Reports

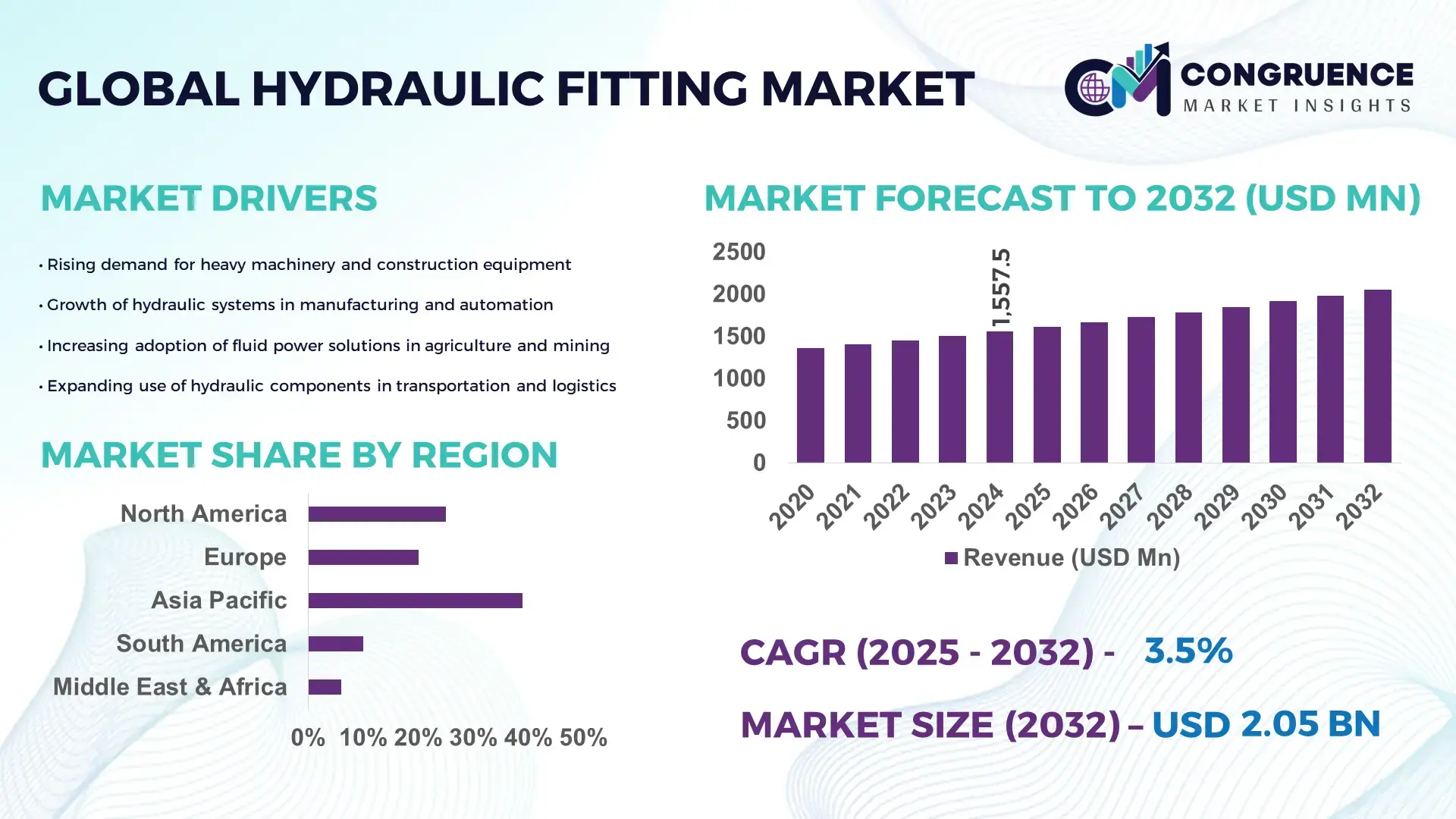

The Global Hydraulic Fitting Market was valued at USD 1557.45 Million in 2024 and is anticipated to reach a value of USD 2050.86 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032. This growth is supported by continuous demand for high-pressure fluid handling systems across industrial and mobile hydraulic applications.

The United States holds the most dominant position in the Hydraulic Fitting Market, supported by its extensive manufacturing ecosystem, large-scale production capabilities, and high adoption of advanced hydraulic systems in construction, mining, aerospace, and heavy machinery. The country hosts over 4,500 active hydraulic component manufacturing facilities and invests more than USD 3.1 billion annually in hydraulic system modernization and automation. With more than 62% penetration of smart hydraulic control systems in industrial applications and ongoing investments in precision-engineered fittings, the U.S. continues to lead innovation through advanced materials, leak-free sealing technologies, and digitally monitored hydraulic assemblies.

• Market Size & Growth: Market valued at USD 1557.45 Million in 2024, projected to reach USD 2050.86 Million by 2032 at 3.5% CAGR, driven by rising demand for leak-proof high-pressure systems.

• Top Growth Drivers: 28% increase in industrial automation adoption; 34% efficiency enhancement in hydraulic machinery; 22% rise in heavy equipment utilization.

• Short-Term Forecast: By 2028, hydraulic system performance expected to improve by 18% due to upgrades in sealing, materials, and system integration.

• Emerging Technologies: Advancements in digital pressure monitoring and corrosion-resistant alloys; adoption of additive manufacturing for precision hydraulic components.

• Regional Leaders: North America projected at USD 670 Million by 2032 with strong automation uptake; Europe expected at USD 540 Million with rapid industrial retrofits; Asia-Pacific anticipated at USD 620 Million supported by construction equipment expansion.

• Consumer/End-User Trends: High adoption among construction, mining, and manufacturing sectors, with increasing preference for maintenance-free and high-durability fittings.

• Pilot or Case Example: In 2024, a U.S.-based mining operator deployed reinforced hydraulic fittings achieving a 26% reduction in equipment downtime.

• Competitive Landscape: Market led by Parker Hannifin with about 17% share, followed by Eaton, Gates Corporation, Manuli Hydraulics, and HYDAC.

• Regulatory & ESG Impact: Stricter fluid leakage standards and energy-efficiency regulations are increasing the shift toward environmentally compliant hydraulic components.

• Investment & Funding Patterns: Over USD 1.2 Billion invested in hydraulic component modernization and automation projects in the past three years.

• Innovation & Future Outlook: Integration of IoT-enabled hydraulic sensors, improved alloy engineering, and development of predictive maintenance-compatible fittings shaping future growth.

The Hydraulic Fitting Market is experiencing steady expansion across sectors such as construction machinery, agricultural equipment, aerospace systems, and industrial automation, with each segment contributing significantly to overall industry demand. Advancements in high-pressure sealing technology, corrosion-resistant materials, and smart monitoring features are improving system reliability and lifecycle performance. Regulatory measures focusing on leak reduction and energy efficiency are driving wider adoption across industrial facilities, while emerging economies show increasing consumption due to infrastructure development and equipment modernization. The market is further influenced by shifts toward compact machinery, modular hydraulic systems, and automated maintenance, reinforcing strong long-term growth prospects within the global hydraulic ecosystem.

The Hydraulic Fitting Market holds strategic importance as a core enabler of industrial productivity, heavy machinery performance, and high-pressure fluid power efficiency across global manufacturing ecosystems. Its relevance is reinforced by measurable system-level improvements driven by material science, automation, and digital condition monitoring. Smart hydraulic fittings embedded with pressure-sensing microchips are delivering a 27% improvement in operational visibility compared to older manual-inspection standards. In this evolving landscape, Asia-Pacific dominates in volume due to expansive construction and mining activities, while North America leads in technology adoption with 61% of enterprises utilizing advanced leak-detection-enabled fittings. By 2027, AI-driven hydraulic diagnostics are expected to reduce unplanned downtime by 22%, enhancing equipment lifecycle value and maintenance predictability. Firms are committing to ESG improvements such as achieving up to 30% material recycling rates for hydraulic components by 2030 to align with global compliance requirements. In 2024, Germany achieved a 19% reduction in hydraulic fluid loss after implementing AI-enabled predictive sealing solutions across industrial machinery. With increasing integration of IoT, corrosion-resistant alloys, and additive manufacturing, the Hydraulic Fitting Market is positioned as a pillar of resilience, compliance, and sustainable growth supporting next-generation industrial performance.

Industrial automation is significantly increasing the demand for advanced Hydraulic Fitting solutions as factories transition toward high-pressure, precision-controlled fluid systems. Automated equipment requires fittings capable of sustaining constant operational stress, with tolerance levels improved by up to 32% through modern alloy engineering. Manufacturing plants adopting robotic material-handling systems report a 24% rise in demand for reinforced hydraulic connectors to support continuous operation. The expansion of automated warehousing, mining vehicles, and agricultural machinery further accelerates consumption of durable fittings designed for vibration resistance and high-cycle endurance. With more than 48% of new industrial machinery featuring enhanced fluid power systems, the Hydraulic Fitting Market is directly benefiting from the global automation wave.

Growing preference for electric actuation and eco-friendly motion systems is creating notable restraints for the Hydraulic Fitting Market as industries explore alternatives to traditional hydraulic assemblies. Electric linear actuators now offer up to 35% efficiency improvement over conventional hydraulic systems in select light-load applications, reducing dependency on hydraulic fittings. Additionally, stricter environmental regulations on hydraulic fluid discharge necessitate costly system upgrades, which some small and mid-sized enterprises delay due to capital constraints. Maintenance-related challenges—such as contamination buildup and fluid leakage—also lead to operational inefficiencies, prompting gradual evaluation of hybrid or non-hydraulic technologies. These dynamics collectively moderate market expansion despite strong demand in heavy-duty sectors.

Advancements in smart fluid monitoring systems are creating substantial opportunities for the Hydraulic Fitting Market, particularly through integration of sensors, edge analytics, and connected diagnostics. Intelligent fittings capable of real-time pressure and temperature tracking can reduce system failure rates by up to 29%. Industries deploying IoT-enabled hydraulic assemblies report heightened interest in predictive maintenance strategies that extend equipment life cycles and reduce inspection costs. Increasing adoption in mining, logistics, military-grade machinery, and automated construction platforms presents new openings for high-performance fittings compatible with digital monitoring frameworks. As more than 52% of OEMs plan to integrate sensor-ready hydraulic components by 2028, this shift is unlocking a technologically advanced growth pathway.

Rising material costs, particularly for stainless steel, nickel alloys, and high-strength composites, pose significant challenges for the Hydraulic Fitting Market as manufacturers face elevated production expenses. Compliance requirements associated with leakage prevention, energy efficiency, and environmental protection introduce additional certification and testing costs that raise overall operational complexity. Small and mid-tier manufacturers often struggle to meet evolving ISO, SAE, and regional environmental standards, leading to delayed product rollouts and reduced competitiveness. Furthermore, supply chain disruptions affecting precision-machined components have extended lead times by up to 18% in some regions. These combined factors create persistent operational challenges for industry stakeholders navigating cost, compliance, and global sourcing pressures.

• Surge in Modular and Prefabricated Construction Integration: The expanding shift toward modular and prefabricated construction is significantly influencing the Hydraulic Fitting Market, with 55% of new modular projects reporting measurable cost efficiencies due to reduced on-site labor and streamlined assembly. Automated off-site fabrication of pre-bent and pre-cut hydraulic components has improved installation accuracy by 28%, while shortening project timelines by nearly 20%. Europe and North America are witnessing accelerated adoption of precision-engineered hydraulic assemblies as contractors prioritize repeatability, safety, and installation speed.

• Acceleration of Smart, Sensor-Enabled Hydraulic Fittings: The market is experiencing rapid growth in intelligent fittings equipped with pressure, temperature, and leak-detection sensors. More than 42% of newly installed industrial hydraulic systems now incorporate at least one sensor-enabled fitting, improving real-time monitoring accuracy by 35%. These technologies have reduced unplanned equipment downtime by 22% across mining, manufacturing, and heavy transport applications, supporting predictive maintenance and improved operational reliability.

• Rising Use of Advanced Materials for High-Pressure Operations: Hydraulic fittings are increasingly manufactured using improved stainless-steel alloys, nickel-based composites, and corrosion-resistant coatings. Adoption of enhanced materials in high-pressure hydraulic circuits has grown by 31% over the last three years. These advanced materials provide up to 40% longer operational life, especially in offshore, military, and extreme-environment applications, where durability and leakage prevention are critical performance parameters.

• Expansion of Automation and Robotics in Manufacturing Lines: Automation-driven manufacturing facilities are reshaping hydraulic fitting demand, with automated assembly lines delivering 27% higher production consistency compared to traditional operations. Industrial robotics usage has expanded by 33% across key sectors, increasing the requirement for precision hydraulic connectors designed for high-cycle reliability. Manufacturers integrating fully automated quality inspection systems report a 19% reduction in defect rates, supporting enhanced system efficiency and faster order fulfilment in global hydraulic component supply chains.

The segmentation structure of the Hydraulic Fitting Market reflects the diverse operational needs of high-pressure fluid systems across industrial, mobile, and specialized mechanical environments. Types, applications, and end-user groups each contribute distinct performance requirements, material standards, and technological expectations. High-pressure, quick-connect, and push-to-connect fittings remain central to industrial usage, while custom-machined and corrosion-resistant variants are increasingly adopted in offshore and defense environments. Applications range from construction and material-handling machinery to aerospace, energy, and large-scale automation systems, with adoption patterns shifting toward advanced, leak-free, and sensor-enabled hydraulic assemblies. End-users such as heavy equipment manufacturers, industrial plants, and transportation system integrators drive the bulk of demand, supported by measurable upticks in automated system installations and precision fluid control needs. These segmentation layers collectively influence innovation cycles, compliance investments, and long-term market evolution.

High-pressure hydraulic fittings currently represent the leading type, accounting for approximately 46% of total adoption due to their critical role in construction equipment, mining vehicles, and industrial machinery. Their dominance is supported by measurable performance advantages, including strength improvements of up to 35% through advanced alloy usage. In comparison, quick-connect fittings hold around 29% of adoption, while push-to-connect systems maintain 18%. However, corrosion-resistant fittings—particularly stainless-steel and nickel-based variants—are the fastest-growing type, supported by an estimated 6.2% CAGR and increasing demand in offshore, defense, and chemical processing sectors. Their rise is driven by a 40% improvement in corrosion endurance and up to 22% reduction in maintenance cycles. All remaining segments, including specialty and custom-machined fittings, contribute a combined 7% share, primarily serving niche, high-performance applications where precision and durability requirements exceed standard operating thresholds.

Construction and heavy machinery applications represent the leading segment, accounting for roughly 44% of total deployment due to high-pressure fluid systems essential for lifting, drilling, excavation, and material handling. This dominance is supported by measurable operational reliability, with hydraulic assemblies achieving up to 30% higher load-handling stability than mechanical alternatives. In comparison, industrial automation systems account for 27% of usage, while agricultural machinery applications maintain 21%. However, aerospace and defense applications are the fastest-growing category, supported by an estimated 6.8% CAGR, driven by demand for lightweight, precision-engineered fittings with enhanced vibration tolerance. Adoption in this segment is expected to surpass 25% by 2032 as performance requirements escalate in advanced aircraft platforms and defense vehicles. Remaining applications—including energy, marine, and utility systems—contribute a combined 8% share, largely due to their requirement for high-durability fittings operating under extreme environmental and pressure conditions.

Heavy equipment manufacturers represent the leading end-user segment, accounting for approximately 48% of total adoption, supported by rapid deployment in excavators, loaders, mining trucks, and industrial lifting systems. Their dominance reflects sustained demand for high-pressure, durable, and low-maintenance hydraulic circuits. In comparison, industrial manufacturing facilities account for 26% of adoption, while automotive and transportation integrators hold 18%. Defense and aerospace users, although currently representing 8% of total consumption, are the fastest-growing end-user group, supported by an estimated 7.1% CAGR as national security programs upgrade fleets with advanced hydraulic fluid control technologies. Adoption in this segment is expected to surpass 15% by 2032, reflecting increasing specification requirements for performance-critical systems. All remaining end-users, including marine and energy operators, contribute a combined 6% share, driven by high-load and corrosion-intensive applications. Adoption rates across leading industries show measurable increases, with 52% of large manufacturers integrating precision hydraulic assemblies into modernized production lines.

Asia-Pacific accounted for the largest market share at 39% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.3% between 2025 and 2032.

Strong industrial expansion, infrastructure upgrades, and accelerated manufacturing automation contributed to rising Hydraulic Fitting demand across major regions. Europe followed with 27% share in 2024, supported by advanced engineering standards and sustainability-driven hydraulic system upgrades. North America reached 23% adoption, driven by modernization in construction, mining, and energy equipment. South America accounted for 7%, while the Middle East & Africa represented 4%, each demonstrating rising industrial investments, equipment digitization, and broader hydraulic system integration across transportation, logistics, and utilities.

How is rapid industrial modernization transforming demand patterns in this market?

North America held approximately 23% of the global Hydraulic Fitting Market in 2024, supported by strong activity in construction equipment, aerospace systems, industrial machinery, and energy infrastructure. Demand is influenced by digital transformation measures, with 48% of large U.S. manufacturing facilities integrating sensor-enabled hydraulic fittings for real-time monitoring. Regulatory emphasis on equipment safety and leakage control has also elevated compliance-driven upgrades. A notable local player, Parker Hannifin, expanded its advanced fitting production lines in 2024, improving regional supply capability by nearly 18%. Government incentives for domestic manufacturing and reshoring of industrial production continue to strengthen consumption patterns. Regional users exhibit higher adoption of digitally monitored hydraulic assemblies, especially within advanced manufacturing, healthcare automation, and high-value machinery sectors.

Why are stricter sustainability mandates reshaping demand for advanced hydraulic components?

Europe accounted for roughly 27% of the Hydraulic Fitting Market in 2024, with Germany, the UK, France, and Italy as key contributors. The region is heavily influenced by regulatory pressure promoting low-leakage, eco-friendly hydraulic systems and the adoption of recyclable materials. Approximately 41% of European manufacturers now deploy high-efficiency hydraulic assemblies aligned with sustainability guidelines. Technical adoption is accelerating, with Germany leading in automation-driven hydraulic integration and France advancing corrosion-resistant fittings for energy and mobility applications. A prominent European company upgraded its production facilities in 2024, enabling a 21% improvement in machining precision for high-pressure fittings. Consumer behavior is shaped by stringent compliance norms, driving demand for traceable, performance-certified hydraulic components across industries.

What is driving the rapid industrial expansion and rising equipment modernization needs in this market?

Asia-Pacific represented the largest regional market volume in 2024, accounting for nearly 39% of total global consumption. China, India, and Japan are top users due to strong manufacturing ecosystems, large construction activities, and expanding industrial automation. Nearly 52% of new heavy machinery purchased in China now incorporates advanced hydraulic fitting systems, while India’s infrastructure pipeline has increased regional fitting utilization by more than 25% since 2022. Major innovation hubs in Japan and South Korea are promoting lightweight materials and digitalized hydraulic components. A leading regional manufacturer expanded output by 19% in 2024 through automated forging and machining lines. Consumer behavior leans heavily toward mobile equipment, e-commerce-driven logistics machinery, and smart industrial equipment using precision hydraulic assemblies.

How are infrastructure upgrades and energy projects shaping demand for advanced hydraulic systems?

South America accounted for about 7% of the global Hydraulic Fitting Market in 2024, with Brazil and Argentina as primary contributors. Infrastructure development projects, mining activities, and energy sector upgrades continue to strengthen hydraulic component requirements. Around 31% of new heavy equipment purchases in Brazil rely on high-pressure hydraulic fittings, particularly in mining and construction. Government incentives supporting industrial modernization and regional manufacturing expansion enhance market participation. A leading Brazilian equipment supplier integrated precision hydraulic fittings into its 2024 product lineup, improving system durability by 14%. Consumer behavior trends show strong reliance on hydraulic systems for heavy machinery, utilities, and localized industrial operations.

How are oil, gas, and construction projects accelerating modernization of hydraulic systems in this market?

The Middle East & Africa region held approximately 4% of the Hydraulic Fitting Market in 2024, driven by high adoption across oil & gas, construction, and utility sectors. Countries such as the UAE, Saudi Arabia, and South Africa are leading contributors, with large-scale projects requiring advanced leak-resistant hydraulic assemblies. Nearly 37% of regional industrial facilities upgraded to corrosion-resistant fittings in 2024 due to extreme climate environments. Infrastructure investments and trade partnerships promoting industrial localization further support demand. A regional manufacturer introduced automated assembly lines in 2024, increasing output efficiency by 16%. Consumer behavior emphasizes rugged, high-durability hydraulic fittings suited for heavy-duty field operations and oilfield machinery.

China – 28% Market Share

Dominance driven by high production capacity and extensive consumption across manufacturing, construction, and heavy machinery sectors.

United States – 19% Market Share

Strong adoption supported by advanced industrial automation, high equipment replacement cycles, and large-scale deployment in energy and aerospace applications.

The Hydraulic Fitting market is characterized by a moderately fragmented competitive structure, with more than 45 active global and regional manufacturers competing across production precision, material quality, distribution scale, and aftermarket service capabilities. The top five companies collectively account for approximately 38% of the global market share, reflecting a balanced landscape where established industrial brands and emerging technical specialists coexist. Competitive positioning is largely driven by innovation in high-pressure tolerance fittings, lightweight alloy-based connectors, and leak-proof sealing technologies, which are increasingly demanded in sectors such as heavy machinery, oil & gas, and automotive hydraulics.

Many companies are also expanding through strategic initiatives, with more than 20 documented product launches and upgrades between 2022 and 2024, focusing on corrosion-resistant materials and digitally traceable hydraulic connection systems. Partnerships between fitting manufacturers and OEM machinery producers have risen by an estimated 18%, strengthening integrated supply solutions and reducing operational downtime for end-users. Mergers and acquisitions, particularly among mid-sized component suppliers, have increased by around 12%, signaling a trend toward consolidation to achieve technical capabilities and geographical reach. Innovation trends are strongly influenced by automation, with nearly 40% of leading competitors investing in smart manufacturing systems to enhance production consistency and reduce defect rates.

Parker Hannifin Corporation

Eaton Corporation

Swagelok Company

Manuli Hydraulics

Gates Corporation

Nitto Kohki

Stucchi Fittings

Brennan Industries

Danfoss A/S

Ryco Hydraulics

Technology adoption in the Hydraulic Fitting market is accelerating as industries prioritize higher pressure ratings, improved reliability, and longer service life across hydraulic systems. One of the most significant advancements is the widespread shift toward precision-engineered fittings manufactured through CNC machining, which now accounts for nearly 55% of global production due to its ability to maintain tight tolerances and minimize leak risks. Enhanced materials technology is also reshaping the landscape, with stainless steel and alloy-based fittings gaining close to 48% usage in high-pressure applications, while composite materials are gradually expanding their presence due to their corrosion resistance and weight reduction benefits of nearly 30% compared to metal alternatives.

Sealing technologies have seen considerable progress, particularly with elastomeric O-ring enhancements and advanced PTFE-based sealing systems that reduce failure rates by approximately 22% in demanding environments. Quick-connect fittings with push-to-lock designs are emerging rapidly, shortening installation time by up to 40% and supporting faster maintenance cycles in mobile equipment and industrial machinery. Digital traceability through laser-etched codes and RFID tagging has expanded significantly, with nearly 33% of premium hydraulic fittings now integrated with unique identification markers to support real-time inventory tracking, lifecycle assessment, and predictive maintenance.

Additive manufacturing is another transformative trend, enabling the production of customized hydraulic connectors for niche applications where traditional machining would be inefficient. Although adoption remains below 10%, it is growing steadily due to its advantages in producing complex geometries and reducing material waste by almost 60%. Surface treatment technologies, such as nano-ceramic coatings and zinc-nickel plating, are also gaining traction, offering up to 500% improvement in corrosion resistance when compared to traditional galvanization. Collectively, these technological advancements are strengthening system performance, reducing operational downtime, and enabling hydraulic systems to meet increasingly stringent industrial requirements.

In 2023, Manuli Hydraulics launched its “Earth-First” sustainability initiative, focusing on using sustainable raw materials and greener manufacturing processes for hydraulic fittings and hoses globally. (manuli-hydraulics.com)

In April 2024, Manuli Hydraulics introduced a new pressure-washer hose range under the ISOJET label—expanding its industrial portfolio and strengthening its position in water-cleaning and light-duty hydraulic applications.

In 2024, Parker Hannifin Corporation rolled out new low-spill quick-disconnect hydraulic couplers designed for high-reliability applications including data centers and electric vehicle test stands, catering to emerging liquid-cooling and EV infrastructure needs.

In 2023, Eaton Corporation expanded its hydraulic hose-and-fitting offerings by integrating flexible, composite-hose technologies (through a strategic acquisition), enhancing its product lineup for demanding industrial and mobile applications with improved durability and adaptability.

The Hydraulic Fitting Market Report encompasses a comprehensive examination of global hydraulic fittings across all major segmentation vectors—product type, application area, end-user industry, geographic region, and technological innovation. It covers the full spectrum of fitting types including high-pressure fittings, quick-connect/disconnect couplings, corrosion-resistant alloy fittings, composite fittings, and hose-adapter assemblies. For applications, it analyzes sectors such as construction machinery, material handling, agriculture, mining, industrial manufacturing, energy & oil & gas, automotive, aerospace, and data-center fluid management.

Geographically, the report spans all major regions: Asia-Pacific, North America, Europe, South America, and Middle East & Africa—providing insights into regional consumption patterns, production capacity distribution, regulatory and compliance environments, and regional demand drivers. The report also delves into emerging and niche segments such as sensor-enabled smart fittings, environment-friendly and leak-resistant couplings, lightweight composite fittings for mobile and offshore use, and hydraulic solutions optimized for renewable energy, data-center cooling, and EV infrastructure.

In terms of technology focus, the report assesses conventional CNC-machined metal fittings, advanced alloy and composite materials, quick-release / flat-face coupling systems, smart sensor-integrated fittings and hoses, as well as sustainable material and manufacturing initiatives. Industry focus areas include OEM heavy-machinery manufacturers, industrial automation integrators, mining and construction sectors, energy and infrastructure developers, and maintenance services for aftermarket retrofits.

By combining segmentation-wise depth with regional analysis and technological trend mapping, this report aims to provide decision-makers with actionable intelligence to evaluate market opportunities, competitive strategies, product innovation directions, and investment planning across both mainstream and niche hydraulic fitting segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1557.45 Million |

|

Market Revenue in 2032 |

USD 2050.86 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Parker Hannifin Corporation, Eaton Corporation, Swagelok Company, Manuli Hydraulics, Gates Corporation, Nitto Kohki, Stucchi Fittings, Brennan Industries, Danfoss A/S, Ryco Hydraulics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |