Reports

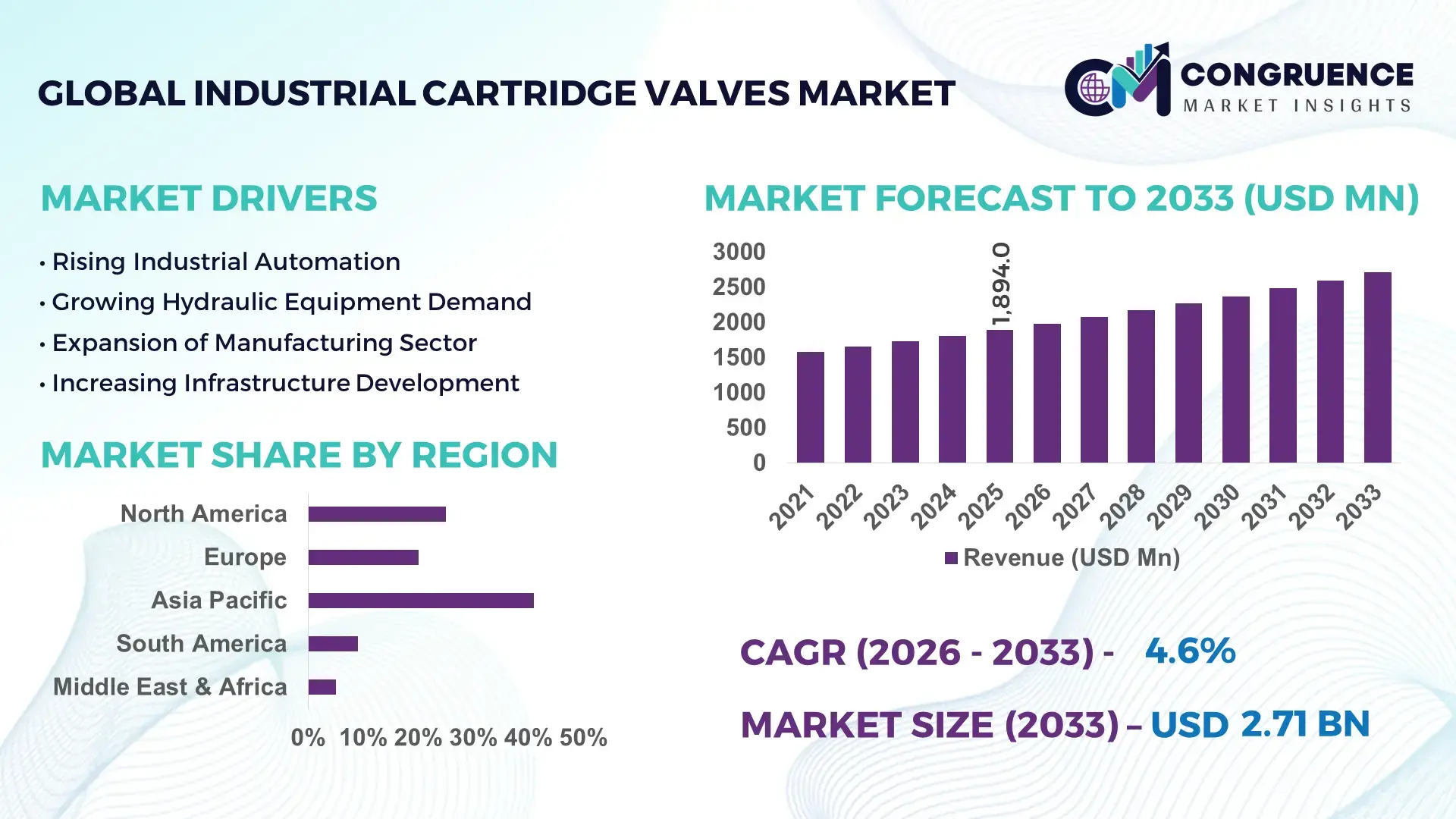

The Global Industrial Cartridge Valves Market was valued at USD 1894 Million in 2025 and is anticipated to reach a value of USD 2714.14 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033.

Demand for advanced industrial cartridge valves is accelerating due to the rapid integration of electro-hydraulic automation systems, with smart hydraulic control platforms improving energy efficiency by nearly 18% in heavy manufacturing and mobile equipment applications. Between 2024 and 2026, reshoring initiatives across North America and Europe, combined with stricter industrial fluid management regulations and Red Sea shipping disruptions, increased procurement focus on localized hydraulic component sourcing and high-durability valve architectures.

China remains the dominant production and consumption hub, accounting for approximately 34% of global industrial cartridge valve demand in 2026, supported by large-scale investments in construction machinery, mining equipment, industrial robotics, and steel processing automation. The country operates over 30% of the world’s hydraulic equipment manufacturing capacity, while smart factory upgrades across coastal industrial provinces improved automated valve integration rates by nearly 22% compared with 2023 levels. In comparison, Germany maintains stronger penetration in precision-engineered proportional cartridge valves used in aerospace and advanced industrial motion systems, where failure-rate reduction below 1.5% has become a competitive benchmark.

Manufacturers prioritizing compact high-pressure valve systems, regionalized supply chains, and predictive maintenance compatibility are positioned to secure stronger OEM partnerships and long-term industrial infrastructure contracts through 2033.

Market Size & Growth: Global market reached USD 1894 Million in 2025 and is projected at USD 2714.14 Million by 2033, driven by rising hydraulic automation across industrial machinery and mobile equipment sectors.

Top Growth Drivers: Industrial automation adoption increased 21%, compact hydraulic system demand rose 17%, and energy-efficient fluid control installations expanded 19% globally.

Short-Term Forecast: By 2027, advanced cartridge valve integration is expected to reduce hydraulic leakage losses by 14% and improve equipment operating efficiency by 16%.

Emerging Technologies: AI-enabled predictive maintenance, proportional valve digitization, and advanced corrosion-resistant alloys improved system uptime by nearly 20% in high-cycle industrial operations.

Regional Leaders: Asia-Pacific exceeds USD 980 Million demand with strong factory automation adoption, Europe advances precision hydraulic systems, and North America expands localized hydraulic manufacturing investments.

Consumer/End-User Trends: Over 42% of OEMs now prioritize modular cartridge valve platforms to simplify maintenance cycles and reduce equipment downtime in industrial operations.

Pilot/Case Example: In 2025, an automated mining hydraulics upgrade project improved pressure stability by 18% while lowering unplanned maintenance shutdowns by 12%.

Competitive Landscape: Top manufacturers collectively control nearly 46% market share, with competition centered on smart hydraulic integration, compact designs, and high-pressure durability.

Regulatory & ESG Impact: Stricter industrial fluid-efficiency standards lowered hydraulic energy consumption by approximately 11% across newly deployed industrial systems between 2024 and 2026.

Investment & Funding: More than USD 780 Million was directed toward hydraulic automation expansion, regional manufacturing facilities, and smart valve technology integration initiatives.

Innovation & Future Outlook: Next-generation electro-hydraulic cartridge valves with embedded diagnostics and digital monitoring capabilities are reshaping high-growth industrial automation strategies globally.

Industrial machinery accounts for nearly 38% of total industrial cartridge valve consumption, followed by construction equipment at 24% and mining applications at 16%, reflecting strong demand from high-pressure hydraulic systems. Manufacturers are accelerating development of digitally controlled proportional valves and compact high-flow designs that improve response accuracy by over 15%. Asia-Pacific continues to lead volume demand due to rapid factory automation expansion, while Europe strengthens adoption of precision hydraulic technologies under stricter industrial efficiency standards. Supply chain regionalization and smart maintenance integration are emerging as defining competitive priorities, setting the stage for deeper strategic investments across automated industrial infrastructure.

Industrial cartridge valves are rapidly becoming a strategic control point in global hydraulic automation as manufacturers prioritize compact fluid-power systems, energy optimization, and predictive maintenance integration. Competitive intensity is accelerating because advanced cartridge valve architectures directly influence machine uptime, pressure stability, and energy efficiency across mining, industrial robotics, marine equipment, and construction machinery. Rising industrial electrification and high-pressure automation requirements are transforming procurement strategies, with OEMs increasing smart hydraulic component integration by 23% since 2024. Simultaneously, supply chain localization pressures and stricter industrial efficiency mandates are forcing manufacturers to redesign sourcing and production footprints across North America and Europe.

Digitally controlled proportional cartridge valves improve operational efficiency by 21% while reducing maintenance cost by 16% compared to legacy mechanical hydraulic systems. Asia-Pacific leads in manufacturing volume, while Europe leads in precision adoption and intelligent hydraulic integration with over 31% penetration across advanced industrial automation facilities. Over the next three years, predictive maintenance-enabled valve systems are projected to reduce unplanned industrial downtime by nearly 18%. ESG positioning is also becoming a competitive advantage, as low-leakage hydraulic platforms reduce fluid waste by 14%, improving regulatory compliance and operational sustainability simultaneously.

In 2025, a large-scale automated steel processing upgrade in Germany improved hydraulic response accuracy by 19% through next-generation cartridge valve deployment integrated with AI-based monitoring systems. Major manufacturers are shifting capital allocation toward modular valve platforms, regional production hubs, and digitally optimized hydraulic ecosystems to secure long-cycle industrial contracts. Companies that accelerate intelligent valve integration, localized manufacturing resilience, and energy-efficient hydraulic innovation are positioning themselves to dominate the next phase of industrial automation competition.

Industrial automation expansion is accelerating demand for advanced cartridge valves as manufacturers prioritize compact hydraulic architectures, faster response cycles, and lower maintenance intensity across heavy equipment and process industries. Automated hydraulic system deployment increased 24% between 2024 and 2026, while adoption of proportional cartridge valves in industrial robotics rose 19%. Global supply chain restructuring and regional manufacturing localization are forcing OEMs to secure higher-performance hydraulic components with shorter delivery cycles and improved durability. This shift directly impacts equipment efficiency, reducing hydraulic energy losses by nearly 15% in automated production systems. In response, leading manufacturers are expanding localized assembly capacity, increasing smart valve investments, and forming strategic partnerships with industrial automation firms to strengthen long-term supply resilience and technology integration.

Raw material volatility and precision manufacturing costs are constraining scalable industrial cartridge valve production, particularly for high-pressure applications requiring advanced steel alloys and corrosion-resistant components. Stainless steel input costs fluctuated by over 18% during 2024–2026, while machining and compliance expenses increased nearly 13% across industrial hydraulic supply chains. Dependence on concentrated component sourcing in Asia continues creating procurement delays and inventory instability for North American and European manufacturers. These pressures directly impact production timelines, margin stability, and contract fulfillment reliability. To mitigate risk, companies are diversifying supplier networks, securing long-term material agreements, and increasing investment in alternative lightweight alloys and digitally optimized machining technologies that improve manufacturing precision while reducing operational dependency on volatile commodity cycles globally.

Smart hydraulic integration is redefining growth opportunities in the industrial cartridge valves market as manufacturers shift toward digitally monitored, energy-efficient fluid control systems. Predictive maintenance adoption increased 27% across automated manufacturing facilities, while intelligent proportional valve deployment improved hydraulic response precision by nearly 20%. Emerging industrial infrastructure investments in Southeast Asia and the Middle East are creating new demand pockets for compact high-pressure valve systems integrated with AI-driven monitoring platforms. A major future signal is the rapid transition toward electro-hydraulic hybrid equipment, which reduces hydraulic energy consumption by approximately 16% compared with conventional systems. Companies are aggressively positioning for long-term dominance through advanced R&D programs, regional production expansion, and ecosystem partnerships focused on automation software, industrial IoT compatibility, and modular hydraulic architecture optimization.

Advanced cartridge valve deployment faces execution challenges linked to integration complexity, skilled labor shortages, and rising performance expectations across automated industrial systems. Nearly 29% of industrial operators report difficulties integrating digitally controlled hydraulic components with legacy infrastructure, while maintenance skill gaps increased implementation delays by approximately 17% during 2025. Global energy-efficiency regulations and pressure-control compliance requirements are also forcing costly redesign cycles for hydraulic equipment manufacturers. These constraints threaten long-term scalability and operational consistency, particularly in high-cycle mining, marine, and construction applications where reliability thresholds continue tightening. To remain competitive, companies must accelerate workforce training, expand collaborative engineering partnerships, and invest in modular smart-valve platforms capable of delivering higher durability, real-time diagnostics, and simplified integration across increasingly automated industrial environments.

24% Rise in Smart Valve Integration Across Automated Facilities is reshaping industrial hydraulic operations as manufacturers deploy sensor-enabled cartridge valves with predictive monitoring capabilities. Automated diagnostics reduced maintenance downtime by 18% while improving pressure stability by 14% in high-cycle operations. Companies are accelerating partnerships with industrial automation providers to integrate real-time hydraulic analytics into production environments.

19% Shift Toward Compact High-Pressure Valve Designs is redefining equipment engineering across construction machinery and mobile hydraulics. Manufacturers reduced hydraulic system footprint by nearly 16% while improving operational responsiveness by 13% through compact cartridge valve architectures. Rising freight costs and supply chain disruptions are forcing OEMs to optimize machine weight, component density, and localized assembly strategies simultaneously.

27% Increase in Regionalized Manufacturing Expansion is transforming procurement and production structures across North America and Europe. Industrial buyers are prioritizing localized hydraulic sourcing to reduce delivery volatility and improve compliance responsiveness. Lead times declined by 21% in regionalized supply networks, prompting valve manufacturers to restructure production footprints, expand machining capacity, and secure multi-region component partnerships.

31% Growth in Electro-Hydraulic Proportional Valve Deployment is accelerating the replacement of legacy mechanical control systems in precision industrial applications. Advanced proportional platforms improved energy efficiency by 17% and reduced fluid leakage losses by 12% in automated material handling operations. Companies are rapidly scaling digitally controlled product portfolios as labor shortages and stricter efficiency regulations force higher automation intensity across industrial infrastructure.

The industrial cartridge valves market is segmented by type, application, and end-user, with demand increasingly concentrating around automation-driven hydraulic performance. Directional and pressure control valves collectively account for over 48% of deployment due to broad integration across industrial machinery and mobile equipment platforms. Hydraulic systems and industrial automation remain the largest application areas as manufacturers prioritize compact high-pressure fluid control and predictive maintenance compatibility. Manufacturing and construction sectors contribute more than 44% of end-user demand, supported by automation upgrades and infrastructure expansion. Demand is shifting toward proportional valve technologies, intelligent fluid power systems, and high-efficiency mobile hydraulics, forcing suppliers to accelerate modular product development, regional production expansion, and digitally integrated valve platform strategies.

Directional control valves dominate the industrial cartridge valves market with approximately 32% share, supported by their critical role in controlling hydraulic flow paths across industrial automation, construction machinery, and mobile hydraulic systems. Their structural dominance comes from lower integration complexity, broad scalability, and strong compatibility with compact hydraulic architectures. Pressure control valves maintain strong penetration in high-load industrial applications where stable system protection and pressure regulation remain essential for operational safety and equipment reliability. However, proportional valves are emerging as the fastest-growing category, recording nearly 18% adoption expansion due to rising deployment in smart hydraulic systems and precision-controlled automation environments. Compared with traditional directional systems, proportional valves improve hydraulic response precision by almost 20% while reducing energy waste across automated production lines. Flow control, check, and auxiliary valve categories collectively represent around 29% of market demand, serving specialized applications requiring controlled fluid velocity, backflow prevention, and system stability. Manufacturers are increasingly shifting investments toward digitally controlled proportional technologies, modular cartridge platforms, and compact high-pressure designs to capture higher-margin automation projects and long-cycle industrial infrastructure contracts.

“According to a 2025 report by the International Fluid Power Association, proportional cartridge valve technology was adopted by over 41% of advanced industrial automation facilities, resulting in nearly 17% improvement in hydraulic efficiency and reduced maintenance intervention frequency, reinforcing its growing strategic importance.”

Hydraulic systems remain the leading application segment, accounting for nearly 35% of industrial cartridge valve deployment due to extensive usage across heavy machinery, industrial processing equipment, and mobile hydraulic platforms. Demand concentration exists because cartridge valves directly influence pressure control, flow precision, and operational reliability in high-cycle hydraulic environments. Industrial automation is the fastest-growing application area, expanding by approximately 21% as factories accelerate adoption of electro-hydraulic control systems, predictive maintenance integration, and intelligent fluid management technologies. Compared with mature hydraulic system applications, industrial automation deployments prioritize digitally controlled proportional valves capable of improving operational efficiency and reducing downtime simultaneously. Mobile equipment and construction machinery collectively contribute around 28% of market demand, supported by infrastructure expansion, compact equipment development, and stricter fuel-efficiency targets. Fluid power control and material handling equipment applications are also gaining momentum as manufacturers optimize warehouse automation and precision load-handling operations. Companies are responding through targeted automation partnerships, expanded high-pressure valve production, and development of compact modular hydraulic platforms designed for flexible industrial deployment and faster integration cycles.

“According to a 2025 report by the International Society of Automation, industrial automation hydraulic systems were deployed across over 52,000 manufacturing facilities globally, improving equipment operating efficiency by 18%, highlighting their rapid operational adoption.”

Manufacturing dominates the industrial cartridge valves market with nearly 29% share due to intensive hydraulic system usage across automated production lines, industrial robotics, and heavy processing equipment. High operational dependency on fluid control precision, pressure stability, and machine uptime continues driving concentrated demand from manufacturing facilities undergoing automation upgrades. Mining is emerging as the fastest-growing end-user segment, expanding by approximately 16% as operators invest in high-durability hydraulic systems for autonomous drilling, material transport, and high-pressure excavation equipment. Compared with traditional manufacturing demand focused on efficiency optimization, mining prioritizes ruggedized valve systems capable of sustaining harsh operating conditions and minimizing unplanned shutdowns. Oil and gas, agriculture, construction, and marine industry applications collectively account for around 54% of market demand, with increasing emphasis on corrosion-resistant designs, compact hydraulic integration, and predictive maintenance compatibility. Companies are strategically targeting these sectors through customized valve configurations, long-term OEM supply agreements, regional service expansion, and application-specific hydraulic engineering support designed to strengthen customer retention and operational reliability.

“According to a 2025 report by the Global Fluid Power Council, adoption among mining operators increased by 22%, with over 8,500 industrial sites implementing advanced cartridge valve systems, leading to nearly 15% improvement in equipment uptime and hydraulic efficiency, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific dominates industrial cartridge valve demand due to large-scale hydraulic equipment manufacturing, infrastructure expansion, and rapid industrial automation adoption across China, Japan, and India. Europe contributes nearly 28% of global demand and leads in precision-engineered proportional valve integration, particularly within advanced manufacturing and energy-efficient industrial systems. North America represents approximately 24% share, driven by reshoring initiatives, smart factory deployment, and localized hydraulic supply-chain investments. Meanwhile, Middle East & Africa demand is accelerating through oil infrastructure modernization and industrial construction expansion. Regulatory pressure on industrial fluid efficiency and ongoing supply-chain regionalization are reshaping procurement priorities globally. Companies are increasingly focusing investments on Asia-Pacific production scale, North American localization strategies, and European smart hydraulic innovation capabilities to secure long-term competitive positioning.

North America accounts for nearly 24% of global industrial cartridge valve demand, supported by strong adoption across industrial automation, construction machinery, and advanced manufacturing operations. Hydraulic system modernization and smart factory expansion are accelerating deployment of digitally controlled proportional valves, with automated hydraulic integration rising 22% since 2024. Reshoring strategies and industrial supply-chain localization are structurally reshaping procurement decisions, forcing OEMs to prioritize domestic sourcing reliability and shorter delivery cycles. Manufacturers expanded regional machining and assembly capacity by approximately 18% to reduce import dependency and improve operational responsiveness. Industrial buyers increasingly favor predictive maintenance-compatible valve systems that lower downtime and maintenance intensity. Companies continue prioritizing North America because localized production, automation expansion, and infrastructure modernization are creating higher-value long-cycle industrial contracts.

Europe contributes approximately 28% of industrial cartridge valve demand, led by Germany, Italy, and France through advanced manufacturing, industrial robotics, and precision hydraulic engineering. Stricter industrial efficiency standards and fluid leakage regulations are forcing rapid adoption of energy-efficient proportional cartridge valves across automated production systems. Digitally optimized hydraulic platforms improved operational efficiency by nearly 16% while reducing fluid losses by 12% in newly upgraded industrial facilities. Companies are restructuring product portfolios around low-emission hydraulic architectures and corrosion-resistant valve technologies to meet tightening sustainability requirements. Enterprise buyers prioritize reliability, compliance performance, and long-term maintenance reduction over low-cost sourcing strategies. Europe remains strategically critical because regulatory intensity is redefining product standards, forcing global manufacturers to accelerate hydraulic innovation and advanced industrial compliance capabilities.

Asia-Pacific leads the industrial cartridge valves market with nearly 41% global demand share, supported by massive hydraulic equipment production capacity across China, Japan, South Korea, and India. Construction machinery expansion, industrial automation growth, and mining equipment manufacturing continue accelerating regional cartridge valve consumption. Smart manufacturing deployment increased approximately 26% between 2024 and 2026, while localized hydraulic component production improved supply responsiveness by 21%. Major manufacturers are expanding machining facilities and automated assembly operations to strengthen export competitiveness and reduce production bottlenecks. Industrial buyers across the region prioritize cost efficiency, production scale, and rapid equipment delivery over premium customization models. Asia-Pacific remains indispensable for global expansion strategies because it combines manufacturing scale, infrastructure intensity, and fast-moving industrial automation demand within a highly competitive production ecosystem.

South America represents nearly 7% of global industrial cartridge valve demand, with Brazil and Argentina leading regional consumption through mining, agriculture, and construction equipment applications. Infrastructure modernization and agricultural mechanization are increasing demand for compact hydraulic systems, particularly in mobile equipment and material handling operations. However, import dependency and currency volatility continue constraining procurement stability, increasing hydraulic equipment acquisition costs by nearly 14% during recent industrial expansion cycles. Manufacturers are responding through localized distribution partnerships and region-specific product customization focused on durability and maintenance simplicity. Industrial buyers remain highly price-sensitive and increasingly prioritize operational reliability over advanced digital integration. South America presents strong long-term industrial expansion potential, but companies must balance growth opportunities against infrastructure limitations, procurement volatility, and uneven industrial investment patterns.

Middle East & Africa accounts for approximately 9% of industrial cartridge valve demand, driven primarily by oil and gas infrastructure, mining operations, and large-scale construction projects across Saudi Arabia, the UAE, and South Africa. Industrial modernization programs and energy infrastructure investments are accelerating deployment of high-pressure hydraulic systems integrated with advanced cartridge valve technologies. Automated hydraulic adoption in large industrial projects increased nearly 17% between 2024 and 2026, while regional infrastructure investments expanded industrial equipment procurement activity by approximately 15%. Companies are strengthening regional partnerships, expanding service capabilities, and increasing localized technical support to capture long-cycle infrastructure contracts. Enterprise buyers prioritize equipment durability, operational continuity, and rapid maintenance access. The region is emerging as a strategic expansion zone where infrastructure spending and industrial diversification continue reshaping hydraulic equipment demand patterns.

China Industrial Cartridge Valves Market – 34% Share: China dominates through large-scale hydraulic equipment manufacturing capacity, rapid industrial automation deployment, and strong infrastructure-driven demand across construction and mining sectors.

Germany Industrial Cartridge Valves Market – 16% Share: Germany leads in precision-engineered industrial cartridge valves due to advanced manufacturing integration, high adoption of proportional hydraulic systems, and strict industrial efficiency standards.

The industrial cartridge valves market is defined by competition between global hydraulic technology leaders such as Bosch Rexroth, Parker Hannifin, Eaton, Danfoss, and HydraForce, against regional cost-focused manufacturers and specialized precision-valve innovators. The top five players collectively control nearly 46% of market activity through broad OEM relationships, integrated hydraulic portfolios, and advanced automation capabilities. Competition is intensifying around digitally controlled proportional valves, compact high-pressure systems, and predictive maintenance integration, with smart hydraulic platforms improving operational efficiency by nearly 18% compared with conventional systems. Regional suppliers compete aggressively on delivery speed and pricing, while global leaders focus on customization, vertical integration, and engineering support. Manufacturers are expanding localized machining capacity, forming industrial automation partnerships, and accelerating modular valve innovation to strengthen supply resilience. Rising compliance standards and precision manufacturing requirements create high entry barriers, forcing competitors to differentiate through automation expertise, application-specific engineering, and long-term industrial reliability performance.

Bosch Rexroth AG

Parker Hannifin Corporation

Eaton Corporation

Danfoss Power Solutions

HydraForce Inc.

Sun Hydraulics Corporation

Moog Inc.

Bucher Hydraulics

HYDAC International GmbH

Kawasaki Heavy Industries Ltd.

Yuken Kogyo Co., Ltd.

Emerson Electric Co.

IMI plc

Atos S.p.A.

Industrial cartridge valve technology is rapidly shifting toward digitally controlled proportional systems integrated with industrial automation platforms and predictive diagnostics. Smart electro-hydraulic valves improved pressure accuracy by nearly 21% while reducing maintenance intervention by 17% across automated manufacturing environments in 2025–2026. Over 38% of newly deployed industrial hydraulic systems now integrate sensor-enabled cartridge valves connected through EtherCAT, CANopen, and Profinet protocols. Manufacturers are prioritizing compact modular architectures that reduce hydraulic footprint by approximately 15%, enabling faster machine assembly and lower operational complexity in material handling, construction machinery, and robotics applications.

Emerging technologies are redefining hydraulic responsiveness and energy optimization through AI-assisted tuning software, low-power solenoid architectures, and digitally configurable valve platforms. Advanced proportional cartridge valves improve operational efficiency by 19% while reducing energy loss by 14% compared with legacy mechanical hydraulic systems. Adoption of closed-loop hydraulic monitoring systems exceeded 29% across precision industrial automation facilities during 2026. Companies deploying intelligent hydraulic platforms benefit from reduced downtime, faster commissioning, and stronger lifecycle cost control, creating competitive advantages in high-cycle industrial environments where operational continuity directly impacts production efficiency.

Disruptive innovation between 2026 and 2028 is accelerating around integrated diagnostics, high-flow compact cartridge systems, and software-defined hydraulic control ecosystems. New-generation digital amplifiers and embedded diagnostics reduced troubleshooting time by nearly 22% while improving system tuning speed by 18%. Global hydraulic technology leaders are expanding investments in configurable valve software, modular hydraulic integrated circuits, and intelligent motion-control platforms to capture automation-driven industrial demand. Companies acting now gain faster integration capability, stronger OEM positioning, and higher resilience against tightening industrial efficiency standards and growing automation intensity.

October 2025 – Danfoss Power Solutions launched the next-generation AxisPro proportional valve platform with digital amplifiers and multi-network protocol support, improving tuning precision and hydraulic stability across industrial automation systems. The platform achieved pressure gain performance of 2.05% and improved commissioning speed through real-time software configuration capabilities. This strengthened Danfoss’ position in intelligent hydraulic automation markets. [Digital Motion Upgrade] Source: Danfoss

August 2025 – Danfoss Power Solutions introduced the SLP13-10 cartridge valve featuring patented low-power architecture for electrified hydraulic systems. The valve reduced electrical power consumption by 65% compared with conventional valve platforms while improving battery runtime and operational efficiency in mobile hydraulic equipment. The launch accelerated competitive positioning in energy-efficient hydraulic integration. [Low-Power Hydraulics] Source: Danfoss Power Solutions News

April 2026 – Bosch Rexroth AG expanded its LC-8X 2-way cartridge valve portfolio with new nominal sizes 80, 100, and 125 to support higher-flow industrial applications. The compact logic valve architecture improved energy and operational efficiency across demanding hydraulic systems while expanding deployment flexibility for industrial infrastructure projects and automated processing environments. [High-Flow Expansion] Source: Bosch Rexroth

February 2024 – Danfoss Power Solutions integrated multiple legacy cartridge valve and hydraulic integrated circuit portfolios into a unified industrial platform producing over 5 million valves annually. The restructuring simplified product integration, accelerated custom hydraulic circuit design workflows, and improved global delivery responsiveness for OEMs seeking scalable fluid-power solutions. [Portfolio Integration Shift]

This report delivers comprehensive coverage of the industrial cartridge valves market across product types, applications, end-user industries, regional demand structures, and evolving hydraulic control technologies. The analysis evaluates directional control, pressure control, flow control, check, and proportional valve segments while assessing deployment trends across hydraulic systems, industrial automation, construction machinery, mobile equipment, and material handling operations. End-user analysis spans manufacturing, mining, oil and gas, agriculture, construction, and marine industries across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report also examines emerging technologies including smart proportional valves, electro-hydraulic integration, predictive maintenance platforms, and digitally configurable hydraulic systems.

The study analyzes more than 25 strategic demand indicators, including adoption penetration, localization intensity, operational efficiency shifts, and automation deployment patterns. Approximately 41% of market demand is concentrated in Asia-Pacific manufacturing ecosystems, while digitally controlled proportional valve integration surpassed 30% across advanced automation facilities during 2026. Over 14 major industrial hydraulic companies are profiled with detailed assessment of production expansion, intelligent hydraulic integration, and supply-chain restructuring strategies.

The report supports investment planning, regional expansion decisions, supplier benchmarking, and competitive positioning by identifying high-growth industrial applications, emerging hydraulic technologies, operational transition risks, and evolving procurement priorities shaping industrial fluid-power systems between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1894 Million |

|

Market Revenue in 2033 |

USD 2714.14 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Danfoss Power Solutions, HydraForce Inc., Sun Hydraulics Corporation, Moog Inc., Bucher Hydraulics, HYDAC International GmbH, Kawasaki Heavy Industries Ltd., Yuken Kogyo Co., Ltd., Emerson Electric Co., IMI plc, Atos S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |