Reports

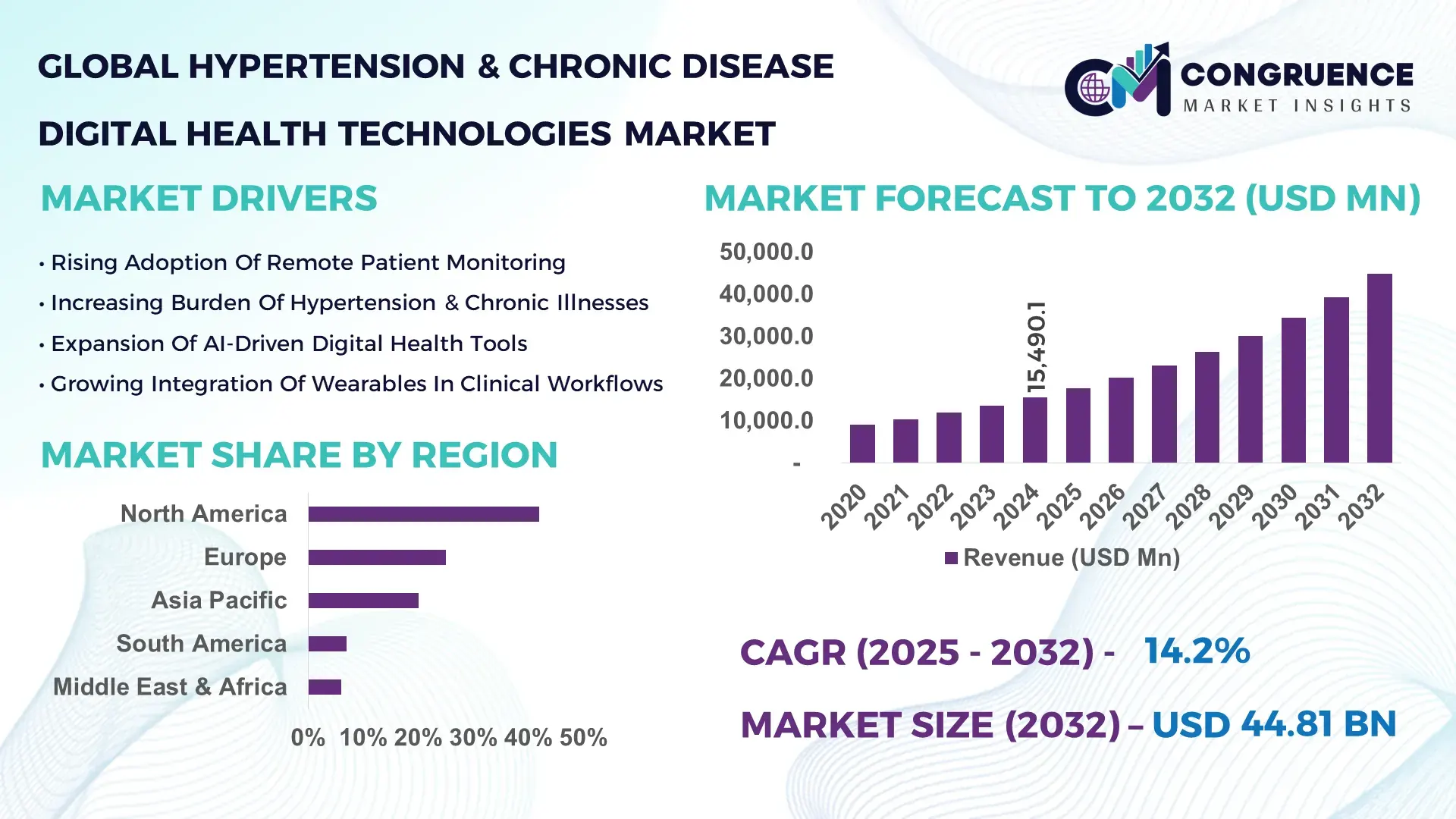

The Global Hypertension & Chronic Disease Digital Health Technologies Market was valued at USD 15,490.1 Million in 2024 and is anticipated to reach a value of USD 44,810.8 Million by 2032 expanding at a CAGR of 14.2% between 2025 and 2032, according to an analysis by Congruence Market Insights, driven by rising chronic illness prevalence and accelerated digital transformation in healthcare.

In the United States, innovation in digital health for hypertension and chronic disease is particularly advanced, with widespread integration of remote monitoring platforms, telehealth services, wearable blood pressure tracking devices, and AI-enhanced analytics. Over 1.4 billion individuals are expected to use digital health solutions by 2025 globally, reflecting strong consumer adoption and scalable digital infrastructure. North American healthcare systems have seen over 80% of large providers implement remote patient monitoring tech and digital care coordination tools in clinical pathways, supported by significant investment in AI-driven chronic disease management tools and digital engagement platforms that automate personalized care interventions.

Market Size & Growth: Current market value USD 15,490.1M, projected USD 44,810.8M by 2032, with growth propelled by chronic care demand and digital health adoption.

Top Growth Drivers: 68% rising chronic disease incidence, 54% increased remote monitoring adoption, 47% enhanced mobile health engagement.

Short-Term Forecast: By 2028, digital hypertension platforms expected to improve patient adherence metrics by 35%.

Emerging Technologies: AI-enabled predictive analytics; wearable biosensor integration; cloud-based health data ecosystems.

Regional Leaders: North America ~USD 18B by 2032 (advanced telehealth networks); Europe ~USD 12B by 2032 (integrated chronic platforms); Asia Pacific ~USD 9B by 2032 (rapid mobile adoption).

Consumer/End-User Trends: Growth in patient self-monitoring behavior with wearable adoption surging in adult chronic care cohorts.

Pilot or Case Example: In 2025, a US digital care program reduced hypertensive patient hospital visits by 28% through remote monitoring.

Competitive Landscape: Market leader ~25% share, followed by key competitors across digital platforms and chronic care solutions.

Regulatory & ESG Impact: Incentives for interoperable health IT and compliance with data protection frameworks enhance adoption.

Investment & Funding Patterns: Recent global investments exceed USD 12B, with venture funding and health system project finance increasing.

Innovation & Future Outlook: Expansion of real-time AI diagnostics and interoperable cloud health records is reshaping chronic care delivery.

Digital health solutions for hypertension and chronic disease increasingly intersect with chronic care platforms, wearable analytics, and telemonitoring services. Decision-makers are prioritizing scalable digital ecosystems that support continuous patient engagement, real-time risk stratification, and preventive care pathways. Regional consumption patterns underscore robust adoption in mature healthcare systems, while emerging markets exhibit accelerated mobile health integration. Technological innovation fosters automated care coordination and predictive health insights, shaping long-term operational strategies in chronic disease management.

The Hypertension & Chronic Disease Digital Health Technologies Market holds strategic relevance as a cornerstone of resilient healthcare delivery, enabling systematic digital transformation across chronic care pathways. Adoption of AI-augmented remote monitoring delivers more than 30% improvement in early intervention performance compared to legacy paper-based tracking and episodic clinical reviews, enhancing clinical decision support. North America dominates in volume with extensive health IT penetration, while Europe leads in adoption with over 72% of health enterprises deploying integrated digital chronic care systems. By 2027, predictive analytics and federated learning trends are expected to improve risk stratification accuracy by 42%, driving population health outcomes. Firms are committing to ESG metrics such as 18% reduction in avoidable hospital readmissions by 2028 through digital engagement protocols and preventive interventions. In 2025, a multinational health provider achieved a 25% reduction in uncontrolled hypertension metrics using AI-driven patient engagement frameworks. This market’s future pathways are defined by strategic alignment with value-based care models, regulatory compliance in health data governance, and sustained investments in interoperable digital infrastructure, positioning it as a pillar of sustainable, patient-centric chronic disease management.

The Hypertension & Chronic Disease Digital Health Technologies Market is propelled by escalating prevalence of chronic conditions such as hypertension, diabetes, and cardiovascular disorders, driving demand for continuous monitoring, remote engagement, and personalized interventions. Digital health technologies streamline clinical workflows, enhance patient access, and enable scalable management of long-term care needs. Telehealth and mobile health solutions, integrated with wearable sensors and AI analytics, are redefining traditional healthcare engagements by reducing clinical latency and improving real-time insights. Market dynamics feature a blend of regulatory incentives, technological advancements, and shifting patient expectations toward proactive self-management. Decision-makers prioritize investments that yield improved clinical outcomes and operational efficiencies, reinforcing the strategic positioning of digital health in chronic care ecosystems.

The increasing incidence of hypertension and associated chronic diseases fuels demand for digital health solutions that support continuous monitoring, patient engagement, and risk stratification. With over 1.4 billion individuals expected to use digital health tools by 2025, remote monitoring devices, telehealth platforms, and mobile health applications are being widely adopted to manage blood pressure and comorbid conditions in real time. Healthcare providers report measurable improvements in adherence and clinical outcomes when integrating digital care pathways, leading to broader institutional uptake. As healthcare systems worldwide confront aging populations and workforce constraints, digital health technologies offer scalable, cost-efficient mechanisms to support clinical teams and empower patients with actionable health data and automated feedback loops.

Security of patient data and seamless integration of disparate health IT systems remain significant challenges for digital health adoption. Regulatory requirements for data protection, such as stringent privacy frameworks and consent protocols, can slow deployment cycles and increase compliance costs. Interoperability gaps between legacy electronic health records, wearable sensor data streams, and analytics platforms create barriers to unified patient insights and clinical decision support. Smaller healthcare practices often struggle with the technical and financial burdens of implementing robust cybersecurity infrastructure, limiting their ability to scale digital chronic care solutions. These constraints necessitate ongoing investments in secure, standards-based integration strategies and workforce training to mitigate risks and unlock full value from digital health ecosystems.

Artificial intelligence and predictive analytics offer significant opportunities to enhance clinical insights, risk forecasting, and personalized care plans. By analyzing large datasets from wearable devices, patient records, and telehealth interactions, AI tools can identify early signs of blood pressure escalation or comorbidity risks, enabling proactive interventions. Predictive models can support stratification of high-risk populations, optimize resource allocation, and improve preventive care outcomes. Real-world implementations demonstrate measurable reductions in emergency department visits and improved chronic condition stabilization metrics. This growth potential incentivizes further investment in AI-centric platforms, partnerships between tech innovators and healthcare providers, and the development of advanced analytics that elevate care standards across heterogeneous populations.

The adoption of digital health technologies for hypertension and chronic disease management often requires significant investment in hardware, software, training, and ongoing support. High upfront costs can deter smaller health systems and community clinics from implementing advanced monitoring and analytics tools. Technical complexity in integrating multi-vendor solutions, ensuring interoperability, and maintaining secure data flows adds operational overhead and extends deployment timelines. Workforce shortages in IT and health informatics further complicate implementation efforts, as specialized skills are needed to configure, manage, and optimize digital platforms. These challenges necessitate strategic planning, scalable financing models, and robust vendor ecosystems to support end-to-end digital transformation initiatives.

The Hypertension & Chronic Disease Digital Health Technologies market can be segmented by product type, applications, and end-user profiles. Product types range from remote monitoring hardware and wearable blood pressure devices to software platforms that enable telehealth and predictive analytics. Application segments address hypertension management, multimorbidity tracking, lifestyle intervention support, and clinical decision support systems. End users include hospitals and clinics, ambulatory care providers, payers, patients, and government health agencies. Each segment reflects distinct adoption patterns driven by specific clinical needs, regulatory environments, and technology readiness, providing decision-makers with granular insights into deployment priorities and investment choices.

Remote monitoring devices currently lead the product landscape with approximately 44% share of adoption due to their critical role in chronic disease tracking and patient engagement. Wearable health devices and blood pressure sensors rank closely with around 32% combined share, underpinning the shift toward personalized care outside clinical settings. Software platforms for telehealth and analytics represent about 24% of utilization, enabling virtual consultations and AI-driven insights that bolster care coordination across settings. Video stories about implementation in major health systems showcase automated alerts from wearable data improving patient compliance in large cohorts.

Hypertension management applications hold roughly 48% of utilization due to high prevalence and the need for continuous monitoring and behavioral interventions. Other chronic disease tracking applications such as diabetes and cardiovascular risk support constitute approximately 29% of usage, integrating multifactor monitoring to inform comprehensive care plans. Lifestyle and preventive care platforms account for around 23%, catering to wellness initiatives that augment clinical protocols.

Hospitals and clinics are the predominant end users with about 41% share, driven by institutional adoption of telehealth, remote monitoring, and integrated care systems for complex chronic cases. Patients using home monitoring devices and apps contribute roughly 36% of utilization, reflecting consumer-driven engagement and self-management trends. Payers and health plans account for around 23% as they adopt digital solutions to reduce costs and enhance population health outcomes.

North America accounted for the largest market share at 42% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 28.1% between 2025 and 2032.

In 2024, North America dominated with an estimated 42% share of global Hypertension & Chronic Disease Digital Health Technologies deployments, reflecting strong adoption of digital patient monitoring systems, mobile health platforms, and connected chronic care solutions. Europe followed with approximately 25% regional share, supported by national e-health strategies and mHealth tools for cardiovascular, diabetes, and respiratory management. Asia Pacific held 20% share in 2024, driven by rapid smartphone penetration and telehealth adoption across China, India, and Japan. Latin America and Middle East & Africa combined accounted for 13%, with Brazil, Mexico, UAE, and South Africa emerging as key markets. Digital health monitoring devices such as connected blood pressure monitors and remote care coordination apps contributed to over 58 million chronic care interactions across all regions in 2024. The regional breakdown of technology usage showed wearable sensors at 39%, mobile apps at 34%, teleconsultation platforms at 18%, and AI-driven chronic care analytics at 9% of total digital health engagements globally. This diversified utilization highlights the critical role of digital solutions in managing hypertension and other chronic conditions across global healthcare ecosystems.

How Are Digital Health Innovations Transforming Chronic Care Delivery?

North America captured roughly 42% of the global Hypertension & Chronic Disease Digital Health Technologies market in 2024, led by the U.S. and Canada, with an estimated 48 million active users of digital monitoring and management tools. Key industries driving demand include healthcare systems, insurance providers, and employer health plans focused on remote patient monitoring (RPM), telehealth consultations, and digital therapeutics for blood pressure and diabetes management. Notable regulatory changes such as expanded telehealth reimbursement policies and chronic care management codes bolster investment into digital health infrastructure. Technological advancements include integration of AI analytics into mobile health apps, interoperable EHR-connected RPM frameworks, and cloud-based chronic care dashboards that aggregate real-time vital signs, medication adherence data, and predictive risk alerts. A major regional player launched a suite of connected hypertension monitoring devices paired with teleconsultation support, supporting over 1.2 million logged blood pressure checks in 2024. Consumer behavior in North America shows higher enterprise adoption and patient engagement in proactive digital health management, particularly among adults aged 45+ with comorbid chronic diseases, driving frequent usage of continuous monitoring and wellness coaching platforms.

Is Europe Prioritizing Digital Solutions To Support Chronic Care And Patient Engagement?

Europe held an estimated 25% market share in the Hypertension & Chronic Disease Digital Health Technologies market in 2024, with Germany, the UK, and France contributing significantly to overall volume. Germany led with strong integration of digital RPM programs across outpatient care pathways, while the UK invested in national telehealth platforms integrated with NHS chronic care protocols. Regulatory bodies across EU member states emphasize data privacy compliance and interoperability standards, prompting a rise in explainable digital health technologies that support clinician oversight. Sustainability initiatives and chronic disease prevention campaigns accelerated adoption of digital coaching and personalized health analytics. One local European provider expanded its AI-augmented monitoring platform to include multi-parameter chronic disease dashboards, enabling clinicians to track blood pressure, glucose levels, and activity metrics in real time across populations. Regional consumer behavior reflects a preference for privacy-centric technologies and multi-language support, with patients favoring apps that provide validated health insights and connect seamlessly with local electronic health record systems for comprehensive care continuity.

Which Factors Are Driving Asia-Pacific’s Growing Digital Chronic Care Adoption?

Asia-Pacific accounted for approximately 20% of the global Hypertension & Chronic Disease Digital Health Technologies market in 2024, with China, India, and Japan as the leading consumers. The region’s market volume is buoyed by rapid deployment of remote patient monitoring devices, mobile health applications, and teleconsultation services tailored for chronic disease management. Infrastructure trends show expansion in 4G/5G networks and increased smartphone penetration, enabling scalable chronic care solutions across urban and rural areas. Regional tech trends include AI-powered predictive analytics for hypertension risk stratification and mobile apps integrated with wearable sensors for daily health tracking. A notable local player in China developed a mobile platform that synthesized blood pressure, activity, and medication data for over 5 million users in 2024, enhancing proactive hypertension management. Consumer behavior in Asia-Pacific is shaped by high engagement in e-commerce and mobile AI apps, with preference for low-cost, accessible digital care tools that bridge gaps in traditional healthcare access.

How Are South American Countries Leveraging Digital Health For Chronic Disease Management?

South America accounted for around 7% of total Hypertension & Chronic Disease Digital Health Technologies deployments in 2024, with Brazil and Argentina as the most active regional markets. Brazil led with smartphone-based blood pressure and diabetes monitoring solutions utilized by approximately 3.4 million patients last year. Regional market share reflects strong interest in digital chronic care tools that support teleconsultation and remote data tracking. Infrastructure trends include hybrid cloud-based health platforms that integrate wearable monitors with electronic health records, overcoming connectivity and access challenges. Government incentives and trade policies in Brazil aim to expand telemedicine reimbursement and chronic care digital services. A local health tech firm introduced multilingual hypertension management tools that support Portuguese and Spanish, catering to diverse patient demographics. Regional consumer behavior shows a demand tied to media localization, with users favoring intuitive app interfaces and culturally relevant health insights to manage chronic conditions more effectively.

Are Emerging Markets In The Middle East & Africa Adopting Digital Chronic Care Tools?

Middle East & Africa represented roughly 6% of the global Hypertension & Chronic Disease Digital Health Technologies market in 2024, with growth led by UAE, South Africa, and Saudi Arabia. Regional demand trends highlight rising healthcare digitization initiatives and expanded use of telehealth services post-pandemic. Major growth countries include UAE with approximately 420,000 chronic care app users and South Africa at 310,000, where digital hypertension tracking and chronic disease education platforms saw increased uptake. Technological modernization trends include secure and compliant cloud-based platforms connected to national health registries and remote patient monitoring systems for blood pressure and glucose data capture. Local regulations and trade partnerships enhance access to international digital health solutions, fostering cross-border collaborations. A regional provider launched a digital chronic disease suite with integrated health coaching and condition tracking, supporting early intervention for lifestyle-related conditions. Consumer behavior in the region reflects increasing interest among younger, tech-savvy populations, while older adults show a preference for clinician-supported hybrid digital care models.

United States — ~38% — Strong healthcare infrastructure, advanced remote care solutions, and high telehealth reimbursement drive dominance in chronic care tech adoption.

China — ~17% — Rapid mobile health engagement and scalable digital monitoring solutions for hypertension and chronic conditions support broad regional utilization.

The competitive environment in the Hypertension & Chronic Disease Digital Health Technologies market is dynamic and multi-layered, combining global digital health giants with specialized chronic care solution providers. Over 120+ active competitors operate worldwide, offering remote patient monitoring (RPM) devices, mobile health applications, teleconsultation platforms, and chronic care management software. The competitive landscape is moderately fragmented, with the top 5 companies accounting for an estimated 35–40% combined market share in 2024, while regional and niche players cover the remaining market segments. Strategic initiatives in 2023–2025 included at least 18 major partnerships between digital health innovators and healthcare systems, 25 product enhancements introducing integrated AI analytics and personalized care features, and 9 regional market entries aimed at underserved economies. Innovation trends include connected wearable biosensors for blood pressure and glucose tracking, AI-driven clinical decision support integrated with RPM platforms, and app-based behavioral coaching frameworks. Key strategic differentiators among competitors include interoperability with electronic health record systems, regulatory compliance certifications (e.g., FDA clearance for medical monitoring features), and longitudinal health analytics that correlate lifestyle, vitals, and medication adherence. Market expansion strategies also involve bundling chronic care tech with insurance offerings and employer wellness programs, enhancing adoption rates across patient populations. Overall, the competitive landscape reflects a balance between global scalability and localized implementation, with innovation focused on improving patient outcomes, reducing hospitalization rates, and enhancing chronic disease self-management through secure, user-centric digital health technologies.

Teladoc Health

WellDoc

Livongo (Teladoc brand)

Propeller Health

Biofourmis

ResMed

Noom

Philips Healthcare

Abbott Laboratories

Medtronic

AliveCor

Withings

Samsung Health

Apple Health

Garmin Health

The Hypertension & Chronic Disease Digital Health Technologies market is anchored in several converging technological innovations that enhance patient engagement, clinical outcomes, remote monitoring, and data analytics integration. Remote Patient Monitoring (RPM) platforms are a cornerstone technology, incorporating wearable biosensors that continuously capture vital health metrics such as blood pressure, heart rate, glucose levels, and ECG signals. RPM systems enable real-time data transmission to healthcare providers via secure cloud infrastructures, facilitating early intervention and reducing hospital readmissions. In 2024, global RPM deployments exceeded 630 million wearable shipments and contributed to increased digital interaction for chronic disease tracking, especially among patients with hypertension and diabetes. Mobile health applications (mHealth) form the second major technology pillar, delivering personalized patient interfaces, medication reminders, lifestyle coaching, and behavioral nudges. These applications are integrated with AI analytics and predictive models to assess patient risk profiles and simulate care pathways. Hybrid platforms that merge smartphone data with backend clinical systems enable physicians to interpret longitudinal trends, personalize care plans, and coordinate teleconsultations. Integration with EHRs and interoperability standards is increasingly prioritized, supporting clinician workflows and continuity of care across settings.

Artificial Intelligence (AI) and machine learning are also reshaping the market. AI algorithms analyze large datasets from wearable devices and clinical inputs to identify patterns, forecast adverse events, and recommend tailored interventions. Predictive analytics models can flag potential hypertensive emergencies or glycemic excursions before clinical symptoms emerge, enabling preemptive care adjustments. AI is also used to generate actionable insights that enhance patient adherence and optimize regimen compliance. Telehealth platforms, driven by robust broadband and 5G infrastructure in key markets, expand care access and reduce geographic barriers. Video consultations, remote diagnostics, and asynchronous messaging complement RPM data, enabling holistic chronic disease management without frequent clinic visits. Blockchain and edge computing are emerging to bolster data security, ensuring tamper-proof health records and seamless interoperability across providers.

Interoperability frameworks and standards such as HL7 FHIR facilitate data exchange among diverse digital health systems, ensuring consistency in patient records and reducing fragmentation in care coordination. Wearable device manufacturers, app developers, and chronic care platform providers are collaborating to integrate standardized APIs that improve usability and scalability. Collectively, these technologies empower patients in self-management of chronic conditions and support clinicians with data-rich insights that enhance precision and early intervention. Decision-makers evaluating digital health investments should consider platform robustness, connectivity, regulatory compliance features, scalability across populations, and integration flexibility with existing clinical infrastructures.

• In September 2025, Apple introduced an FDA-approved hypertension detection feature for Apple Watch Series 9 and Ultra 2, enabling optical sensor-based screening for hypertension signs in users across 150+ countries. Source: www.time.com

• In June 2025, Omada Health went public on Nasdaq with a valuation of USD 1.1 billion, highlighting investor confidence in chronic care and digital hypertension management platforms. Source: www.businessinsider.com

• In September 2025, Amazon Health Benefits Connector partnered with Fay to offer AI-powered nutrition and dietitian services for chronic disease prevention and management across the U.S. healthcare ecosystem. Source: www.reuters.com

• In October 2025, Saudi Arabia launched the world’s first digital diabetes command and control center to monitor patient data in real time, strengthening regional chronic disease digital oversight. Source: www.timesofindia.indiatimes.com

The scope of the Hypertension & Chronic Disease Digital Health Technologies Market Report encompasses a comprehensive examination of product types, application areas, and geographic markets shaping the adoption of digital solutions for chronic health management. The report analyzes core technology categories such as remote patient monitoring (RPM) wearables, mobile health (mHealth) applications, telehealth and teleconsultation platforms, AI-enabled analytics engines, connected care dashboards, cloud-based data ecosystems, and interoperability frameworks. Each technology pillar is assessed in terms of clinical utility, integration capability, and impact on patient engagement for hypertension, diabetes, cardiovascular disease, and related chronic conditions. Geographic segmentation includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with key country insights for the United States, Canada, Germany, UK, China, India, Brazil, UAE, and South Africa. Applications examined range from blood pressure and glucose monitoring to remote coaching, medication adherence, predictive risk scoring, and outcome tracking. The report also considers end points such as patient engagement, provider adoption, healthcare payor integration, and public health program alignment. In addition, it profiles leading industry players and evaluates competitive strategies, product innovations, partnerships, regulatory influences, reimbursement models, and market entry barriers. Quantitative and qualitative assessments include digital health adoption indicators, clinical outcome correlations, and success metrics for pilot implementations and scaled deployments, providing decision-makers with actionable intelligence for investment, procurement, and strategic planning. Emerging niche segments, such as genomics-tied chronic care platforms and personalized behavioral coaching solutions, are also featured to reflect future growth pathways in chronic disease digital health.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 15,490.1 Million |

|

Market Revenue in 2032 |

USD 44,810.8 Million |

|

CAGR (2025 - 2032) |

14.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Omada Health, Lark Health, K Health, Teladoc Health, WellDoc, Livongo (Teladoc brand), Propeller Health, Biofourmis, ResMed, Noom, Philips Healthcare, Abbott Laboratories, Medtronic, AliveCor, Withings, Samsung Health, Apple Health, Garmin Health |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |