Reports

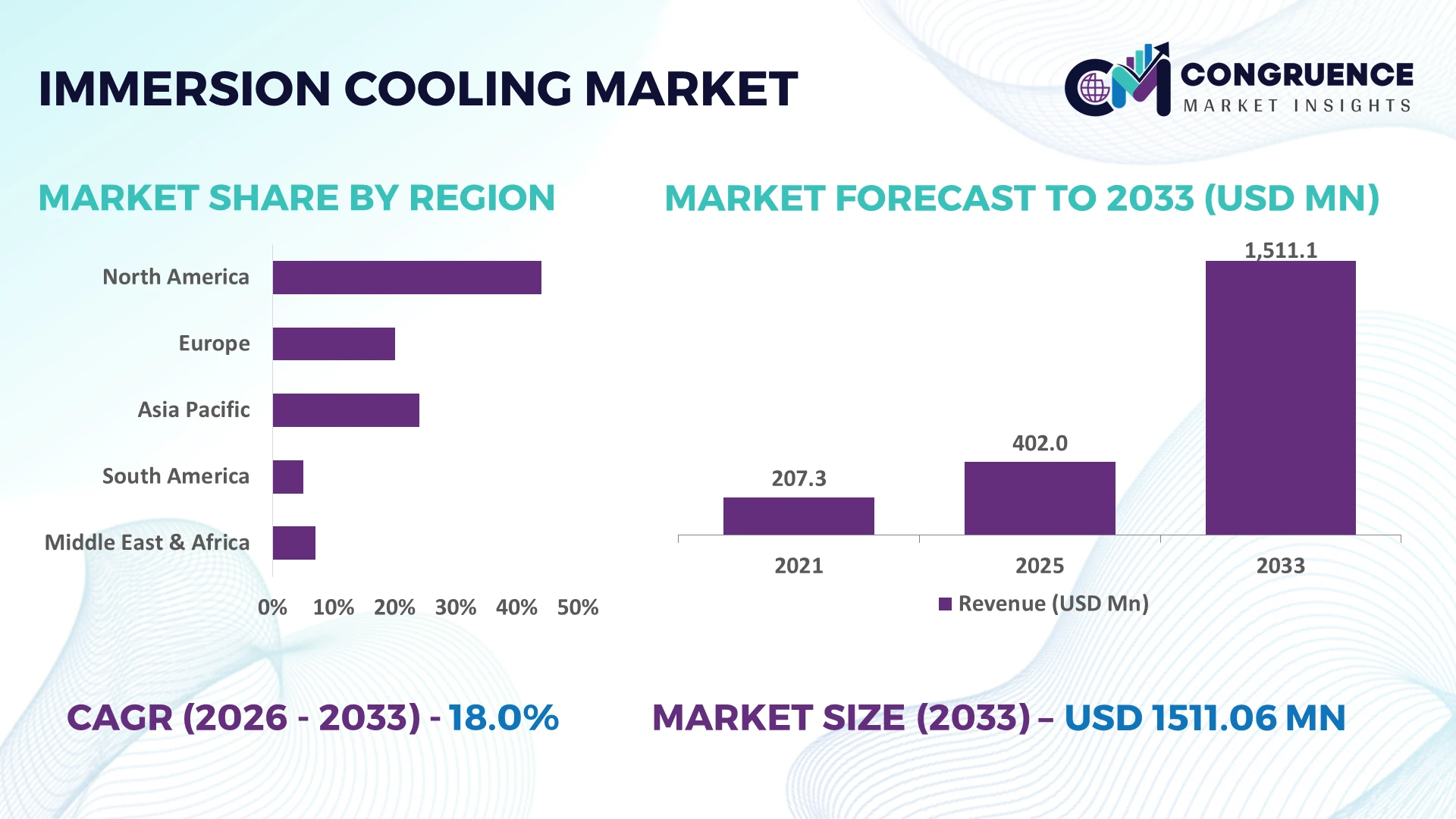

The Global Immersion Cooling Market was valued at USD 402 Million in 2025 and is anticipated to reach a value of USD 1511.06 Million by 2033 expanding at a CAGR of 18% between 2026 and 2033. Market expansion is driven by hyperscale AI infrastructure, high-density data centers exceeding 100 kW per rack, advanced liquid cooling deployment, and stricter energy-efficiency targets that accelerate replacement of conventional air-cooling architectures.

The United States remains the dominant country, accounting for approximately 36% of global immersion cooling deployments, supported by multi-billion-dollar AI data center investments and rapid hyperscale expansion. China follows with nearly 24% share, driven by cloud computing, semiconductor manufacturing, and industrial digitalization. Export controls on advanced chips continue influencing regional infrastructure strategies, while North American facilities report power usage effectiveness approaching 1.05 through advanced immersion cooling implementation.

Organizations prioritizing scalable immersion cooling infrastructure gain stronger operational resilience, lower energy intensity, and improved readiness for next-generation AI computing capacity.

Market Size & Growth: USD 402 Million (2025) to USD 1511.06 Million (2033) at 18% CAGR, driven by hyperscale AI computing and high-density data center expansion.

Top Growth Drivers: AI infrastructure (+38%), rack power density above 100 kW, and energy-efficiency improvements exceeding 30% accelerate deployment.

Short-Term Forecast: By 2028, cooling energy consumption declines by nearly 40% while server density increases over 25% across advanced facilities.

Emerging Technologies: AI-based thermal optimization, two-phase immersion cooling, and advanced dielectric fluids improve cooling precision and operational automation.

Regional Leaders: North America (~USD 560 Million), Asia-Pacific (~USD 470 Million), and Europe (~USD 300 Million) benefit from hyperscale expansion, semiconductor investment, and sustainability initiatives.

Consumer/End-User Trends: Over 55% of new AI and HPC deployments evaluate liquid-based cooling for higher computing density and lower operating costs.

Pilot/Case Example: In 2026, an enterprise AI infrastructure project reduced cooling energy by approximately 45% while increasing compute utilization by more than 20%.

Competitive Landscape: Leading vendors collectively control nearly 40% of the market, with GRC, Submer, LiquidStack, Asperitas, and Iceotope strengthening global competition.

Regulatory & ESG Impact: Advanced cooling solutions reduce data center energy consumption by up to 40%, supporting stricter carbon reduction and efficiency objectives.

Investment & Funding: More than USD 2 Billion in infrastructure investment supports strategic partnerships, manufacturing expansion, and regional supply-chain diversification.

Innovation & Future Outlook: Next-generation dielectric fluids, modular immersion systems, and AI-enabled thermal management strengthen long-term competitiveness and global infrastructure resilience.

Increasing AI training clusters, hyperscale cloud facilities, and high-performance computing environments are expanding demand for advanced immersion cooling solutions. Recent innovation focuses on environmentally optimized dielectric fluids, modular tank systems, and intelligent thermal monitoring, improving cooling efficiency by over 30%. Ongoing semiconductor supply-chain localization and stricter energy-efficiency requirements are reinforcing deployment priorities, setting the stage for broader strategic market assessment.

Immersion cooling has become a strategic infrastructure technology as AI computing, hyperscale cloud expansion, and high-performance computing continue raising rack power densities beyond conventional cooling capabilities. Infrastructure modernization and stricter energy-efficiency standards are accelerating investment decisions, while semiconductor supply-chain restructuring is encouraging localized data center expansion in the United States, Japan, and India. Enterprises increasingly view thermal management as a competitive differentiator that directly influences computing capacity, operating costs, and facility utilization.

Compared with traditional air cooling, immersion cooling can reduce cooling energy consumption by approximately 35–45% while supporting rack densities exceeding 100 kW with lower maintenance requirements. The United States leads commercial deployment through hyperscale AI infrastructure, whereas Japan emphasizes precision engineering and high-reliability industrial computing. Over the next two to three years, enterprise liquid-cooling adoption across newly commissioned AI facilities is expected to surpass 30%, supported by modular deployment models and standardized cooling ecosystem development.

A practical example is the deployment of immersion-cooled AI clusters that increase server utilization while reducing cooling-related downtime through simplified thermal management. Vendors are strengthening partnerships with dielectric fluid suppliers, server manufacturers, and colocation providers while expanding localized production capabilities. Companies that integrate immersion cooling into long-term digital infrastructure strategies secure stronger operational efficiency, infrastructure resilience, and competitive positioning in next-generation computing environments.

The rapid deployment of AI training clusters and high-performance computing infrastructure is transforming immersion cooling into a core operational requirement. Modern AI servers increasingly operate above 100 kW per rack, while immersion technology lowers cooling energy demand by nearly 40% and improves server utilization by over 20%. The United States continues expanding hyperscale campuses, while India is accelerating domestic AI infrastructure under digital transformation initiatives. This structural shift is prompting equipment manufacturers to develop immersion-ready servers and collaborate with cooling solution providers. Strategic partnerships, localized manufacturing, and integrated thermal management platforms are enabling faster deployment cycles while improving infrastructure efficiency and long-term operating performance.

Large-scale deployment remains constrained by specialized infrastructure costs, retrofit complexity, and limited interoperability across hardware platforms. Converting conventional facilities into immersion-ready environments typically increases initial installation expenditure by 20–35%, while more than 60% of existing enterprise data centers were originally designed around air-cooling architecture. Supply concentration for advanced dielectric fluids also creates procurement challenges during periods of industrial expansion. To reduce operational risk, companies are diversifying component sourcing, establishing regional manufacturing partnerships, and negotiating long-term procurement agreements. Standardized system architecture is becoming a priority to improve deployment consistency and reduce lifecycle ownership costs across enterprise facilities.

The emergence of edge AI, modular computing infrastructure, and sovereign digital infrastructure programs is creating new commercial opportunities beyond hyperscale facilities. Modular immersion systems can reduce physical cooling footprints by approximately 30% while improving deployment flexibility for industrial campuses and telecom facilities. Japan and Singapore are encouraging energy-efficient digital infrastructure through sustainability-focused policies, accelerating adoption of advanced cooling technologies. Companies are investing in next-generation dielectric fluids, AI-enabled thermal monitoring, and integrated modular platforms to serve distributed computing environments. A significant strategic opportunity lies in designing standardized immersion solutions for edge deployments where space constraints and power efficiency deliver stronger competitive value.

Long-term market expansion depends on overcoming integration complexity across diverse enterprise IT environments rather than simply increasing cooling capacity. More than 70% of existing enterprise facilities continue operating mixed hardware generations, making migration planning and workload compatibility technically demanding. The growing use of AI workloads also increases infrastructure monitoring requirements and operational skill demands. Germany and the United States are investing in advanced digital infrastructure expertise to address workforce capability gaps alongside technology deployment. Companies must strengthen engineering capabilities, workforce training, software-driven thermal management, and ecosystem partnerships to achieve consistent implementation quality while maintaining operational resilience and long-term infrastructure competitiveness.

AI Rack Density Expansion AI infrastructure is rapidly shifting toward rack densities above 100 kW, with immersion-ready deployments increasing by nearly 35% across new hyperscale facilities. Server utilization improves by more than 20% while cooling energy declines by approximately 40%. U.S. cloud operators are redesigning facility layouts, and equipment vendors are expanding partnerships with server manufacturers to deliver integrated immersion-ready platforms as advanced AI hardware transitions accelerate.

Modular Deployment Becomes Standard Modular immersion cooling systems are shortening installation timelines by nearly 30% while reducing facility expansion complexity by over 25%. Enterprise operators increasingly deploy prefabricated cooling units to support phased capacity additions rather than complete infrastructure replacement. Japan's emphasis on efficient digital infrastructure is encouraging standardized modular designs, prompting vendors to automate manufacturing and strengthen regional deployment partnerships for faster commercial implementation.

Advanced Dielectric Fluid Innovation Next-generation dielectric fluids are improving thermal transfer efficiency by approximately 18% while extending equipment service intervals by nearly 15%. Growing environmental compliance requirements and operational sustainability targets are encouraging suppliers to develop recyclable fluid formulations. Companies are investing in joint product development, fluid monitoring software, and certification programs to improve long-term reliability while simplifying maintenance across high-density computing environments.

Integrated Digital Thermal Management AI-enabled thermal analytics are reducing unplanned cooling incidents by almost 25% while improving predictive maintenance accuracy above 90%. Enterprise operators increasingly combine immersion systems with digital infrastructure monitoring platforms to optimize workload distribution and energy performance. Supply-chain diversification for cooling components is also reshaping procurement strategies, leading technology providers to strengthen software integration capabilities and long-term service partnerships.

Single-Phase Cooling remains the dominant segment because of its straightforward deployment, lower maintenance complexity, and compatibility with existing enterprise server architectures. Approximately 55% of commercial immersion installations continue using single-phase technology due to simplified operations and faster implementation across hyperscale and enterprise facilities. Closed Bath Systems are also gaining steady acceptance where contamination control and long-term operational stability are critical. Open Bath Systems remain relevant for laboratory environments and pilot deployments, while Modular Systems are strengthening their position through flexible infrastructure expansion and standardized installation models.

Two-Phase Cooling represents the fastest-growing segment as advanced AI processors and high-density computing require superior heat dissipation. Thermal transfer efficiency can improve by nearly 20% compared with conventional immersion configurations, making the technology attractive for next-generation AI clusters. Vendors are increasing investment in advanced dielectric fluids, engineering partnerships, and modular product development to accelerate deployment. Enterprise buyers are balancing proven operational simplicity with future thermal performance, creating a gradual shift toward higher-value immersion technologies across mission-critical computing environments.

Data Centers represent the largest application segment as hyperscale cloud providers and enterprise facilities continue replacing conventional cooling systems with immersion technologies for higher computing density. Nearly 60% of large-scale immersion deployments support data center infrastructure where lower cooling energy consumption and improved rack utilization directly enhance operating efficiency. High-Performance Computing remains a mature application supporting research, engineering simulation, and industrial modeling where sustained thermal performance is essential for continuous processing.

AI Computing is the fastest-growing application as generative AI training infrastructure rapidly increases hardware density and thermal requirements. Enterprise AI deployments have expanded by more than 30% in advanced computing environments, encouraging suppliers to integrate immersion-ready servers and intelligent thermal management software. Edge Computing is emerging as distributed digital infrastructure expands, while Cryptocurrency Mining continues adopting immersion systems to improve equipment longevity and energy efficiency. Companies are scaling deployment partnerships and integrated infrastructure offerings to capture demand across multiple computing environments.

Cloud Service Providers account for the largest share of immersion cooling deployments because hyperscale infrastructure requires continuous thermal optimization and high server utilization. Around 58% of advanced immersion installations are associated with large cloud environments supporting AI, analytics, and enterprise digital services. IT & Telecom organizations continue expanding adoption as network virtualization and edge infrastructure increase equipment density, requiring scalable cooling solutions capable of supporting uninterrupted operations.

Government organizations represent the fastest-growing end-user segment as sovereign AI initiatives and national digital infrastructure programs accelerate investment in secure computing facilities. Public-sector digital infrastructure projects have increased by approximately 25% across several technology-focused economies, encouraging suppliers to develop customized cooling platforms and long-term support agreements. BFSI institutions are adopting immersion cooling for high-performance transaction processing, while Research Institutions continue deploying specialized systems for scientific computing. Vendors are strengthening ecosystem partnerships, customized service models, and enterprise integration capabilities to secure long-term competitive positioning across diverse customer groups.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 20.4% CAGR between 2026 and 2033.

AI Infrastructure Expansion Strengthens Market Leadership

North America maintains the leading position through extensive hyperscale data center construction, advanced semiconductor ecosystems, and rapid enterprise AI deployment. The region represents approximately 39% of global immersion cooling adoption, supported by large-scale cloud infrastructure and high-performance computing investments. Rack densities exceeding 100 kW are accelerating the transition from conventional cooling systems toward immersion technologies. A growing number of new AI facilities are being designed with liquid-ready architectures from the planning stage, reducing retrofit complexity and improving operational efficiency. Strategic collaborations among cloud providers, cooling technology developers, and server manufacturers continue expanding integrated deployment capabilities, while infrastructure modernization programs strengthen long-term competitiveness across enterprise and research computing environments.

United States Market Outlook: The United States remains the regional growth engine through its concentration of hyperscale cloud operators, AI infrastructure investments, and semiconductor innovation. More than 65% of North American large-scale AI data center deployments are located within the country, encouraging wider adoption of immersion cooling technologies. Enterprises are expanding long-term partnerships with equipment manufacturers and dielectric fluid suppliers while integrating advanced thermal management into next-generation digital infrastructure to improve computing efficiency and operational resilience.

Sustainability Policies Accelerate Cooling Modernization

Europe is strengthening immersion cooling adoption through energy-efficiency regulations, sustainable data center initiatives, and expanding AI infrastructure. The region accounts for approximately 27% of global deployment activity, with enterprises prioritizing lower power consumption and improved thermal performance. Growing investment in sovereign digital infrastructure and research computing is encouraging broader implementation of advanced liquid cooling technologies. Several operators are modernizing existing facilities with modular immersion platforms capable of reducing cooling energy demand by nearly 35%. Equipment suppliers are expanding engineering partnerships and localized support capabilities to meet stricter environmental performance standards while improving infrastructure reliability across enterprise computing environments.

Germany Market Outlook: Germany leads the European market through its advanced industrial manufacturing base, engineering expertise, and expanding digital infrastructure. Enterprise operators are increasingly deploying immersion cooling within AI research facilities and industrial computing centers, while national sustainability objectives encourage efficient thermal management solutions. Large technology partnerships and continued investment in high-performance computing strengthen Germany's position as a primary innovation and deployment hub for advanced cooling technologies.

Manufacturing Scale Drives Rapid Deployment

Asia-Pacific is emerging as the fastest-expanding regional market due to accelerated AI infrastructure development, semiconductor manufacturing growth, and increasing hyperscale cloud investments. The region contributes approximately 25% of global immersion cooling deployments while rapidly expanding manufacturing capacity for cooling components and supporting infrastructure. China, Japan, Singapore, and India are strengthening enterprise digital infrastructure through new data center developments and localized technology ecosystems. Infrastructure projects increasingly integrate immersion-ready designs, improving deployment efficiency and reducing long-term operating costs. Technology vendors are expanding manufacturing facilities, strategic partnerships, and regional engineering support to address rising demand for advanced thermal management solutions.

China Market Outlook: China leads regional deployment through extensive cloud computing capacity, semiconductor manufacturing, and industrial digitalization initiatives. Approximately 45% of Asia-Pacific hyperscale data center expansion is concentrated within China, creating sustained demand for high-density cooling technologies. Domestic companies continue investing in localized immersion cooling production, integrated AI infrastructure, and advanced dielectric fluid development to strengthen supply-chain resilience and support national computing capacity expansion.

Digital Infrastructure Creates Emerging Demand

South America is gradually expanding immersion cooling adoption as enterprise digital transformation and cloud infrastructure investment increase across major economies. The region contributes roughly 5% of global market activity, with deployment concentrated in modern data centers supporting financial services, telecommunications, and enterprise computing. Infrastructure limitations remain a practical constraint, yet operators are prioritizing energy-efficient cooling technologies to improve facility performance. Modular deployment approaches are shortening implementation timelines by nearly 20%, encouraging broader commercial adoption. Technology providers are strengthening regional distribution partnerships and localized technical support to improve deployment consistency and reduce implementation complexity.

Brazil Market Outlook: Brazil represents the largest market within South America through its expanding cloud infrastructure, financial technology ecosystem, and enterprise digitalization programs. Large metropolitan data center clusters continue investing in advanced cooling technologies to support higher computing densities and improve operational efficiency. Companies are establishing regional service partnerships and technical integration capabilities while modernizing facilities for AI-enabled enterprise workloads and long-term infrastructure scalability.

Strategic Infrastructure Investment Expands Adoption

The Middle East & Africa market is advancing through digital infrastructure modernization, hyperscale data center development, and government-supported technology diversification initiatives. The region accounts for approximately 4% of global immersion cooling deployment, with increasing investment directed toward AI-ready computing infrastructure and sustainable facility design. Large-scale digital transformation projects are encouraging adoption of advanced cooling systems capable of improving thermal efficiency while supporting demanding enterprise workloads. International technology partnerships and regional infrastructure investments are strengthening deployment capabilities, particularly in strategically located cloud and colocation facilities designed for future computing requirements.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through ambitious smart infrastructure programs, expanding cloud investments, and strong international technology partnerships. Enterprise operators are integrating immersion cooling into new high-performance computing facilities while prioritizing energy-efficient infrastructure. Continued investment in digital economy initiatives and AI innovation ecosystems is reinforcing the country's role as the principal regional hub for advanced data center technologies and next-generation thermal management solutions.

The market is led by GRC, Submer, LiquidStack, Iceotope, and Asperitas, while regional engineering specialists compete through localized deployment, and dielectric fluid suppliers challenge OEM-led integrated solutions. The top five players collectively control approximately 52% of the global market. Competition centers on thermal efficiency, deployment speed, and integrated infrastructure rather than pricing alone. Advanced immersion platforms reduce cooling energy by nearly 40%, while modular deployment shortens installation time by about 30%, giving technology-focused vendors a measurable advantage. Global leaders strengthen positions through hyperscale partnerships, manufacturing expansion, and integrated server compatibility, whereas regional providers compete with customized engineering and faster project execution. Vertical integration between cooling hardware, dielectric fluids, and monitoring software is reshaping procurement decisions. Consolidation is increasing as AI infrastructure providers seek complete cooling ecosystems instead of standalone products. The principal entry barrier remains engineering validation and enterprise qualification for mission-critical environments. Sustainable competitive success depends on scalable technology, proven reliability, ecosystem partnerships, and rapid deployment capability.

GRC

Submer

LiquidStack

Iceotope Technologies

Asperitas

Fujitsu Limited

Schneider Electric

Vertiv Holdings Co.

Green Revolution Cooling

Midas Immersion Cooling

LiquidCool Solutions

Asperitas BV

Wiwynn Corporation

Immersion cooling technology is evolving from specialized deployment into mainstream digital infrastructure for AI and high-performance computing. Single-phase immersion remains the most widely implemented technology because of operational simplicity and compatibility with existing server platforms, while two-phase immersion is expanding across ultra-high-density workloads requiring superior heat transfer. Compared with advanced air cooling, modern immersion systems reduce cooling energy consumption by approximately 35–45% while supporting rack densities exceeding 100 kW. More than 30% of newly designed AI-ready facilities now evaluate liquid-based thermal architectures during infrastructure planning, reflecting a structural shift toward higher computing efficiency.

Emerging innovation focuses on advanced dielectric fluids, AI-driven thermal analytics, digital twin integration, and modular immersion platforms. Intelligent monitoring improves predictive maintenance accuracy by nearly 25%, while automated thermal optimization enhances infrastructure utilization by around 20%. Hyperscale cloud providers, semiconductor manufacturers, and enterprise AI operators gain the strongest competitive advantage through lower operating costs, greater equipment reliability, and improved computing density. Vendors are integrating cooling platforms with intelligent infrastructure management software to strengthen lifecycle performance and simplify large-scale deployments.

Between 2026 and 2028, standardized immersion-ready server designs, recyclable dielectric fluids, and factory-built modular systems will accelerate enterprise implementation. Organizations investing early in integrated immersion ecosystems, software-driven thermal management, and strategic technology partnerships will achieve faster infrastructure scaling, stronger operational resilience, and superior competitiveness in AI-intensive computing environments.

September 2024 LiquidStack secured a USD 20 million Series B extension led by Tiger Global to expand U.S. manufacturing and accelerate direct-to-chip and immersion cooling portfolios. The investment strengthened production capacity for AI-driven data center demand and faster commercial deployment.

October 2024 Submer, together with Castrol and Supermicro, showcased targeted-flow immersion cooling for AI servers supporting up to 1,000W thermal design power per node using NVIDIA Grace Hopper systems. The demonstration validated higher-density AI infrastructure with improved thermal efficiency.

November 2025 LiquidStack signed a strategic partnership with Innovo to co-develop liquid-cooled modular data centers for the UAE, enabling higher compute density with improved energy efficiency through modular infrastructure integration. The collaboration expands commercial deployment across Middle Eastern AI facilities.

February 2026 Trane Technologies announced its acquisition of LiquidStack to strengthen end-to-end data center thermal management capabilities, integrating advanced immersion and liquid cooling technologies into its global portfolio. The move expands worldwide deployment capacity for hyperscale AI infrastructure.

This report provides comprehensive coverage of the immersion cooling market across major technology types, applications, end-users, and regional markets between 2026 and 2033. The analysis evaluates Single-Phase Cooling, Two-Phase Cooling, Open Bath Systems, Closed Bath Systems, and Modular Systems while examining adoption across data centers, AI computing, high-performance computing, edge computing, and cryptocurrency mining. It also assesses demand from cloud service providers, IT & telecom, BFSI, research institutions, and government organizations, representing more than 90% of commercial deployment activity.

The study combines competitive benchmarking, technology assessment, regional deployment trends, and operational performance analysis to support investment planning and expansion strategies. It evaluates deployment patterns, enterprise adoption, infrastructure modernization, and evolving supply-chain dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Strategic insights include technology positioning, partnership activity, innovation priorities, competitive differentiation, and emerging niche opportunities, enabling stakeholders to strengthen market positioning and make informed long-term business decisions.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 402 Million |

Market Revenue in 2033 | USD 1511.06 Million |

CAGR (2026 - 2033) | 18% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | GRC, Submer, LiquidStack, Iceotope Technologies, Asperitas, Fujitsu Limited, Schneider Electric, Vertiv Holdings Co., Green Revolution Cooling, Midas Immersion Cooling, LiquidCool Solutions, Asperitas BV, Wiwynn Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |