Reports

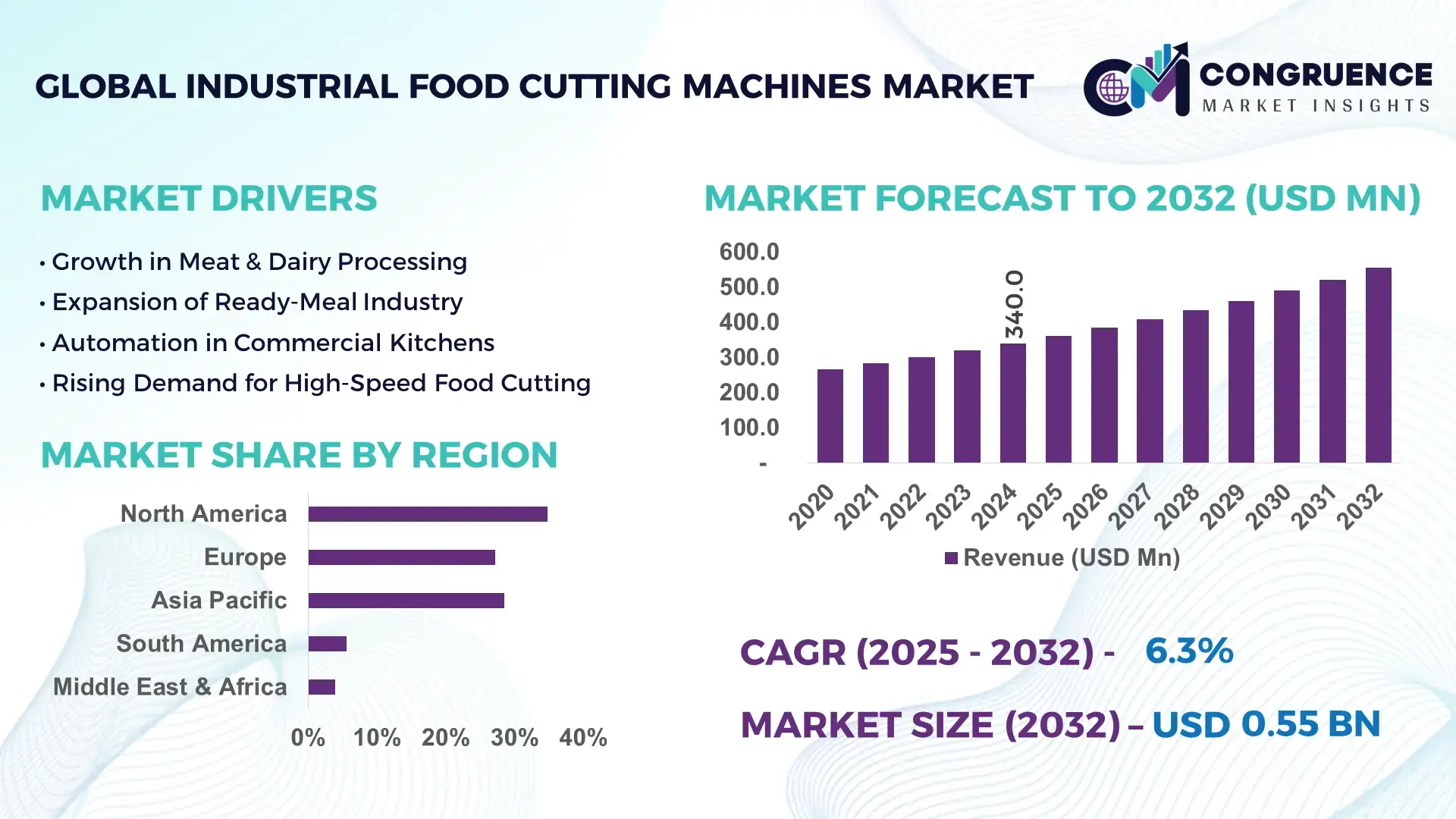

The Global Industrial Food Cutting Machines Market was valued at USD 340.0 Million in 2024 and is anticipated to reach USD 554.3 Million by 2032, expanding at a CAGR of 6.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is driven by rising demand for precision-based, automated processing systems across industrial food production lines.

The United States maintains the strongest position in the market, supported by advanced food-processing infrastructure, an installed base of over 8,500 automated cutting lines, and annual investments exceeding USD 1.2 billion in processing automation. The country leads in high-capacity dicing and slicing technologies used in meat, bakery, and packaged foods, with over 62% of major facilities integrating vision-guided or sensor-driven cutting systems to enhance throughput consistency and safety compliance.

Market Size & Growth: Valued at USD 340.0 Million in 2024, projected to reach USD 554.3 Million by 2032, growing at 6.3% CAGR due to increased adoption of automated food-processing equipment.

Top Growth Drivers: Automation adoption up 48%; processing efficiency improved by 32%; hygiene-compliance installations up 41%.

Short-Term Forecast: By 2028, automated cutting systems expected to improve line-level labor efficiency by 27%.

Emerging Technologies: AI-based blade optimization, vision-guided portioning, and IoT-enabled machine diagnostics.

Regional Leaders: North America projected to reach USD 172 Million by 2032 with high automation uptake; Europe to reach USD 141 Million driven by sustainability compliance; Asia Pacific to reach USD 163 Million with rapid processing-capacity expansion.

Consumer/End-User Trends: Ready-to-eat segment adopting precision cutting machines at 38% growth due to demand for uniform product quality.

Pilot or Case Example: In 2026, a poultry-processing pilot improved cut-accuracy by 29% using AI-calibrated slicing systems.

Competitive Landscape: Market leader holds approx. 11% share, followed by major players specializing in intelligent cutting systems and high-capacity industrial lines.

Regulatory & ESG Impact: Food-safety directives accelerating advanced sanitation-compliant machine deployment; firms adopting 25% equipment-level sustainability improvements by 2030.

Investment & Funding Patterns: Over USD 420 Million invested recently in processing automation, driven by plant upgrades and digital transformation initiatives.

Innovation & Future Outlook: Advancements in robotics, smart blades, and predictive maintenance shaping next-generation industrial cutting ecosystems.

The market is influenced by demand from meat, bakery, and processed-food sectors, driven by innovations in automated dicing, slicing, and portioning technologies. Regulatory emphasis on hygiene and worker safety continues to support machine upgrades, while Asia Pacific and North America show strong consumption trends and capacity expansion. Emerging automation platforms and precision-cutting solutions position the sector for sustained growth across key applications.

The Industrial Food Cutting Machines Market plays a strategic role in strengthening global food-processing productivity, ensuring consistent output quality, and enabling scalable manufacturing performance across diverse product categories. The integration of automation, AI-driven calibration, and advanced materials is accelerating measurable efficiency improvements. For instance, AI-enabled blade optimization delivers up to 34% better cutting uniformity compared to conventional mechanical systems, reducing reprocessing loads and enhancing throughput reliability. Across geographies, Asia Pacific dominates in volume, while North America leads in adoption with nearly 58% of enterprises utilizing semi- or fully automated cutting lines.

Short-term projections indicate that by 2027, machine-learning-based predictive diagnostics will reduce unplanned equipment downtime by 22%, strengthening production continuity. Regulatory frameworks targeting food-safety modernization, worker-safety compliance, and sanitization efficiency are reinforcing the transition toward high-precision systems. ESG objectives are also shaping investments, with firms committing to 20–25% reductions in energy consumption and water usage by 2030 through upgraded cutting and processing lines.

A notable micro-scenario occurred in 2026, when a major European facility achieved a 31% reduction in trimming losses through the deployment of smart-sensing cutting modules. These improvements highlight the industry’s move toward integrated digital manufacturing ecosystems that combine increased accuracy, waste reduction, and sustainability alignment.

Overall, the Industrial Food Cutting Machines Market is evolving into a critical pillar of resilience, compliance, and sustainable growth, supporting the next generation of efficient, automated food-processing systems worldwide.

The Industrial Food Cutting Machines Market is experiencing strong transformation driven by automation, digital optimization, and evolving operational requirements across industrial food-processing environments. Increasing production volumes, rising demand for packaged and ready-to-eat foods, and the need for consistent, high-precision cutting outcomes are shaping market direction. Manufacturers are expanding machine functionality to support diverse food categories such as meat, dairy, bakery, and confectionery, while integrating smart controls for enhanced reliability. The move toward labor reduction and improved hygiene standards is accelerating the adoption of equipment featuring advanced materials, automated wash-down capabilities, and predictive maintenance systems. Regional production expansions, regulatory modernization, and technological evolution collectively shape the market’s dynamic landscape.

Automation is significantly influencing demand for advanced food-cutting machines as processing plants seek higher throughput, consistency, and compliance. Modern industrial cutting machines equipped with servo-driven blades, programmable logic controllers, and real-time calibration capabilities help manufacturers deliver precise cuts at high speeds, reducing manual labor by up to 40% in large facilities. The rapid shift toward automation in meat, poultry, bakery, and processed-food segments has increased equipment installations, especially where production volumes exceed 50,000 tons annually. Automated cutting systems enable uniform slicing and dicing with accuracy deviations below ±2 mm, supporting strict quality and safety standards. As global food manufacturers expand capacity to meet rising consumption, automated cutting lines are becoming a critical operational investment.

Despite strong adoption potential, the market faces constraints due to complex integration requirements for advanced automated cutting systems. Many mid-sized manufacturers experience operational challenges integrating vision systems, calibration software, and sanitation-compliant components into legacy processing lines. Maintenance of high-precision blades, high-speed motors, and wash-down assemblies requires skilled technicians and consistent upkeep intervals, often every 350–500 operational hours. Additionally, stringent hygiene-compliance standards necessitate specialized cleaning protocols, increasing operational effort. These complexities can limit rapid modernization in cost-sensitive markets, slowing the transition from manual to automated cutting equipment.

Technological innovation is creating strong opportunities for the market, especially through advancements such as AI-guided cutting, robotic portioning, and blade-life optimization systems. Newer systems deliver precision improvements of up to 35%, reducing waste and ensuring consistent product weight and shape. Machine manufacturers are integrating IoT sensors for real-time predictive maintenance, capable of identifying performance deviations with more than 90% accuracy. Growth in ready-meal and packaged food consumption is encouraging investment in high-capacity cutting machinery capable of processing 8–12 tons per hour, supporting scalability for growing production facilities. These innovations present strong potential for market expansion.

Industrial food-cutting systems involve considerable operational and lifecycle costs, including energy usage, blade replacement, sanitation procedures, and technician-level maintenance. High-capacity machines often require electricity consumption above 20–30 kWh per hour, increasing utility expenditure in regions with rising energy prices. Additionally, evolving food-safety regulations require advanced contamination-control features, stainless-steel construction, and wash-down-resistant components, raising equipment and operational costs. Compliance with international standards—particularly for meat and poultry plants—demands frequent audits and equipment upgrades, creating adoption challenges for small and mid-scale facilities.

Surge in AI-Integrated Cutting Systems: AI-enabled cutting solutions are increasingly used to achieve precision levels exceeding 96%, reducing product waste by 18–22%. Facilities using sensor-driven calibration systems report improved cycle times by 15%, enabling greater processing throughput across meat and bakery segments.

Expansion of High-Speed Automation Lines: Demand for high-capacity cutting lines capable of processing 10–14 tons per hour has risen sharply. Automated lines have shown a 30% reduction in manual labor, with North American plants leading adoption due to labor-efficiency priorities and hygiene compliance.

Growth of Hygienic Design & Sanitation Innovation: Equipment with wash-down capability and corrosion-resistant construction has increased by 42%, driven by food-safety regulations. Plants employing hygienic-design cutting systems report a 25% decrease in contamination-related downtime.

Increased Adoption in Ready-to-Eat and Packaged Foods: The rise of ready-meal consumption has accelerated adoption of multi-functional cutting machines, with usage growing 38% in large processing units. Machines offering flexible blade adjustments and portion-weight accuracy within ±1.5% support expanding product lines across global markets.

The Industrial Food Cutting Machines Market is segmented by type, application, and end-user, each contributing uniquely to the industry’s operational and technological landscape. Product types vary from high-speed slicers to dicing and shredding systems, meeting efficiency, hygiene, and precision requirements across processing facilities. Application segmentation reflects usage in meat processing, bakery production, dairy operations, and ready-meal manufacturing—each with distinct throughput and accuracy demands. End-user insights indicate strong adoption among large-scale food processors, driven by rising automation rates and stringent hygiene standards, while mid-sized manufacturers are rapidly adopting digitalized systems for quality and labor optimization. The segmentation structure highlights evolving needs in high-capacity processing, portion standardization, and waste reduction, supported by measurable performance gains across industries and regions.

Industrial food cutting machines include high-speed slicers, dicers, cutters, shredders, bowl choppers, and portioning systems, each tailored to specific processing requirements. High-speed slicers currently account for approximately 44% of total adoption, driven by their ability to handle large volumes and maintain accuracy within ±1.5 mm across diverse food textures. In comparison, industrial dicers hold around 27%, and shredding systems contribute nearly 18%, while bowl choppers and specialty cutters together represent the remaining 11% of the market. Portioning systems are the fastest-growing type, supported by demand for weight-consistent, packaged foods and automated portion control. These systems are expanding at the fastest rate, with growth positioned above 7.2%, backed by rising labor-efficiency and quality-standard requirements in meat and ready-meal production. Other machine types maintain niche relevance, particularly in applications requiring fine texture modification or high-volume slicing for bakery and cheese processing. Combined, these segments contribute approximately 29% of total adoption.

Industrial food cutting machines are widely used across meat processing, bakery production, dairy operations, frozen foods, and ready-meal manufacturing. Meat processing is the leading application segment, accounting for nearly 46% of overall adoption, driven by high-volume throughput needs, strict hygiene controls, and the demand for precise cutting consistency. In comparison, bakery applications hold 23%, dairy operations represent 17%, while frozen and ready-meal applications collectively contribute 14%. The fastest-growing application is ready-meal manufacturing, supported by rapid urbanization, rising consumption of convenience foods, and the need for portioning accuracy. Growth in this segment is estimated above 7.5%, outperforming meat, bakery, and dairy equipment due to increased SKU diversification and automated packaging integration. Additional applications maintain steady adoption supported by packaging standardization and hygiene compliance trends across global facilities. Consumer insights show that in 2024, over 39% of enterprises implemented automated cutting systems to enhance consistency in ready-to-eat (RTE) products, while nearly 28% of consumers in APAC reported increased preference for uniformly cut, packaged ingredients.

End-users in the Industrial Food Cutting Machines Market include large-scale food processors, mid-sized manufacturers, commercial kitchens, and institutional food service units. Large-scale food processing companies represent the leading end-user group with approximately 49% share, supported by continuous capacity expansion, plant automation, and stringent output-standardization needs. In comparison, mid-sized manufacturers account for 31%, commercial kitchens hold 12%, and institutional food service contributes the remaining 8%.

The fastest-growing end-user segment is mid-sized processors, expanding at over 7.1%, driven by increasing adoption of automated cutting lines, tighter labor availability, and improved access to modular machinery that supports flexible operations. Other end-users, including commercial kitchens and institutional food facilities, are increasing adoption at a combined rate of nearly 20%, particularly in regions with maturing hospitality sectors and central kitchens. In 2024, more than 36% of global food manufacturers reported adopting automated cutting technologies to enhance throughput and hygiene outcomes, while over 52% of food-service operators in North America indicated higher reliance on machine-cut ingredients for consistency and safety.

North America accounted for the largest market share at 34.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

The global Industrial Food Cutting Machines market continues to exhibit strong regional variations driven by food processing capacity, automation maturity, cold-chain expansion, and packaged food consumption patterns. North America's dominance stems from high penetration of industrial slicers, dicers, and portion cutters across bakery, meat processing, and ready-meal production units. Europe captured 27.2% of the market in 2024, supported by stringent hygiene compliance and Industry 4.0 integration. Asia-Pacific held 28.5%, driven by rapid industrialization, rising food exports, and accelerated investments in automated processing lines. South America and the Middle East & Africa collectively accounted for 9.5%, with increasing adoption of automated cutting technologies in poultry, seafood, and fruit processing facilities. As automation costs decline and precision cutting becomes essential for high-volume production, these regions are expected to register substantial increases in machine installations by 2032.

North America held 34.8% of the global Industrial Food Cutting Machines market in 2024, driven by strong demand from the meat, poultry, frozen foods, dairy, and bakery segments. The U.S. remains the regional powerhouse, supported by large-scale food manufacturers integrating automated slicing, precision dicing, ultrasonic cutting, and vision-guided portioning systems. Regulatory frameworks such as FSMA and USDA sanitation requirements have accelerated adoption of stainless-steel hygienic designs and automated blade-safety systems. Technology integration—including robotic pick-and-place, AI-based defect detection, and digital maintenance platforms—is reshaping production workflows. Local players such as Urschel Laboratories continue to innovate with high-capacity cutting equipment tailored for large food processors across frozen vegetables and meat applications. Consumer behavior shows a shift toward convenience and portion-controlled foods, resulting in higher enterprise adoption across retail food manufacturing. The region also benefits from increasing investments in clean-label and fresh-cut technologies, supporting machine upgrades in both large and mid-size processing plants.

Europe accounted for 27.2% of the Industrial Food Cutting Machines market in 2024, with Germany, the UK, France, the Netherlands, and Italy standing out as key adopters. The region’s strict hygiene and sustainability regulations—including EFSA food safety standards—continue to push manufacturers toward energy-efficient, low-waste cutting technologies. Precision cutting machines, ultrasonic slicers, and automated trimming systems are increasingly used in European dairy, bakery, confectionery, and seafood processing units. Industry 4.0 integration has accelerated, with widespread deployment of smart sensors, predictive maintenance software, and robotics in food processing lines. Local players such as Marel (Europe operations) contribute significantly with advanced cutting platforms designed for meat and poultry optimization. Consumer behavior in Europe reflects strong preference for freshness, traceability, and sustainable packaging, leading processors to invest in equipment that reduces waste and ensures portion uniformity. The region’s push toward digital transformation and sustainability is a major driver of stable long-term demand.

Asia-Pacific represented 28.5% of global market volume in 2024 and ranked as the fastest-growing region due to expanding food manufacturing clusters. China, India, Japan, South Korea, and Thailand are among the top consuming countries, with rapid growth in meat processing, snacks, ready-made meals, and bakery production lines. Infrastructure expansion—including new cold-chain facilities and modernized processing plants—continues to boost demand for industrial slicers, dicers, shredders, and automated portion cutters. The region is emerging as an innovation hub with increasing adoption of robotics-driven cutting, IoT machine monitoring, and AI-enabled product inspection. Local manufacturers such as Gongda Machine Company are expanding regional equipment distribution, offering mid-cost automated cutting systems aligned with local processing requirements. Consumer behavior in Asia-Pacific is heavily influenced by e-commerce, rising packaged food consumption, and increasing preference for fresh-cut fruits and vegetables, driving high-volume cutting machine demand across both large factories and mid-scale enterprises.

South America registered 5.6% of the global market share in 2024, with Brazil and Argentina leading demand for industrial food cutting equipment. The region’s growing meat, poultry, fruit, and dairy processing sectors continue to adopt automated cutting technologies to improve yields and reduce operational losses. Investments in food infrastructure—particularly in cold storage, export-oriented meat processing plants, and modernized packaging lines—support increased machine installations. Government incentives in Brazil for food industry modernization have driven upgrades to automated slicers and precision dicers. Local players such as Jamar Industria support the ecosystem through region-specific equipment solutions. Consumer behavior reflects rising interest in processed and portioned foods, especially in urban centers, leading to broader industrial adoption. Trade policies promoting food exports to North America and Europe also encourage facilities to adopt globally compliant cutting technologies.

The Middle East & Africa held 3.9% of the global market in 2024, driven by rising demand from poultry, bakery, confectionery, and packaged food industries. Countries such as the UAE, Saudi Arabia, and South Africa lead adoption as they continue investing in large-scale food manufacturing hubs and modern retail supply chains. The region is witnessing accelerated modernization, with increased use of automated cutting lines, stainless-steel hygienic systems, and precision slicing equipment to support large-scale production. Trade partnerships and food import substitution programs in GCC countries are encouraging local processing expansion. Companies such as Al Thika Packaging play a notable role by distributing and integrating advanced cutting solutions tailored to regional production needs. Consumer behavior is influenced by growing preference for convenient, ready-to-cook foods, supporting sustained investments in cutting automation across processing facilities.

United States – 28.5% Market Share: Strong dominance due to large-scale food processing capacity, high automation maturity, and continuous investments in smart cutting technologies.

China – 21.7% Market Share: Leadership supported by rapid industrialization, high domestic food production volumes, and expansion of automated processing plants across major provinces.

The competitive environment in the Industrial Food Cutting Machines Market remains moderately consolidated, with a mix of long-established global manufacturers and multiple mid-size firms active worldwide. There are over 20 significant competitors operating globally, ranging from traditional cutting-machine specialists to newer firms offering customized food-processing solutions. The top 5 companies collectively control roughly 60–65% of the global equipment installations, indicating a strong but not monopolistic concentration.

Leading incumbents dominate market positioning through deep installed bases, widespread after-sales service networks, and broad product portfolios covering slicers, dicers, shredders, portioners, and turnkey processing lines. These players frequently pursue strategic initiatives such as expanded distribution partnerships, modular system launches, and integration of automation and digital services. For example, one leading firm recently introduced modular high-speed dicers capable of 2,400 cuts per minute. Others are investing heavily in ultrasonic cutting, AI-driven portioning, predictive maintenance, and sanitation-compliant wash-down systems.

The market exhibits fragmented competitive dynamics beyond the top tier, with dozens of small-to-medium players focusing on regional demand, niche food categories (e.g. fruit & vegetable, pet food, artisanal processing), or customized retrofit solutions. This structure fosters ongoing competition on price, service support, flexibility, and adaptation to local regulation and hygiene standards. Innovation trends such as sensor-based portion control, automated blade calibration, and energy-efficient designs increasingly shape competitive differentiation, compelling firms to continuously upgrade their technological offerings and service delivery capabilities.

Urschel Laboratories

FAM STUMABO

Marel hf

TREIF Maschinenbau GmbH

Holac Maschinenbau GmbH

The Industrial Food Cutting Machines Market is undergoing a significant technological transformation driven by innovations in automation, robotics, digital monitoring, and hygiene-compliant design. Traditional cutting machines with manual setup are increasingly being replaced by servo-driven slicers and dicers with programmable logic controls that enable uniform slicing, dicing, and portioning across varying food types — from meat to vegetables, dairy, and bakery products. Modern machines now support vision-guided portion control, allowing real-time adjustments for product size, weight, and shape that improve consistency and minimize product waste.

Emerging technologies such as ultrasonic cutting, water-jet slicing, and laser-guided trimming are gaining traction especially for delicate or high-value food items, offering high precision with minimal product deformation or contamination risk. In parallel, IoT-enabled predictive maintenance systems are being integrated in cutting lines — sensors monitor blade wear, motor load, and hygiene cycles, generating alerts for maintenance before breakdowns, thereby reducing unplanned downtime by a significant margin.

Robotic automation is also entering cutting processes: collaborative robot arms working alongside human operators can safely perform slicing, trimming, and portioning tasks in meat processing lines, offering both safety and productivity improvements. These robotics-supported lines enhance throughput and provide flexibility for mixed-product runs.

Hygiene and sanitization remain a critical focus: stainless-steel construction, wash-down capability, easy disassembly for cleaning, and automated sanitation cycles are increasingly standard — essential for compliance with food-safety regulations. Additionally, modular machine architectures allow processors to scale capacity by adding or replacing modules rather than entire lines, facilitating gradual upgrades and cost-effective scaling.

Overall, technological developments are driving enhanced operational efficiency, precision, safety, and flexibility — enabling food processors to meet growing demand for consistent-quality, compliant, and diversified food products across global markets.

In early 2024, KRONEN reported that Alzarro Dönerworld GmbH began production using KRONEN processing lines for its take-and-bake döner kebab facility, automating vegetable washing, cutting and portioning to support continuous production runs and hygienic, sealed product formats. Source: www.kronen.eu

Effective January 1, 2024, Weber Maschinenbau formally changed its corporate identity to Weber Food Technology GmbH, consolidating its global branding and signalling a strategic shift toward full-line solution provision, expanded international presence, and integrated customer-centric processing solutions. Source: us.weberweb.com

On 12 March 2024, GEA launched InsightPartner, a real-time monitoring and diagnostic platform showcased at Anuga FoodTec, providing continuous equipment health monitoring, production analytics, and remote diagnostics to reduce unplanned downtime and optimize processing-line performance. Source: www.gea.com

In 2024, TREIF’s HAWK portion cutter / RoboPacker solution was introduced as a plug-and-play portioning and automated tray-packing offering, capable of up to 360 slices per minute with intelligent scanning to maximise yield and streamline tray packaging for protein processors. Source: www.marel.com

This report encompasses a comprehensive global analysis of the Industrial Food Cutting Machines Market, covering all major product types including slicers, dicers, shredders, portioners, shred/cube systems, specialty cutters, and modular turnkey processing lines. It addresses all key applications across meat & poultry, seafood, dairy, bakery/confectionery, fruits & vegetables, and ready-meal/processed foods. The geographic scope spans all major regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — with detailed regional segmentation and regional demand patterns.

The report evaluates end-user segments including large-scale food processors, mid-size manufacturers, food-service operators, institutional kitchens, and fresh-cut produce processors. It also includes technology coverage, detailing current-generation digital cutters, automated portioning systems, robotic-assisted cutting lines, ultrasonic and water-jet cutting technologies, intelligent maintenance and IoT-enabled diagnostics, and hygiene-compliant sanitation systems.

Furthermore, the scope includes industry focus areas such as food safety and regulatory compliance, energy and resource efficiency, sustainability initiatives, automation-driven labor reduction, modular expansion strategies, aftermarket services and maintenance, and supply-chain readiness for global food standards. The report examines innovation trends, regional consumption and export-driven demand, capacity expansion for high-volume production, and the evolving needs of processed and ready-to-eat food markets.

Overall, the report offers decision-makers a panoramic view of current market structure, technological evolution, regional demand variation, product segmentation, end-user dynamics, and future growth levers — providing strategic insights for investment, product development, and market entry planning in the Industrial Food Cutting Machines sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 340.0 Million |

| Market Revenue (2032) | USD 554.3 Million |

| CAGR (2025–2032) | 6.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GEA Group AG, Weber Maschinenbau GmbH, KRONEN GmbH, Urschel Laboratories, FAM STUMABO, Marel hf, TREIF Maschinenbau GmbH, Holac Maschinenbau GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |