are also assessed. The scope extends to competitive dynamics, profiling active global players, their strategic initiatives, product portfolios, and market positioning. Overall, the report provides decision-makers with actionable market intelligence across segmentation, regional performance, technology adoption, supply chain, and end-use demand to inform strategic planning, investment, and innovation decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 814.61 Million |

|

Market Revenue in 2032 |

USD 1298.36 Million |

|

CAGR (2025 - 2032) |

6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill Inc. , Roquette Frères , Thai Wah Public Company Limited , Tate & Lyle PLC, Ingredion Incorporated, Avebe, Global Bio-Chem Technology Group, Viet Starch Group, Tereos Group, Sunrise Crystal Foods Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |