Reports

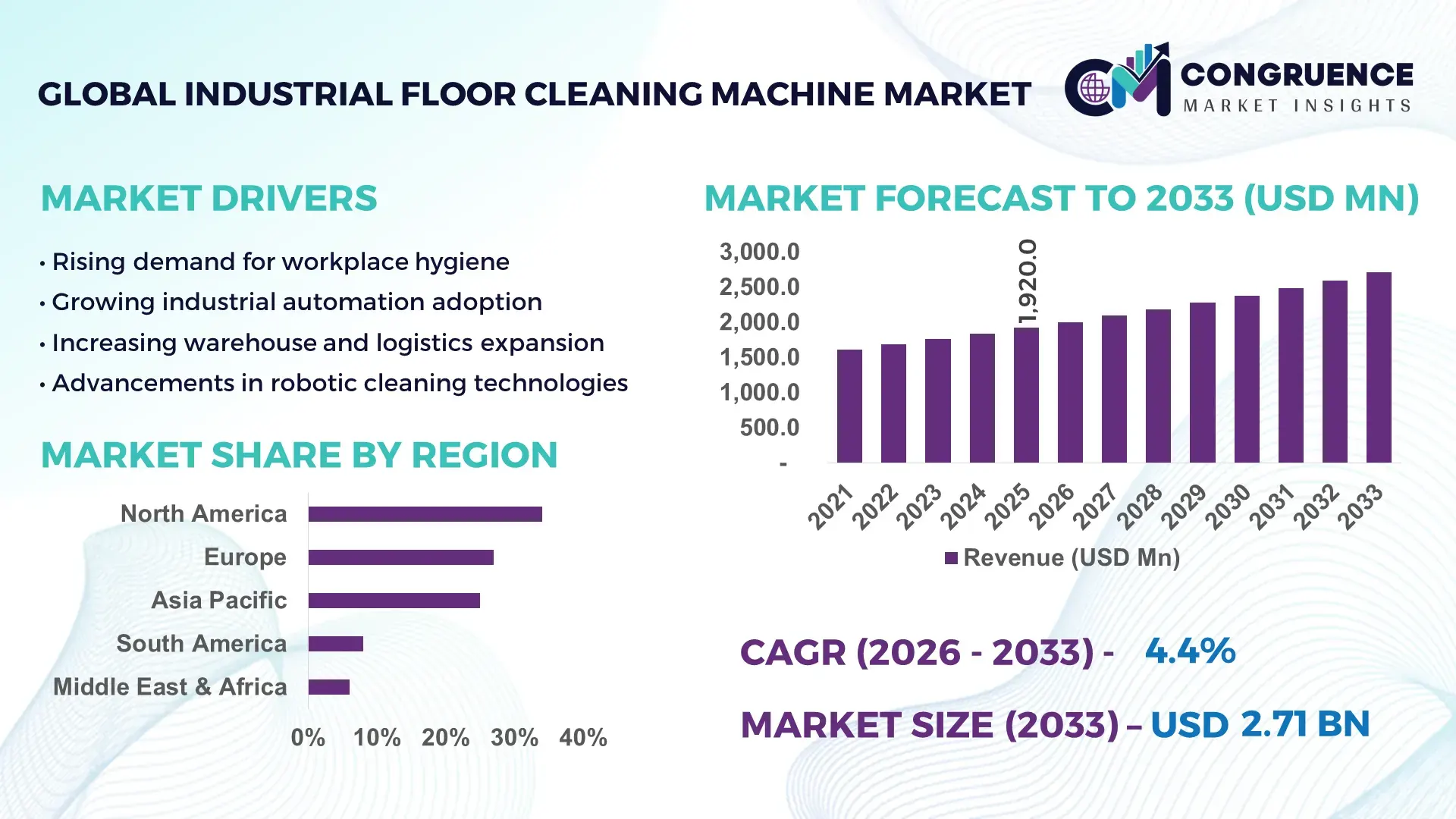

The Global Industrial Floor Cleaning Machine Market was valued at USD 1,920 Million in 2025 and is anticipated to reach a value of USD 2,709.6 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033.

The market is being driven by rapid integration of autonomous and sensor-enabled cleaning systems, with robotic scrubber adoption increasing by over 28% across large-scale warehouses and manufacturing facilities seeking labor cost optimization and operational precision. Between 2024 and 2026, global supply chain restructuring and stricter workplace hygiene mandates—especially post-pandemic regulatory tightening in the EU and North America—are accelerating replacement cycles for conventional cleaning systems.

The United States dominates the global landscape with approximately 34% market share, supported by over 120,000 large industrial facilities and aggressive automation investments exceeding 18% annually in facility management technologies; the logistics and e-commerce sector alone accounts for nearly 42% of advanced machine deployments, compared to 27% in Europe, reflecting stronger automation penetration. Compared to manual cleaning methods, automated industrial machines improve cleaning efficiency by up to 35% while reducing water consumption by nearly 20%, reinforcing their operational advantage across high-traffic environments.

This positions the market as a critical lever for cost efficiency and compliance, compelling companies to prioritize automation-led cleaning infrastructure as a long-term strategic investment.

Market Size & Growth: USD 1,920M (2025) to USD 2,709.6M (2033) at 4.4%, driven by 28% rise in automation-led facility upgrades.

Top Growth Drivers: Automation adoption (+28%), labor cost pressure (+22%), hygiene compliance (+19%).

Short-Term Forecast: By 2027, cleaning cycle efficiency improves by 30% while labor costs decline by 18%.

Emerging Technologies: AI navigation, IoT-enabled monitoring, lithium-ion battery systems improving uptime by 25%.

Regional Leaders: North America (~USD 780M), Europe (~USD 610M), Asia-Pacific (~USD 530M); driven by automation, regulation, and industrial expansion.

Consumer/End-User Trends: Over 46% of large facilities shifting to autonomous scrubbers for continuous operations.

Pilot/Case Example: 2025 warehouse automation project improved cleaning speed by 33% and reduced downtime by 21%.

Competitive Landscape: Top player holds ~17% share; key firms include Tennant, Nilfisk, Kärcher, Hako, and IPC Group.

Regulatory & ESG Impact: Water-efficient machines cut usage by 20%, aligning with sustainability compliance mandates.

Investment & Funding: Over USD 420M invested in smart cleaning tech, driven by partnerships and robotics expansion.

Innovation & Future Outlook: Next-gen robotic fleets and predictive maintenance reshaping large-scale facility operations.

Industrial demand is primarily led by manufacturing (38%), logistics & warehousing (31%), and healthcare (14%), reflecting high-intensity cleaning requirements. Advanced robotic systems with AI-based navigation have improved operational efficiency by 30%, while battery innovations extend runtime by 25%. Asia-Pacific is witnessing a 27% rise in demand due to rapid industrialization, while supply chain realignment continues to push localized production. The shift toward autonomous cleaning ecosystems is redefining operational standards and setting the stage for strategic transformation.

The Industrial Floor Cleaning Machine Market is rapidly transforming into a critical battleground for operational efficiency, cost optimization, and regulatory compliance, making it a high-priority investment segment for facility operators and industrial enterprises. As industries scale automation, cleaning operations are no longer peripheral but central to productivity, safety, and asset longevity. A major structural shift is emerging from tightening hygiene and sustainability regulations, forcing companies to upgrade legacy cleaning systems and integrate smart, resource-efficient technologies.

Autonomous robotic cleaning systems improve efficiency by 35% while reducing labor costs by 22% compared to manual or semi-automatic systems, creating a decisive performance gap that is accelerating adoption across large facilities. North America leads in volume with nearly 34% share, while Asia-Pacific leads in adoption acceleration with over 27% increase in deployment rates driven by rapid industrial expansion and cost-sensitive automation strategies.

In the next 2–3 years, facilities are expected to achieve up to 30% improvement in cleaning cycle productivity and reduce water usage by 20%, directly impacting operational cost structures. ESG positioning is emerging as a competitive advantage, as water-efficient and energy-optimized machines enable up to 18% cost savings while ensuring compliance with tightening environmental standards.

A real-world example includes a global logistics operator deploying robotic scrubbers across distribution hubs, achieving 32% reduction in cleaning time and 24% labor cost savings within one year. Meanwhile, leading manufacturers are shifting capital allocation toward AI-enabled product lines and expanding production capacity by over 15% to meet demand. The market is decisively shifting toward intelligent, automated ecosystems, and companies that accelerate adoption, optimize operations, and align with sustainability mandates will secure a durable competitive edge in this evolving landscape.

The Industrial Floor Cleaning Machine Market is undergoing a structural transformation driven by automation, sustainability requirements, and operational efficiency mandates. Increasing industrialization and the expansion of large-scale facilities such as warehouses, manufacturing plants, and logistics hubs are intensifying demand for high-performance cleaning systems. Over 45% of large industrial sites have already transitioned to mechanized cleaning solutions, reflecting a clear shift from manual processes to automated systems.

Technological advancements such as AI-enabled navigation, IoT-based monitoring, and energy-efficient battery systems are redefining product capabilities and operational outcomes. At the same time, regulatory pressures related to water usage and workplace hygiene are compelling industries to adopt advanced cleaning technologies. However, cost sensitivity in emerging markets and infrastructure limitations continue to influence adoption patterns. Overall, the market is characterized by a strong push toward automation balanced by operational and economic constraints, creating a dynamic environment for strategic decision-making.

The primary growth driver in the Industrial Floor Cleaning Machine Market is the accelerating shift toward automation, driven by rising labor costs and the need for operational efficiency. Automated and robotic cleaning machines have seen adoption rates increase by over 28%, particularly in logistics and manufacturing sectors where continuous operations demand consistent cleaning performance. The global labor shortage and wage inflation, especially post-COVID supply chain disruptions, have further intensified this shift. This transition is directly improving productivity, with automated systems delivering up to 35% higher cleaning efficiency and reducing labor dependency by nearly 22%. Companies are responding by expanding production capacity, investing in R&D, and forming strategic partnerships to develop advanced robotic solutions. The result is a rapid transformation of cleaning operations from labor-intensive processes to technology-driven systems, fundamentally reshaping demand dynamics.

Despite strong growth momentum, high upfront costs and infrastructure limitations remain key restraints in the Industrial Floor Cleaning Machine Market. Advanced robotic cleaning machines can cost 30–40% more than conventional equipment, limiting adoption among small and medium enterprises. Additionally, inconsistent power infrastructure and limited technical expertise in developing regions restrict scalability. Supply chain disruptions and dependence on imported components—particularly batteries and sensors—have led to cost volatility of up to 18% in recent years. These factors directly impact purchasing decisions, delaying large-scale deployment. To mitigate these challenges, companies are diversifying supply chains, investing in localized manufacturing, and offering flexible financing models. However, cost sensitivity continues to constrain widespread adoption, particularly in price-sensitive markets.

The integration of AI, IoT, and data analytics presents a significant opportunity for the Industrial Floor Cleaning Machine Market. Smart cleaning systems equipped with real-time monitoring and predictive maintenance capabilities are improving operational efficiency by over 30% while reducing downtime by 25%. Emerging markets are witnessing adoption growth exceeding 26%, driven by rapid industrialization and infrastructure expansion. A key innovation shift is the development of fully autonomous cleaning fleets capable of operating 24/7, unlocking new efficiency gains and cost advantages. Companies are investing heavily in R&D and forming ecosystem partnerships to accelerate innovation. This is creating new revenue streams and positioning advanced cleaning technologies as a critical component of smart facility management systems.

Scalability and integration challenges represent a major hurdle for the Industrial Floor Cleaning Machine Market. Deploying advanced cleaning systems across large, complex facilities requires significant infrastructure upgrades and integration with existing operational systems. Approximately 32% of companies report difficulties in integrating new technologies with legacy systems, impacting deployment timelines. Additionally, performance consistency in diverse industrial environments remains a concern, with efficiency variations of up to 15% depending on floor type and operational conditions. Regulatory compliance and evolving safety standards further add complexity. Companies must invest in continuous innovation, workforce training, and strategic partnerships to address these challenges. Failure to do so could limit long-term scalability and competitive positioning.

Automation penetration exceeds 45% in large facilities, reshaping execution models: Adoption of autonomous cleaning systems has crossed 45% in high-capacity warehouses and manufacturing plants, with deployment cycles accelerating by 22%. Companies are integrating AI navigation and real-time monitoring, reducing manual intervention by 30% and optimizing cleaning schedules, directly improving operational uptime and cost efficiency.

Battery and energy efficiency improvements reduce downtime by 25%: Lithium-ion battery adoption has increased by 35%, extending machine runtime and reducing charging frequency by 25%. This shift is driven by energy cost pressures and sustainability mandates, enabling companies to maintain continuous operations while lowering energy consumption and operational disruptions.

Asia-Pacific demand surges by 27% driven by industrial expansion: Rapid industrialization and infrastructure investments are pushing demand growth beyond 27% in Asia-Pacific. Local manufacturing expansion and supply chain diversification are enabling faster deployment, while cost-sensitive buyers prioritize scalable and efficient solutions, forcing global players to localize production strategies.

Service-based business models expand by 20%, redefining ownership structures: Subscription-based and leasing models have grown by 20%, allowing companies to adopt advanced cleaning systems without high upfront costs. This shift is reducing financial barriers, enabling faster adoption, and creating recurring revenue streams for manufacturers, while also intensifying competition on service quality and uptime guarantees.

The Industrial Floor Cleaning Machine Market is segmented by type, application, and end-user, reflecting diverse operational needs and adoption patterns across industries. Scrubber machines dominate with approximately 48% share due to their efficiency in large-scale cleaning, while sweepers and robotic cleaners are gaining traction with combined growth exceeding 25%. Demand is heavily concentrated in manufacturing and logistics applications, which together account for over 65% of usage, driven by high cleaning frequency and large floor areas.

A clear shift is observed toward automated and robotic solutions, particularly in high-traffic industrial environments where efficiency and cost optimization are critical. End-user demand is led by manufacturing industries, followed by warehousing and healthcare sectors. Companies are strategically aligning product portfolios to target high-growth segments, focusing on automation, energy efficiency, and scalability to capture evolving demand patterns.

Scrubber machines dominate the Industrial Floor Cleaning Machine Market with approximately 48% share, driven by their superior cleaning performance, water efficiency, and suitability for large industrial spaces. Their ability to deliver consistent cleaning outcomes while reducing water usage by nearly 20% makes them the preferred choice across manufacturing and logistics facilities. In contrast, robotic cleaners are the fastest-growing segment, witnessing adoption growth exceeding 28%, fueled by increasing automation and labor cost pressures. A direct comparison highlights that while traditional scrubbers maintain dominance due to cost-effectiveness and reliability, robotic systems are rapidly gaining traction due to their ability to improve efficiency by over 30% and operate autonomously. Sweepers and other specialized machines account for the remaining 24% share, serving niche applications such as outdoor and heavy debris cleaning. Companies are responding by expanding robotic product lines and integrating AI capabilities into traditional machines. This shift indicates a strategic transition toward automation-driven solutions, with investment increasingly directed toward high-growth robotic segments.

• According to a 2025 report by International Cleaning Equipment Association, robotic floor cleaning machines were adopted by over 32% of large industrial facilities, resulting in a 30% improvement in operational efficiency, reinforcing their growing strategic importance.

Manufacturing facilities lead the application segment with approximately 38% share, driven by continuous production cycles and strict hygiene requirements. Logistics and warehousing follow closely with 31%, reflecting the rapid expansion of e-commerce and distribution networks. Healthcare facilities are the fastest-growing segment, with adoption increasing by over 26%, due to stringent sanitation standards and regulatory compliance requirements. Comparatively, manufacturing remains a mature segment with stable demand, while healthcare is experiencing rapid adoption driven by advanced cleaning technologies and infection control protocols. Other applications, including retail and infrastructure, account for the remaining 31% share, offering steady but less intensive demand. Companies are adapting by developing specialized solutions tailored to industry-specific requirements, such as antimicrobial cleaning systems for healthcare and high-capacity machines for logistics hubs. This evolving demand pattern highlights the importance of targeted product innovation and strategic market positioning.

• According to a 2025 report by Global Facility Management Association, automated cleaning systems were deployed across over 45,000 industrial facilities, improving cleaning efficiency by 28%, highlighting its rapid operational adoption.

Manufacturing industries dominate the end-user segment with approximately 40% share, driven by high cleaning frequency and large operational spaces. Warehousing and logistics represent around 30% of demand, reflecting the rapid growth of e-commerce and distribution networks. Healthcare institutions are the fastest-growing end-user group, with adoption increasing by over 25%, supported by strict hygiene regulations and rising healthcare infrastructure investments. A comparison between manufacturing and healthcare reveals that while manufacturing leads in volume due to scale, healthcare is rapidly gaining importance due to regulatory-driven demand and higher standards of cleanliness. Other end-users, including retail and infrastructure sectors, collectively account for 30% share, showing steady adoption trends. Companies are targeting these segments through customized solutions, flexible pricing models, and strategic partnerships, enabling them to capture evolving demand patterns. This indicates a clear shift toward high-value, regulation-driven markets.

• According to a 2025 report by Industrial Cleaning Federation, adoption among healthcare facilities increased by 27%, with over 18,000 institutions implementing automated cleaning systems, leading to a 25% improvement in hygiene compliance, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America leads in demand concentration due to high automation adoption and advanced facility management practices, while Europe holds approximately 27% share driven by regulatory compliance and sustainability mandates. Asia-Pacific, with nearly 25% share, is accelerating due to rapid industrialization and infrastructure expansion, supported by a 27% increase in manufacturing investments. South America and Middle East & Africa collectively account for 14%, reflecting emerging demand and infrastructure development. A key structural shift includes supply chain localization, pushing production closer to high-growth regions. Companies are prioritizing Asia-Pacific for expansion, North America for innovation, and Europe for compliance-driven product development.

North America holds approximately 34% share, driven by high adoption across manufacturing and logistics sectors. Automation penetration exceeds 48%, with enterprises prioritizing efficiency and labor cost reduction. Regulatory pressure on workplace hygiene and sustainability is forcing upgrades to advanced cleaning systems. Companies are deploying AI-enabled machines, improving operational efficiency by 35%. A key strategic move includes expanding robotic cleaning fleets across large warehouses, increasing deployment scale by over 20%. Enterprises prefer high-performance, data-driven solutions, emphasizing ROI and operational continuity. This positions North America as a priority region for innovation-led investments and advanced technology deployment.

Europe accounts for nearly 27% share, led by Germany, France, and the UK. Strict environmental regulations and water usage restrictions are driving demand for energy-efficient and eco-friendly machines. Adoption of sustainable cleaning technologies has increased by 30%, with companies focusing on compliance and operational efficiency. Manufacturers are introducing low-water consumption systems, reducing usage by 20%. Enterprises prioritize quality and compliance-driven solutions, often opting for premium technologies. This regulatory-driven market forces continuous innovation and positions Europe as a leader in sustainable cleaning solutions.

Asia-Pacific holds around 25% share and is the fastest-growing region, driven by China, India, and Southeast Asia. Industrial expansion and infrastructure development are increasing demand by over 27%. Local manufacturing advantages and cost efficiency are enabling rapid adoption. Companies are scaling production capacity by 22% to meet regional demand. Enterprises prioritize cost-effective, scalable solutions, balancing performance with affordability. This makes Asia-Pacific critical for volume growth and global expansion strategies.

South America contributes approximately 8% share, led by Brazil and Argentina. Industrial growth and infrastructure development are driving demand, particularly in manufacturing and logistics sectors. However, cost sensitivity and limited access to advanced technologies remain key constraints, with adoption rates lagging by nearly 15% compared to global averages. Companies are introducing affordable solutions and flexible financing models to drive adoption. Enterprises prioritize cost-effective and durable machines. This region presents both opportunity and risk, requiring strategic pricing and localized approaches.

Middle East & Africa account for around 6% share, driven by infrastructure and construction activities in the UAE and Saudi Arabia. Demand is increasing by over 18%, supported by large-scale development projects. Companies are deploying advanced cleaning systems in commercial and industrial facilities, improving efficiency by 25%. Strategic partnerships and investments are enabling technology adoption. Enterprises prioritize performance and reliability in harsh environments. This region is emerging as a strategic market driven by infrastructure-led demand and modernization initiatives.

United States – 34% Market share: Dominance driven by high automation adoption and extensive industrial infrastructure supporting advanced cleaning solutions.

China – 21% Market share: Strong manufacturing base and rapid industrial expansion fueling large-scale demand for cost-efficient cleaning systems.

The Industrial Floor Cleaning Machine Market is characterized by intense competition between global leaders, regional manufacturers, and emerging technology innovators. Key players such as Tennant Company, Nilfisk Group, Kärcher, Hako Group, and IPC Group collectively hold approximately 52% market share, competing on technology innovation, product performance, and global distribution networks.

Competition is primarily driven by automation capabilities, with robotic cleaning solutions improving efficiency by over 30%, while cost-focused players emphasize affordability and scalability. Global leaders are investing heavily in R&D and expanding product portfolios, while regional players focus on localized manufacturing and competitive pricing. Strategic partnerships, mergers, and vertical integration are becoming common, enabling companies to strengthen supply chains and enhance market reach.

A key competitive shift is the transition toward AI-enabled and IoT-integrated systems, redefining performance benchmarks. High entry barriers include technological complexity and capital investment requirements. To succeed, companies must prioritize innovation, operational efficiency, and strategic expansion to maintain competitive advantage.

Nilfisk Group

Alfred Kärcher SE & Co. KG

Hako Group

IPC Group

Comac S.p.A.

Fimap S.p.A.

Taski (Diversey Holdings)

Numatic International Ltd.

Roots Multiclean Ltd.

Amano Corporation

Bucher Industries (Municipal Division)

The Industrial Floor Cleaning Machine Market is being reshaped by rapid technological advancements, particularly in automation, connectivity, and energy efficiency. AI-powered navigation systems are now deployed in over 40% of advanced machines, enabling real-time obstacle detection and route optimization, improving cleaning efficiency by up to 35%. IoT integration allows predictive maintenance, reducing downtime by nearly 25% and enhancing operational reliability.

Battery technology is another critical area, with lithium-ion systems replacing traditional lead-acid batteries in over 35% of machines. These advanced batteries extend runtime by 25% and reduce charging cycles, significantly lowering operational costs. Compared to legacy systems, modern battery-powered machines improve energy efficiency by 20% while reducing maintenance requirements.

A key competitive advantage lies in the integration of robotics and data analytics, enabling autonomous cleaning fleets capable of continuous operation. Leading companies are investing in smart platforms that provide real-time performance insights, allowing enterprises to optimize cleaning schedules and resource allocation.

Looking ahead to 2026–2028, the adoption of fully autonomous and cloud-connected cleaning ecosystems is expected to exceed 50%, transforming facility management practices. Companies that leverage these technologies will gain a significant edge in efficiency, scalability, and cost optimization.

March 2026 – Tennant Company Acquired Swedish distributors Clean Machine Falkenberg AB and Repax AB to strengthen regional distribution and accelerate European expansion, directly increasing market access and service reach across Scandinavia. [Market Expansion] Source: www.tennantco.com

January 2025 – Tennant Company Expanded manufacturing of its X4 ROVR™ autonomous scrubber in Europe, enabling localized production and faster delivery cycles while scaling supply capacity for rising AMR demand across EMEA.[Production Scaling]

February 2025 – Tennant Company Began European manufacturing of the T16AMR robotic floor scrubber, marking a major operational shift toward regionalized production and reducing logistics dependency for high-demand autonomous systems. [Localization Strategy]

February 2026 – Nilfisk Group Reported strengthened competitiveness through pricing optimization and operational efficiency improvements, maintaining a 42.0% gross margin despite tariff pressures and supply chain cost fluctuations. [Operational Optimization]

This report provides a comprehensive analysis of the Industrial Floor Cleaning Machine Market, covering segmentation by type, application, and end-user, along with detailed regional insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates key technologies including robotic automation, IoT integration, and energy-efficient battery systems, offering a complete view of the evolving market landscape.

The report delivers in-depth analytical insights, examining over 12 key market segments and profiling more than 10 major companies. It includes adoption trends, with automation penetration exceeding 45% in large facilities and energy-efficient systems reducing operational costs by up to 20%. Regional distribution and demand patterns are analyzed using precise share-based insights, ensuring a balanced and accurate market perspective.

Strategically, the report supports decision-making by identifying high-growth segments, emerging technologies, and competitive dynamics. It highlights future opportunities between 2026 and 2033, focusing on automation, sustainability, and digital transformation. This enables businesses to optimize investments, expand market presence, and strengthen competitive positioning in a rapidly evolving industrial environment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,920 Million |

| Market Revenue (2033) | USD 2,709.6 Million |

| CAGR (2026–2033) | 4.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tennant Company; Nilfisk Group; Alfred Kärcher SE & Co. KG; Hako Group; IPC Group; Comac S.p.A.; Fimap S.p.A.; Diversey Holdings (TASKI); Numatic International Ltd.; Roots Multiclean Ltd.; Amano Corporation; Bucher Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |