Reports

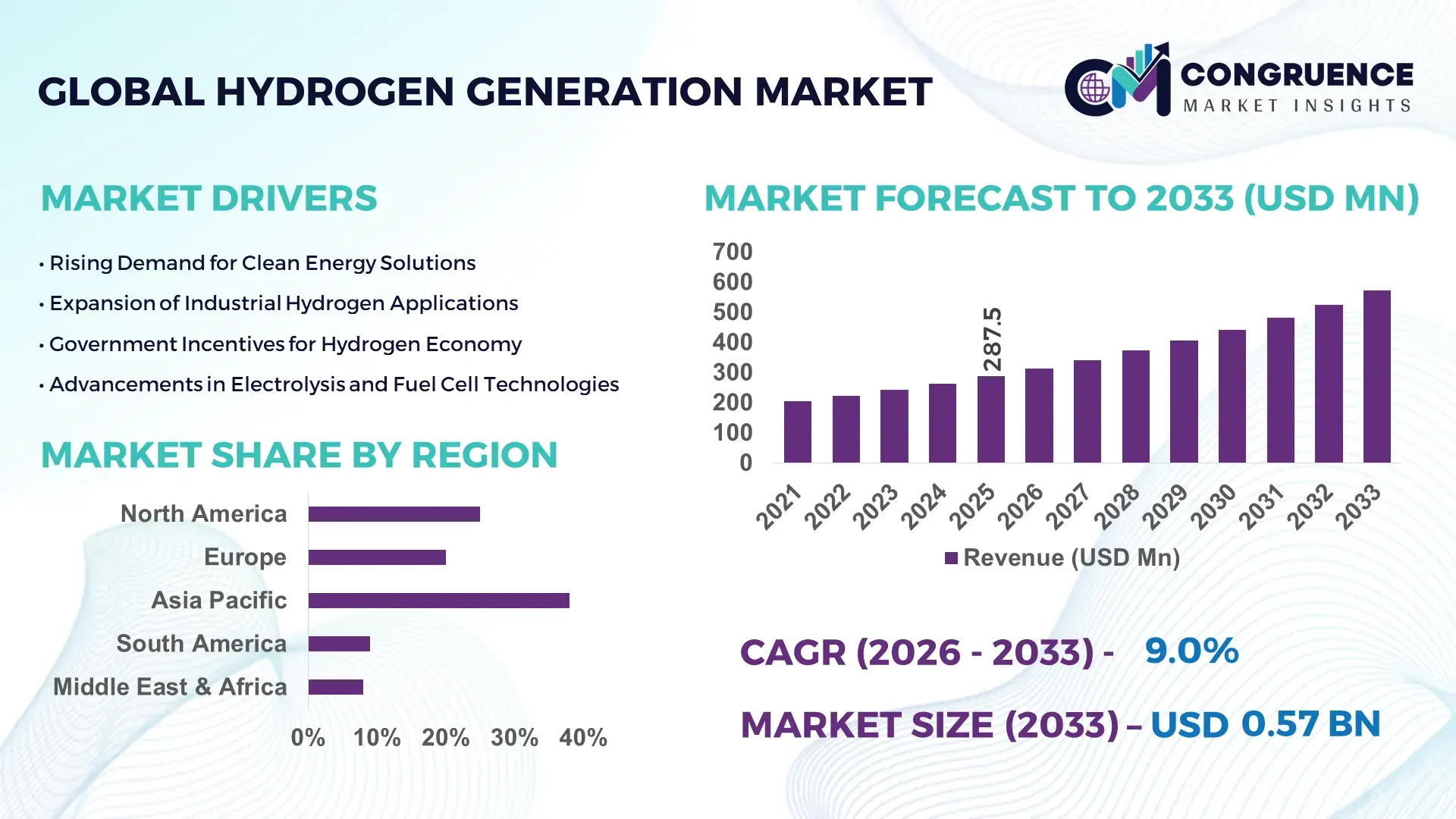

The Global Hydrogen Generation Market was valued at USD 287.52 Million in 2025 and is anticipated to reach a value of USD 572.9 Million by 2033 expanding at a CAGR of 9% between 2026 and 2033. Growth is supported by rising clean energy investments, industrial decarbonization initiatives, and increasing deployment of hydrogen across refining, chemicals, and power applications.

China represents the most influential country within the hydrogen generation landscape, driven by large-scale industrial demand and rapid infrastructure expansion. The country produces over 33 million metric tons of hydrogen annually, primarily for ammonia synthesis, petroleum refining, and methanol production. Public and private investments exceeded USD 6.7 billion in hydrogen-related projects during 2024, with more than 120 green hydrogen pilot projects announced. China has also commissioned electrolysis capacity exceeding 1.2 GW, supported by advances in alkaline and PEM electrolyzer manufacturing, and increasing integration of hydrogen into steelmaking, mobility, and grid-scale energy storage applications.

Market Size & Growth: Valued at USD 287.52 Million in 2025, projected to reach USD 572.9 Million by 2033, growing at a CAGR of 9%, driven by industrial decarbonization and clean fuel substitution initiatives.

Top Growth Drivers: Industrial hydrogen demand up by 18%, electrolyzer efficiency improvement of 22%, renewable-powered hydrogen adoption growth of 27%.

Short-Term Forecast: By 2028, average hydrogen production costs are expected to decline by 19% due to scale-up of electrolyzer manufacturing and renewable energy integration.

Emerging Technologies: High-efficiency PEM electrolysis, solid oxide electrolysis systems, and AI-enabled hydrogen production optimization platforms.

Regional Leaders: Asia-Pacific projected at USD 228 Million by 2033 with industrial hydrogen clusters; Europe at USD 176 Million driven by green hydrogen mandates; North America at USD 142 Million supported by clean hydrogen incentives.

Consumer/End-User Trends: Refining and chemicals account for over 48% of consumption, while mobility and power applications show adoption growth above 20% annually.

Pilot or Case Example: A 2025 green hydrogen pilot in industrial gas production achieved a 17% reduction in energy consumption per unit output.

Competitive Landscape: Leading player holds approximately 24% share, followed by four major competitors collectively accounting for nearly 45% of installed capacity.

Regulatory & ESG Impact: Clean hydrogen tax credits, carbon pricing mechanisms, and national hydrogen roadmaps are accelerating low-emission hydrogen deployment.

Investment & Funding Patterns: Over USD 9.4 Billion invested globally during 2024–2025, with strong growth in project finance and public–private partnerships.

Innovation & Future Outlook: Integration of hydrogen with renewable power, storage systems, and industrial heat applications is shaping next-generation hydrogen ecosystems.

The Hydrogen Generation Market is primarily supported by refining, ammonia production, methanol synthesis, and emerging steel decarbonization applications, which together contribute over 70% of total demand. Technological innovations such as higher-capacity electrolyzers, modular hydrogen plants, and renewable-powered electrolysis are improving cost efficiency and scalability. Regulatory frameworks promoting low-carbon fuels, emissions reduction targets, and clean energy subsidies continue to stimulate adoption. Asia-Pacific leads consumption growth due to industrial expansion, while Europe focuses on green hydrogen transition. Future outlook remains positive, with increased cross-sector integration, export-oriented hydrogen hubs, and accelerated commercialization of advanced electrolysis technologies.

The Hydrogen Generation Market holds growing strategic relevance as governments and industries align energy systems with decarbonization, energy security, and industrial resilience objectives. Hydrogen is increasingly positioned as a cross-sector enabler for refining, chemicals, steel, power generation, and long-duration energy storage. From a strategy standpoint, investments are shifting from captive gray hydrogen toward scalable green and low-carbon hydrogen systems integrated with renewable power assets. Proton Exchange Membrane (PEM) electrolysis delivers 28% efficiency improvement compared to conventional steam methane reforming-based captive hydrogen units, strengthening its commercial viability for industrial users seeking lower emissions and operational flexibility.

Regionally, Asia-Pacific dominates in volume due to extensive industrial consumption, while Europe leads in adoption with nearly 42% of large industrial enterprises integrating hydrogen into decarbonization roadmaps. By 2028, AI-enabled electrolyzer optimization and predictive maintenance platforms are expected to improve electrolyzer uptime by 21% and reduce operational downtime across large hydrogen plants. From an ESG perspective, firms are committing to emissions intensity improvements such as 30% lifecycle carbon reduction in hydrogen production by 2030 through renewable sourcing and process electrification.

In 2025, a national-scale green hydrogen initiative in Japan achieved a 19% reduction in production energy intensity through advanced electrolyzer control systems and grid-balancing algorithms. Looking forward, the Hydrogen Generation Market is positioned as a pillar of energy resilience, regulatory compliance, and sustainable industrial growth, supporting long-term competitiveness across energy-intensive sectors.

Industrial decarbonization mandates are a primary driver of the Hydrogen Generation Market, particularly in refining, ammonia, methanol, and steel manufacturing. Heavy industries account for over 55% of global hydrogen consumption, with a growing shift toward low-emission hydrogen to meet tightening emissions thresholds. Carbon pricing mechanisms exceeding USD 80 per metric ton in several regions are incentivizing industries to replace fossil-based hydrogen. Additionally, renewable electricity penetration above 30% in key industrial regions is enabling cost-competitive green hydrogen production. As industries prioritize Scope 1 and Scope 2 emissions reductions, hydrogen generation systems are increasingly embedded into long-term operational strategies.

Despite technological progress, high capital expenditure for electrolyzers, power electronics, and balance-of-plant systems remains a major restraint. Large-scale electrolyzer installations require substantial upfront investment, while electricity costs can represent more than 60% of total hydrogen production expenses. Grid constraints, limited access to low-cost renewable power, and regional electricity price volatility affect project economics. Additionally, insufficient hydrogen transport and storage infrastructure increases reliance on localized production, limiting scalability. These cost-related barriers slow adoption among small and mid-sized industrial users and delay broader commercialization timelines.

Rapid expansion of renewable energy capacity presents significant opportunities for the Hydrogen Generation Market. Global installed renewable power capacity additions exceeded 400 GW in recent years, creating surplus electricity during off-peak periods. Hydrogen generation offers a pathway to monetize excess renewable energy through power-to-gas conversion. Co-locating electrolyzers with solar and wind assets reduces curtailment and improves asset utilization. Emerging hydrogen hubs and industrial clusters further support shared infrastructure and cost efficiencies. These developments open new opportunities for export-oriented hydrogen production and long-term energy storage solutions.

Regulatory inconsistency and lack of standardized hydrogen certification frameworks pose ongoing challenges. Definitions of green, blue, and low-carbon hydrogen vary across jurisdictions, complicating cross-border trade and investment decisions. Permitting timelines for hydrogen facilities can extend beyond 24 months, delaying project execution. Safety regulations, grid interconnection standards, and transport codes are still evolving in many regions. These uncertainties increase compliance costs and risk premiums for developers, underscoring the need for harmonized standards and clearer policy signals to support sustained market growth.

Rapid Shift Toward Modular and Prefabricated Hydrogen Plants Improving Deployment Efficiency

The adoption of modular and prefabricated construction is reshaping demand dynamics in the Hydrogen Generation market. Nearly 55% of newly announced hydrogen generation projects report measurable cost advantages through modular construction approaches. Off-site prefabrication of electrolysis skids, piping systems, and power units has reduced on-site labor requirements by approximately 32% and shortened average project timelines by 25%. In Europe and North America, where labor costs are high, modular hydrogen systems are increasingly preferred for industrial and distributed generation applications, driving higher demand for precision-manufactured components and factory-assembled electrolyzer units.

Accelerated Integration of Renewable Energy With Hydrogen Generation Systems

Hydrogen generation facilities are increasingly being co-located with renewable energy assets to optimize power utilization and reduce grid dependency. Over 48% of new hydrogen projects now integrate direct solar or wind power inputs, enabling electricity cost reductions of up to 20% at the production level. Curtailment recovery rates exceeding 18% are being achieved by converting surplus renewable electricity into hydrogen during low-demand periods. This trend is particularly pronounced in regions with renewable penetration above 35%, where hydrogen acts as a balancing and storage mechanism for intermittent power generation.

Digitalization and AI-Based Optimization Enhancing Operational Performance

Digital monitoring and AI-driven optimization tools are becoming standard across large-scale hydrogen generation facilities. More than 40% of operational plants have implemented predictive maintenance platforms, resulting in electrolyzer uptime improvements of nearly 22%. AI-enabled process control systems are also improving energy efficiency by approximately 15% through real-time load balancing and degradation monitoring. These technologies are reducing unplanned downtime by up to 28% while extending electrolyzer stack life, improving long-term asset performance and cost predictability for operators.

Rising Adoption of Hydrogen in Hard-to-Abate Industrial Applications

Hydrogen usage is expanding beyond traditional refining and ammonia production into steelmaking, high-temperature industrial heating, and backup power systems. Industrial pilots indicate hydrogen substitution rates of 20%–35% in direct reduced iron processes, significantly lowering fossil fuel dependency. In heavy manufacturing, hydrogen-based burners are achieving thermal efficiency gains of nearly 12% compared to conventional systems. This trend reflects growing confidence in hydrogen as a scalable industrial fuel, supported by improvements in supply reliability and on-site generation capabilities.

The Hydrogen Generation market is segmented by type, application, and end-user, reflecting differences in production pathways, usage intensity, and adoption maturity across industries. By type, the market spans conventional fossil-based hydrogen, low-carbon hydrogen with carbon capture, and renewable-powered hydrogen systems, each serving distinct regulatory and operational requirements. Application-wise, hydrogen is primarily consumed in refining and chemical synthesis, while emerging use cases such as power generation, mobility, and energy storage are expanding rapidly. End-user segmentation highlights strong industrial concentration, alongside growing participation from utilities, transportation operators, and public-sector entities. These segments collectively illustrate how hydrogen generation is transitioning from a traditional industrial input to a multi-sector energy vector, supported by technology evolution, policy alignment, and changing end-user priorities.

Conventional fossil-based hydrogen, commonly produced via steam methane reforming without carbon capture, remains the leading type and accounts for approximately 46% of total hydrogen generation adoption due to its established infrastructure and consistent output for large industrial users. Low-carbon hydrogen with carbon capture systems represents about 28% of adoption, driven by compliance-oriented industries seeking emissions reduction without full process electrification. However, renewable-powered green hydrogen is the fastest-growing type, expanding at an estimated CAGR of 32%, supported by falling renewable electricity costs and electrolyzer efficiency gains. Green hydrogen currently holds around 18% of adoption but is rapidly scaling through industrial pilots and large electrolyzer installations. Other niche production methods, including biomass-based and byproduct hydrogen recovery, collectively contribute the remaining 8%, serving localized or specialized applications.

Petroleum refining is the dominant application, accounting for nearly 39% of hydrogen usage, as hydrogen is critical for desulfurization and fuel upgrading processes. Ammonia and methanol production together represent about 31% of applications, reflecting hydrogen’s role as a core feedstock in chemical synthesis. Power generation and energy storage applications, while currently accounting for approximately 14%, are the fastest-growing application segment with an estimated CAGR of 29%, driven by grid balancing needs and seasonal energy storage requirements. Mobility-related applications, including fuel cell vehicles and material handling equipment, contribute roughly 9% and are gaining traction through fleet-based adoption models. Remaining applications, such as electronics manufacturing and specialty industrial heating, collectively represent about 7%.

Industrial manufacturers are the leading end-user segment, accounting for approximately 58% of hydrogen generation adoption, primarily across refining, chemicals, metals, and glass production. Energy and utility providers represent around 21% of end-user demand, leveraging hydrogen for grid balancing, backup power, and renewable integration. Transportation and mobility operators currently account for about 11% but form the fastest-growing end-user segment, expanding at an estimated CAGR of 27% due to increased deployment of hydrogen-powered buses, trucks, and logistics fleets. Public infrastructure operators and research institutions collectively contribute the remaining 10%, supporting pilot-scale and demonstration projects. Adoption rates among large industrial facilities exceed 60%, while utility-scale hydrogen usage penetration has crossed 25% in regions with high renewable capacity.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Asia-Pacific continues to dominate due to high hydrogen consumption exceeding 36 million metric tons annually, driven by large-scale refining, ammonia, and methanol production. Europe, while smaller in volume, shows accelerated momentum with over 210 active hydrogen projects and electrolyzer capacity surpassing 2.4 GW by 2025. North America held approximately 24% market share, supported by strong industrial hydrogen demand and policy incentives. The Middle East & Africa contributed nearly 10%, leveraging low-cost renewable energy and export-oriented hydrogen strategies. South America accounted for around 6%, with growing investments in green hydrogen linked to renewable-rich geographies. Regional differentiation is shaped by infrastructure readiness, industrial demand intensity, regulatory maturity, and technology deployment scale.

How is advanced industrial adoption accelerating low-emission hydrogen deployment?

The market in this region accounted for nearly 24% of global hydrogen generation adoption in 2025, supported by strong demand from petroleum refining, chemicals, steel, and emerging clean power applications. Industrial hydrogen consumption exceeded 11 million metric tons, with over 60% used in refining and chemical processing. Government-backed clean hydrogen incentives and tax credits have accelerated project announcements exceeding 120 large-scale installations. Digital transformation trends include AI-enabled electrolyzer monitoring and predictive maintenance, improving system uptime by over 20%. A major regional industrial gas producer expanded on-site hydrogen generation capacity by 15% to support low-emission refining operations. Regional consumer behavior reflects higher enterprise adoption in energy-intensive industries and utilities, with increasing preference for on-site hydrogen generation to reduce supply risk.

Why is policy-driven decarbonization reshaping hydrogen deployment strategies?

This region held approximately 22% market share in 2025, with Germany, the UK, and France collectively accounting for over 65% of regional hydrogen demand. Hydrogen consumption exceeded 9 million metric tons, increasingly shifting toward low-carbon and green hydrogen pathways. Regulatory frameworks aligned with climate neutrality targets have resulted in over 45% of new hydrogen projects being renewable-powered. Electrolyzer installations surpassed 2.4 GW, reflecting strong adoption of PEM and alkaline technologies. A leading regional energy utility launched a hydrogen cluster supplying industrial and mobility users, improving emissions intensity by 30%. Consumer behavior is influenced by regulatory pressure, driving demand for transparent, certifiable hydrogen production methods.

What factors are sustaining large-scale production leadership?

Asia-Pacific ranked first globally by volume, accounting for around 38% of hydrogen generation activity in 2025. China, Japan, and India are the top consuming countries, together producing and consuming over 36 million metric tons annually. Infrastructure expansion includes more than 1.5 GW of commissioned electrolyzer capacity and extensive hydrogen pipeline networks supporting industrial hubs. Manufacturing-led hydrogen usage dominates, particularly in steel, refining, and chemical synthesis. A major regional manufacturer scaled domestic electrolyzer production capacity by 40% to meet industrial demand. Regional consumer behavior is driven by industrial self-sufficiency and cost efficiency, with high adoption of captive hydrogen systems within manufacturing clusters.

How are renewable-rich economies shaping hydrogen potential?

This region accounted for approximately 6% of global hydrogen generation activity, led by Brazil and Argentina. Hydrogen demand is closely linked to refining, fertilizer production, and emerging export-oriented green hydrogen initiatives. Installed renewable capacity exceeding 280 GW supports low-cost hydrogen generation potential. Government incentives and bilateral trade agreements have encouraged pilot projects focused on ammonia and synthetic fuels. A regional energy firm initiated a green hydrogen project integrating wind power, achieving a 25% reduction in fossil-based hydrogen use. Consumer behavior shows demand tied to energy exports and localized industrial applications rather than widespread domestic consumption.

Why is low-cost energy positioning the region as a future supply hub?

The region contributed nearly 10% of global hydrogen generation demand, driven by oil & gas processing, refining, and petrochemical industries. The UAE and South Africa are key growth countries, with hydrogen consumption exceeding 4.5 million metric tons combined. Large-scale solar and wind projects enable competitive hydrogen production costs, supporting export-focused strategies. Technological modernization includes digital plant optimization and high-capacity electrolyzer deployment. A regional energy company announced a multi-gigawatt hydrogen project targeting industrial and export markets. Consumer behavior reflects strong demand from heavy industry and state-backed infrastructure projects rather than decentralized adoption.

China Hydrogen Generation Market – 31% market share

Dominance driven by massive industrial hydrogen production capacity and integration across refining, chemicals, and steel manufacturing.

United States Hydrogen Generation Market – 21% market share

Leadership supported by strong industrial demand, extensive hydrogen infrastructure, and large-scale clean hydrogen project deployment.

The Hydrogen Generation market exhibits a moderately fragmented competitive structure, with more than 40 active global and regional competitors operating across conventional, low-carbon, and green hydrogen production technologies. The top five companies collectively account for approximately 46% of installed hydrogen generation capacity worldwide, reflecting increasing consolidation at the technology and project development level while leaving room for regional and specialized players. Competitive positioning is strongly influenced by electrolyzer manufacturing scale, project execution capability, and access to low-cost renewable electricity.

Strategic initiatives are centered on long-term supply agreements, joint ventures with renewable energy developers, and large-scale electrolyzer deployments exceeding 100 MW per project. Over 60% of leading players have announced partnerships focused on green hydrogen hubs, industrial clusters, or export-oriented ammonia projects. Product innovation trends include higher current-density electrolyzers, modular hydrogen plants, and digitally optimized control systems, with more than 35% of companies integrating AI-based monitoring to improve plant efficiency by over 15%. Mergers and strategic equity investments are also rising, particularly among technology providers seeking vertical integration. Overall, competition is intensifying as firms differentiate through scale, cost efficiency, and compliance-ready hydrogen solutions.

Siemens Energy AG

Nel ASA

Plug Power Inc.

Cummins Inc.

Thyssenkrupp Nucera

Messer Group

Bloom Energy Corporation

The Hydrogen Generation market is being reshaped by both mature and emerging production technologies, each driving efficiency, cost optimization, and sustainability outcomes. Conventional steam methane reforming (SMR) remains the backbone of industrial hydrogen production, contributing approximately 46% of global output, primarily for refining and chemical synthesis. However, low-carbon SMR integrated with carbon capture and storage (CCS) systems now accounts for around 28% of adoption, enabling industrial users to achieve verified CO₂ reductions exceeding 2.5 million metric tons annually at large-scale facilities.

Green hydrogen technologies, particularly Proton Exchange Membrane (PEM) and alkaline electrolysis, are rapidly gaining traction. PEM electrolyzers currently represent roughly 18% of adoption and are preferred for industrial and mobility applications due to their operational flexibility and fast start-up capabilities. Alkaline electrolysis contributes about 14% of installed capacity and remains a cost-effective option for large-scale hydrogen hubs. Solid oxide electrolysis systems (SOEC) are emerging, delivering up to 28% higher electrical-to-hydrogen efficiency compared to conventional alkaline systems, particularly when integrated with high-temperature industrial waste heat.

Digitalization and AI-driven optimization are key enablers, with over 40% of operational plants deploying predictive maintenance, real-time load balancing, and degradation monitoring tools. These technologies have improved electrolyzer uptime by 22% and reduced unplanned downtime by nearly 28%, enhancing overall system reliability. Modular and prefabricated hydrogen plant designs are also transforming deployment timelines, reducing construction labor by 32% and installation durations by 25%. Together, these innovations are advancing hydrogen generation toward scalable, low-carbon, and economically viable solutions for industrial, mobility, and energy storage applications.

• In October 2025, Plug Power delivered the first 10 MW electrolyzer unit for the 100 MW green hydrogen project at Galp’s Sines Refinery, marking the initial phase of one of Europe’s largest renewable hydrogen production hubs focused on decarbonizing refining operations. (ir.plugpower.com)

• In March 2025, INOX Air Products commissioned India’s first solar-powered green hydrogen plant at Asahi India Glass Limited’s facility in Soniyana, Rajasthan, capable of producing up to 190 tons of green hydrogen per year, enabling clean feedstock for float glass manufacturing.

• In April 2025, Air Liquide’s 20 MW PEM electrolyzer in Oberhausen, Germany was integrated into its industrial pipeline network and began supplying renewable hydrogen to local industrial and mobility customers, producing up to 2,900 tons annually.

• In Q1 2025, HydrogenPro announced a 100 MW electrolyzer order from ANDRITZ for a green hydrogen plant in Rostock, Germany, advancing large-scale electrolysis deployment in northern Europe. (Euronext Live)

The Hydrogen Generation Market Report spans multiple facets of the hydrogen economy, offering comprehensive insights into production technologies, regional deployment, end‑user consumption, and emerging value chains. The report systematically analyzes production types including conventional steam methane reforming, low‑carbon hydrogen with carbon capture integration, and renewable power‑driven electrolyzers such as PEM, alkaline, and solid oxide systems. Each type’s technical parameters, scalability, and integration into industrial processes are examined alongside infrastructure requirements and operational characteristics.

Geographically, the report covers all major markets including Asia‑Pacific, Europe, North America, South America, and Middle East & Africa, with detailed volume, capacity metrics, and regional prioritization trends. It evaluates application areas such as petroleum refining, ammonia and methanol synthesis, power generation, energy storage, and mobility fueling, offering insights into how hydrogen generation is reshaping energy and industrial sectors. End‑user segments including heavy manufacturing, utilities, transport operators, and public infrastructure are profiled to highlight consumption patterns and technology adoption rates.

The scope further encompasses regulatory environments, incentive frameworks, and investment landscapes shaping deployment strategies across jurisdictions. Technology focus includes electrolyzer advancements, modular plant architectures, digital optimization tools such as AI‑enabled control systems, and integrated renewable generation models. Emerging segments such as hydrogen hubs, export‑oriented production, and niche production pathways (e.g., biomass or chemical looping) are also identified. The report is structured for decision‑makers seeking actionable intelligence on capacity build‑outs, technology roadmaps, operational benchmarks, and strategic partnerships driving the hydrogen generation ecosystem forward.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Air Liquide, Linde plc, Air Products and Chemicals, Inc., Siemens Energy AG, Nel ASA, Plug Power Inc., Cummins Inc., Thyssenkrupp Nucera, Messer Group, Bloom Energy Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |