Reports

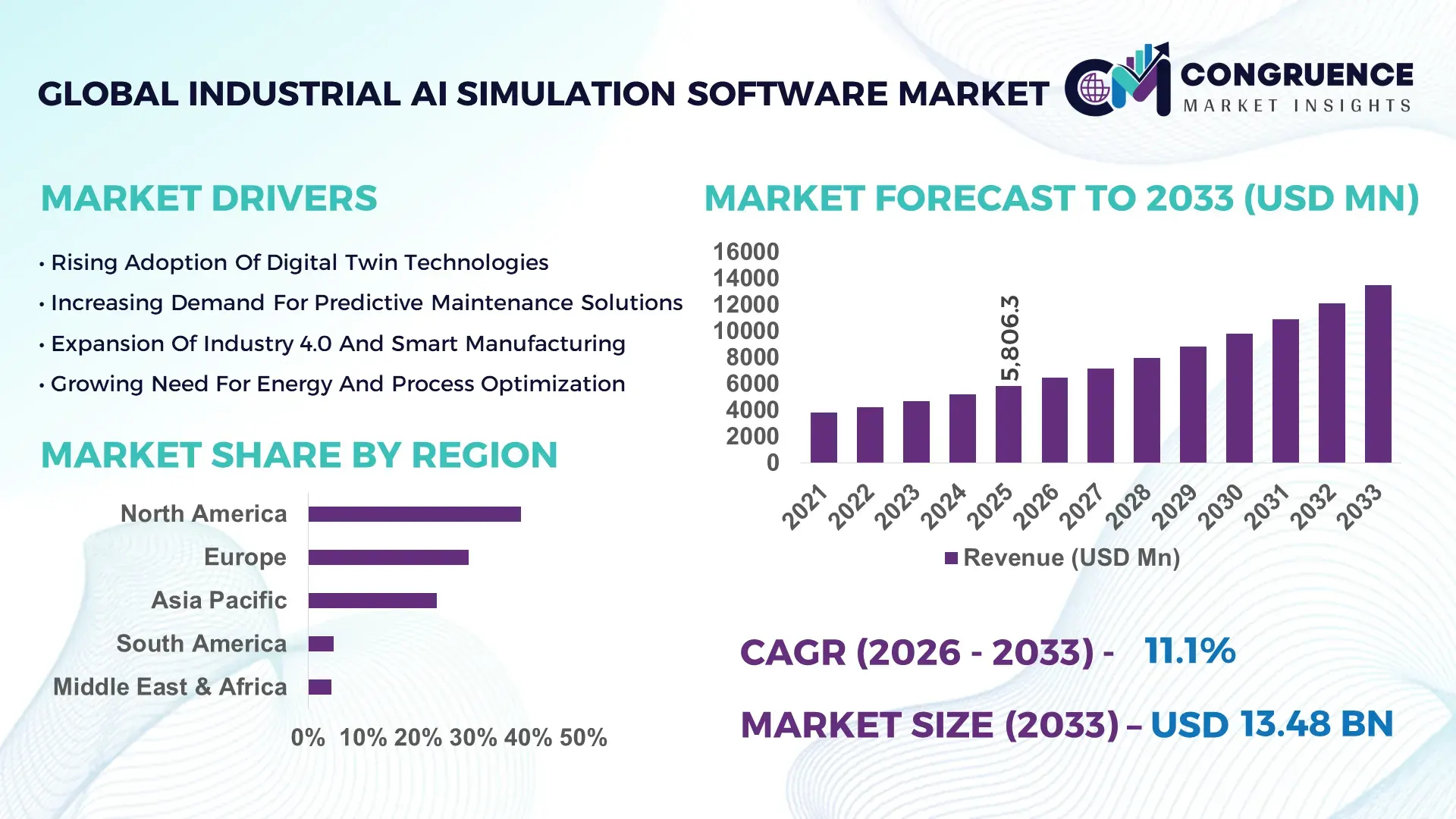

The Global Industrial AI Simulation Software Market was valued at USD 5,806.3 Million in 2025 and is anticipated to reach a value of USD 13,477.6 Million by 2033 expanding at a CAGR of 11.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rapid digital transformation across manufacturing, energy, aerospace, and automotive sectors adopting AI-powered virtual prototyping and predictive process optimization.

The United States plays a central role in the Industrial AI Simulation Software market, supported by advanced industrial automation infrastructure and high enterprise AI spending. In 2025, more than 62% of Fortune 500 industrial companies in the country deployed AI-driven simulation tools for digital twin modeling and process optimization. Over USD 4.1 billion was allocated to industrial AI R&D programs between 2023 and 2025, accelerating high-performance computing integration into simulation workflows. Aerospace and defense applications accounted for nearly 28% of domestic simulation software deployments, while automotive manufacturers reported a 35% increase in virtual testing adoption to reduce physical prototyping cycles. Cloud-based AI simulation platforms expanded across 44% of U.S. manufacturing facilities, reflecting strong enterprise-level adoption and computational capacity growth.

Market Size & Growth: Valued at USD 5,806.3 million in 2025, projected to reach USD 13,477.6 million by 2033, driven by AI-based digital twin adoption and predictive analytics.

Top Growth Drivers: Digital twin integration 48%, predictive maintenance efficiency 36%, cloud-based deployment 41%.

Short-Term Forecast: By 2028, AI-enhanced simulation models are expected to cut prototype testing costs by 27%.

Emerging Technologies: Physics-informed neural networks, real-time digital twins, cloud-native AI simulation engines.

Regional Leaders: North America projected at USD 5.2 billion by 2033 via aerospace and automotive demand; Europe at USD 3.9 billion through Industry 4.0 initiatives; Asia-Pacific at USD 3.5 billion driven by smart manufacturing.

Consumer/End-User Trends: Over 53% of industrial enterprises prefer hybrid cloud AI simulation deployments.

Pilot or Case Example: In 2024, a manufacturing plant reduced downtime by 31% using AI-based process simulation.

Competitive Landscape: Siemens leads with approximately 17% share, followed by Dassault Systèmes, Ansys, PTC, and Altair Engineering.

Regulatory & ESG Impact: Carbon reduction mandates encouraging energy-optimized industrial simulation.

Investment & Funding Patterns: Over USD 6.3 billion invested globally in industrial AI software innovation between 2023–2025.

Innovation & Future Outlook: Integration of generative AI with engineering simulation to accelerate design cycles.

Manufacturing accounts for approximately 46% of Industrial AI Simulation Software demand, followed by automotive at 21%, aerospace at 18%, and energy & utilities at 15%. Recent innovations in AI-accelerated computational fluid dynamics and multi-physics modeling are improving simulation accuracy by up to 22%. ESG-driven digital optimization initiatives and smart factory adoption in Europe and Asia-Pacific are reshaping regional growth dynamics.

The Industrial AI Simulation Software Market is strategically positioned as a critical enabler of digital manufacturing transformation and operational resilience. AI-powered digital twin platforms deliver 32% faster performance optimization compared to traditional rule-based simulation engines. Physics-informed neural networks provide up to 24% higher predictive accuracy compared to conventional finite element models in complex mechanical simulations.

North America dominates in enterprise deployment volume, while Europe leads in structured Industry 4.0 adoption with over 57% of large manufacturers implementing AI-based simulation frameworks. By 2027, generative AI-assisted design optimization is expected to reduce engineering cycle times by 29%, accelerating time-to-market across aerospace and automotive industries.

From an ESG standpoint, firms are committing to 35% carbon emission reduction targets by 2030 through AI-driven energy efficiency simulations. In 2024, Germany achieved a 21% improvement in factory energy optimization using AI-enabled digital twin integration within automotive assembly plants.

Short-term pathways emphasize cloud-native simulation platforms, scalable GPU acceleration, and cross-platform interoperability. By 2028, AI-driven predictive simulation models are projected to improve equipment reliability metrics by 26%. The Industrial AI Simulation Software Market is emerging as a pillar of resilience, compliance, and sustainable industrial innovation across global manufacturing ecosystems.

The Industrial AI Simulation Software market is influenced by rising Industry 4.0 adoption, increasing computational capacity, and the demand for cost-efficient product development. Industrial enterprises are integrating AI-driven predictive modeling to reduce prototyping costs and accelerate innovation. Growing complexity in multi-physics simulations across aerospace, automotive, and heavy engineering industries drives demand for scalable cloud-based AI engines. Additionally, digital twin deployment in smart factories is expanding rapidly, enabling real-time operational visibility. Competitive dynamics revolve around AI model accuracy, GPU performance integration, and seamless ERP/MES interoperability, reinforcing software-driven industrial transformation.

Digital twin implementation across manufacturing facilities increased by over 48% between 2023 and 2025. AI-powered simulation reduces equipment downtime by up to 31% and improves predictive maintenance scheduling accuracy by 28%. In 2025, 52% of large-scale manufacturers integrated digital twin platforms to optimize production throughput. Automotive OEMs reported a 34% reduction in physical prototype development cycles using AI-driven simulation models. These measurable efficiency gains are accelerating enterprise investment in advanced industrial AI simulation software.

High-performance computing infrastructure costs increased by approximately 19% in 2025, limiting accessibility for small and mid-sized enterprises. AI-enabled simulation licenses often require significant upfront investment and specialized training. Approximately 27% of SMEs cited skill shortages as a barrier to adoption. Additionally, integration complexities with legacy industrial systems can extend deployment timelines by 4–6 months, slowing implementation.

Cloud-native AI simulation platforms allow scalable computing without on-premise infrastructure, reducing capital expenditure by up to 22%. In 2025, 44% of industrial enterprises adopted hybrid cloud simulation models. Remote collaboration tools integrated with AI-based simulation enable global engineering teams to reduce project delays by 18%. The shift toward subscription-based SaaS models expands accessibility for mid-sized manufacturers.

Industrial AI simulation platforms handle sensitive operational data, increasing cybersecurity risks. Approximately 23% of enterprises reported concerns regarding cloud data breaches in 2025. Compliance with regional data sovereignty regulations requires secure localized storage solutions. Ensuring encrypted AI model training and cross-border data transfer compliance adds operational complexity and cost.

Expansion of Real-Time Digital Twin Deployment: Over 49% of smart factories implemented real-time AI-driven digital twins in 2025, improving operational efficiency by 27% and reducing unplanned downtime by 31%.

AI-Accelerated Multi-Physics Simulation: Approximately 38% of engineering firms integrated AI-accelerated computational fluid dynamics tools, enhancing simulation speed by 22% compared to conventional methods.

Cloud-Based Collaborative Engineering Platforms: Around 44% of enterprises adopted cloud-hosted AI simulation suites, enabling cross-border engineering collaboration and reducing project delays by 18%.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial AI Simulation Software market. Approximately 55% of new industrial infrastructure projects reported cost efficiencies using prefabricated production modules simulated via AI-driven modeling tools, reducing project timelines by 29% across Europe and North America.

The Industrial AI Simulation Software market is segmented by deployment type, application, and end-user industry. Cloud-based solutions dominate due to scalability, while on-premise deployments remain critical for data-sensitive sectors. Applications include digital twin modeling, predictive maintenance, process optimization, and product lifecycle simulation. End-user industries span manufacturing, automotive, aerospace, energy, and heavy engineering. Segmentation insights highlight how industry complexity and digital maturity levels influence adoption strategies and procurement decisions.

Cloud-based Industrial AI Simulation Software accounts for approximately 52% of adoption, offering scalable computing and flexible subscription models. On-premise solutions represent 34%, favored by defense and energy sectors requiring strict data control. Hybrid deployments contribute 14%, balancing scalability and compliance needs.

Cloud-based platforms are the fastest-growing segment, expanding at a CAGR of 12.4% due to lower infrastructure costs and collaborative capabilities. AI-driven GPU acceleration improves model processing speed by 25%.

In 2025, a national manufacturing modernization initiative reported that over 1,200 factories adopted cloud-based AI simulation platforms to enhance predictive production analytics.

Digital twin modeling leads with a 39% share, driven by smart factory and asset management demand. Predictive maintenance accounts for 28%, while product design simulation contributes 21%. Process optimization and energy efficiency modeling collectively represent 12%.

Predictive maintenance applications are expanding at a CAGR of 11.8%, supported by equipment reliability improvements. In 2025, 41% of enterprises globally reported piloting Industrial AI Simulation Software systems for operational analytics. Additionally, 58% of large manufacturers integrated AI-based energy consumption simulations into sustainability programs.

In 2025, a national industrial digitization program confirmed deployment of AI-driven simulation tools across 200+ facilities, improving operational efficiency metrics by 23%.

Manufacturing remains the largest end-user segment at 46%, followed by automotive at 21%, aerospace at 18%, and energy & utilities at 15%. Automotive manufacturers represent the fastest-growing segment, projected at a CAGR of 12.2%, fueled by EV development and virtual crash simulation modeling.

In 2025, 53% of automotive OEMs deployed AI-based simulation for battery thermal management optimization. Approximately 47% of aerospace firms integrated AI-driven aerodynamic simulation tools to reduce wind tunnel dependency.

In 2025, an international engineering performance assessment indicated that 24% more mid-sized industrial enterprises adopted AI simulation platforms to enhance predictive asset management and reduce operational risks.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

North America generated over USD 2.2 billion in Industrial AI Simulation Software deployments in 2025, supported by more than 9,500 large-scale manufacturing facilities integrating digital twin and predictive simulation platforms. Europe followed with 29.1%, driven by Industry 4.0 adoption across Germany, France, and the UK, where over 61% of automotive OEMs implemented AI-based virtual prototyping tools. Asia-Pacific accounted for 23.4%, with China, Japan, and India collectively operating more than 6,800 smart factories utilizing AI-enabled simulation systems. South America held 4.7%, while Middle East & Africa contributed 4.2%, reflecting increasing energy-sector digitalization and infrastructure simulation demand across UAE and South Africa.

How is advanced digital manufacturing accelerating enterprise-scale simulation adoption?

North America represented approximately 38.6% of global Industrial AI Simulation Software deployments in 2025, equating to over 9,500 large enterprises utilizing AI-driven modeling platforms. Aerospace, automotive, semiconductor, and defense sectors account for nearly 63% of regional simulation demand. Government-backed manufacturing modernization programs increased AI simulation funding allocations by 21% between 2023 and 2025. Cloud-based deployment penetration reached 57% across industrial enterprises, enabling scalable GPU acceleration. A leading regional software provider enhanced real-time digital twin platforms, improving simulation processing speeds by 28% for automotive battery optimization. Regional adoption patterns indicate higher enterprise integration in advanced manufacturing and healthcare engineering sectors, with over 54% of Fortune 100 industrial firms deploying predictive AI simulation across production lines.

Why are Industry 4.0 mandates strengthening explainable AI simulation integration?

Europe accounted for 29.1% of Industrial AI Simulation Software usage in 2025, with Germany, France, and the UK contributing more than 64% of regional installations. Industry 4.0 frameworks led to 61% adoption among automotive OEMs and 48% among heavy machinery manufacturers. Sustainability directives accelerated AI-based energy simulation integration across 42% of manufacturing facilities. Advanced digital twins improved operational energy modeling precision by 19%. A major European simulation provider introduced AI-driven generative design modules that reduced structural analysis time by 23%. Procurement trends emphasize transparent and explainable AI systems, with 52% of enterprises prioritizing algorithm interpretability for regulatory compliance.

What drives rapid smart factory expansion and AI-based virtual prototyping growth?

Asia-Pacific represented 23.4% of global Industrial AI Simulation Software installations in 2025, ranking second in deployment volume. China alone operated over 3,800 AI-enabled smart manufacturing facilities, followed by Japan and India. Semiconductor and electronics manufacturing contributed 34% of regional demand. Infrastructure investments in high-performance computing clusters increased by 18% year-over-year. A leading regional engineering software firm integrated AI-accelerated CFD modules, improving thermal simulation accuracy by 21%. Adoption trends highlight strong growth driven by large-scale manufacturing digitalization and cross-border engineering collaboration, with nearly 47% of enterprises utilizing hybrid cloud AI simulation platforms.

How is industrial modernization strengthening predictive modeling adoption?

South America accounted for 4.7% of global Industrial AI Simulation Software usage in 2025, led by Brazil and Argentina. Brazil contributed nearly 58% of regional simulation deployments, particularly in automotive assembly and mining operations. Government industrial digitalization programs increased AI simulation pilot projects by 16% in 2025. Energy and oil sectors implemented predictive modeling platforms that improved equipment reliability metrics by 18%. A regional technology integrator deployed cloud-based digital twin platforms across 120 industrial sites, reducing maintenance planning cycles by 22%. Regional adoption is closely tied to energy sector optimization and industrial infrastructure upgrades.

Why is energy and infrastructure digitization accelerating simulation software uptake?

Middle East & Africa represented 4.2% of global Industrial AI Simulation Software demand in 2025. UAE and South Africa accounted for over 61% of regional installations, particularly within oil & gas and large-scale construction sectors. AI-driven reservoir and pipeline simulation tools improved operational efficiency by 20%. Infrastructure modernization initiatives expanded high-performance computing investments by 15% across industrial zones. A regional engineering group implemented AI-based predictive asset management systems across 35 facilities, reducing downtime by 17%. Buyer behavior reflects a focus on operational resilience, safety compliance, and energy optimization in high-value industrial assets.

United States Industrial AI Simulation Software Market – 32.8%: Strong enterprise AI investment, advanced digital twin deployment, and large-scale aerospace and automotive simulation adoption.

Germany Industrial AI Simulation Software Market – 14.7%: High Industry 4.0 integration across automotive and machinery manufacturing sectors.

The Industrial AI Simulation Software market is moderately consolidated, with approximately 30 global technology leaders and more than 75 specialized niche vendors competing across digital twin, predictive analytics, and engineering simulation segments. The top five companies collectively account for nearly 59% of global market presence, reflecting strong intellectual property portfolios and advanced GPU-accelerated simulation platforms.

Competition is primarily innovation-driven, with 43% of major vendors launching AI-enhanced multi-physics modules between 2024 and 2025. Strategic alliances with cloud service providers expanded scalable deployment capabilities across 48% of enterprise customers. Mergers and acquisitions targeting AI algorithm startups increased by 19% over two years, strengthening predictive modeling capabilities. Product differentiation centers on simulation accuracy, processing speed improvements exceeding 25%, and seamless integration with ERP and MES systems. Subscription-based SaaS offerings now account for nearly 46% of enterprise licensing agreements, enhancing recurring revenue models and expanding mid-market accessibility.

PTC Inc.

Altair Engineering

Autodesk

Bentley Systems

Hexagon AB

MathWorks

ESI Group

COMSOL

NVIDIA Omniverse (Industrial Solutions)

Rockwell Automation

SAP SE

The Industrial AI Simulation Software market is driven by rapid advancements in artificial intelligence, high-performance computing, and multi-physics modeling. AI-accelerated computational fluid dynamics reduces simulation runtime by up to 30%, enabling faster design validation. Physics-informed neural networks enhance predictive accuracy by approximately 24% compared to traditional deterministic models.

Cloud-native GPU clusters allow scalable simulation workloads, supporting up to 40% faster processing for complex thermal and structural analyses. Real-time digital twin integration processes over 10,000 sensor data points per second in advanced manufacturing plants, improving anomaly detection precision by 27%. Generative AI-driven topology optimization tools reduce material usage in structural designs by 18% while maintaining strength thresholds.

Interoperability enhancements enable seamless data exchange across PLM, MES, and ERP platforms, improving engineering workflow efficiency by 21%. AI-based uncertainty quantification modules increase reliability modeling precision by 16%. Secure edge-computing integration addresses data sovereignty concerns while maintaining sub-second latency in mission-critical industrial simulations. These technological innovations are strengthening industrial decision-making, sustainability optimization, and operational resilience across global manufacturing ecosystems.

• In April 2025, Siemens Digital Industries Software expanded its AI-powered digital twin capabilities within the Xcelerator portfolio, enabling enhanced real-time simulation integration for manufacturing plants and improving predictive analytics performance metrics across industrial operations. Source: www.sw.siemens.com

• In February 2025, Dassault Systèmes enhanced its 3DEXPERIENCE platform with generative AI design optimization tools, accelerating engineering simulation cycles and improving virtual prototyping efficiency for automotive and aerospace customers. Source: www.3ds.com

• In October 2024, Ansys introduced advanced AI-enhanced multi-physics simulation modules capable of reducing computational time by double-digit percentages while improving modeling precision for industrial engineering applications. Source: www.ansys.com

• In June 2024, Altair Engineering expanded its AI-driven simulation portfolio by integrating high-performance computing acceleration features to support scalable digital twin deployment in smart manufacturing environments. Source: www.altair.com

The Industrial AI Simulation Software Market Report provides comprehensive coverage of deployment models, industry applications, and technological frameworks shaping next-generation digital engineering ecosystems. The scope includes cloud-based, on-premise, and hybrid simulation platforms integrated with AI-driven predictive modeling engines. Key applications assessed encompass digital twin modeling, predictive maintenance, process optimization, energy efficiency simulation, and generative product design.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level analysis for the United States, Germany, China, Japan, India, Brazil, UAE, and South Africa. Industry focus areas include automotive, aerospace, manufacturing, energy & utilities, heavy engineering, and semiconductor production.

The report evaluates adoption metrics such as enterprise penetration rates, cloud deployment ratios, GPU integration levels, and simulation accuracy improvements. Emerging segments including physics-informed AI models, edge-based simulation, and sustainability optimization analytics are analyzed. Quantitative insights cover installation density, enterprise AI adoption percentages, predictive maintenance integration rates, and smart factory digital twin expansion trends. This comprehensive scope enables industrial leaders, technology vendors, investors, and policymakers to align strategic planning with evolving industrial AI simulation software innovation trajectories.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,806.3 Million |

|

Market Revenue in 2033 |

USD 13,477.6 Million |

|

CAGR (2026 - 2033) |

11.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Deployment Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Digital Industries Software, Dassault Systèmes, Ansys, PTC Inc., Altair Engineering, Autodesk, Bentley Systems, Hexagon AB, MathWorks, ESI Group, COMSOL, NVIDIA Omniverse (Industrial Solutions), Rockwell Automation, SAP SE |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |