Reports

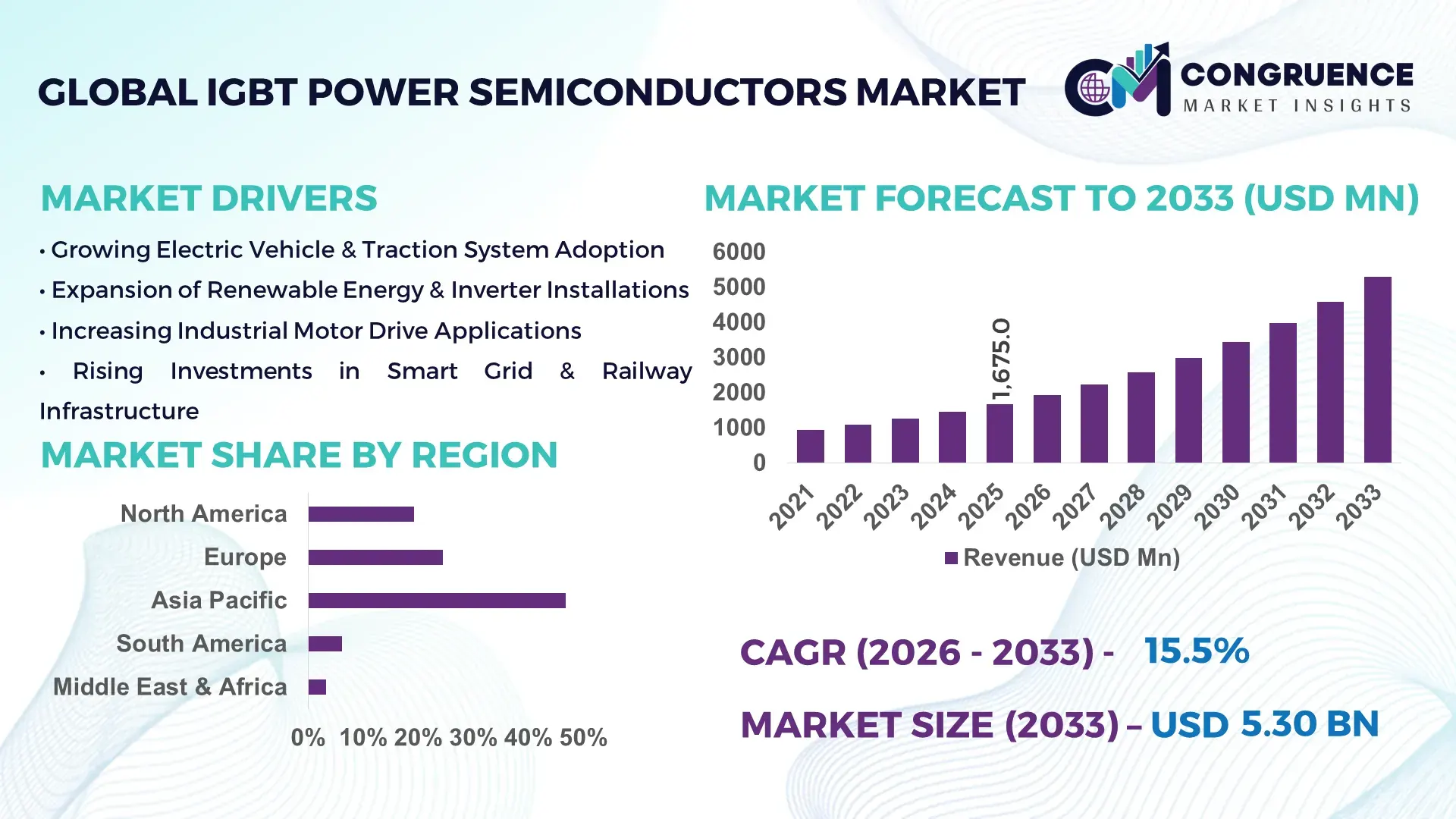

The Global IGBT Power Semiconductors Market was valued at USD 1,675.0 Million in 2025 and is anticipated to reach a value of USD 5,304.8 Million by 2033 expanding at a CAGR of 15.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by accelerating electrification across transportation, industrial automation, and renewable energy infrastructure.

China dominates the IGBT Power Semiconductors Market through its scale of manufacturing capacity, capital deployment, and application intensity across electric mobility and power infrastructure. By 2024, China operated more than 70 dedicated power semiconductor fabrication lines, with annual IGBT module output exceeding 1.2 billion units. State-backed investments in domestic semiconductor programs surpassed USD 45 billion between 2020 and 2024, with a strong focus on 650V and 1,200V trench IGBT platforms. Over 65% of electric vehicle inverters manufactured in China integrate locally produced IGBT modules, while more than 58% of new wind turbines installed in 2023 used Chinese-sourced power devices.

Market Size & Growth: USD 1,675.0 Million in 2025, projected to reach USD 5,304.8 Million by 2033 at 15.5% CAGR, driven by electrification of transport and renewable power systems.

Top Growth Drivers: EV inverter adoption +32%, industrial energy-efficiency upgrades +27%, renewable grid integration +24%.

Short-Term Forecast: By 2028, average IGBT switching losses are expected to decline by 18% through trench-gate optimization.

Emerging Technologies: 1,700V field-stop IGBTs, hybrid SiC–IGBT modules, and AI-optimized gate drivers.

Regional Leaders: Asia Pacific USD 2,420 Million by 2033 with EV inverter dominance; Europe USD 1,380 Million with rail traction focus; North America USD 1,050 Million with grid-scale storage adoption.

Consumer/End-User Trends: Automotive OEMs account for 41% of demand, followed by industrial drives at 28%.

Pilot or Case Example: In 2024, a Japanese rail operator achieved 14% traction efficiency improvement using next-gen 1,200V IGBT modules.

Competitive Landscape: Infineon ~22% share, followed by Mitsubishi Electric, Fuji Electric, STMicroelectronics, and onsemi.

Regulatory & ESG Impact: Efficiency mandates target 20% inverter loss reduction by 2030 across major markets.

Investment & Funding Patterns: Over USD 18 billion invested globally in power semiconductor fabs between 2021–2024.

Innovation & Future Outlook: Integration of digital gate control and co-packaged cooling systems reshaping high-power modules.

IGBT power semiconductors serve automotive traction systems with 41% demand contribution, industrial motor drives at 28%, and renewable energy inverters at 21%. Recent innovations include 7th-generation trench field-stop devices reducing conduction losses by 20% and advanced sintered-silver packaging extending module lifetimes beyond 20 years. Regulatory efficiency standards and grid decarbonization policies are reshaping regional consumption, while hybrid IGBT–SiC architectures define the next performance frontier.

The IGBT Power Semiconductors Market occupies a central strategic role in the global electrification and energy-transition agenda. IGBTs form the switching backbone of electric vehicle drivetrains, rail traction converters, wind turbine inverters, and high-voltage industrial drives, where reliability and efficiency directly affect system-level performance and lifecycle cost. In automotive traction, modern 1,200V trench IGBTs deliver 12% lower conduction losses compared to planar gate standards, enabling extended driving range and reduced thermal management loads.

From a technology benchmark perspective, silicon carbide MOSFETs deliver 35% higher switching efficiency compared to legacy IGBT modules in high-frequency applications, while IGBTs retain a 40–50% cost advantage in medium-voltage power classes. Regionally, Asia Pacific dominates in volume, while Europe leads in adoption with over 62% of rail traction systems migrating to next-generation IGBT platforms by 2024.

By 2028, AI-assisted gate control is expected to cut inverter failure rates by 25% through predictive switching optimization. Firms are committing to ESG metrics such as 30% reduction in module-level energy losses and 90% recyclable packaging by 2030. In 2023, a leading German manufacturer achieved a 17% reduction in thermal cycling degradation through advanced sintering and digital monitoring integration. Looking forward, the IGBT Power Semiconductors Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable electrification growth.

The IGBT Power Semiconductors Market dynamics are shaped by accelerating electrification, tightening energy-efficiency standards, and rising system voltage levels across transport and industrial sectors. Demand growth is closely linked to inverter installations in electric vehicles, renewable energy plants, and factory automation. Technological progress in trench-gate design, field-stop layers, and advanced packaging is improving power density and thermal stability. At the same time, supply chains are influenced by fab localization strategies, government semiconductor incentives, and qualification cycles exceeding 24 months. Adoption patterns increasingly favor integrated intelligent power modules, reshaping competitive positioning and system design architectures across regions.

Electric vehicle electrification is a primary driver for IGBT adoption, as traction inverters rely on 650V to 1,200V devices for power conversion. By 2024, over 38 million electric vehicles globally used IGBT-based inverters, with average device content per vehicle exceeding USD 120. Rail electrification projects added more than 9,000 km of new electric track annually, each kilometer requiring high-power IGBT converters for substations and rolling stock. Industrial electrification further amplifies demand, with variable-frequency drives now installed in over 60% of new heavy motors worldwide.

Wide-bandgap devices such as silicon carbide and gallium nitride increasingly substitute IGBTs in high-frequency and high-efficiency segments. In fast-charging infrastructure, over 45% of new 350 kW chargers now use SiC MOSFETs instead of IGBTs due to 30–40% lower switching losses. Qualification costs for next-generation IGBT platforms exceed USD 15 million per device family, extending development cycles and limiting rapid innovation. Thermal management constraints and packaging complexity further restrict performance scaling in ultra-high-frequency applications.

Global renewable installations create sustained opportunity for medium- and high-voltage IGBTs in wind and solar inverters. In 2024, more than 320 GW of new renewable capacity required grid-tied converters using 1,700V IGBT modules. Offshore wind turbines now integrate over 250 IGBT chips per nacelle for pitch control and power conversion. Energy storage systems deploy multi-level IGBT inverters exceeding 2 MW per unit, opening demand for high-reliability, long-lifetime modules in utility-scale projects.

IGBT manufacturing faces rising complexity from tighter defect density targets and longer qualification cycles. Advanced trench devices require over 450 process steps, with yield losses exceeding 8% in early production ramps. Power module packaging now integrates double-sided cooling and sintered interconnects, increasing assembly cost by 22%. Regulatory compliance on lead-free and halogen-free materials further raises material qualification time and testing expenditure, slowing time-to-market for new platforms.

Shift Toward High-Voltage 1,700V Platforms: Adoption of 1,700V IGBTs increased by 29% between 2022 and 2024 as wind turbines above 8 MW became standard, reducing converter count by 18% per turbine.

Integration of Intelligent Power Modules: Over 46% of new industrial drives in 2024 used intelligent IGBT modules with embedded sensors, cutting field failure rates by 21%.

Advanced Packaging and Cooling: Double-sided cooled modules improved current density by 34% and reduced junction temperature swing by 26% in traction applications.

Localization of Fabrication Capacity: Regional fab investments grew 31% between 2021 and 2024, shortening supply lead times from 26 weeks to under 16 weeks for automotive-qualified devices.

The segmentation of the IGBT Power Semiconductors Market reflects clear differentiation across device types, application domains, and end-user industries, driven by voltage class requirements, thermal performance needs, and system integration depth. By type, segmentation is structured around discrete IGBTs, IGBT modules, and intelligent power modules, with adoption patterns closely linked to power density and reliability thresholds. By application, traction systems, renewable energy inverters, industrial motor drives, power supplies, and consumer power electronics define the core demand clusters, each with distinct switching frequency and voltage class profiles. End-user segmentation highlights automotive OEMs, industrial manufacturers, energy utilities, rail operators, and consumer electronics producers, where qualification cycles and lifecycle reliability heavily influence procurement. Across all segments, higher-voltage classes above 1,200V are gaining weight, while system-level integration is reshaping how value is distributed between discrete devices and module-based solutions.

IGBT modules represent the leading product type, accounting for approximately 54% of total adoption, driven by their high current handling, integrated protection features, and suitability for traction inverters and grid-scale converters. Discrete IGBTs follow with about 28% share, primarily used in low- to mid-power industrial drives and consumer power supplies. Intelligent power modules currently hold 18% share, benefiting from integrated sensing and gate control that reduces system-level design complexity.

While IGBT modules dominate in volume today, intelligent power modules are the fastest-growing type, expanding at an estimated 18.2% CAGR, supported by rising demand for compact inverters and predictive maintenance features in industrial automation. Discrete IGBTs continue to serve niche applications, with the combined share of remaining specialized packages and hybrid modules accounting for approximately 20% of installations.

• According to a 2025 industry technology audit, a national rail operator deployed next-generation 1,700V IGBT modules across 1,200 locomotives, reducing traction inverter failure rates by 23% within two years.

Traction and electric mobility applications lead the market with approximately 41% share, supported by widespread use of IGBTs in electric vehicle drivetrains, rail propulsion systems, and metro networks. Renewable energy inverters account for 26% of adoption, reflecting the expansion of wind and utility-scale solar installations. Industrial motor drives hold 21% share, while power supplies and consumer power electronics together represent 12% combined share.

Renewable energy inverters are the fastest-growing application, expanding at an estimated 17.6% CAGR, driven by high-voltage turbine converters and grid-forming inverters for energy storage. In 2025, more than 38% of industrial enterprises globally reported deploying high-efficiency IGBT drives to meet internal energy-reduction targets. In the automotive sector, over 45% of new EV platforms adopted 800V inverter architectures using advanced IGBT modules.

• According to a 2025 national energy agency deployment review, IGBT-based inverters were installed in more than 140 GW of new renewable capacity, improving grid conversion efficiency by 11% on average.

Automotive manufacturers form the leading end-user group with approximately 39% of total demand, reflecting the concentration of IGBT usage in traction inverters, onboard chargers, and auxiliary power units. Energy utilities follow with 24% share, driven by wind, solar, and grid-stabilization projects. Industrial manufacturers account for 22%, while rail operators and consumer electronics producers together represent 15% combined share.

Energy utilities are the fastest-growing end-user segment, expanding at an estimated 16.9% CAGR, supported by grid modernization and large-scale energy storage deployments. In 2025, more than 42% of utilities in developed markets reported upgrading medium-voltage converters with next-generation IGBT platforms. Among industrial users, over 58% of large factories adopted variable-frequency drives using high-reliability IGBT modules to cut motor energy consumption.

• According to a 2025 transport infrastructure assessment, a national rail authority modernized 320 substations with new IGBT converters, achieving a 19% reduction in traction energy losses across its network.

Asia Pacific accounted for the largest market share at 46.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

Asia Pacific’s dominance is supported by more than 1.2 billion IGBT devices shipped annually across China, Japan, and South Korea, with over 65% of global EV inverter production concentrated in this region. Europe held approximately 24.5% share in 2025, driven by rail electrification and renewable energy deployment exceeding 180 GW of installed wind capacity. North America accounted for 19.3% share, supported by over 14 million electric vehicles on the road and more than 55% adoption of high-efficiency industrial drives in new factories. South America and Middle East & Africa together represented 9.4% combined share, with grid modernization projects exceeding USD 35 billion in cumulative investment between 2021 and 2024.

North America holds approximately 19.3% of global IGBT adoption, supported by strong demand from electric vehicles, renewable energy, and industrial automation. Automotive electrification accounts for nearly 44% of regional device usage, while renewable inverters represent 27%. Federal clean-energy programs enabled installation of more than 95 GW of new solar and wind capacity between 2021 and 2024, directly increasing demand for 1,200V and 1,700V IGBT modules. Industrial digitalization led to over 52% of new motor drives integrating high-efficiency IGBTs. A leading local supplier expanded a 300-mm power device fab in Arizona, adding 120,000 wafers per year of IGBT capacity. Enterprise buyers show higher adoption in automotive, energy, and data center power systems, with over 48% of utilities prioritizing next-generation grid converters.

Europe accounts for approximately 24.5% of global demand, led by Germany, France, and the UK, which together contribute over 68% of regional consumption. Rail traction systems consume nearly 35% of European IGBT volumes, supported by more than 210,000 km of electrified rail lines. Sustainability directives pushed over 60% of new industrial inverters to meet higher efficiency classes. Germany alone operates more than 40 advanced power semiconductor fabs, producing high-voltage modules for wind turbines and metro systems. A major European manufacturer introduced double-sided cooled modules that reduced thermal losses by 22%. Buyers in this region show strong preference for certified, low-loss devices, with over 70% of utilities requiring lifecycle efficiency audits before procurement.

Asia-Pacific leads with 46.8% market share and the highest shipment volume globally. China, Japan, and South Korea together account for over 72% of global IGBT wafer starts. China alone operates more than 70 dedicated power semiconductor fabs, producing over 1.2 billion IGBT chips annually. EV traction inverters represent 49% of regional demand, while renewable energy systems contribute 31%. Japan remains a hub for advanced trench-gate design, with over 55% of patents in high-voltage IGBTs filed in this region. A major domestic supplier expanded 1,700V module capacity by 35% in 2024. Adoption is driven by manufacturing and mobility, with over 62% of industrial plants using variable-frequency drives.

South America represents approximately 6.1% of global demand, led by Brazil and Argentina, which together account for over 71% of regional consumption. Renewable energy inverters form 42% of installations, supported by more than 38 GW of wind and solar capacity added since 2020. Industrial motor drives contribute 34%, while rail and metro projects represent 14%. Government incentives in Brazil supported over 120 new grid substations using high-voltage IGBT converters. A regional integrator localized assembly of medium-voltage modules, cutting lead times by 28%. Buyers show preference for robust, long-life devices, with over 57% of utilities prioritizing extended warranty products.

Middle East & Africa accounts for approximately 3.3% of global demand, with the UAE, Saudi Arabia, and South Africa leading adoption. Oil & gas electrification and metro construction represent 46% of regional usage, while renewable projects contribute 29%. More than 22 GW of solar capacity installed since 2021 required high-power IGBT inverters. Smart grid programs led to over 18,000 new converter installations across substations. A regional engineering group deployed modular IGBT-based drives across 1,400 pumping stations. Buyers prioritize durability, with over 64% of utilities specifying high-temperature rated modules for desert environments.

China – 32.4% Market Share: Dominates through the largest global production capacity and extensive EV and renewable installations.

Japan – 14.6% Market Share: Leads in advanced device design, high-reliability manufacturing, and rail traction applications.

The competitive environment of the IGBT Power Semiconductors Market is both intense and strategically dynamic, featuring 20+ active global competitors spanning diversified product portfolios from basic discrete devices to high-voltage, multi-level power modules. The market remains moderately fragmented, but the top 5 companies together represent an estimated ~54–58% combined share of installed device volumes across automotive, industrial, and renewable applications, reflecting significant concentration among leading firms. Key players maintain differentiated positioning through strategic product launches, partnerships, and technology specialization in trench gate IGBTs, intelligent power modules, and high-voltage architectures. For instance, Infineon Technologies AG has expanded its portfolio with new-generation EDT3 and RC-IGBT devices for 400 V and 800 V electric drivetrain platforms achieving up to 20% lower total losses versus prior generations, enhancing automotive inverter performance in 2025.

Mitsubishi Electric Corporation initiated sample shipments of its LV100 1.2 kV IGBT module with ~15% reduced power loss and 1.5× higher current rating for solar and renewable systems in 2025, signaling elevated industrial use focus. Magnachip’s multi-year strategic partnership with Hyundai Mobis underscores industry collaboration to drive traction inverter innovations and broaden market reach across automotive, industrial, and AI-oriented segments. Competitive initiatives also include Infineon’s expansion of high-power discrete IGBTs up to 350 A nominal current, further indicating aggressive product development to capture ESS, UPS, and inverter demand.

Market participants continuously emphasize innovative design trends, such as intelligent modules with embedded sensors, optimized thermal management, and blended wide-bandgap hybrid solutions, shaping competitive differentiation and influencing procurement patterns among OEMs and system integrators globally.

STMicroelectronics N.V.

ON Semiconductor (onsemi)

Fuji Electric Co., Ltd.

Hitachi, Ltd.

ABB Ltd.

Danfoss Group

ROHM Co., Ltd.

Semikron (Semikron Danfoss)

Vincotech GmbH

Renesas Electronics Corporation

Magnachip Semiconductor

NXP Semiconductors

The IGBT Power Semiconductors Market is driven by continuous innovation in device architectures, packaging technologies, and material systems tailored for high-efficiency conversion and high-power reliability. Core technology trends include advanced trench-gate field-stop structures, which reduce conduction and switching losses while enhancing junction temperature tolerance, enabling devices rated from 600 V to multi-kV classes to reliably operate under high load and elevated thermal conditions. Integrated intelligent power modules (IPMs) are increasingly embedding on-chip sensors, gate drivers, and protection logic, reducing system complexity and enabling predictive diagnostics, which directly benefits industrial automation and large motor drive ecosystems. Moving beyond silicon, hybrid integration with wide-bandgap materials—such as silicon carbide (SiC) MOSFETs in combination with traditional IGBTs—improves overall system efficiency by delivering higher switching frequencies and lower losses, particularly in EV inverters and renewable energy converters. Continuous enhancements in thermal-management solutions, such as double-sided cooling and sintered interconnects, support higher current densities while extending operational lifetimes. Manufacturers are also optimizing package designs—from TO-247 and PressFIT modules to high-power press packs capable of handling up to 6.5 kV—for scalable deployment in grid infrastructure and heavy industrial segments. These advancements enable IGBTs to remain competitive against pure wide-bandgap substitutes by balancing cost-efficiency, performance, and robustness in diverse application domains.

• In March 2025, Magnachip Semiconductor Corporation launched two new Gen6 650 V IGBTs designed for solar inverters with polyimide insulation and integrated fast recovery diodes, yielding up to ~25% lower conduction loss and ~15% system efficiency gains in 15 kW configurations. Source: www.businesswire.com

• In early 2025, Infineon Technologies AG introduced a new generation of EDT3 and RC-IGBT devices for electric vehicle drivetrains that deliver up to 20% lower total losses in high-load conditions compared with previous product lines. Source: www.infineon.com

• Beginning February 2025, Mitsubishi Electric Corporation began shipping samples of its LV100 1.2 kV IGBT module for industrial and renewable power systems, achieving ~15% reduced power loss and a 1.5× higher current rating, improving inverter output power. Source: www.mitsubishielectric.com

• In 2025, a strategic 10-year partnership between Magnachip and Hyundai Mobis was announced to leverage advanced IGBT technologies for traction inverter mass production planned for 2026, expanding industrial and EV market penetration. Source: www.businesswire.com

The scope of the IGBT Power Semiconductors Market Report encompasses a comprehensive assessment of product segments, technological landscapes, geographic regions, and demand-side dynamics shaping industry strategies. It covers IGBT device categories—from discrete components and high-voltage modules to intelligent power modules (IPMs) integrated with advanced gate drivers and protection features—evaluating their technical attributes, reliability profiles, and deployment suitability across traction, renewable energy, industrial drives, uninterruptible power supplies, and power transmission infrastructures. The report analyzes segmentation by voltage classes, packaging formats, and end-user industries, highlighting performance thresholds and application demand gradients. Geographic coverage spans major regions including Asia Pacific, North America, Europe, South America, and Middle East & Africa, offering regional insights into production hubs, consumption trends, regulatory drivers, and infrastructure build-outs. The review also integrates technological trends such as trench-gate and field-stop device enhancements, intelligent sensing integration, thermal-management solutions, and co-packaged wide-bandgap innovations that influence competitive positioning and adoption patterns. Additionally, the report examines supply-chain configurations, strategic partnerships, and product pipelines that inform future investment decisions, making it a valuable resource for OEMs, power electronics integrators, and strategic planners seeking nuanced, data-driven insights into the evolving IGBT semiconductor ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,675.0 Million |

| Market Revenue (2033) | USD 5,304.8 Million |

| CAGR (2026–2033) | 15.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Infineon Technologies, Mitsubishi Electric, STMicroelectronics, ON Semiconductor (onsemi), Fuji Electric, ROHM Semiconductor, Renesas Electronics, Hitachi, ABB, Danfoss, Semikron Danfoss, Vincotech, Magnachip Semiconductor, Texas Instruments, NXP Semiconductors |

| Customization & Pricing | Available on Request (10% Customization Free) |