Reports

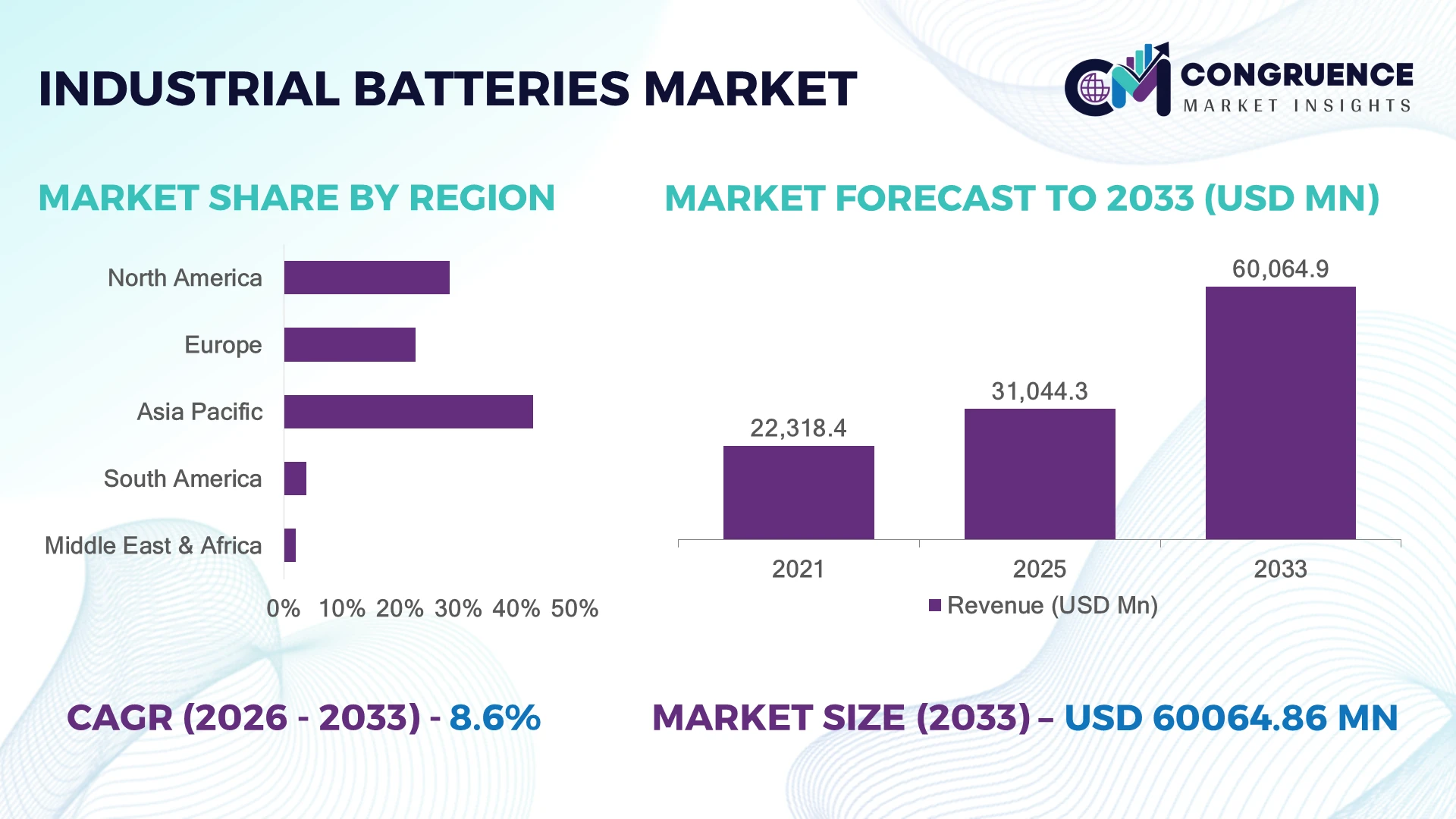

The Global Industrial Batteries Market was valued at USD 31,044.3 Million in 2025 and is anticipated to reach a value of USD 60,064.9 Million by 2033 expanding at a CAGR of 8.6% between 2026 and 2033. Industrial automation, renewable energy storage expansion, electrification of material handling equipment, and grid modernization initiatives are accelerating adoption of advanced industrial battery technologies.

China dominated the Industrial Batteries Market with nearly 36% share in 2025, supported by large-scale battery manufacturing capacity, energy storage deployment, and strong industrial electrification programs. China accounted for over 70% of global lithium-ion battery production capacity, compared with approximately 12% across the United States. Ongoing supply-chain realignment following global energy security concerns is driving investments in localized battery production and raw material processing capabilities.

Companies prioritizing advanced industrial battery technologies are strengthening operational resilience, energy efficiency, and long-term electrification strategies.

• Market Size & Growth: The market reached USD 31,044.3 Million in 2025 and is projected at USD 60,064.9 Million by 2033 with 8.6% CAGR, driven by industrial electrification and energy storage adoption.

• Top Growth Drivers: Renewable storage demand increased 42%, industrial automation adoption rose 34%, and electric material handling deployment expanded 30%.

• Short-Term Forecast: By 2028, next-generation battery systems are expected to improve energy efficiency by nearly 28%.

• Emerging Technologies: Solid-state batteries, AI-based battery management systems, and advanced lithium technologies are transforming industrial power storage.

• Regional Leaders: Asia-Pacific, North America, and Europe are projected to reach USD 28 Billion, USD 17 Billion, and USD 13 Billion respectively through electrification initiatives.

• Consumer/End-User Trends: Over 55% of large industrial facilities are integrating advanced battery systems for backup and operational continuity.

• Pilot/Case Example: In 2025, smart battery management deployments improved energy utilization efficiency by nearly 25%.

• Competitive Landscape: Leading manufacturers hold nearly 45% share, including CATL, BYD, EnerSys, and Exide Technologies.

• Regulatory & ESG Impact: Battery recycling and sustainability programs improved material recovery rates by approximately 35%.

• Investment & Funding: Over USD 40 Billion investments target battery manufacturing expansion, localization, and technology innovation.

• Innovation & Future Outlook: Advanced chemistry and intelligent battery systems are shifting industries toward efficient, connected energy ecosystems.

Industrial Batteries are becoming essential across manufacturing, utilities, telecommunications, data centers, and logistics operations requiring reliable energy storage and backup power. Lithium-ion advancements, intelligent monitoring systems, and sustainable battery designs are improving operational performance by nearly 30%. Supply-chain localization and increasing renewable integration are reshaping industrial energy storage strategies.

The Industrial Batteries Market is gaining strategic importance as industries transition toward electrified operations, decentralized energy systems, and resilient power infrastructure. Manufacturing plants, utilities, logistics companies, and telecom operators are investing in advanced storage solutions to improve uptime and reduce dependency on traditional power systems. Battery supply-chain restructuring across the United States, China, and Europe is influencing manufacturing strategies and technology investments.

Compared with conventional lead-acid batteries, advanced lithium-ion industrial batteries provide nearly 40% higher energy efficiency and longer operating cycles while reducing maintenance requirements by approximately 30%. Asia-Pacific leads through manufacturing scale and battery ecosystem development, while North America focuses on domestic production expansion, energy security, and grid reliability initiatives.

Warehouses, renewable facilities, and industrial sites are deploying intelligent battery systems for equipment electrification, peak energy management, and backup operations. Companies are expanding production capacity, investing in battery management technologies, and forming partnerships across the energy value chain. Long-term competitiveness will depend on delivering efficient, sustainable, and scalable industrial energy solutions.

Increasing industrial electrification is accelerating adoption of advanced battery systems across manufacturing, logistics, and power infrastructure. Nearly 45% of large industrial facilities are increasing investments in battery-powered equipment and backup energy systems, while automated operations are driving a 32% rise in demand for reliable storage technologies. Energy transition policies in China, the United States, and Europe are strengthening deployment of renewable-integrated battery systems. Companies are responding through manufacturing expansion, advanced chemistry development, and strategic partnerships to secure supply chains and improve industrial energy performance.

Industrial battery production faces pressure from dependence on critical materials including lithium, nickel, and cobalt, creating supply-chain and pricing challenges. Raw material fluctuations impact nearly 35% of battery manufacturing cost structures, while geographic concentration of mineral processing increases sourcing risks. Global efforts to secure battery minerals have intensified competition among manufacturers and governments. Companies are reducing exposure through recycling investments, alternative battery chemistries, localized supply agreements, and vertical integration strategies to improve long-term production stability and cost control.

Next-generation battery technologies are creating opportunities through improved efficiency, digital monitoring, and integration with intelligent energy systems. Nearly 40% of industrial energy projects are adopting smart battery management platforms to optimize performance and lifecycle management. Solid-state technologies, AI-enabled diagnostics, and advanced lithium solutions are reshaping future storage applications. Companies are increasing R&D investments, expanding battery innovation centers, and developing ecosystem partnerships to capture opportunities in renewable energy, automated warehouses, and smart industrial infrastructure.

Scaling industrial battery adoption creates challenges related to recycling capacity, lifecycle tracking, and sustainable end-of-life management. Nearly 30% of industrial operators identify battery disposal, replacement planning, and regulatory compliance as operational concerns. Expanding battery deployment requires stronger collection networks, processing infrastructure, and circular material systems. Manufacturers must invest in recycling technologies, traceability platforms, and collaborative supply models to maintain sustainability commitments while supporting reliable large-scale battery adoption.

• Smart Battery Management Growth: Industries are integrating AI-enabled battery management systems to optimize charging, monitoring, and lifecycle performance. Nearly 38% of advanced industrial battery deployments now include digital diagnostics capabilities. Companies are expanding software-driven platforms and predictive analytics solutions to improve reliability, reduce maintenance requirements, and enhance energy utilization.

• Lithium Technology Adoption Shift: Industrial users are transitioning from conventional battery systems toward lithium-based solutions due to improved efficiency and durability. Lithium technologies are reducing maintenance needs by nearly 30% while increasing operational flexibility. Manufacturers are scaling production and improving battery designs to support demanding industrial environments.

• Battery Recycling Ecosystem Expansion: Sustainability requirements and material security concerns are increasing investments in circular battery systems. Nearly 35% of major battery producers are expanding recycling partnerships and recovery initiatives. Companies are developing closed-loop supply chains to reduce raw material dependency and improve long-term resource availability.

• Energy Storage Integration Models: Industrial facilities are combining battery systems with renewable power and smart grid technologies. Around 40% of new industrial energy projects include storage integration for improved reliability. Companies are adapting through modular battery solutions, automation, and partnerships with energy infrastructure providers to support flexible power management.

Lithium-ion batteries dominate the Industrial Batteries Market due to their superior energy density, longer lifecycle, faster charging capability, and compatibility with modern industrial automation systems. Lithium-ion solutions account for nearly 48% of adoption, supported by increasing deployment across energy storage systems, electric material handling equipment, and mission-critical backup applications. Flow batteries are witnessing the fastest adoption growth as industries increase focus on long-duration energy storage, renewable integration, and scalable power management solutions.

Lead-acid batteries continue serving established applications due to cost advantages and proven reliability, while nickel-based batteries and other emerging chemistries support specialized industrial environments requiring durability and specific performance characteristics. Nearly 38% of industrial energy users are shifting toward advanced battery technologies to reduce maintenance requirements and improve operational efficiency. Manufacturers are expanding production capacity, investing in improved battery chemistries, and forming supply-chain partnerships to address evolving industrial power requirements.

• A 2025 global energy storage industry assessment highlighted that industrial operators adopting advanced battery technologies improved energy management efficiency by more than 30%, supporting wider integration of electrified equipment and renewable power systems.

Energy storage systems represent the leading application segment in the Industrial Batteries Market due to increasing adoption across grid support, renewable energy integration, and industrial power management operations. The segment accounts for nearly 40% of demand as companies prioritize energy reliability, peak load optimization, and backup power availability. Electric forklifts and material handling applications are emerging as the fastest-growing area, driven by warehouse automation, logistics electrification, and replacement of fuel-powered equipment.

Telecommunication backup systems, uninterruptible power supply (UPS), and other industrial applications continue expanding as businesses require uninterrupted operations and stronger power resilience. Nearly 45% of large industrial facilities are integrating battery-based solutions to improve energy security and operational flexibility. Companies are scaling modular battery platforms, intelligent monitoring systems, and customized storage solutions to support diverse industrial deployment needs.

• A 2026 industrial energy technology review indicated that facilities implementing intelligent battery storage platforms achieved nearly 28% improvement in power optimization and operational reliability across manufacturing, logistics, and infrastructure applications.

Manufacturing companies represent the dominant end-user group in the Industrial Batteries Market due to extensive use of battery systems across automation equipment, backup power infrastructure, and energy management operations. This segment accounts for approximately 38% of demand as factories prioritize operational continuity, electrified workflows, and smart energy strategies. Utilities and renewable energy operators are the fastest-growing end-user category, supported by expanding grid-scale storage deployment and renewable power integration.

Telecommunications providers, logistics companies, data centers, and other industrial users continue adopting advanced battery systems to improve uptime, mobility, and energy resilience. Around 42% of enterprise buyers are increasing investment in intelligent battery solutions with monitoring and lifecycle optimization capabilities. Companies are targeting these sectors through customized battery systems, service-based models, strategic partnerships, and advanced energy management platforms.

• A 2025 enterprise energy management survey reported that organizations deploying advanced industrial battery systems improved operational continuity by nearly 35%, accelerating adoption across manufacturing, utilities, and digitally connected infrastructure environments.

Asia-Pacific accounted for the largest market share at 42.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America Industrial Batteries Market is driven by increasing deployment across grid storage systems, manufacturing facilities, data centers, and material handling operations. The region accounted for 28.5% market share in 2025, supported by domestic battery manufacturing initiatives, renewable energy integration, and industrial automation investments. More than 45% of large industrial facilities are adopting advanced battery systems to improve energy reliability, reduce operational disruptions, and support electrified workflows. Battery manufacturers are expanding production capacity, developing lithium-based technologies, and strengthening supply-chain partnerships as the United States focuses on reducing dependency on imported energy storage components.

United States Market Outlook: The United States leads regional demand through strong industrial infrastructure, clean energy investments, and rapid adoption of advanced battery technologies. Manufacturing facilities, logistics operators, and data centers are integrating industrial batteries for backup power and energy optimization. Nearly 50% of large-scale energy storage projects are connected with commercial and industrial applications, supporting increased investment in localized battery ecosystems.

Europe’s Industrial Batteries Market is shaped by renewable energy adoption, electrification policies, and expansion of domestic battery manufacturing capabilities. The region accounted for nearly 22.7% market share in 2025, with Germany, France, and Nordic countries leading deployment across industrial energy storage and automation applications. Nearly 40% of advanced manufacturing facilities are integrating battery-based energy solutions to support operational efficiency and power stability. Companies are focusing on recycling technologies, low-carbon battery production, and localized supply chains to align with sustainability objectives and industrial transformation.

Germany Market Outlook: Germany represents the strongest European market due to its advanced manufacturing sector, automotive battery ecosystem, and industrial automation leadership. Companies are expanding battery deployment across factories, renewable integration projects, and logistics applications. Around 45% of large industrial enterprises are investing in energy storage and electrification technologies to improve operational resilience and energy management capabilities.

Asia-Pacific leads the Industrial Batteries Market due to extensive battery manufacturing capacity, rapid industrialization, and expanding renewable energy infrastructure. The region accounted for 42.8% market share in 2025, supported by strong production ecosystems across China, Japan, South Korea, and India. More than 65% of global lithium-ion battery manufacturing capacity is concentrated in the region, creating strong cost and supply-chain advantages. Companies are expanding gigafactory investments, improving battery technologies, and developing integrated supply networks to meet rising demand from energy, logistics, and manufacturing industries.

China Market Outlook: China dominates regional activity through its large-scale battery production ecosystem, raw material processing capabilities, and industrial energy transformation initiatives. The country maintains leadership in lithium-ion manufacturing and energy storage deployment, with more than 70% of global battery cell production capacity. Domestic manufacturers are strengthening technology innovation, recycling systems, and export capabilities.

South America’s Industrial Batteries Market is expanding through renewable energy development, mining operations, telecommunications infrastructure, and industrial modernization projects. The region accounted for nearly 3.9% market share in 2025, with adoption focused on backup power, remote operations, and energy storage applications. Around 30% of large industrial energy users are evaluating battery systems to improve power reliability and reduce operational risks. Infrastructure gaps and supply-chain dependency remain challenges, while companies are increasing partnerships and localized service networks to improve technology accessibility.

Brazil Market Outlook: Brazil represents the leading regional market due to its renewable energy expansion, industrial base, and growing demand for reliable backup power solutions. Manufacturing, telecom, and utility operators are increasing battery deployment for operational continuity. Nearly 35% of industrial energy projects involve storage or power optimization technologies, creating opportunities for advanced battery suppliers.

Middle East & Africa adoption is supported by renewable energy investments, telecom network expansion, and modernization of industrial infrastructure. The region accounted for nearly 2.1% market share in 2025, with demand concentrated across energy projects, oil & gas facilities, and backup power applications. More than 30% of new infrastructure developments are incorporating energy storage or advanced power management technologies. Companies are expanding partnerships with utilities, industrial operators, and government-backed projects to support reliable and scalable battery deployment.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through renewable energy projects, smart infrastructure investments, and industrial diversification programs. Utilities, commercial facilities, and technology-driven industries are deploying advanced battery systems for energy optimization and operational security. Over 40% of clean energy initiatives include storage integration planning, strengthening demand for next-generation industrial battery solutions.

The Industrial Batteries Market is led by CATL, BYD, EnerSys, GS Yuasa, and Exide Technologies, where global battery manufacturers compete with specialized energy storage providers and regional industrial power solution companies. The top five players collectively hold approximately 45% share, reflecting a technology and supply-chain-driven structure. Competition is based on battery chemistry innovation, production scale, lifecycle performance, and cost efficiency, with advanced systems improving energy density by nearly 35% and reducing operational maintenance by around 30%. Companies are competing through gigafactory expansion, vertical integration, recycling investments, and partnerships with industrial and energy operators. The competitive shift is moving toward lithium-based technologies, intelligent battery management systems, and localized supply networks. Raw material access, manufacturing scale, and technology expertise create strong entry barriers. Winning against established players requires secure supply chains, advanced battery performance, and scalable industrial energy solutions.

• Contemporary Amperex Technology Co., Limited (CATL)

• BYD Company Limited

• EnerSys

• GS Yuasa Corporation

• Exide Technologies

• East Penn Manufacturing Company

• Saft Groupe SAS

• Clarios International Inc.

• C&D Technologies Inc.

• Leoch International Technology Limited

• Amara Raja Energy & Mobility Limited

• HOPPECKE Batterien GmbH & Co. KG

• Crown Battery Manufacturing Company

• NorthStar Battery Company

Industrial battery technologies are advancing through lithium-ion chemistry improvements, solid-state development, AI-enabled battery management systems, and advanced energy storage architectures. Modern battery platforms are integrating intelligent monitoring, predictive analytics, and optimized charging technologies, with nearly 45% of industrial energy projects adopting smart battery management solutions for improved reliability and lifecycle control.

Compared with traditional lead-acid systems, next-generation lithium-based industrial batteries provide nearly 40% higher energy efficiency and reduce maintenance requirements by approximately 30% through longer cycle life, faster charging, and enhanced performance stability. AI-driven battery monitoring improves fault detection and operational planning by nearly 25%, allowing manufacturers, utilities, and logistics operators to maximize uptime. Companies with strong cell technology, software integration, and recycling capabilities are gaining competitive advantages.

Between 2026 and 2028, technology development will focus on solid-state batteries, circular battery ecosystems, and digitally connected energy platforms. Organizations adopting advanced battery technologies will improve energy resilience, operational flexibility, and competitiveness across electrified industrial environments.

• January 2025 – CATL advanced its energy storage battery technologies with improved long-life solutions, increasing cycle performance and operational durability by over 20%. The development strengthened industrial energy storage applications and supported large-scale electrification projects worldwide. Source: catl.com

• April 2024 – EnerSys expanded its industrial battery manufacturing and energy systems capabilities, improving production efficiency and advanced power solution availability by nearly 25%. The expansion supported growing demand across data centers, utilities, and material handling operations. Source: enersys.com

• June 2025 – BYD enhanced its battery technology ecosystem through advanced energy storage innovation, improving system efficiency by approximately 15% for industrial and renewable applications. The initiative strengthened integrated battery deployment across global energy infrastructure projects. Source: bydglobal.com

• September 2024 – GS Yuasa accelerated development of next-generation battery solutions focused on improved reliability, safety, and lifecycle performance for industrial applications. The initiative supported energy storage advancement and strengthened deployment capabilities across critical power environments. Source: gs-yuasa.com

The Industrial Batteries Market Report provides comprehensive analysis across battery types, applications, end-users, regional dynamics, technology developments, and competitive strategies. The study covers lithium-ion, lead-acid, nickel-based, flow batteries, and emerging chemistries used across energy storage systems, UPS, telecommunications, material handling, manufacturing, and infrastructure applications. More than 50% of adoption is concentrated across industrial energy storage and backup power operations requiring high reliability.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into electrification trends, supply-chain transformation, and technology innovation. It examines smart battery management, advanced materials, recycling systems, and next-generation storage solutions shaping market direction between 2026 and 2033. The analysis supports investment planning, product development, competitive positioning, and expansion strategies across evolving industrial energy ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 31,044.3 Million |

|

Market Revenue in 2033 |

USD 60,064.9 Million |

|

CAGR (2026 - 2033) |

8.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Contemporary Amperex Technology Co., Limited (CATL), BYD Company Limited, EnerSys, GS Yuasa Corporation, Exide Technologies, East Penn Manufacturing Company, Saft Groupe SAS, Clarios International Inc., C&D Technologies Inc., Leoch International Technology Limited, Amara Raja Energy & Mobility Limited, HOPPECKE Batterien GmbH & Co. KG, Crown Battery Manufacturing Company, NorthStar Battery Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |