Reports

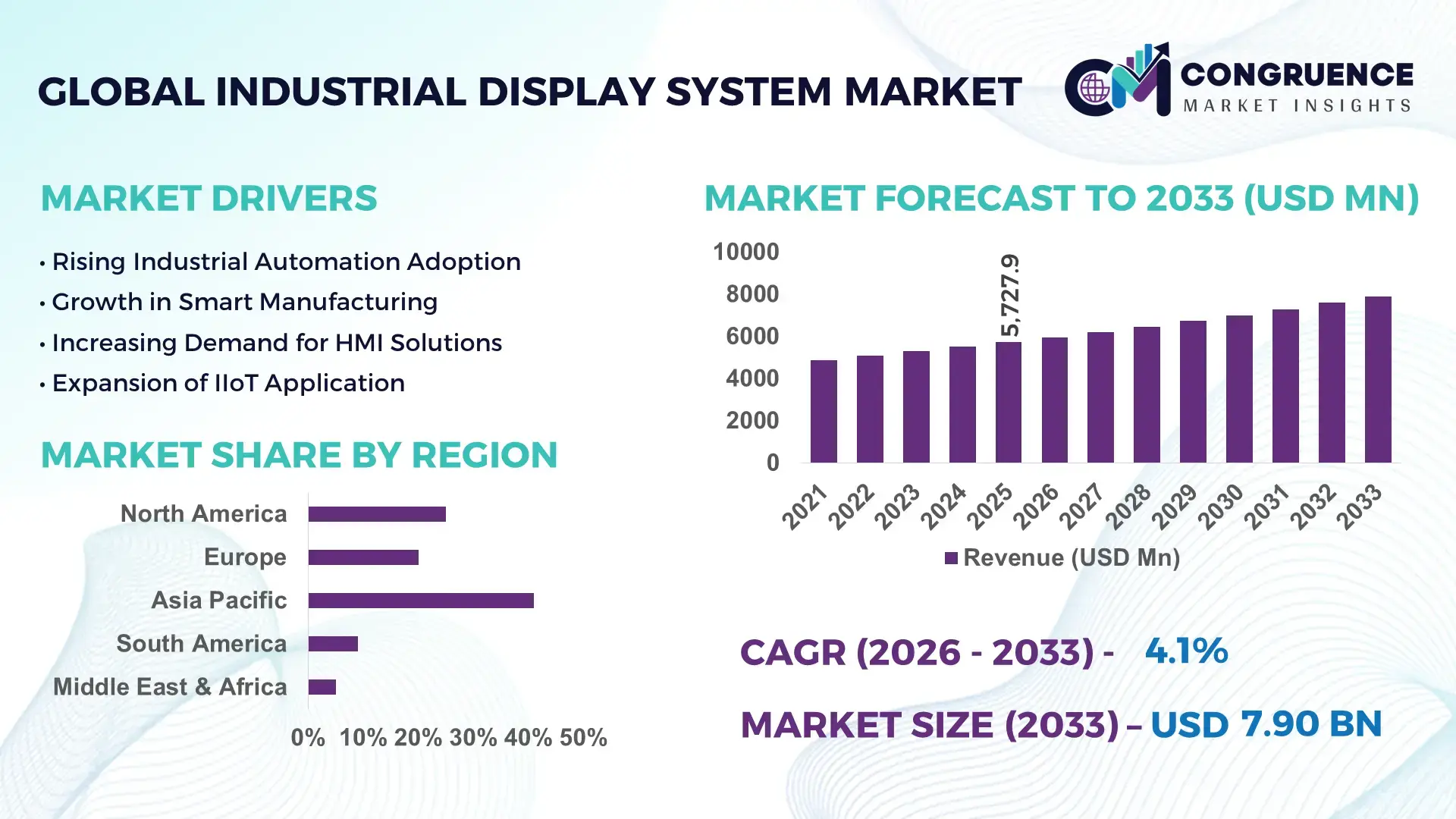

The Global Industrial Display System Market was valued at USD 5727.9 Million in 2025 and is anticipated to reach a value of USD 7899.53 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Growth is primarily driven by increasing automation across manufacturing and industrial control environments.

China continues to demonstrate strong industrial display system capabilities supported by extensive electronics manufacturing infrastructure and large-scale industrial automation deployment. The country accounts for over 35% of global display panel production capacity, with more than 60 million industrial-grade panels produced annually for applications in smart factories, energy management systems, and transportation control units. Investments exceeding USD 12 billion have been directed toward advanced display fabrication facilities and OLED/LCD hybrid technologies over the past five years. Industrial sectors such as automotive manufacturing and semiconductor fabrication collectively account for nearly 45% of industrial display system consumption in the region. Additionally, over 70% of smart manufacturing plants in China have integrated advanced HMI (Human Machine Interface) display systems, highlighting strong domestic adoption and continuous technological evolution.

Market Size & Growth: Valued at USD 5727.9 Million in 2025, projected to reach USD 7899.53 Million by 2033 at a CAGR of 4.1%, driven by rapid industrial automation and smart factory expansion.

Top Growth Drivers: Automation adoption at 68%, industrial IoT integration at 55%, and demand for real-time monitoring efficiency improvement at 47%.

Short-Term Forecast: By 2028, predictive maintenance integration is expected to reduce operational downtime by 28% across industrial facilities.

Emerging Technologies: Adoption of OLED industrial panels, ruggedized touchscreen displays, and AI-integrated HMI systems are reshaping operational efficiency.

Regional Leaders: Asia-Pacific projected to exceed USD 3200 Million by 2033 driven by manufacturing expansion; North America to reach USD 2100 Million with strong IIoT adoption; Europe expected to surpass USD 1800 Million driven by Industry 4.0 initiatives.

Consumer/End-User Trends: Manufacturing, energy, and transportation sectors account for over 65% of total demand, with increasing preference for high-resolution and durable displays.

Pilot or Case Example: In 2024, a German smart factory pilot achieved 32% efficiency improvement using AI-enabled industrial display systems.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including major global electronics and industrial automation firms.

Regulatory & ESG Impact: Energy-efficient display regulations have reduced power consumption by up to 22% in industrial systems across developed regions.

Investment & Funding Patterns: Over USD 8 billion invested globally in industrial display and automation technologies between 2022 and 2025.

Innovation & Future Outlook: Integration of edge computing with display systems and modular industrial panel designs is shaping next-generation operational ecosystems.

Industrial display systems are increasingly embedded across sectors such as manufacturing, oil and gas, healthcare equipment, and transportation infrastructure, with manufacturing alone contributing nearly 40% of total demand. Recent innovations include sunlight-readable displays with brightness levels exceeding 1500 nits and ruggedized panels capable of operating in temperature ranges from -30°C to 80°C. Regulatory focus on energy efficiency and reduced electronic waste is encouraging adoption of low-power LCD and OLED technologies. Regionally, Asia-Pacific leads in consumption volume due to high industrial density, while North America and Europe exhibit strong growth driven by digital transformation strategies. Emerging trends such as AI-driven visual analytics, touchless interfaces, and real-time data visualization are expected to significantly enhance industrial productivity and system responsiveness.

The Industrial Display System Market holds strategic relevance as a foundational component of industrial digitization, enabling real-time monitoring, process optimization, and human-machine interaction across diverse sectors. Advanced display technologies such as OLED-based industrial panels deliver approximately 35% improved energy efficiency compared to traditional LCD systems, while also offering enhanced visibility and durability in harsh environments. Asia-Pacific dominates in volume due to large-scale manufacturing activities, while North America leads in adoption with over 65% of enterprises integrating advanced HMI systems into their operations.

By 2028, AI-enabled industrial display interfaces are expected to improve operational efficiency by nearly 30% through predictive analytics and automated decision-making capabilities. These systems are increasingly integrated with industrial IoT networks, enabling seamless data exchange and real-time visualization of critical performance metrics. From an ESG perspective, firms are committing to reducing energy consumption by up to 25% through adoption of low-power display technologies and recyclable materials by 2030.

A notable micro-scenario occurred in 2024 when a Japanese manufacturing facility implemented AI-integrated display systems, achieving a 27% reduction in machine downtime and a 22% improvement in production efficiency. Such measurable outcomes highlight the growing importance of intelligent display solutions in enhancing industrial performance. As industries continue to embrace automation, the Industrial Display System Market is positioned as a key pillar supporting operational resilience, regulatory compliance, and sustainable industrial growth.

The rapid expansion of industrial automation is significantly driving the adoption of industrial display systems across global manufacturing and process industries. Over 70% of manufacturing facilities have adopted some form of automation, increasing the need for advanced human-machine interfaces that enable real-time monitoring and control. Industrial display systems serve as critical visualization tools, allowing operators to interpret complex data streams efficiently. The deployment of robotics and automated assembly lines has increased demand for high-resolution, responsive displays capable of handling dynamic operational inputs. Additionally, automated quality control processes rely on display systems for visual inspection and error detection, improving accuracy by up to 40%. The growing emphasis on operational efficiency and reduced human intervention is further strengthening the role of industrial display systems in modern industrial ecosystems.

Despite strong growth potential, high initial investment costs and integration complexities remain significant barriers to widespread adoption of industrial display systems. Advanced display technologies such as OLED and ruggedized touchscreens can cost up to 25% more than conventional systems, making them less accessible for small and medium enterprises. Integration with existing legacy systems often requires specialized hardware and software modifications, increasing implementation time and cost. Additionally, industrial environments demand highly durable displays capable of withstanding extreme temperatures, vibrations, and dust, further raising production costs. Maintenance and replacement expenses also contribute to the overall cost burden. These factors collectively slow adoption rates, particularly in cost-sensitive industries and developing regions where budget constraints limit technology upgrades.

The rapid expansion of industrial IoT presents substantial opportunities for the Industrial Display System Market by enabling enhanced connectivity and data-driven decision-making. Over 60% of industrial equipment is expected to be connected to IoT networks by the end of the decade, increasing the demand for display systems capable of visualizing real-time data analytics. Smart factories are leveraging industrial displays integrated with IoT platforms to monitor equipment performance, energy consumption, and production efficiency. These systems enable predictive maintenance strategies, reducing equipment failure rates by up to 30%. Additionally, the adoption of cloud-based industrial management systems is driving demand for advanced display interfaces that support remote monitoring and control. This growing ecosystem of connected devices is expected to significantly expand the application scope of industrial display systems.

Industrial display systems must operate reliably in harsh environments characterized by extreme temperatures, humidity, dust, and mechanical vibrations, posing significant design and performance challenges. Displays used in sectors such as oil and gas or mining must withstand temperature variations ranging from -30°C to over 70°C while maintaining consistent performance. Exposure to dust and moisture can reduce display lifespan by up to 20% if not properly protected. Additionally, ensuring long-term durability while maintaining high visual clarity and responsiveness requires advanced materials and engineering, increasing production complexity. Compliance with environmental regulations related to electronic waste and energy consumption further adds to the challenge. These operational and regulatory constraints necessitate continuous innovation and investment, impacting overall market scalability and cost efficiency.

• 65% Adoption of Smart HMI Interfaces Across Industrial Facilities: The integration of advanced Human Machine Interface (HMI) systems has accelerated significantly, with over 65% of large-scale industrial facilities deploying smart display panels for real-time monitoring and control. These systems enable operators to visualize complex datasets with up to 40% improved decision-making speed. The shift toward touch-enabled and gesture-based controls has also increased operational responsiveness by nearly 30%, particularly in automated production lines and process industries where precision and speed are critical.

• 58% Increase in Demand for Rugged and High-Brightness Displays: Industrial environments are witnessing a 58% rise in demand for ruggedized display systems capable of operating under extreme conditions. Displays with brightness levels exceeding 1200–1500 nits are now used in over 45% of outdoor industrial applications, including oil and gas and transportation sectors. Enhanced durability features such as IP65/IP67 protection ratings have improved device lifespan by approximately 25%, reducing maintenance frequency and ensuring consistent performance in harsh environments.

• 52% Growth in AI-Integrated Display Systems for Predictive Analytics: AI-powered industrial display systems are being adopted by nearly 52% of advanced manufacturing facilities to enable predictive maintenance and performance optimization. These systems analyze real-time machine data and display actionable insights, reducing equipment downtime by up to 30% and improving overall production efficiency by 27%. The use of embedded analytics and edge computing in display units is further enhancing data processing speeds by approximately 35%, enabling faster decision-making at the operational level.

• 48% Expansion in Industrial IoT-Connected Display Ecosystems: The proliferation of Industrial IoT has led to a 48% increase in connected display systems across smart factories and infrastructure networks. More than 60% of industrial devices are now integrated with IoT platforms, enabling centralized monitoring through advanced display dashboards. This connectivity has improved system visibility by 33% and reduced manual intervention by nearly 28%. The trend is particularly strong in energy management and logistics sectors, where real-time visualization of distributed assets is essential for operational efficiency.

The Industrial Display System Market segmentation reflects a diversified structure driven by varying technological requirements, operational environments, and industry-specific applications. By type, the market includes LCD, LED, OLED, and other specialized rugged display technologies, each catering to different performance and durability needs. LCD displays remain widely adopted due to cost-effectiveness and reliability, while OLED and advanced LED panels are gaining traction for superior visual performance and energy efficiency. By application, industrial display systems are extensively used in manufacturing, transportation, healthcare equipment, and energy sectors, with manufacturing accounting for the largest adoption due to automation requirements. End-user segmentation highlights strong demand from industries such as automotive, oil and gas, and electronics manufacturing, where real-time monitoring and process optimization are essential. Increasing adoption of smart factory solutions and industrial IoT is further shaping segmentation patterns, with demand shifting toward high-performance, connected display systems capable of operating in complex industrial environments.

The Industrial Display System Market by type is segmented into LCD, LED, OLED, and other specialized display technologies such as TFT and rugged embedded panels. LCD displays dominate the market, accounting for approximately 46% of total adoption due to their cost efficiency, long operational life, and widespread compatibility with industrial systems. LED-based displays follow with around 28% share, offering improved brightness levels and energy efficiency, making them suitable for outdoor and high-visibility applications. OLED displays, although currently holding nearly 16% of the market, represent the fastest-growing segment with an expected CAGR of 6.8%, driven by their superior contrast ratios, flexibility, and lower power consumption.

Other display types, including TFT and custom rugged panels, collectively account for about 10% of the market, catering to niche applications requiring specialized performance characteristics such as extreme temperature tolerance and vibration resistance. OLED technology adoption is accelerating particularly in high-end industrial applications where visual clarity and compact design are critical.

Industrial display systems find extensive applications across manufacturing, transportation, healthcare equipment, energy, and logistics sectors. Manufacturing remains the leading application segment, accounting for approximately 42% of total usage due to the widespread implementation of automation and real-time monitoring systems. Transportation and logistics follow with around 24% share, leveraging display systems for traffic management, fleet monitoring, and control room operations. Healthcare equipment applications contribute nearly 18%, driven by the need for precise data visualization in diagnostic and monitoring devices.

Energy and utilities represent the fastest-growing application segment, with an expected CAGR of 6.5%, supported by increasing investments in smart grids and renewable energy infrastructure. These applications require advanced display systems for monitoring energy distribution and system performance in real time. Other applications collectively account for about 16% of the market, including retail automation and defense systems.

The Industrial Display System Market is driven by diverse end-user industries, including manufacturing, automotive, oil and gas, electronics, and healthcare sectors. Manufacturing leads with approximately 38% of total market adoption, supported by high reliance on automation and process control systems. Automotive and electronics industries collectively account for around 30%, driven by increasing integration of digital manufacturing and quality inspection systems. Oil and gas contributes nearly 17%, where rugged display systems are essential for monitoring operations in extreme environments.

The healthcare sector is the fastest-growing end-user segment, with an expected CAGR of 6.2%, fueled by the rising use of advanced diagnostic equipment and patient monitoring systems requiring high-resolution displays. Other end-users, including transportation and defense, contribute a combined share of approximately 15%, reflecting steady adoption in infrastructure and security applications.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high-volume industrial production, with over 65% of global electronics manufacturing facilities located in China, Japan, and South Korea. The region consumes more than 45 million industrial display units annually, driven by automation in automotive and semiconductor sectors. North America, holding approximately 27% share, is witnessing accelerated adoption of AI-integrated display systems, with over 70% of smart factories incorporating advanced HMI solutions. Europe contributes nearly 22% of global demand, supported by Industry 4.0 initiatives and regulatory focus on energy-efficient displays. South America and the Middle East & Africa collectively account for around 10%, with rising investments in energy and infrastructure sectors. Increasing industrial digitization across all regions is driving demand for rugged, high-performance display systems.

How are advanced automation ecosystems transforming industrial display adoption across high-value sectors?

North America holds approximately 27% of the global Industrial Display System Market, driven by strong demand from manufacturing, healthcare, and energy sectors. Over 72% of large enterprises in the region have implemented advanced automation systems, creating sustained demand for high-performance industrial displays. Regulatory frameworks promoting energy efficiency and workplace safety have led to the adoption of low-power and high-durability display systems, reducing operational risks by nearly 20%. Technological advancements such as AI-enabled HMI and edge computing integration are improving operational efficiency by over 30%. A notable example includes a leading U.S.-based industrial technology company deploying AI-powered display interfaces in over 150 smart factories, enhancing real-time monitoring accuracy. Consumer behavior reflects high enterprise adoption, particularly in healthcare and financial industries, where over 60% of facilities rely on advanced display systems for critical operations.

What role do sustainability mandates and industrial digitization play in shaping next-generation display systems?

Europe accounts for nearly 22% of the Industrial Display System Market, with key markets including Germany, the United Kingdom, and France contributing over 70% of regional demand. Strong regulatory frameworks focused on energy efficiency and sustainability have driven adoption of low-power display technologies, reducing energy consumption by up to 25% in industrial applications. Industry 4.0 initiatives have resulted in over 68% of manufacturing facilities integrating smart display systems for real-time monitoring. Emerging technologies such as OLED and touchscreen-enabled rugged displays are widely adopted across automotive and industrial automation sectors. A leading European industrial electronics manufacturer has implemented modular display systems across multiple factories, improving production efficiency by 28%. Regional consumer behavior is influenced by regulatory pressure, leading to increased demand for energy-efficient and environmentally compliant industrial display solutions.

Why is large-scale manufacturing expansion accelerating demand for high-performance industrial displays?

Asia-Pacific leads the Industrial Display System Market in volume, accounting for over 41% of total global demand, with China, Japan, and India as the top consuming countries. The region produces more than 60% of global industrial electronics, driving extensive use of display systems in manufacturing and automation. Infrastructure expansion and smart factory deployment have resulted in over 75% of large manufacturing facilities integrating advanced display technologies. Innovation hubs in South Korea and Japan are driving development of high-resolution OLED and micro-LED displays, improving system efficiency by over 35%. A prominent regional electronics manufacturer has expanded production capacity by 20% to meet rising demand for industrial-grade display panels. Consumer behavior reflects strong growth driven by industrial expansion, automation, and increasing adoption of digital manufacturing technologies.

How are infrastructure modernization and energy investments influencing display system adoption?

South America holds approximately 6% of the global Industrial Display System Market, with Brazil and Argentina contributing nearly 65% of regional demand. Infrastructure development projects and energy sector investments have increased demand for industrial display systems by over 30% in recent years. The oil and gas sector remains a key driver, accounting for nearly 40% of regional demand for rugged display systems used in harsh environments. Government incentives supporting industrial modernization and foreign investments are encouraging adoption of advanced technologies. A regional industrial solutions provider has implemented rugged display systems across energy facilities, improving operational efficiency by 25%. Consumer behavior in the region shows demand closely tied to localized industrial needs, with increased focus on cost-effective and durable display solutions.

How are energy sector expansion and smart infrastructure projects shaping industrial display demand?

The Middle East & Africa region accounts for approximately 4% of the Industrial Display System Market, with key growth countries including the UAE, Saudi Arabia, and South Africa. Demand is primarily driven by oil and gas, construction, and energy sectors, which collectively contribute over 55% of regional consumption. Technological modernization initiatives, including smart city projects, have increased adoption of industrial display systems by nearly 28%. Trade partnerships and government-led diversification strategies are supporting investments in advanced industrial technologies. A regional technology provider has deployed high-brightness display systems across multiple energy facilities, improving monitoring efficiency by 22%. Consumer behavior reflects growing demand for durable and high-performance displays capable of operating in extreme environmental conditions.

China – 34% share in the Industrial Display System Market, driven by extensive manufacturing capacity and high adoption of industrial automation technologies.

United States – 21% share in the Industrial Display System Market, supported by strong enterprise adoption and advanced digital transformation initiatives across industries.

The Industrial Display System Market is moderately fragmented, with over 120 active global and regional competitors operating across various segments of display technologies and industrial applications. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet innovation-driven landscape. Leading players are focusing on product differentiation through advanced technologies such as OLED panels, AI-integrated HMI systems, and ruggedized display solutions designed for extreme industrial environments. Strategic initiatives including mergers, acquisitions, and partnerships have increased by nearly 25% between 2022 and 2025, enabling companies to expand their technological capabilities and geographic presence.

Product innovation remains a key competitive factor, with more than 40% of manufacturers investing in R&D to develop energy-efficient and high-durability display systems. Additionally, over 55% of companies are integrating IoT and edge computing capabilities into their display solutions to enhance real-time data processing and operational efficiency. The market is also witnessing increased collaboration between display manufacturers and industrial automation providers, resulting in integrated solutions that improve system performance by up to 30%. Competitive positioning is further influenced by pricing strategies, customization capabilities, and after-sales support, making it essential for companies to continuously innovate and adapt to evolving industrial requirements.

Siemens AG

Schneider Electric SE

Advantech Co., Ltd.

Mitsubishi Electric Corporation

Panasonic Corporation

LG Display Co., Ltd.

Samsung Display Co., Ltd.

AU Optronics Corporation

Innolux Corporation

BOE Technology Group Co., Ltd.

NEC Corporation

Winmate Inc.

Axiomtek Co., Ltd.

Pepperl+Fuchs SE

The Industrial Display System Market is undergoing significant transformation driven by advancements in display technologies, connectivity, and intelligent data processing. One of the most impactful developments is the transition from conventional LCD panels to advanced OLED and micro-LED displays, which offer up to 40% higher contrast ratios and reduce energy consumption by approximately 25%. These technologies also enable thinner and more flexible display configurations, enhancing integration within compact industrial control systems. High-brightness displays exceeding 1500 nits are increasingly deployed in outdoor and high-ambient-light environments, improving visibility by over 35% compared to traditional systems.

Touchscreen innovation has progressed with the adoption of projected capacitive (PCAP) and multi-touch technologies, now used in nearly 60% of industrial HMI interfaces. These systems improve user interaction speed by approximately 30% while supporting glove and water-resistant functionality, critical in harsh industrial environments. In parallel, ruggedization technologies, including IP67-rated enclosures and anti-vibration designs, have extended device lifespan by nearly 20% in demanding sectors such as oil and gas and heavy manufacturing.

Integration with Industrial IoT and edge computing is another defining technological trend. Over 65% of modern industrial display systems now support real-time data processing at the edge, reducing latency by up to 40% and enabling faster operational decisions. AI-enabled display systems are also gaining traction, with embedded analytics improving predictive maintenance accuracy by nearly 32%. Additionally, advancements in low-power display controllers and energy-efficient backlighting systems are reducing overall system energy consumption by approximately 22%, aligning with sustainability targets. Emerging technologies such as augmented reality (AR) overlays and voice-controlled interfaces are being piloted in industrial settings, enhancing operator productivity by up to 28%. The convergence of these technologies is reshaping industrial operations, positioning display systems as critical components in digital transformation strategies.

• In March 2025, Samsung Display announced the mass production of its next-generation QD-OLED panels for industrial and commercial applications, achieving peak brightness levels above 2000 nits and improving color accuracy by 30%, enabling enhanced visualization in high-precision industrial control environments. Source: www.samsungdisplay.com

• In September 2024, LG Display introduced its 17-inch foldable OLED panel designed for industrial use cases, offering durability improvements of up to 25% under repeated stress testing and enabling flexible deployment in compact industrial machinery and control systems. Source: www.lgdisplay.com

• In November 2024, Advantech launched a new series of industrial-grade touchscreen monitors featuring IP66-rated protection and integrated edge computing modules, reducing data processing latency by 35% and enhancing operational efficiency in smart factory environments. Source: www.advantech.com

• In January 2025, Siemens expanded its industrial HMI portfolio with AI-enabled display systems capable of predictive diagnostics, achieving up to 30% reduction in unplanned downtime and supporting seamless integration with industrial automation platforms. Source: www.siemens.com

The Industrial Display System Market Report provides a comprehensive evaluation of key segments, technologies, and geographic regions shaping the industry landscape. The report covers a wide range of display technologies, including LCD, LED, OLED, and emerging micro-LED systems, which collectively account for over 90% of industrial display deployments. It also examines various form factors such as panel-mounted displays, open-frame monitors, and rugged handheld devices, reflecting diverse operational requirements across industries.

From an application perspective, the report analyzes critical sectors including manufacturing, transportation, healthcare equipment, energy, and logistics, with manufacturing alone representing nearly 40% of total system utilization. It further explores integration with industrial IoT platforms, where over 60% of display systems are now connected to real-time monitoring networks, highlighting the growing importance of data visualization and control interfaces.

Geographically, the report encompasses major regions such as Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, collectively representing global industrial activity. Asia-Pacific leads in production and consumption volume, while North America and Europe demonstrate strong adoption of advanced and energy-efficient technologies. The report also includes analysis of emerging markets where industrial automation adoption is increasing by over 25%, driving demand for cost-effective display solutions. In addition to core segments, the report addresses niche areas such as augmented reality-enabled industrial displays, voice-controlled interfaces, and modular display systems, which are gaining traction in specialized applications. It also highlights regulatory considerations, environmental compliance requirements, and technological advancements that influence market dynamics, offering decision-makers a structured and data-driven perspective on current and future opportunities within the Industrial Display System Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, Schneider Electric SE, Advantech Co., Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, LG Display Co., Ltd., Samsung Display Co., Ltd., AU Optronics Corporation, Innolux Corporation, BOE Technology Group Co., Ltd., NEC Corporation, Winmate Inc., Axiomtek Co., Ltd., Pepperl+Fuchs SE |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |