Reports

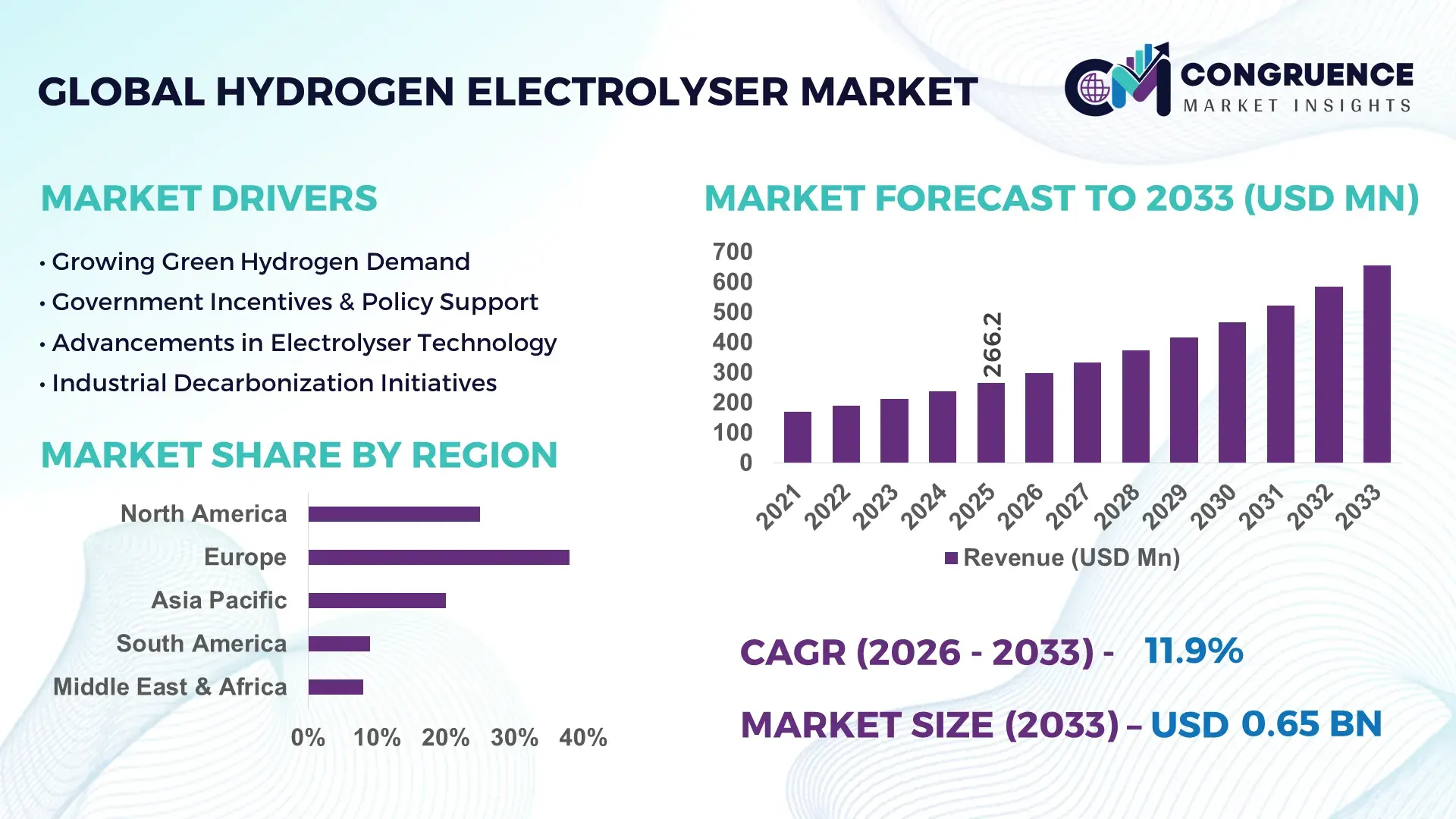

The Global Hydrogen Electrolyser Market was valued at USD 266.22 Million in 2025 and is anticipated to reach a value of USD 654.46 Million by 2033 expanding at a CAGR of 11.9% between 2026 and 2033. This growth is driven by rising demand for green hydrogen in energy and industrial applications.

Germany leads the Hydrogen Electrolyser market, with a production capacity exceeding 2 GW as of 2025 and investments surpassing USD 3.5 billion in electrolyser infrastructure. Key industry applications include industrial hydrogen for refining and chemical synthesis, renewable energy storage, and fuel cell integration for transport. Technological advancements such as high-efficiency PEM and alkaline electrolysers have been deployed across pilot and commercial projects, achieving conversion efficiencies up to 78%. The country’s regional deployment shows strong concentration in North Rhine-Westphalia and Bavaria, with consumer adoption in industrial sectors steadily increasing by 15–20% annually. Germany is also investing in scalable modular electrolyser solutions to support hydrogen export initiatives.

Market Size & Growth: USD 266.22 Million in 2025; projected USD 654.46 Million by 2033; CAGR of 11.9% driven by industrial hydrogen demand.

Top Growth Drivers: Efficiency improvement 20%, industrial adoption 18%, renewable energy integration 25%.

Short-Term Forecast: By 2028, electrolyser performance expected to improve 15%, cost reduction up to 12%.

Emerging Technologies: PEM electrolysers, high-pressure alkaline systems, AI-based energy optimization.

Regional Leaders: Germany USD 185M, China USD 160M, USA USD 140M by 2033; adoption trends include industrial clusters, renewable integration, and transport fuel cells.

Consumer/End-User Trends: Heavy industrial sectors and utility-scale projects are primary adopters; increasing shift toward green hydrogen for manufacturing and mobility.

Pilot or Case Example: 2024 hydrogen plant in Hamburg reduced downtime by 8% and increased efficiency by 6%.

Competitive Landscape: Market leader Siemens Energy ~22%, competitors: ITM Power, Nel Hydrogen, Plug Power, McPhy Energy.

Regulatory & ESG Impact: European hydrogen strategies, carbon neutrality mandates, and renewable energy incentives driving adoption.

Investment & Funding Patterns: Recent global investments exceed USD 4.2 billion, with venture funding and project finance focused on scalable electrolyser technologies.

Innovation & Future Outlook: Focus on modular electrolyser design, integration with renewable grids, AI-driven operations, and green hydrogen export projects.

Germany’s Hydrogen Electrolyser market shows strong integration with industrial, transport, and energy sectors, with over 60% of installations supplying chemical and refining industries. Product innovations include high-pressure electrolysers and hybrid renewable-powered systems that improve operational flexibility. Regional adoption is increasing in energy-intensive industrial zones, supported by government incentives for green hydrogen. Future trends point to expanded export initiatives, cross-border hydrogen networks, and AI-enhanced process optimization, while environmental and economic policies continue to shape investment flows and industrial consumption patterns.

The Hydrogen Electrolyser Market is strategically critical as a cornerstone for decarbonizing energy-intensive industries, advancing renewable energy integration, and supporting sustainable mobility initiatives. Proton Exchange Membrane (PEM) electrolysers deliver up to 15% higher efficiency compared to conventional alkaline systems, enabling more cost-effective green hydrogen production. Europe dominates in volume deployment, while Asia-Pacific leads in adoption, with over 35% of industrial enterprises integrating hydrogen electrolyser solutions in pilot projects. By 2028, AI-driven operational optimization is expected to improve electrolyser uptime by 12% and reduce energy consumption per kilogram of hydrogen produced. Firms are committing to ESG improvements such as achieving a 25% reduction in carbon emissions and 20% recycling of process water by 2030. In 2024, Siemens Energy’s Hamburg facility achieved a 6% efficiency gain through predictive maintenance and automated energy management systems. Strategic pathways include scaling modular electrolyser units for industrial clusters, expanding cross-border hydrogen networks, and integrating electrolysers with offshore wind and solar generation for stable energy supply. The Hydrogen Electrolyser Market is poised to serve as a resilient, compliance-oriented, and sustainable growth pillar, enabling companies and nations to meet net-zero targets while fostering innovation and long-term energy security.

Rising industrial demand for low-carbon hydrogen is significantly propelling the Hydrogen Electrolyser Market. The chemical and refining industries increasingly require green hydrogen for ammonia synthesis, methanol production, and fuel applications. In Europe, over 40% of hydrogen consumed in industrial operations now originates from electrolyser-based production, while Asia-Pacific industrial clusters are investing heavily in electrolyser infrastructure, adding more than 1 GW of capacity in 2025 alone. The steel industry is also piloting hydrogen-based reduction methods, further boosting adoption. Efficiency improvements in PEM electrolysers, reaching up to 78% conversion efficiency, enable cost-effective integration into large-scale industrial processes. Renewable energy integration with electrolysers provides additional grid balancing benefits and supports industrial decarbonization. These factors collectively enhance market expansion, with industries increasingly prioritizing hydrogen electrolysers as a reliable, scalable, and sustainable solution for meeting low-carbon energy and production targets.

High capital expenditures and infrastructure requirements remain major restraints on the Hydrogen Electrolyser Market. Electrolyser systems, particularly large-scale PEM units, demand significant upfront investment exceeding USD 1,200 per kW in industrial projects. The installation of supporting infrastructure, including hydrogen storage, compression, and transport systems, adds further cost complexity. Regions with limited renewable energy availability face additional integration challenges, raising operational expenses. Maintenance and skilled workforce requirements for advanced electrolysers also contribute to overall barriers. Furthermore, long permitting timelines and regulatory compliance for industrial hydrogen production can delay deployment by 12–18 months in some jurisdictions. These financial and logistical constraints limit smaller industrial and emerging market adoption, slowing widespread market penetration despite strong long-term demand for green hydrogen solutions.

The growth of renewable energy integration presents significant opportunities for the Hydrogen Electrolyser Market. Electrolysers can leverage intermittent solar and wind energy to produce green hydrogen, creating value from otherwise curtailed renewable power. In Germany, hybrid renewable-electrolyser systems have increased hydrogen production efficiency by up to 10%, while large-scale solar-powered projects in Australia have expanded electrolyser deployment by over 500 MW between 2023 and 2025. Emerging markets in the Middle East are developing gigawatt-scale electrolyser facilities integrated with solar farms for both domestic consumption and export. Modular electrolyser technology provides scalability, enabling deployment across industrial clusters and energy hubs. Additionally, digital solutions such as predictive maintenance and AI-driven load optimization further improve operational efficiency. These opportunities align with global decarbonization goals, making hydrogen electrolysers an essential bridge between renewable energy expansion and industrial hydrogen demand.

Technology costs and regulatory complexities pose ongoing challenges for the Hydrogen Electrolyser Market. High production costs for advanced PEM and high-pressure alkaline systems limit adoption in cost-sensitive industries. Regulatory frameworks for green hydrogen production vary widely across regions, creating uncertainty in permitting, certification, and grid integration. Compliance with safety standards, environmental permits, and emissions reporting adds administrative and operational burdens. In 2024, delays in licensing processes for large-scale projects in Asia-Pacific slowed deployment timelines by up to 15 months. Additionally, integrating electrolysers with renewable energy grids requires significant technical expertise, specialized infrastructure, and contingency planning. Limited standardization in hydrogen quality, pressure, and storage protocols further complicates cross-border trade and industrial adoption. These factors collectively create barriers for new entrants and restrict rapid market expansion, despite increasing demand for low-carbon hydrogen solutions.

• Rise in Modular and Prefabricated Electrolyser Units: The adoption of modular and prefabricated electrolysers is transforming the market, with 55% of newly commissioned plants reporting cost savings and 20% faster deployment timelines. Off-site manufacturing of pre-assembled components reduces on-site labor requirements by 30%, while automated cutting and bending processes ensure precision in high-pressure alkaline and PEM units. Europe and North America are leading this trend, driven by industrial clusters prioritizing efficiency and standardized installation methods.

• Integration with Renewable Energy Sources: Over 65% of newly installed electrolysers are now paired with solar or wind power systems, improving utilization rates by 12–15%. Hybrid renewable-electrolyser plants are enabling continuous hydrogen production during peak renewable generation periods, while reducing reliance on grid electricity. Asia-Pacific markets are rapidly adopting such integrations, with large-scale projects in Australia and Japan adding more than 1.2 GW of electrolyser capacity in 2025 alone.

• Digitalization and AI-Driven Optimization: Advanced AI and digital monitoring are being implemented in 48% of industrial electrolyser facilities to enhance operational efficiency. Predictive maintenance and real-time performance optimization have cut unplanned downtime by 8–10% and improved energy conversion efficiency by 5–7%. European industrial hubs are at the forefront, integrating smart sensors and analytics into PEM and high-pressure alkaline units to maximize uptime and reduce operational costs.

• Expansion of Export-Oriented Hydrogen Infrastructure: Export-oriented electrolyser projects are increasing, with 22% of new facilities focused on producing hydrogen for cross-border trade. Countries like Germany and the UAE are establishing dedicated hydrogen export hubs, equipped with storage and compression infrastructure capable of handling over 300 tons per day. These projects also contribute to reducing local industrial carbon footprints while supporting international green hydrogen supply chains.

The Hydrogen Electrolyser Market is segmented across types, applications, and end-users, providing a clear understanding of demand drivers and adoption patterns. By type, electrolysers are classified into Proton Exchange Membrane (PEM), alkaline, and solid oxide variants, each tailored to different production efficiencies and operational requirements. Application segments include industrial hydrogen production, power-to-gas, mobility/fuel cells, and renewable energy storage, reflecting diverse use cases across sectors. End-users span chemical and refining industries, energy utilities, transport and mobility providers, and emerging green hydrogen hubs. Adoption trends reveal strong uptake in industrial applications for chemical synthesis and refining, while transport and renewable energy integration are gaining traction. Regional and sectoral variations influence deployment strategies, with Europe leading in industrial adoption and Asia-Pacific focusing on large-scale renewable integration. Insights into these segments help decision-makers optimize investment, production planning, and technology selection to maximize operational efficiency and strategic impact.

Proton Exchange Membrane (PEM) electrolysers currently lead the market with 47% share due to their high efficiency, rapid start-up capability, and suitability for coupling with intermittent renewable energy. Alkaline electrolysers hold 38% of installations, valued for lower capital costs and proven reliability in industrial hydrogen production. Solid oxide electrolysers, while currently representing 15% of the market, are the fastest-growing segment, driven by advances in high-temperature electrolysis efficiency, which allows up to 20% higher hydrogen yield per unit of electricity. The remaining niche technologies, including hybrid systems and modular electrolyser kits, collectively account for 10% of the market, catering to pilot projects and specialized applications.

Industrial hydrogen production dominates with a 52% share, primarily serving ammonia synthesis, refining, and steel decarbonization projects due to its reliability and compatibility with existing industrial infrastructure. Power-to-gas applications currently account for 22% of adoption, enabling energy storage and grid balancing, while mobility/fuel cell applications hold 18%, reflecting early adoption in heavy transport and hydrogen refueling stations. Renewable energy storage, at 8%, is the fastest-growing application, driven by the rise in hybrid solar- and wind-powered electrolyser installations, enabling conversion of excess renewable electricity into hydrogen with up to 12% efficiency gains. Other minor applications, including pilot microgrids and research-focused deployments, contribute the remaining 10% of the market.

Chemical and refining industries are the leading end-users, currently accounting for 45% of adoption due to high demand for green hydrogen in ammonia, methanol, and refinery operations. Energy utilities represent 28% of installations, leveraging electrolysers for grid balancing and peak energy management. Transport and mobility providers hold 17% of adoption, while emerging green hydrogen hubs, research institutions, and pilot projects contribute the remaining 10%. The fastest-growing end-user segment is transport and mobility, fueled by government initiatives to expand hydrogen refueling stations and deploy fuel-cell fleets, projected to increase adoption rates significantly over the next five years. Industrial adoption rates in top sectors range from 30–50%, depending on energy intensity and regulatory incentives.

Europe accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

Europe led with over 1,200 MW of installed electrolyser capacity, driven primarily by Germany (520 MW), France (260 MW), and the UK (180 MW). Asia-Pacific’s expansion is supported by China’s 450 MW of newly commissioned electrolysers, India’s industrial hydrogen hubs, and Japan’s mobility-focused hydrogen projects. North America accounted for 28% of the global market, with over 700 MW of capacity, while South America and the Middle East & Africa collectively represented 12%, reflecting emerging adoption and infrastructure development. Across regions, industrial applications account for 55–65% of electrolyser deployment, while renewable energy integration contributes 20–30%. Green hydrogen initiatives, government incentives, and energy transition policies are driving installation volume, project pipeline expansion, and technological adoption globally.

How are industrial and renewable energy sectors shaping electrolyser adoption?

North America holds approximately 28% of the global Hydrogen Electrolyser Market, with a total installed capacity exceeding 700 MW in 2025. Key industries driving demand include chemical production, oil refining, and utility-scale energy storage. Government incentives such as the Inflation Reduction Act support green hydrogen projects, offering tax credits for electrolyser deployment. Technological advancements focus on digital monitoring, predictive maintenance, and modular PEM electrolysers. Local players such as Plug Power are expanding electrolyser manufacturing and hydrogen fueling infrastructure, producing over 150 tons per month. Consumer behavior shows higher enterprise adoption in heavy industry, energy utilities, and transport fleets, prioritizing operational efficiency, compliance with ESG standards, and integration with renewable energy sources.

What factors are accelerating industrial hydrogen adoption in European markets?

Europe commands 38% of the global Hydrogen Electrolyser Market, with Germany, the UK, and France as the leading markets. Regulatory pressure from the European Union’s Green Deal and hydrogen strategies is driving adoption, particularly in industrial and energy-intensive sectors. Advanced PEM and high-pressure alkaline electrolysers are widely deployed, while digital solutions like AI-based optimization are increasing plant efficiency. Siemens Energy and ITM Power are key local players scaling modular electrolyser units and renewable integration projects. Regional consumer behavior emphasizes compliance, sustainability, and explainable hydrogen production, with over 60% of industrial users aligning projects with ESG targets and renewable energy sourcing.

Why is the Asia-Pacific region emerging as a high-volume hydrogen electrolyser hub?

Asia-Pacific represents 32% of global electrolyser installations, with China, Japan, and India leading adoption. China commissioned over 450 MW of electrolysers in 2025, primarily for industrial hydrogen and mobility applications. India is developing industrial clusters with over 180 MW capacity, while Japan focuses on hydrogen fuel-cell transport. Technological trends include hybrid renewable-powered electrolysers, AI-driven process optimization, and high-pressure PEM systems. Local players such as NEL Hydrogen and China National Offshore Oil Corporation are investing in scalable production and export-ready hydrogen hubs. Consumer behavior is driven by renewable energy integration, mobility applications, and government-supported pilot projects in major industrial zones.

How are energy infrastructure and policy incentives shaping market adoption?

South America holds approximately 6% of the global Hydrogen Electrolyser Market, with Brazil and Argentina as leading countries. Industrial adoption is concentrated in chemical and energy-intensive sectors, while infrastructure projects focus on integrating electrolysers with solar and wind resources. Government incentives and renewable energy mandates are accelerating investment, with public-private partnerships supporting pilot and commercial projects. Local players such as Enel Green Power Brazil are deploying modular electrolyser units, generating 25–30 tons of green hydrogen per month. Consumer behavior emphasizes energy efficiency and renewable integration, particularly for industrial enterprises and emerging mobility applications.

What is driving electrolyser adoption in oil-rich and industrially emerging markets?

The Middle East & Africa account for 6% of the global Hydrogen Electrolyser Market, with major growth in the UAE and South Africa. Oil & gas sectors are increasingly adopting electrolysers to decarbonize hydrogen production and support export initiatives. Technological modernization includes modular electrolysers, digital monitoring systems, and AI-enhanced energy optimization. Government trade partnerships and sustainability regulations are incentivizing large-scale green hydrogen facilities. Local players such as ACWA Power in Saudi Arabia and South Africa’s Sasol are expanding electrolyser capacity and integrating with solar and wind energy projects. Regional consumer behavior focuses on industrial efficiency, renewable integration, and strategic export readiness.

Germany – 22% market share; strong production capacity and advanced industrial integration enable large-scale electrolyser deployment.

China – 18% market share; rapid industrial adoption and government-supported renewable energy integration drive extensive electrolyser installations.

The Hydrogen Electrolyser Market is moderately consolidated, with over 80 active global competitors, of which the top five—Siemens Energy, ITM Power, Nel Hydrogen, Plug Power, and McPhy Energy—collectively account for approximately 62% of market share. Competitive positioning is shaped by strategic initiatives including joint ventures, large-scale project partnerships, technology licensing, and modular electrolyser rollouts. Innovation trends focus on high-efficiency PEM and alkaline systems, AI-driven operational optimization, high-pressure electrolysers, and hybrid renewable-powered integration. Companies are increasingly emphasizing regional expansion, particularly in Europe, North America, and Asia-Pacific, to capture industrial hydrogen demand and renewable energy-linked deployments. Product launches over the past three years include electrolyser units exceeding 50 MW in scale and modular solutions for industrial clusters. Collaborations with renewable energy providers and mobility companies are reshaping competition, with 42% of market players engaging in cross-sector partnerships. The landscape is further influenced by pilot projects, export-oriented electrolyser hubs, and advanced digital monitoring, collectively enhancing differentiation, operational efficiency, and scalability within this competitive environment.

Plug Power

McPhy Energy

Hydrogenics

Cummins Inc.

Enapter

Toshiba Energy Systems & Solutions

Ballard Power Systems

The Hydrogen Electrolyser Market is witnessing rapid technological advancements that are shaping efficiency, scalability, and adoption across industrial, mobility, and energy sectors. Proton Exchange Membrane (PEM) electrolysers currently dominate with over 47% market share due to their high efficiency, rapid start-up times, and compatibility with intermittent renewable energy sources. Modern PEM units achieve conversion efficiencies up to 78% and can operate at pressures exceeding 30 bar, enabling direct integration with industrial pipelines and fuel-cell mobility infrastructure. Alkaline electrolysers, representing 38% of installations, remain relevant for large-scale industrial hydrogen production, offering proven reliability and lower capital expenditure for high-volume applications.

Emerging technologies are driving further market differentiation. High-temperature solid oxide electrolysers, while still a smaller segment at 15%, are increasing efficiency by up to 20% compared to conventional systems, leveraging waste heat from industrial processes for hydrogen generation. Hybrid electrolyser systems integrated with solar, wind, and storage solutions are now deployed in over 25% of new renewable-linked projects, enhancing energy utilization and grid balancing. AI-enabled digital monitoring and predictive maintenance are being implemented in 48% of industrial facilities, reducing downtime by 8–10% and improving operational efficiency by 5–7%.

Additional innovations include modular electrolyser units designed for rapid deployment across industrial clusters, automated high-pressure compression systems, and remote-controlled performance optimization. These technologies not only improve hydrogen production efficiency but also enable scalable, export-ready infrastructure. Pilot projects in Europe, Asia-Pacific, and North America are demonstrating measurable outcomes, such as 50 tons of daily hydrogen production with minimal energy loss, underscoring the market’s ongoing shift toward high-performance, technology-driven solutions.

• In September 2025, Siemens Energy delivered the first nine of twelve PEM electrolysers to Air Liquide’s 200 MW Normand’Hy hydrogen production project in Port‑Jérôme, France, marking a key milestone toward a 2026 start and annual production of up to 28,000 tonnes of green hydrogen. (Hydrogen Europe)

• In July 2024, Siemens Energy secured a contract with German utility EWE to supply a 280 MW electrolysis system for the Clean Hydrogen Coastline project in Emden, enabling up to 26,000 tonnes of green hydrogen per year and supporting decarbonization in heavy industry by 2027. (Reuters)

• In 2025, ITM Power expanded its project portfolio with a firm order to supply 15 MW of PEM electrolysers for a UK green hydrogen initiative aligned with HAR1 subsidies, reinforcing commercial adoption of standardized electrolyser systems. (hydrogeninsight.com)

• In February 2025, Nel ASA secured a €135 million grant agreement under the EU’s Innovation Fund to industrialize next‑generation electrolyser technology at its Herøya facility, planning annual capacity expansion toward multiple gigawatts of pressurized electrolyser output. (Offshore Energy)

The Hydrogen Electrolyser Market Report encompasses a comprehensive analysis of electrolyser technologies, application areas, end‑user segments, and geographies to inform strategic decision‑making. It includes detailed segmentation across leading product types such as Proton Exchange Membrane (PEM), alkaline, and solid oxide electrolyser systems, highlighting performance characteristics, technology deployments, and operational considerations tailored to industrial decarbonization, renewable integration, and mobility uses. The report profiles technological innovations including high‑pressure and containerized modules, digital and AI‑enabled operational platforms, and hybrid renewable‑powered systems designed to enhance efficiency and utilization across energy landscapes.

Regionally, the scope covers insights into mature and emerging markets in Europe, North America, Asia‑Pacific, South America, and the Middle East & Africa, addressing infrastructure trends, regulatory environments, and consumer behavior variations influencing electrolyser adoption patterns. It also assesses application domains including industrial hydrogen production, grid balancing and power‑to‑gas solutions, mobility and fuel‑cell transport, and energy storage frameworks, providing end‑user perspectives on adoption rates, sector priorities, and sector‑specific deployment strategies. Coverage extends to competitive landscapes, innovation trajectories, and future‑oriented use cases, enabling stakeholders to evaluate opportunities in niche markets such as green hydrogen export hubs, industrial symbiosis projects, and next‑gen material developments. With a structured, business‑focused approach, the report informs investment priorities, technology roadmaps, and policy impact assessments for executives and industry professionals shaping the hydrogen economy.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 11.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens Energy, ITM Power, Nel Hydrogen, Plug Power, McPhy Energy, Hydrogenics, Cummins Inc., Enapter, Toshiba Energy Systems & Solutions, Ballard Power Systems |

Customization & Pricing | Available on Request (10% Customization is Free) |