Reports

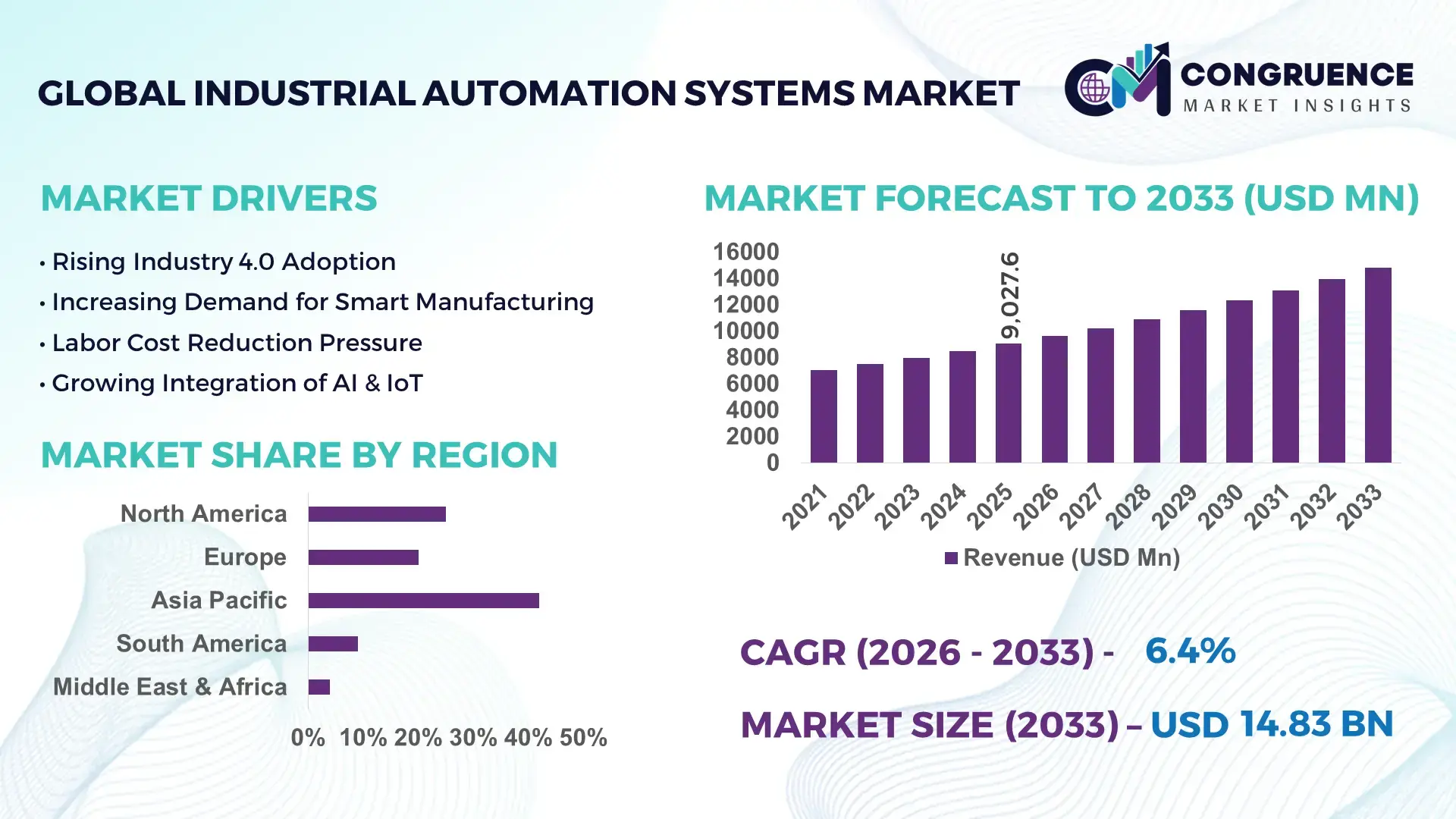

The Global Industrial Automation Systems Market was valued at USD 9027.55 Million in 2025 and is anticipated to reach a value of USD 14828.71 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033. This growth is primarily driven by increasing adoption of smart manufacturing and digital transformation across industrial sectors.

China continues to demonstrate strong industrial automation expansion supported by large-scale manufacturing capacity and consistent capital investments. The country operates over 35% of the world’s manufacturing facilities and has installed more than 290,000 industrial robots annually, reflecting accelerated automation adoption. Government-backed initiatives such as smart factory programs and industrial digitization policies have led to widespread deployment of programmable logic controllers (PLCs), distributed control systems (DCS), and robotics in automotive, electronics, and heavy machinery sectors. Additionally, over 60% of large-scale factories in China have integrated at least one form of advanced automation technology, strengthening production efficiency and operational scalability across industrial clusters.

Market Size & Growth: USD 9027.55 Million in 2025, projected to reach USD 14828.71 Million by 2033 at 6.4% CAGR, driven by rapid adoption of smart factory automation solutions.

Top Growth Drivers: Industrial robotics adoption at 42%, operational efficiency improvement at 35%, and predictive maintenance usage at 28%.

Short-Term Forecast: By 2028, automation integration is expected to reduce operational costs by 22% and improve production efficiency by 27%.

Emerging Technologies: AI-driven process automation, Industrial Internet of Things (IIoT), and digital twin technology are reshaping industrial workflows.

Regional Leaders: Asia-Pacific projected to exceed USD 6200 Million by 2033 with strong manufacturing digitization; North America to reach USD 4100 Million driven by smart factory upgrades; Europe to cross USD 3600 Million supported by Industry 4.0 adoption.

Consumer/End-User Trends: Automotive, electronics, and food processing sectors account for over 55% of automation deployment, emphasizing precision and throughput.

Pilot or Case Example: In 2024, a smart factory deployment reduced downtime by 31% and improved output efficiency by 26% through AI-enabled automation.

Competitive Landscape: Leading player holds approximately 18% share, followed by key players including Siemens, ABB, Schneider Electric, Rockwell Automation, and Mitsubishi Electric.

Regulatory & ESG Impact: Industrial emission reduction targets mandate up to 30% energy efficiency improvements through automation systems by 2030.

Investment & Funding Patterns: Over USD 5 billion invested in automation upgrades and IIoT infrastructure globally in recent years.

Innovation & Future Outlook: Integration of AI, cloud-based control systems, and autonomous robotics is shaping next-generation industrial ecosystems.

Industrial automation systems are extensively utilized across automotive, oil and gas, energy, pharmaceuticals, and food processing sectors, with automotive contributing nearly 30% of automation deployments due to high precision requirements. Recent advancements such as AI-enabled predictive analytics, collaborative robots, and edge computing have significantly enhanced system responsiveness and real-time decision-making capabilities. Environmental regulations promoting energy-efficient manufacturing have accelerated automation adoption, particularly in Europe and North America. Additionally, emerging markets in Asia-Pacific are witnessing increased consumption due to rapid industrialization and infrastructure expansion, while future trends indicate strong momentum toward fully autonomous production environments and integrated smart factories.

Industrial automation systems have become strategically critical for enterprises aiming to enhance productivity, reduce operational variability, and maintain global competitiveness. The integration of artificial intelligence and Industrial Internet of Things technologies is redefining manufacturing efficiency, with AI-driven automation delivering up to 35% improvement in production accuracy compared to traditional rule-based control systems. This shift is particularly evident in high-volume manufacturing sectors where precision and speed are essential for maintaining output consistency.

Asia-Pacific dominates in production volume due to extensive manufacturing infrastructure, while North America leads in adoption, with over 65% of enterprises integrating advanced automation technologies into their operations. The increasing reliance on digital twins and real-time monitoring platforms is enabling predictive maintenance, reducing equipment downtime by nearly 30% across industrial facilities. By 2028, AI-powered automation systems are expected to improve energy efficiency by 25% while reducing unplanned downtime by over 28%. In parallel, organizations are committing to sustainability targets, including a 30% reduction in carbon emissions and enhanced resource optimization through automated energy management systems by 2030.

In 2024, a leading manufacturing hub in Germany achieved a 32% reduction in production cycle time through the implementation of AI-based robotic automation and real-time analytics platforms. These developments highlight the increasing convergence of automation with data intelligence and sustainability initiatives. As industries continue to digitize operations, the Industrial Automation Systems Market is expected to serve as a foundational pillar supporting operational resilience, regulatory compliance, and long-term sustainable growth.

The growing demand for smart manufacturing is a primary driver accelerating the adoption of industrial automation systems. Over 70% of manufacturers globally are investing in digital transformation initiatives aimed at improving operational efficiency and reducing production errors. Automation technologies such as robotics and AI-based control systems have demonstrated the ability to increase production throughput by up to 30% while minimizing defect rates by nearly 25%. In sectors like automotive and electronics, automated assembly lines have reduced production cycle times by approximately 20%, enabling faster time-to-market. Additionally, the integration of Industrial Internet of Things solutions allows real-time monitoring and predictive maintenance, reducing equipment downtime by over 28%. These measurable improvements are prompting industries to adopt scalable and flexible automation systems to remain competitive in a rapidly evolving manufacturing landscape.

High initial capital investment remains a significant barrier to the widespread adoption of industrial automation systems, particularly for small and medium-sized enterprises. The deployment of advanced automation infrastructure, including robotics, sensors, control systems, and software platforms, can require substantial upfront expenditure. On average, setting up a fully automated production line can cost 25% to 40% more than conventional manufacturing systems. Additionally, integration complexities and the need for skilled personnel to operate and maintain these systems further increase operational costs. Many businesses also face challenges related to legacy system compatibility, which requires additional investment in system upgrades and customization. These financial constraints often delay automation adoption, especially in developing regions where access to capital and technical expertise may be limited.

The expansion of Industry 4.0 presents significant opportunities for the industrial automation systems market, particularly through the integration of digital technologies and intelligent systems. The adoption of smart factories, powered by IoT, AI, and machine learning, is expected to increase by over 45% in the next few years, creating strong demand for advanced automation solutions. Digital twin technology, which enables real-time simulation of production processes, is improving operational efficiency by up to 30% and reducing product development cycles by nearly 25%. Additionally, the growing focus on mass customization and flexible manufacturing systems is driving the need for adaptive automation platforms. Emerging economies are also investing heavily in industrial infrastructure, providing new growth avenues for automation vendors. These developments are creating a robust environment for innovation and expansion within the market.

Cybersecurity risks and increasing system complexity pose significant challenges to the industrial automation systems market. As automation systems become more interconnected through IoT and cloud-based platforms, they become vulnerable to cyber threats, with industrial cyberattacks increasing by over 50% in recent years. These threats can disrupt operations, compromise sensitive data, and lead to significant financial losses. Additionally, the complexity of integrating multiple automation technologies, including robotics, AI systems, and legacy infrastructure, can create operational inefficiencies if not managed properly. Organizations must invest in robust cybersecurity frameworks and skilled personnel to mitigate these risks, which adds to the overall cost and complexity of automation deployment. This challenge is particularly critical for industries with highly sensitive operations such as energy, defense, and pharmaceuticals.

• Accelerated Adoption of AI-Driven Automation Systems: Industrial automation is increasingly integrating artificial intelligence to enhance operational efficiency and predictive capabilities. Over 62% of large manufacturing facilities have deployed AI-enabled automation tools, resulting in a 28% reduction in unplanned downtime and a 24% improvement in production accuracy. Machine learning algorithms are being utilized for predictive maintenance, with failure detection accuracy exceeding 85% in complex industrial environments. Additionally, AI-based process optimization has enabled manufacturers to reduce waste by nearly 20%, particularly in high-volume industries such as automotive and electronics manufacturing.

• Expansion of Industrial Internet of Things (IIoT) Connectivity: The proliferation of IIoT devices is transforming automation ecosystems by enabling real-time data exchange across production units. More than 70% of industrial enterprises have integrated connected sensors and devices into their operations, improving monitoring efficiency by 35%. Smart sensors capable of transmitting data every 5–10 seconds are enhancing visibility into production workflows. This connectivity has contributed to a 30% increase in asset utilization rates and a 22% improvement in overall equipment effectiveness (OEE). The trend is particularly prominent in energy and process industries where continuous monitoring is critical.

• Growth in Collaborative Robotics (Cobots) Deployment: Collaborative robots are gaining traction due to their flexibility and ability to work alongside human operators. Approximately 45% of manufacturers have introduced cobots into their production lines, leading to a 26% increase in workforce productivity and a 19% reduction in workplace injuries. Cobots are especially prevalent in small and medium enterprises, where they offer cost-effective automation solutions. Their deployment in assembly, packaging, and quality inspection processes has improved cycle times by up to 18%, while reducing manual intervention significantly.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Automation Systems market. Around 55% of new industrial infrastructure projects have reported cost savings through prefabrication techniques. Automated fabrication systems are used to produce pre-engineered components with precision tolerances below 2%, significantly reducing material waste. In regions such as Europe and North America, over 48% of large-scale construction projects now incorporate modular automation technologies, leading to project completion timelines being shortened by approximately 30% and labor requirements reduced by nearly 25%.

The industrial automation systems market is segmented based on type, application, and end-user industries, each contributing uniquely to overall market development. By type, control systems such as distributed control systems and programmable logic controllers dominate due to their critical role in process optimization and operational control. Robotics and machine vision systems are also gaining traction as industries prioritize precision and efficiency. In terms of application, manufacturing automation accounts for a substantial share, supported by high demand for consistent output and quality assurance across production lines. Process industries, including oil and gas and chemicals, also contribute significantly due to the need for continuous monitoring and safety compliance. From an end-user perspective, sectors such as automotive, energy, and electronics lead adoption, collectively accounting for over 60% of automation deployments. Emerging industries, including pharmaceuticals and food processing, are rapidly increasing their adoption rates as they shift toward digitized and highly controlled production environments.

The industrial automation systems market by type includes distributed control systems (DCS), programmable logic controllers (PLC), supervisory control and data acquisition (SCADA), human-machine interface (HMI), robotics, and machine vision systems. Distributed control systems currently account for approximately 34% of total adoption, driven by their extensive use in process industries such as oil and gas, power generation, and chemicals where continuous monitoring and centralized control are essential. In comparison, programmable logic controllers hold around 26% share due to their flexibility and reliability in discrete manufacturing environments. Robotics, however, is the fastest-growing segment, expanding at an estimated rate of 9.2%, fueled by increasing demand for precision, speed, and reduced labor dependency in manufacturing processes.

SCADA systems and HMI solutions collectively contribute nearly 28% of the market, supporting real-time monitoring and operator interface functionalities. Machine vision systems, though smaller in share at around 12%, are gaining importance in quality inspection and defect detection applications.

By application, the industrial automation systems market is segmented into manufacturing, process industries, packaging, material handling, and quality control. Manufacturing applications dominate with approximately 41% share, as automation is critical for maintaining production consistency, reducing errors, and increasing throughput in industries such as automotive and electronics. Process industries account for around 29% of adoption, driven by the need for continuous operations, safety compliance, and efficient resource management.

Material handling is the fastest-growing application segment, expanding at an estimated rate of 8.7%, supported by increasing demand for warehouse automation and logistics optimization. Automated guided vehicles and robotic handling systems have improved operational efficiency by up to 30% in large distribution centers.

Packaging and quality control applications collectively contribute around 30% of the market, focusing on precision, speed, and compliance with product standards. Automated inspection systems have reduced defect rates by nearly 25% in high-volume production environments.

End-user segmentation of the industrial automation systems market includes automotive, energy and power, oil and gas, electronics, pharmaceuticals, and food and beverage industries. The automotive sector leads with approximately 32% share, driven by high adoption of robotics, assembly line automation, and precision manufacturing requirements. Electronics manufacturing follows with around 21% share, supported by the need for miniaturization and high-speed production.

The pharmaceuticals sector is the fastest-growing end-user segment, expanding at an estimated rate of 9.5%, as regulatory requirements and the need for precision in drug manufacturing drive automation adoption. Automated systems in pharmaceutical production have improved batch consistency by over 20% and reduced contamination risks significantly.

Energy and power, along with oil and gas industries, collectively account for approximately 27% of the market, utilizing automation for process optimization and safety management. The food and beverage sector contributes around 20%, focusing on hygiene, packaging efficiency, and quality control.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by over 60% of global manufacturing output being concentrated in countries such as China, Japan, and India, with more than 300,000 industrial robots deployed annually in the region. North America follows with approximately 26% share, driven by high enterprise automation adoption where over 65% of large-scale manufacturers have implemented smart factory solutions. Europe contributes around 22%, with strong regulatory-driven adoption and over 55% of industries integrating energy-efficient automation systems. South America and the Middle East & Africa collectively account for nearly 10%, with increasing investments in oil & gas, mining, and infrastructure sectors. Across regions, automation penetration in large enterprises exceeds 70%, while small and medium enterprises show a growing adoption rate of approximately 35%, reflecting expanding accessibility of automation technologies.

The North America Industrial Automation Systems Market holds approximately 26% share, supported by strong adoption across automotive, aerospace, healthcare, and electronics industries. Over 65% of manufacturing enterprises in the region have implemented industrial automation solutions to enhance productivity and reduce operational inefficiencies. Regulatory frameworks promoting energy efficiency and workplace safety have driven the integration of advanced control systems and robotics. The region is witnessing rapid adoption of AI-enabled automation and IIoT platforms, with more than 58% of facilities deploying predictive maintenance solutions. A leading local player, Rockwell Automation, has expanded its smart manufacturing capabilities by introducing AI-integrated control systems, improving operational efficiency by over 30% in select facilities. Consumer behavior reflects a high preference for advanced, scalable automation systems, particularly in sectors such as healthcare and finance, where digital transformation adoption exceeds 60%.

Europe accounts for nearly 22% of the industrial automation systems market, with key markets including Germany, the United Kingdom, and France driving demand. Germany alone contributes over 35% of the region’s industrial automation installations due to its strong manufacturing base. Regulatory bodies emphasizing carbon neutrality and energy efficiency have led to over 50% of industrial facilities adopting automation technologies to meet environmental targets. Industry 4.0 initiatives are accelerating the deployment of smart factories, with approximately 48% of enterprises integrating digital twins and AI-driven analytics into production systems. Siemens, a major regional player, has advanced its automation portfolio by deploying cloud-based industrial solutions, improving production efficiency by up to 25% in European manufacturing plants. Consumer behavior in this region reflects a strong preference for sustainable and compliant automation solutions, with regulatory pressure influencing over 60% of purchasing decisions.

The Asia-Pacific Industrial Automation Systems Market leads globally in terms of volume, accounting for approximately 42% of total installations. Key countries such as China, Japan, and India collectively contribute over 70% of regional demand, supported by rapid industrialization and infrastructure development. China alone installs more than 290,000 industrial robots annually, while Japan remains a global leader in robotics innovation. The region is witnessing significant growth in smart manufacturing, with over 55% of large enterprises adopting automation technologies. Mitsubishi Electric, a prominent regional player, has introduced advanced factory automation solutions that have improved production throughput by nearly 28% in electronics manufacturing. Consumer behavior in the region is driven by cost optimization and scalability, with small and medium enterprises increasingly adopting automation solutions, contributing to a 40% rise in adoption rates over recent years.

South America represents approximately 6% of the global industrial automation systems market, with Brazil and Argentina being key contributors. Brazil accounts for over 45% of regional demand due to its strong industrial and energy sectors. Automation adoption is increasing in mining, oil & gas, and food processing industries, where operational efficiency improvements of up to 25% have been recorded through automation integration. Government incentives aimed at industrial modernization and trade policies supporting manufacturing growth have led to a 20% increase in automation investments. A regional player in Brazil has implemented automated process control systems in energy facilities, improving output efficiency by 22%. Consumer behavior in this region is largely driven by the need for cost-effective solutions, with over 50% of enterprises prioritizing automation systems that reduce labor dependency and operational costs.

The Middle East & Africa region accounts for approximately 4% of the industrial automation systems market, with strong demand driven by oil & gas, construction, and utilities sectors. Countries such as the UAE and South Africa are leading adoption, with the UAE investing heavily in smart infrastructure projects where automation adoption has increased by over 30%. The oil & gas sector contributes nearly 40% of regional automation demand, focusing on process optimization and safety enhancements. Technological modernization initiatives have led to the deployment of advanced control systems and robotics in large-scale projects. A key regional development includes automation integration in oil refineries, improving operational efficiency by 27%. Consumer behavior reflects a growing preference for high-reliability systems, particularly in critical industries, with over 55% of enterprises prioritizing automation solutions that enhance safety and operational continuity.

China – 28% share: Industrial Automation Systems market leadership driven by extensive manufacturing capacity and large-scale robotics deployment across industries.

United States – 22% share: Industrial Automation Systems market dominance supported by high enterprise adoption of advanced automation technologies and strong digital transformation initiatives.

The industrial automation systems market is characterized by a moderately consolidated structure with over 150 active global and regional competitors competing across hardware, software, and integrated solutions segments. The top five companies collectively account for approximately 48% of the market, indicating a strong presence of established players while still allowing room for emerging innovators. Leading firms are focusing heavily on research and development, allocating nearly 8% to 12% of their annual budgets toward innovation in AI-driven automation, robotics, and cloud-based control systems.

Strategic initiatives such as mergers, acquisitions, and partnerships are shaping the competitive landscape. Over 35 major strategic collaborations were recorded in recent years, focusing on expanding digital automation capabilities and integrating Industrial Internet of Things platforms. Product innovation remains a key competitive factor, with more than 60% of companies introducing advanced automation solutions incorporating predictive analytics and real-time monitoring features.

The market is also witnessing increased competition from technology providers entering the industrial domain, driving innovation and cost competitiveness. Companies are prioritizing scalable and modular solutions to cater to diverse industry requirements, while nearly 40% of vendors are focusing on sustainability-driven automation technologies to align with global environmental standards. This evolving competitive environment is fostering continuous technological advancements and expanding the overall market scope.

Siemens

ABB

Schneider Electric

Rockwell Automation

Mitsubishi Electric

Honeywell International

Emerson Electric

Yokogawa Electric Corporation

Omron Corporation

Bosch Rexroth

Fanuc Corporation

General Electric

Hitachi Ltd.

The industrial automation systems market is being transformed by rapid advancements in digital technologies, enabling enhanced operational efficiency, real-time decision-making, and improved system scalability. Artificial intelligence and machine learning have become central to modern automation, with over 60% of industrial enterprises deploying AI-driven analytics to optimize production processes. These systems can improve predictive maintenance accuracy by up to 85%, reducing unexpected equipment failures by nearly 30%. AI-powered quality inspection tools are also achieving defect detection rates exceeding 90% in high-precision manufacturing environments.

The Industrial Internet of Things is another key technological driver, with more than 70% of manufacturing facilities integrating connected sensors and smart devices into their operations. These systems generate real-time data streams, enabling a 25% increase in overall equipment effectiveness and a 20% reduction in energy consumption through intelligent resource management. Edge computing is gaining traction, allowing data processing closer to production lines, which reduces latency by up to 40% and enhances responsiveness in time-sensitive applications.

Robotics and collaborative automation technologies continue to evolve, with over 45% of factories incorporating robotic systems to improve throughput and reduce labor dependency. Advanced robotics equipped with vision systems can increase assembly accuracy by 25% and reduce cycle times by approximately 20%. Digital twin technology is also emerging as a critical innovation, enabling real-time simulation and optimization of industrial processes, leading to a 30% improvement in operational efficiency. Additionally, cloud-based automation platforms are enabling remote monitoring and centralized control, with adoption rates exceeding 50% among large enterprises, supporting scalable and flexible industrial operations.

• In January 2025, Siemens expanded its Industrial Operations X portfolio by integrating advanced generative AI capabilities into its automation software, enabling manufacturers to automate engineering workflows and improve productivity by up to 30%. The platform also enhances interoperability across multi-vendor industrial environments. Source: www.siemens.com

• In March 2025, ABB launched a new generation of AI-powered robotic systems designed for precision manufacturing, featuring enhanced vision-guided automation that improves accuracy by 20% and reduces production downtime by 25%. These systems are targeted at automotive and electronics industries. Source: www.abb.com

• In October 2024, Schneider Electric introduced an upgraded EcoStruxure Automation Expert platform with open automation standards, enabling seamless integration of industrial systems and reducing engineering time by nearly 40%. The solution supports flexible and software-defined automation architectures. Source: www.se.com

• In May 2024, Rockwell Automation partnered with a global cloud technology provider to enhance its FactoryTalk platform with advanced analytics and AI capabilities, improving real-time data processing efficiency by 35% and enabling predictive maintenance across connected industrial assets. Source: www.rockwellautomation.com

The Industrial Automation Systems Market Report provides a comprehensive analysis of key segments, technologies, applications, and regional dynamics shaping the industry landscape. The report covers a wide range of automation types including distributed control systems, programmable logic controllers, supervisory control and data acquisition systems, robotics, and machine vision technologies. Among these, control systems and robotics collectively account for over 60% of industrial deployments, highlighting their critical role in modern manufacturing environments.

From an application perspective, the report evaluates automation adoption across manufacturing, process industries, material handling, packaging, and quality control operations. Manufacturing and process industries together contribute more than 70% of total system utilization, reflecting the high demand for precision, efficiency, and continuous operations. The report also explores emerging applications such as smart warehousing and autonomous production systems, which are gaining traction with adoption rates increasing by over 25% in logistics and distribution sectors.

Geographically, the report analyzes key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, covering over 90 countries. Asia-Pacific leads in production volume, while North America and Europe demonstrate strong adoption of advanced digital automation technologies, with enterprise-level implementation rates exceeding 60%. The scope further includes evaluation of technological advancements such as AI, IIoT, edge computing, and digital twins, which are collectively improving operational efficiency by up to 30% across industries.

Additionally, the report examines industry-specific adoption trends across automotive, energy, pharmaceuticals, electronics, and food processing sectors, which together represent over 65% of automation demand. It also highlights niche and emerging segments such as sustainable automation solutions and cloud-based industrial platforms, which are expected to play a pivotal role in shaping future industrial ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, ABB, Schneider Electric, Rockwell Automation, Mitsubishi Electric, Honeywell International, Emerson Electric, Yokogawa Electric Corporation, Omron Corporation, Bosch Rexroth, Fanuc Corporation, General Electric, Hitachi Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |