Reports

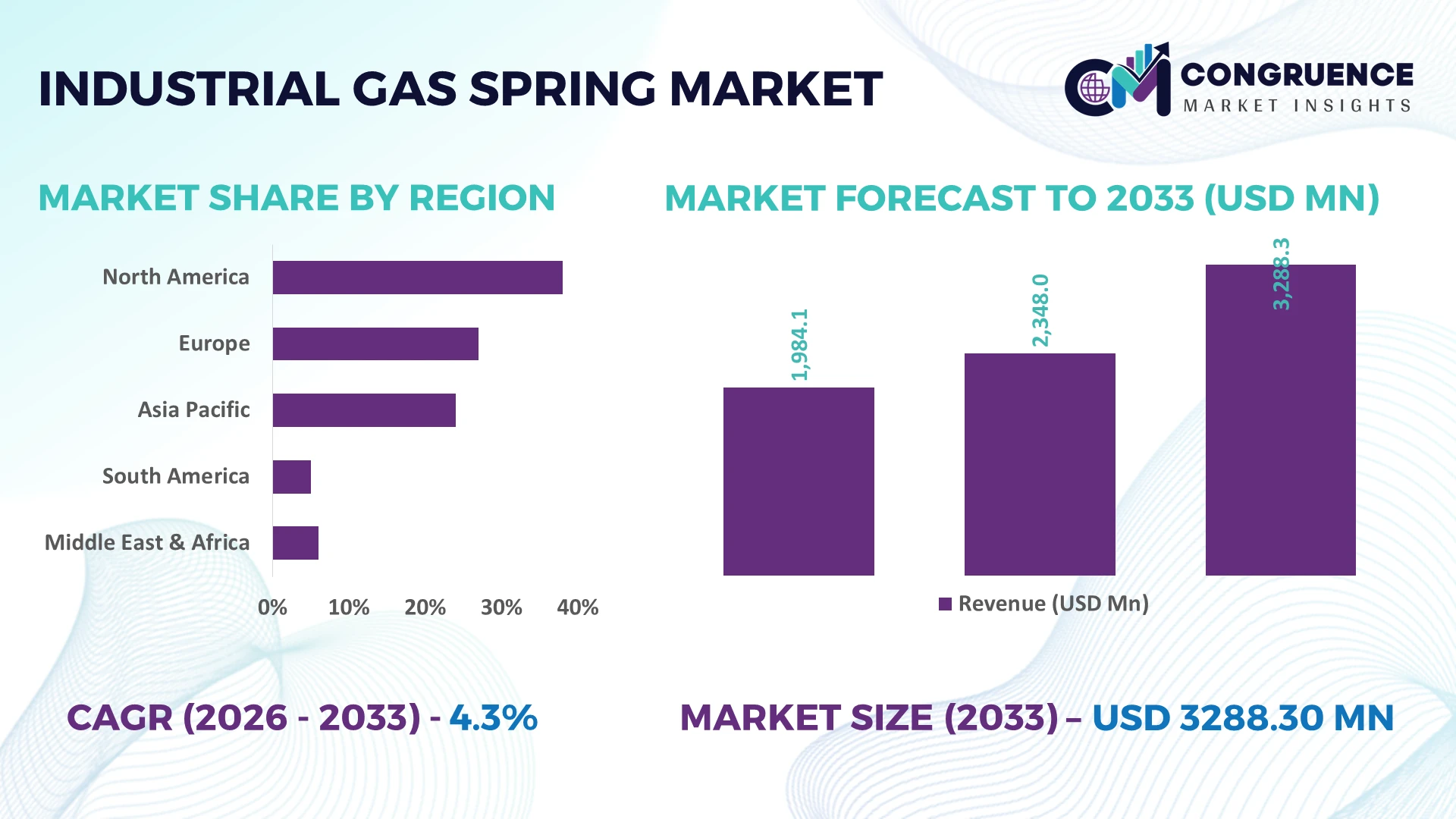

The Global Industrial Gas Spring Market was valued at USD 2348 Million in 2025 and is anticipated to reach a value of USD 3288.3 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Growth is supported by higher deployment of automated manufacturing equipment, ergonomic industrial workstations, electric vehicle production lines, and precision motion-control systems requiring durable gas spring assemblies with longer service life.

Germany remains the dominant country, accounting for approximately 23% of European industrial gas spring production, supported by over €20 billion in annual industrial automation investments and strong automotive and machinery manufacturing. China exceeds Germany in manufacturing volume with more than 31% of global industrial output, driven by large-scale factory automation and equipment exports. Continued supply-chain diversification following Red Sea shipping disruptions in 2026 has accelerated regional sourcing strategies for precision components.

Manufacturers prioritizing localized production, high-cycle performance, and automation-focused product portfolios are positioned to strengthen competitive advantage across industrial equipment markets.

Market Size & Growth: USD 2348 million (2025) to USD 3288.3 million (2033) at 4.3% CAGR, driven by automation upgrades across industrial machinery and material-handling equipment.

Top Growth Drivers: Factory automation (+19%), industrial robotics deployment (+17%), and electric vehicle manufacturing expansion (+14%) continue accelerating component demand.

Short-Term Forecast: By 2028, advanced gas spring integration improves equipment maintenance efficiency by nearly 18% while reducing downtime by approximately 12%.

Emerging Technologies: AI-enabled predictive maintenance, lightweight composite cylinders, and smart manufacturing platforms increase production efficiency by over 20%.

Regional Leaders: Asia-Pacific exceeds USD 1.4 billion, Europe approaches USD 900 million, and North America surpasses USD 620 million, supported by automation and regional manufacturing expansion.

Consumer/End-User Trends: More than 58% of new industrial equipment platforms integrate maintenance-free gas spring systems for improved operator safety and productivity.

Pilot/Case Example: In 2026, an automated assembly modernization project improved workstation cycle efficiency by 16% through optimized gas spring-assisted motion control.

Competitive Landscape: Leading manufacturers collectively hold nearly 36% market share, with Stabilus, SUSPA, ACE Controls, Bansbach Easylift, and Camloc maintaining strong industrial portfolios.

Regulatory & ESG Impact: Lightweight component adoption reduces equipment weight by up to 11%, supporting industrial sustainability targets and stricter manufacturing efficiency standards.

Investment & Funding: More than USD 650 million supports manufacturing expansion, regional production capacity, and strategic partnerships amid global supply-chain realignment.

Innovation & Future Outlook: Digitally engineered gas springs, corrosion-resistant materials, and modular customization strengthen next-generation industrial equipment competitiveness.

Industrial gas springs are experiencing stronger demand across automated production lines, medical equipment, logistics systems, and heavy machinery where precise controlled motion enhances operational reliability. Recent product innovations emphasize corrosion-resistant coatings, lightweight materials, and maintenance-free designs, while approximately 22% of new industrial equipment platforms incorporate customized motion-control solutions. Ongoing regional manufacturing localization and resilient component sourcing strategies are reshaping long-term procurement priorities, setting the stage for broader strategic market evaluation.

Industrial gas springs have become strategically important as manufacturers prioritize automation, workplace safety, and lifecycle cost optimization across production facilities. Infrastructure modernization, reshoring initiatives, and supply-chain restructuring following continued logistics disruptions in 2026 are encouraging equipment manufacturers to secure localized component sourcing. This shift strengthens supplier relationships while reducing procurement uncertainty for industrial machinery, medical equipment, transportation systems, and advanced manufacturing applications.

Compared with conventional mechanical spring assemblies, advanced nitrogen-filled gas spring systems deliver up to 22% longer operational life while reducing maintenance interventions by nearly 18% through consistent force output and compact designs. Germany leads in engineering innovation and high-precision industrial applications, whereas China dominates manufacturing scale and OEM deployment across factory automation. Over the next two to three years, smart production facilities are expected to increase gas spring integration by approximately 16% as digitally connected equipment becomes standard across industrial operations.

A practical example is automated assembly workstations using lockable gas springs to improve ergonomic positioning, reducing operator adjustment time by nearly 20% while supporting higher production consistency. Manufacturers are responding through localized production expansion, engineering partnerships, and customized product portfolios tailored for automation equipment and heavy-duty applications. Companies that combine precision engineering, resilient supply networks, and application-specific innovation will strengthen competitive positioning and secure long-term industrial contracts.

The rapid expansion of automated manufacturing is reshaping demand for industrial gas springs across machine tools, robotics, packaging equipment, and material-handling systems. Factory automation investments have increased by approximately 19%, while industrial robot installations have grown by nearly 16%, driving demand for durable motion-control components with longer service intervals. Germany continues expanding smart manufacturing capabilities, while India's industrial modernization programs are increasing deployment of automated production lines. In response, manufacturers are expanding localized production, introducing corrosion-resistant designs, and forming engineering partnerships with OEMs. A key strategic advantage is that customized gas spring integration shortens equipment commissioning time while improving maintenance planning and production reliability.

Price fluctuations in high-grade steel and specialty alloys continue challenging industrial gas spring manufacturers, with raw material costs varying by nearly 14% during procurement cycles. Imported precision sealing components remain subject to logistics disruptions, while extended lead times of around 18% have affected production planning in several manufacturing hubs. These conditions compress operating margins and complicate inventory optimization for equipment suppliers. Companies are responding by localizing component sourcing, securing multi-year procurement agreements, and redesigning products to reduce dependence on imported materials. Strategic supplier diversification has become essential for maintaining production continuity and protecting delivery commitments.

The growing adoption of intelligent industrial equipment is creating new opportunities for advanced gas spring technologies featuring integrated damping, locking mechanisms, and predictive maintenance compatibility. Around 24% of newly commissioned automated production systems now specify customized motion-control solutions, while lightweight material adoption has improved equipment efficiency by nearly 12%. Japan and South Korea continue investing in precision manufacturing technologies that require highly engineered positioning components. Manufacturers are increasing R&D spending, collaborating with automation integrators, and expanding modular product platforms to address specialized industrial applications. The strongest opportunity lies in supplying engineered solutions instead of standardized replacement components, creating higher customer retention and value-added differentiation.

Expanding customized gas spring production while maintaining consistent quality remains a significant operational challenge. More than 28% of industrial equipment projects require application-specific force calibration, while product qualification timelines can extend by approximately 20% because of OEM validation requirements. Workforce shortages in precision engineering and advanced manufacturing further constrain production scalability in several industrial countries. Companies are investing in automated testing systems, digital engineering tools, and standardized modular manufacturing processes to improve consistency without sacrificing customization. Organizations capable of balancing engineering flexibility with scalable production will achieve stronger operational resilience and sustain long-term competitiveness in demanding industrial sectors.

Smart Manufacturing Integration Industrial equipment manufacturers are integrating gas springs into digitally connected production cells, with smart factory deployments increasing by nearly 18% and predictive maintenance adoption rising 21%. Germany's manufacturing modernization and workforce shortages are accelerating automation investments. Companies are standardizing modular gas spring platforms and integrating digital engineering tools, reducing equipment downtime while improving production consistency and maintenance planning.

Localized Component Sourcing Continued supply-chain adjustments following logistics disruptions in 2026 have increased localized component procurement by approximately 24%, while average lead times have declined by 15% for manufacturers using regional supplier networks. Industrial OEMs are restructuring sourcing strategies, expanding domestic assembly operations, and strengthening supplier partnerships to improve delivery reliability and reduce procurement risk for precision motion-control systems.

Lightweight Material Transition High-strength alloys and stainless-steel gas spring designs now account for nearly 27% of new industrial product launches, while equipment weight reduction averages 11% without compromising load performance. Tighter industrial efficiency standards and lower maintenance requirements are encouraging manufacturers to redesign product portfolios, expand corrosion-resistant solutions, and optimize engineering specifications for demanding industrial environments.

Application-Specific Product Engineering Customized gas spring configurations have increased by approximately 20% as industrial buyers prioritize equipment-specific performance over standardized components. Locking mechanisms, adjustable force calibration, and integrated damping technologies are shortening installation time by nearly 17%. Companies are expanding engineering partnerships and application-focused product development, creating stronger customer retention through tailored industrial motion-control solutions.

Compression Gas Springs remain the leading segment because of their broad integration across industrial machinery, automation systems, material-handling equipment, and heavy-duty manufacturing applications. They account for approximately 46% of installed industrial gas spring systems, supported by reliable load-bearing capability, compact design, and lower maintenance requirements. Manufacturers continue expanding compression gas spring portfolios with corrosion-resistant finishes and extended-cycle performance. Dampers remain strategically important for vibration control and controlled movement, while Tension Gas Springs maintain stable demand in specialized lifting and counterbalance applications where space constraints influence equipment design.

Lockable Gas Springs represent the fastest-growing segment as industrial automation and ergonomic workstation upgrades require adjustable positioning and enhanced operator safety. Adoption has increased by nearly 19% across automated production equipment, while Stainless Steel Gas Springs have recorded approximately 15% higher deployment in food processing, pharmaceutical manufacturing, and harsh operating environments due to corrosion resistance. Companies are increasing investments in modular product platforms, customized engineering, and OEM partnerships to capture higher-value industrial applications while differentiating through application-specific performance.

Industrial Machinery represents the largest application segment, accounting for nearly 44% of total demand because automated production lines, packaging systems, machine tools, and material-handling equipment require durable motion-control components for continuous operation. Equipment modernization programs and factory automation have increased gas spring integration by approximately 18%, encouraging suppliers to expand customized product offerings for industrial OEMs. Furniture maintains stable demand through ergonomic office systems, while Automotive continues integrating gas springs into commercial vehicle access systems and production equipment.

Medical Equipment is the fastest-growing application as hospitals and equipment manufacturers prioritize ergonomic positioning, precision movement, and maintenance-free mechanisms. Deployment in advanced medical devices has increased by around 17%, while Aerospace applications continue expanding through lightweight component adoption and strict performance requirements. Manufacturers are strengthening engineering collaboration, increasing application-specific product development, and expanding production capacity to support specialized customer requirements where reliability and operational precision remain critical purchasing factors.

Manufacturing is the dominant end-user segment, representing approximately 49% of industrial gas spring demand due to continuous investment in automated production lines, machine tools, logistics equipment, and industrial workstations. Factory modernization programs have increased component integration by nearly 18%, while maintenance optimization initiatives have reduced equipment servicing frequency by around 14%. Suppliers are responding through localized manufacturing, customized engineering support, and long-term OEM supply agreements to strengthen customer retention within high-volume industrial operations.

Healthcare is emerging as the fastest-growing end-user as advanced diagnostic equipment, patient handling systems, and laboratory devices require precise, maintenance-free motion control. Adoption has increased by approximately 16% as equipment manufacturers prioritize ergonomic operation and higher reliability. Automotive continues expanding through assembly-line modernization, while Aerospace & Defense emphasizes lightweight engineered components and Furniture maintains consistent replacement demand. Companies are targeting these industries through application-specific product customization, strategic partnerships, and differentiated service models to strengthen competitive positioning across specialized industrial markets.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 5.6% CAGR between 2026 and 2033.

Strategic OEM Automation and Industrial Modernization

North America maintains a leading position through extensive deployment of industrial automation, advanced manufacturing systems, and high-value machinery production. The region contributes nearly 35% of global demand, supported by strong investments in warehouse automation, aerospace manufacturing, and medical equipment production. More than 60% of newly commissioned automated industrial facilities integrate advanced motion-control components to improve operational reliability. Manufacturing reshoring initiatives and localized component sourcing continue strengthening domestic supply networks, while industrial equipment suppliers are expanding engineering capabilities and application-specific product portfolios to meet evolving OEM requirements and reduce production lead times.

United States Market Outlook: The United States remains the region's largest market because of its extensive industrial machinery, aerospace, healthcare equipment, and logistics automation sectors. More than 65% of industrial automation investments within North America originate from the country, supporting wider deployment of engineered gas spring systems. Manufacturers continue investing in digital production facilities, customized component engineering, and domestic supply-chain expansion to improve operational resilience and strengthen long-term OEM partnerships.

Precision Engineering Drives Industrial Competitiveness

Europe remains a technology-intensive market supported by advanced mechanical engineering, industrial machinery production, and stringent manufacturing quality standards. The region accounts for approximately 29% of global deployment, with precision manufacturing and factory modernization accelerating equipment upgrades. Industrial automation projects have increased by nearly 17%, encouraging manufacturers to expand production of corrosion-resistant and high-cycle gas spring solutions. Sustainability targets are also influencing product engineering through lightweight materials and extended service-life designs, enabling industrial operators to improve equipment efficiency while reducing maintenance requirements.

Germany Market Outlook: Germany leads the European market through its globally competitive automotive, machinery, and industrial automation sectors. Nearly one-quarter of Europe's precision manufacturing capacity is concentrated within the country, supporting continuous demand for engineered motion-control components. German manufacturers continue expanding smart factory capabilities, investing in advanced production technologies, and collaborating closely with OEMs to deliver highly customized industrial gas spring solutions for automation-intensive industries.

Manufacturing Scale Accelerates Industrial Deployment

Asia-Pacific has become the fastest-expanding regional market because of large-scale industrial production, infrastructure investment, and accelerating factory automation. The region contributes approximately 31% of global industrial gas spring deployment while accounting for the highest manufacturing equipment output. Industrial robot installations have increased by nearly 18%, encouraging broader adoption of precision motion-control systems across electronics, automotive, and heavy machinery manufacturing. Companies are strengthening regional production capacity, expanding supplier networks, and establishing engineering centers to support localized manufacturing requirements and improve delivery performance.

China Market Outlook: China dominates regional demand through its extensive manufacturing ecosystem, industrial automation programs, and equipment export capabilities. The country accounts for more than 32% of global manufacturing output, creating sustained demand for industrial gas springs across machinery, logistics equipment, and automotive production. Domestic manufacturers continue investing in automated production facilities, precision component manufacturing, and localized innovation to improve product quality and reduce dependence on imported industrial components.

Industrial Modernization Supports Equipment Demand

South America continues strengthening its industrial base through manufacturing upgrades, mining investments, and logistics infrastructure improvements. The region represents approximately 5% of global market activity, with industrial equipment modernization driving steady adoption of engineered gas spring systems. Manufacturing facilities have increased automation investments by nearly 12%, supporting higher demand for ergonomic and maintenance-efficient components. While infrastructure limitations and imported component dependency remain operational challenges, companies are expanding local distribution partnerships and strengthening regional service capabilities to improve equipment availability and customer support.

Brazil Market Outlook: Brazil represents the largest market within South America due to its diversified manufacturing, agricultural equipment, and automotive industries. More than 45% of regional industrial machinery production is concentrated in the country, supporting consistent demand for precision motion-control products. Equipment manufacturers continue expanding domestic assembly operations and technical support capabilities while improving localized sourcing strategies to enhance supply reliability and shorten delivery timelines.

Infrastructure Investment Expands Industrial Applications

The Middle East & Africa market is advancing through industrial diversification, infrastructure modernization, and expanding manufacturing investments. The region contributes approximately 4% of global demand, with industrial projects increasing deployment of automated machinery and material-handling equipment. Industrial facility modernization initiatives have improved adoption of engineered motion-control components by nearly 13%, particularly across logistics, energy, and manufacturing sectors. Companies are strengthening regional distribution networks, establishing technical service partnerships, and increasing localized inventory to support expanding industrial operations and improve customer responsiveness.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through industrial diversification initiatives, manufacturing expansion, and large-scale infrastructure projects. Industrial investment programs continue increasing deployment of automated production equipment across manufacturing and logistics sectors, with machinery localization becoming a strategic priority. Companies are establishing regional partnerships, expanding engineering support, and strengthening supply-chain capabilities to serve growing industrial facilities while supporting long-term equipment modernization objectives.

The Industrial Gas Spring Market is shaped by competition between global engineering leaders including Stabilus, SUSPA, Bansbach Easylift, ACE Controls, and Camloc against regional precision manufacturers focused on cost-efficient production and rapid customization. The top five companies collectively control approximately 38% of the global market, while regional suppliers compete aggressively in OEM replacement and specialized industrial applications. Competition is driven by engineering precision, delivery reliability, customization capability, and localized supply chains rather than price alone. Customized product programs improve customer retention by nearly 24%, while localized manufacturing reduces delivery time by approximately 18% and digital engineering shortens product development cycles by around 15%. Companies are expanding production capacity, forming OEM development partnerships, investing in automated manufacturing, and vertically integrating component production to secure supply continuity. The competitive landscape is shifting toward application-specific engineered solutions instead of standardized products. High certification requirements, precision manufacturing expertise, and long-term OEM qualification remain major entry barriers. Success depends on engineering differentiation, resilient supply networks, rapid customization, and consistent product quality.

Stabilus

SUSPA GmbH

Bansbach Easylift GmbH

ACE Controls Inc.

Camloc Motion Control Ltd.

Hahn Gasfedern GmbH

Industrial Gas Springs Ltd.

Dictator Technik GmbH

Lesjöfors AB

Barnes Group Inc.

Vapsint S.r.l.

Metrol Springs Ltd.

Advanced engineering technologies are transforming industrial gas spring performance through lightweight alloys, precision sealing systems, and digitally optimized product design. Modern gas springs manufactured with high-strength materials deliver approximately 22% longer operating life and reduce maintenance requirements by nearly 18% compared with conventional steel-based designs. Around 47% of newly developed industrial equipment platforms now integrate customized gas spring assemblies during the design phase instead of retrofitting them later, improving production efficiency and lifecycle reliability for OEM manufacturers.

Emerging technologies include AI-assisted engineering simulation, automated force calibration, smart manufacturing, and corrosion-resistant surface treatments. Digital simulation shortens prototype development by approximately 20%, while automated production improves dimensional consistency by nearly 15%. Large industrial OEMs benefit most from these technologies because integrated design validation reduces engineering revisions and accelerates product qualification. Advanced lockable gas springs and intelligent damping technologies are also expanding adoption across medical equipment, automated workstations, and precision manufacturing systems requiring higher operational accuracy.

Between 2026 and 2028, digital engineering, modular manufacturing, and automated quality inspection will redefine competitive performance. Manufacturers investing in predictive production analytics, robotic assembly, and standardized modular platforms will achieve faster product customization, stronger OEM collaboration, and greater supply-chain resilience. Early technology adoption strengthens operational flexibility, reduces production variability, and creates sustainable competitive differentiation in increasingly specialized industrial applications.

July 2025 – Stabilus launched the Industrial POWERISE IPR35 Smart electromechanical actuator with an integrated control unit, eliminating the need for an external controller. The solution simplifies installation and supports advanced industrial automation applications, improving system integration and engineering efficiency. Source: https://www.stabilus.com/

June 2025 – Stabilus introduced the Stabilus4Automation platform, combining five industrial technology brands into a unified automation portfolio. The platform integrates 5 specialist brands, strengthening cross-product compatibility and enabling broader motion-control solutions for industrial OEM customers. Source: https://group.stabilus.com/

March 2026 – Stabilus expanded its Customized to Order (CTO) program for Industrial POWERISE actuators, enabling configuration from batch size 1. The initiative enhances customization flexibility for OEMs while reducing engineering complexity and accelerating deployment across industrial equipment projects. Source: https://ir.stabilus.com/

May 2026 – Stabilus signed an agreement to divest its Fabreeka and Tech Products businesses to VMC Group for an enterprise value of USD 92 million. The transaction sharpens the company's focus on industrial motion-control technologies and strengthens strategic capital allocation. Source: https://www.stabilus.com/

The Industrial Gas Spring Market report delivers a comprehensive assessment of market structure, competitive dynamics, technology evolution, and industrial demand across Compression Gas Springs, Tension Gas Springs, Lockable Gas Springs, Dampers, and Stainless Steel Gas Springs. It evaluates applications including Industrial Machinery, Automotive, Medical Equipment, Furniture, and Aerospace, together with demand trends across Manufacturing, Automotive, Healthcare, Aerospace & Defense, and Furniture end-users. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while analyzing deployment trends, product adoption, and operational developments influencing industrial motion-control systems.

The report also provides strategic insights into automation technologies, customized engineering solutions, supply-chain localization, competitive positioning, and emerging industrial applications between 2026 and 2033. It examines deployment patterns, regional manufacturing capabilities, innovation priorities, and investment strategies to support expansion planning, product portfolio development, partnership evaluation, and long-term business decision-making for manufacturers, suppliers, investors, and industrial equipment OEMs.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2348 Million |

Market Revenue in 2033 | USD 3288.3 Million |

CAGR (2026 - 2033) | 4.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Stabilus, SUSPA GmbH, Bansbach Easylift GmbH, ACE Controls Inc., Camloc Motion Control Ltd., Hahn Gasfedern GmbH, Industrial Gas Springs Ltd., Dictator Technik GmbH, Lesjöfors AB, Barnes Group Inc., Vapsint S.r.l., Metrol Springs Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |