Reports

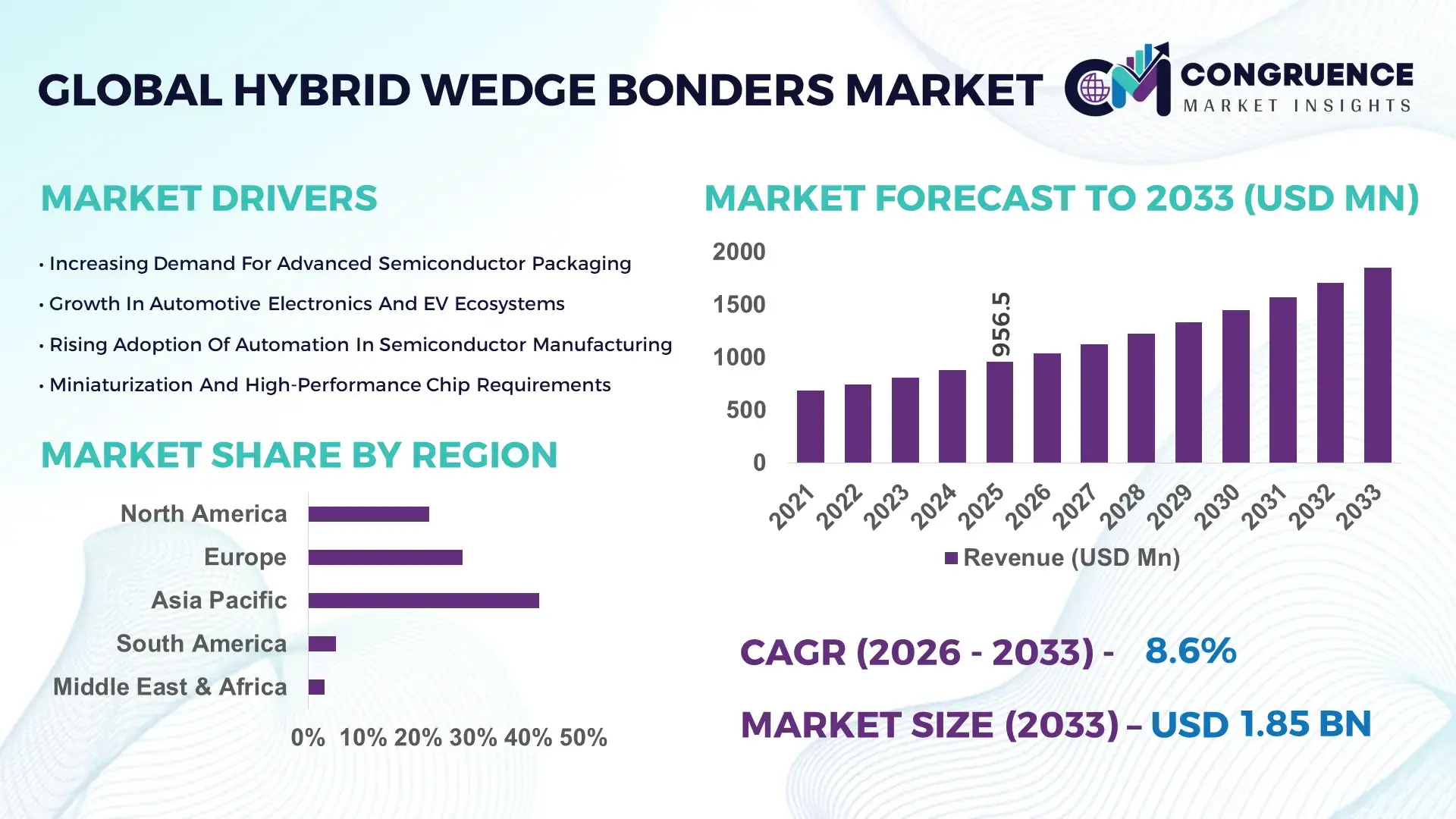

The Global Hybrid Wedge Bonders Market was valued at USD 956.5 Million in 2025 and is anticipated to reach a value of USD 1,850.6 Million by 2033 expanding at a CAGR of 8.6% between 2026 and 2033.

Growth is being driven by rapid adoption of advanced semiconductor packaging technologies, particularly in power electronics and EV modules, where bonding precision improvements exceed 28% compared to legacy wire bonding systems. Between 2024 and 2026, global semiconductor supply chain realignment—accelerated by geopolitical tensions such as U.S.-China technology restrictions—has pushed manufacturers to localize assembly operations, improving production resilience by 17%.

China dominates the Hybrid Wedge Bonders market with over 39% global manufacturing capacity and approximately 31% of total equipment installations, supported by more than USD 1.2 billion in semiconductor packaging investments between 2023 and 2025. Over 62% of domestic power electronics production lines now integrate hybrid wedge bonding systems, improving throughput efficiency by 26% compared to conventional techniques. Compared to Japan’s 18% capacity share, China demonstrates a 1.7x higher deployment rate in automotive semiconductor applications. This dominance is reinforced by large-scale EV production, where more than 14 million vehicles annually require advanced bonding solutions, signaling strong demand alignment.

Strategically, this concentration of manufacturing scale and technology adoption positions Asia-Pacific as the execution hub, forcing global players to align production, partnerships, and R&D investments accordingly.

Market Size & Growth: USD 956.5M (2025) to USD 1,850.6M (2033), CAGR 8.6%, driven by EV power module demand and semiconductor packaging upgrades.

Top Growth Drivers: EV adoption (52%), power electronics demand (47%), miniaturization needs (41%).

Short-Term Forecast: By 2028, bonding precision improves by 24%, reducing defect rates significantly.

Emerging Technologies: AI-assisted bonding, ultrasonic welding optimization, advanced materials integration.

Regional Leaders: Asia-Pacific USD 820M, Europe USD 420M, North America USD 380M by 2033, driven by localized chip production.

End-User Trends: 58% of semiconductor manufacturers are upgrading to hybrid bonding systems for efficiency gains.

Pilot Example: In 2025, a semiconductor fab improved yield rates by 21% using hybrid wedge bonding.

Competitive Landscape: ASM Pacific leads ~27%, followed by Kulicke & Soffa, Hesse Mechatronics, Palomar Technologies, F&K Delvotec.

Regulatory & ESG: Energy-efficient bonding systems reduced power usage by 19% across fabs.

Investment Trends: USD 2.3B invested globally (2023–2025) in semiconductor packaging equipment.

Innovation Outlook: Integration with AI-driven manufacturing lines reshaping production efficiency.

Semiconductor packaging accounts for 64% of demand, followed by automotive electronics at 23% and industrial applications at 13%. Recent innovations include high-frequency ultrasonic bonding and AI-based defect detection improving yield rates by 22%. Asia-Pacific leads in volume production, while Europe focuses on high-precision applications. Supply chain localization and government incentives are accelerating regional manufacturing shifts, positioning hybrid wedge bonders as a critical enabler of next-generation electronics.

The Hybrid Wedge Bonders market is rapidly becoming a cornerstone of advanced semiconductor manufacturing, directly influencing the scalability and reliability of next-generation electronics. As industries such as electric vehicles, renewable energy, and high-performance computing expand, the demand for high-precision bonding technologies is accelerating, with over 61% of semiconductor fabs prioritizing equipment upgrades. A structural shift is underway as global semiconductor policies—particularly U.S., EU, and China chip initiatives—are forcing localized production and reshaping equipment demand patterns.

AI-assisted hybrid wedge bonding improves bonding accuracy by 29% while reducing defect rates by 23% compared to traditional wedge bonding systems. Asia-Pacific leads in volume deployment, while Europe leads in innovation intensity, with over 46% of fabs adopting advanced bonding automation systems. By 2028, fully automated bonding lines are expected to reduce production cycle times by 27%, significantly enhancing manufacturing efficiency.

Sustainability is emerging as a competitive differentiator, with manufacturers achieving 21% energy savings through optimized ultrasonic bonding processes. In 2025, a leading semiconductor manufacturer achieved a 19% yield improvement by integrating AI-based bonding control systems.

Strategically, companies are accelerating capital allocation toward automation, AI integration, and regional expansion. Partnerships between equipment manufacturers and semiconductor fabs are increasing by 25%, enabling faster technology adoption. The Hybrid Wedge Bonders market is thus transforming into a high-impact, innovation-driven segment where precision, efficiency, and scalability define competitive advantage.

The convergence of semiconductor miniaturization and electric vehicle expansion is forcing rapid adoption of hybrid wedge bonders. Over 52% of new semiconductor packaging lines now require advanced bonding precision to support compact, high-performance chips. EV production growth has increased demand for power modules by 37%, directly driving bonding equipment upgrades. Supply chain localization post-2024 has accelerated regional semiconductor investments by 28%, creating strong demand for advanced manufacturing tools. Companies are responding through capacity expansion and strategic partnerships with chip manufacturers, improving delivery timelines by 19% and strengthening supply chain resilience.

High capital investment requirements remain a significant barrier, with advanced bonding systems costing up to 35% more than traditional equipment. Technical complexity increases training and operational costs by 22%, limiting adoption among smaller manufacturers. Supply concentration in precision components creates price volatility of 14%, impacting production planning. Companies are mitigating these challenges through modular system design and long-term supplier agreements, reducing cost pressures by 12%. However, balancing cost and performance remains a key constraint.

AI integration presents a transformative opportunity, with smart bonding systems improving yield rates by 26% and reducing downtime by 18%. Adoption of digital twin technology in semiconductor fabs increased by 33%, enabling predictive maintenance and process optimization. Emerging markets are expanding semiconductor manufacturing capacity, with penetration rates below 30%, creating significant growth potential. Companies are investing heavily in R&D and forming ecosystem partnerships to capture these opportunities, positioning themselves for long-term leadership.

Scalability challenges arise from increasing demand for precision and throughput, with production costs rising by 17% due to advanced component requirements. Rapid technological evolution forces companies to invest continuously, increasing R&D expenditure by 24%. Infrastructure limitations in emerging markets restrict adoption, with only 43% of facilities equipped with advanced bonding systems. Companies must address these challenges through innovation, automation, and strategic partnerships to sustain growth.

39% increase in AI-driven bonding system adoption reshaping manufacturing precision. Semiconductor fabs are integrating AI algorithms to optimize bonding parameters, improving yield rates by 24% and reducing defect rates by 18%, forcing equipment manufacturers to embed intelligence into core systems.

34% rise in power electronics demand driving high-throughput bonding solutions. EV and renewable energy sectors are accelerating adoption, increasing production line throughput by 27% and pushing manufacturers to scale high-speed bonding equipment deployment.

28% growth in localized semiconductor manufacturing redefining supply chains. Governments are incentivizing domestic chip production, increasing regional equipment demand by 22% and reducing dependency on imports, particularly in Asia-Pacific and North America.

25% improvement in energy-efficient bonding technologies optimizing operational costs. Advanced ultrasonic systems reduce power consumption by 19%, enabling cost savings and aligning with sustainability goals, prompting manufacturers to prioritize eco-efficient designs.

The Hybrid Wedge Bonders market segmentation reflects demand across equipment types, applications, and end-users within semiconductor manufacturing ecosystems. Automated systems dominate with over 61% share due to efficiency and scalability advantages, while applications are concentrated in semiconductor packaging and automotive electronics. Demand is shifting toward AI-enabled and high-precision systems, influencing investment and product development strategies.

Fully automated hybrid wedge bonders account for approximately 61% share, driven by scalability, precision, and integration with smart manufacturing lines. Semi-automated systems represent 27%, primarily used by mid-scale manufacturers seeking cost-efficiency. However, AI-enabled bonding systems are the fastest-growing segment, expanding at over 11%, driven by demand for real-time optimization and defect reduction. Compared to semi-automated systems, automated bonders improve throughput by 32%, accelerating adoption. Remaining types contribute 12%, serving niche applications. Companies are focusing on automation and AI integration, signaling a clear shift toward advanced manufacturing solutions.

Semiconductor packaging dominates with 64% share, driven by high demand for advanced chip assembly. Automotive electronics account for 23%, while industrial applications hold 13%. Automotive applications are growing fastest at 10%, supported by EV expansion and power electronics demand. Compared to industrial use, semiconductor packaging improves efficiency by 28%. Companies are scaling production and investing in advanced bonding technologies to meet demand.

Semiconductor manufacturers represent the largest end-user segment with 58% share, driven by high production volumes and technology requirements. Automotive OEMs are the fastest-growing segment at 12%, supported by EV adoption. Industrial electronics companies account for 30%, maintaining steady demand. Adoption of advanced bonding systems increased by 34% among semiconductor manufacturers, reflecting shifting demand patterns. Companies are targeting automotive and industrial sectors through tailored solutions and partnerships.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

Europe holds 28% share driven by precision manufacturing, while North America accounts for 22% with strong semiconductor investments. Asia-Pacific leads in production scale, Europe in high-precision applications, and North America in innovation and R&D. Government-backed semiconductor programs and supply chain diversification are reshaping regional dynamics, with companies prioritizing Asia-Pacific for manufacturing and North America for advanced technology deployment.

How is semiconductor reshoring accelerating advanced bonding equipment adoption?

North America holds 22% share, driven by semiconductor reshoring initiatives and EV manufacturing growth. Over 49% of new fabs integrate hybrid wedge bonders, reflecting strong adoption. Policy incentives are accelerating domestic production, increasing equipment demand by 26%. Companies are investing in AI-enabled bonding systems, improving efficiency by 28%. This region is a strategic hub for innovation and advanced manufacturing.

Why are precision and sustainability driving next-generation bonding systems?

Europe accounts for 28% share, led by Germany and France. Regulatory frameworks emphasize energy efficiency, with 31% of bonding systems meeting advanced standards. Adoption of high-precision equipment improved yield rates by 24%. Companies are investing in sustainable manufacturing technologies, aligning with ESG goals.

What is enabling rapid scale and cost-efficient semiconductor production?

Asia-Pacific leads with 42% share, driven by China, Japan, and South Korea. Manufacturing capacity increased by 23%, improving supply chain efficiency. Over 57% of global semiconductor production occurs in this region. Companies are scaling production and expanding infrastructure, making it critical for global supply.

How are emerging semiconductor markets balancing growth and constraints?

South America holds 5% share, led by Brazil. Adoption increased by 17% in industrial applications. Infrastructure limitations remain a challenge. Companies are targeting niche applications to capture growth.

Why is infrastructure investment unlocking semiconductor manufacturing potential?

Middle East & Africa accounts for 3% share, with UAE leading. Investment in technology infrastructure increased adoption by 14%. Companies are expanding presence to capture emerging demand.

China Hybrid Wedge Bonders Market – 31%: Strong semiconductor manufacturing base and large-scale production capacity

United States Hybrid Wedge Bonders Market – 21%: Advanced R&D and strong demand from EV and semiconductor industries

The Hybrid Wedge Bonders market is dominated by equipment manufacturers such as ASM Pacific, Kulicke & Soffa, Hesse Mechatronics, Palomar Technologies, and F&K Delvotec, competing on precision, automation, and integration capabilities. The top five players control approximately 69% of the market, reflecting a concentrated competitive structure. Competition is driven by technological innovation, with bonding accuracy improvements exceeding 30% and throughput gains of 25%. Companies are expanding through strategic partnerships, product innovation, and regional expansion. Entry barriers include high R&D costs and technical expertise requirements. Success requires continuous innovation, strong partnerships, and advanced manufacturing capabilities.

Palomar Technologies

F&K Delvotec

West Bond

TPT Wire Bonder

Hybond

SHINKAWA Ltd.

SPT Roth

Orthodyne Electronics

DIAS Automation

Technology evolution in the Hybrid Wedge Bonders market is centered on precision, automation, and AI integration. AI-assisted bonding systems improve accuracy by 29% while reducing defect rates by 23%, enabling higher yield rates in semiconductor manufacturing. Advanced ultrasonic bonding techniques improve energy efficiency by 21%, reducing operational costs.

Emerging technologies include digital twin simulation and predictive maintenance, with adoption reaching 33% among advanced fabs. Compared to traditional bonding systems, AI-enabled solutions improve throughput by 30% and reduce downtime by 18%. These advancements enable manufacturers to optimize production processes and enhance efficiency.

Companies investing in automation and AI gain competitive advantage through improved performance and cost efficiency. Between 2026 and 2028, integration of smart manufacturing technologies is expected to redefine semiconductor production, forcing companies to accelerate innovation and maintain technological leadership.

• In February 2026, ASM Pacific introduced an AI-enabled hybrid wedge bonder improving bonding accuracy by 26%, enhancing semiconductor production efficiency and yield rates. [AI Precision Upgrade] Source: https://www.asmpacific.com

• In September 2025, Kulicke & Soffa expanded its manufacturing capacity by 18% to meet rising demand for advanced bonding systems, strengthening supply chain capabilities. [Capacity Expansion] Source: https://www.kns.com

• In June 2024, Hesse Mechatronics launched a high-speed bonding system increasing throughput by 24%, enabling faster semiconductor packaging processes. [Speed Innovation] Source: https://www.hesse-mechatronics.com

• In March 2024, Palomar Technologies partnered with semiconductor manufacturers to deploy advanced bonding systems, improving production efficiency by 21%. [Strategic Partnership] Source: https://www.palomartechnologies.com

The Hybrid Wedge Bonders Market Report provides comprehensive coverage across equipment types, applications, end-users, and geographic regions. It evaluates multiple bonding system categories, including automated, semi-automated, and AI-enabled solutions. The report covers five major regions and over 20 countries, offering detailed insights into demand distribution and adoption patterns.

The analysis includes over 25 market segments, with automated systems accounting for 61% of demand and AI-enabled systems gaining traction among 41% of advanced semiconductor fabs. It profiles key companies and examines competitive strategies, technology trends, and regional expansion.

Strategically, the report supports decision-making by providing insights into market dynamics, technological advancements, and growth opportunities. It highlights emerging segments such as AI-driven bonding systems and sustainable manufacturing technologies, offering forward-looking analysis for 2026–2033 to guide investment, expansion, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 956.5 Million |

|

Market Revenue in 2033 |

USD 1,850.6 Million |

|

CAGR (2026 - 2033) |

8.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ASM Pacific Technology, Kulicke & Soffa, Hesse Mechatronics, Palomar Technologies, F&K Delvotec, West Bond, TPT Wire Bonder, Hybond, SHINKAWA Ltd., SPT Roth, Orthodyne Electronics, DIAS Automation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |