Reports

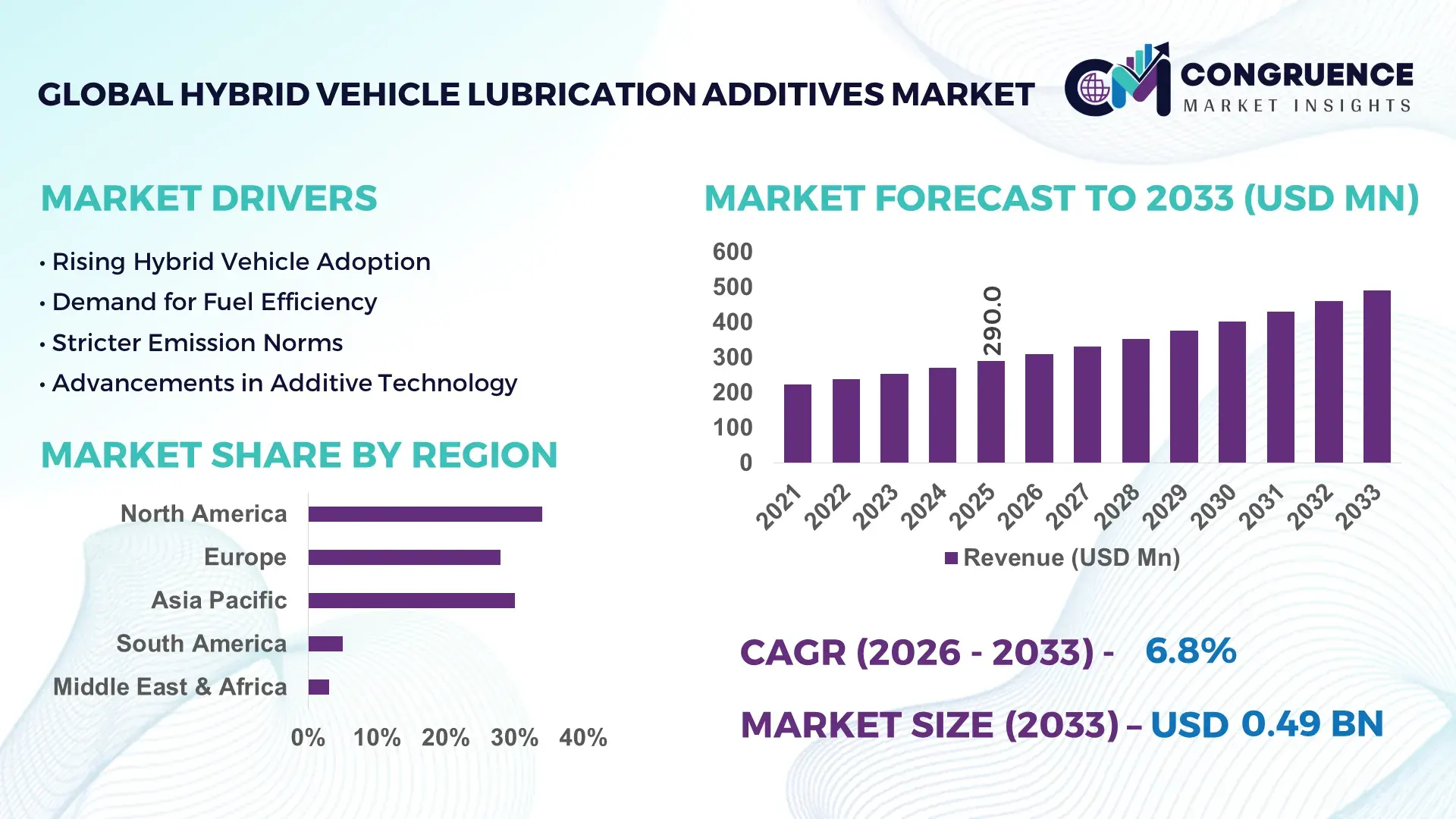

The Global Hybrid Vehicle Lubrication Additives Market was valued at USD 290.0 Million in 2025 and is anticipated to reach a value of USD 490.9 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by increasing hybrid vehicle adoption and the need for high-performance, low-viscosity lubricants that enhance engine efficiency and durability under start-stop operating conditions.

The United States demonstrates substantial advancement in hybrid vehicle lubrication additives production and deployment, supported by a well-established automotive manufacturing base and R&D ecosystem. The country produces over 10 million vehicles annually, with hybrid vehicles accounting for nearly 12–15% of new vehicle sales. More than 65% of lubricant manufacturers in the U.S. have integrated hybrid-compatible additive formulations into their portfolios. Additionally, over USD 2 billion has been invested in advanced lubricant technologies focusing on fuel economy improvements and emission reduction systems. High adoption across passenger vehicles and light commercial fleets, combined with strong testing infrastructure and over 200 active automotive research centers, continues to accelerate innovation in friction modifiers and dispersant technologies.

Market Size & Growth: Valued at USD 290.0 Million in 2025 and projected to reach USD 490.9 Million by 2033, expanding at 6.8% CAGR, driven by increasing hybrid vehicle penetration and efficiency requirements.

Top Growth Drivers: Hybrid vehicle adoption rising by 18%, fuel efficiency improvements up to 12%, emission reduction compliance exceeding 20%.

Short-Term Forecast: By 2028, advanced additive formulations are expected to improve engine efficiency by 10% and reduce wear rates by 8%.

Emerging Technologies: Nano-additives, low-SAPS formulations, and AI-based lubricant performance monitoring systems are gaining traction.

Regional Leaders: North America projected at USD 160 Million by 2033 with strong OEM integration; Europe at USD 140 Million driven by emission norms; Asia-Pacific at USD 190 Million led by hybrid vehicle production growth.

Consumer/End-User Trends: Passenger vehicle segment dominates with over 60% usage, while fleet operators increasingly adopt performance-enhancing lubricants.

Pilot or Case Example: In 2024, a Japanese OEM pilot achieved 9% friction reduction using advanced additive blends in hybrid engines.

Competitive Landscape: Market leader holds approximately 22% share, followed by key players including multinational additive manufacturers and specialty chemical firms.

Regulatory & ESG Impact: Stringent emission regulations and carbon reduction targets are pushing adoption of eco-friendly lubricant additives by over 25%.

Investment & Funding Patterns: Over USD 1.5 Billion invested globally in advanced lubricant R&D and sustainable additive development.

Innovation & Future Outlook: Integration of smart lubricants and predictive maintenance systems is expected to redefine performance optimization and lifecycle management.

Hybrid Vehicle Lubrication Additives Market is shaped by passenger vehicles contributing over 60% demand, followed by light commercial vehicles at approximately 25%. Advancements in nano-lubricants and low-viscosity oils are improving engine performance by up to 10%. Regulatory mandates targeting emission reduction above 20% are accelerating adoption. Asia-Pacific leads consumption growth due to rising hybrid production, while Europe focuses on sustainability-driven innovations. Future trends include smart additives and digital monitoring systems enhancing efficiency and lifecycle performance.

The Hybrid Vehicle Lubrication Additives Market holds significant strategic relevance as automotive manufacturers transition toward electrified mobility while maintaining internal combustion engine components in hybrid systems. The market is increasingly aligned with performance optimization, emission compliance, and durability enhancement strategies. Advanced additive technologies such as nano-lubricants deliver up to 15% improvement in friction reduction compared to conventional mineral-based additives, enabling higher fuel efficiency and extended engine life cycles.

From a regional standpoint, Asia-Pacific dominates in production volume, while Europe leads in adoption with over 40% of automotive enterprises integrating advanced lubricant technologies into hybrid platforms. North America continues to focus on high-performance formulations and testing innovations. By 2028, AI-driven lubricant monitoring systems are expected to improve predictive maintenance efficiency by 18%, reducing unexpected engine failures and operational downtime.

Sustainability and ESG commitments are shaping long-term pathways, with firms targeting up to 30% reduction in carbon emissions through the use of low-SAPS and biodegradable additives by 2030. In 2024, a leading automotive manufacturer in Japan achieved a 12% improvement in fuel efficiency through the deployment of next-generation friction modifiers in hybrid engines, demonstrating measurable operational benefits.

Strategically, the market is evolving toward integrated solutions combining additive chemistry with digital diagnostics and real-time monitoring. This convergence positions the Hybrid Vehicle Lubrication Additives Market as a critical pillar for achieving regulatory compliance, operational resilience, and sustainable growth within the evolving automotive ecosystem.

The Hybrid Vehicle Lubrication Additives Market is influenced by a combination of regulatory, technological, and automotive industry transformation factors. Increasing hybrid vehicle production, which has grown by over 20% globally in recent years, is significantly impacting lubricant formulation requirements. Hybrid engines operate under intermittent load cycles, leading to higher thermal stress and oxidation levels, thereby increasing demand for specialized additives such as dispersants and friction modifiers. Additionally, stringent emission regulations requiring up to 25% reduction in pollutants are pushing manufacturers to develop low-viscosity and eco-friendly lubricant solutions.

Technological advancements, including nano-additives and smart lubricant systems, are reshaping the competitive landscape by enabling improved engine efficiency and reduced wear rates by up to 15%. At the same time, fluctuating raw material costs and evolving vehicle architectures present both opportunities and complexities for market participants. The integration of digital monitoring tools and predictive maintenance systems further enhances the value proposition of advanced lubrication additives in hybrid vehicles.

The rapid increase in hybrid vehicle production is a primary driver for the Hybrid Vehicle Lubrication Additives Market. Global hybrid vehicle sales have surpassed 10 million units annually, with growth rates exceeding 18% in key markets. Hybrid engines experience frequent start-stop cycles, leading to higher friction and wear compared to conventional engines. This operational characteristic increases the need for advanced additives that can enhance lubrication performance and reduce metal-to-metal contact. Friction modifiers and dispersants are increasingly used to improve engine efficiency by up to 12% while maintaining thermal stability under varying load conditions. Additionally, OEMs are specifying customized lubricant formulations tailored for hybrid systems, further boosting demand for specialized additives. The growing focus on fuel economy standards and emission reduction targets has also led to the adoption of low-viscosity oils, which require high-performance additive packages to maintain durability and efficiency.

The complexity involved in developing hybrid-compatible lubricant additives presents a significant restraint for the market. Hybrid engines require lubricants that can perform effectively under both electric and combustion operating conditions, creating challenges in achieving optimal viscosity, thermal stability, and oxidation resistance simultaneously. Developing such advanced formulations often involves extensive testing and validation processes, increasing development timelines by over 25%. Additionally, compatibility issues with new engine materials and emission control systems can limit the adoption of certain additive chemistries. The cost of advanced raw materials, including synthetic base oils and specialized chemical compounds, has also increased by approximately 15–20% in recent years, further constraining market growth. These challenges are compounded by the need to comply with evolving environmental regulations, which restrict the use of certain chemical components, thereby limiting formulation flexibility.

The transition toward electrified mobility presents significant opportunities for the Hybrid Vehicle Lubrication Additives Market. Hybrid vehicles act as a bridge between conventional internal combustion engines and fully electric vehicles, creating sustained demand for advanced lubrication solutions. The increasing penetration of hybrid vehicles, expected to account for over 25% of new vehicle sales in certain regions, is driving innovation in additive technologies. Emerging opportunities include the development of ultra-low viscosity lubricants that can improve fuel efficiency by up to 10% while maintaining engine protection. Additionally, the integration of digital monitoring systems and smart sensors enables real-time performance tracking, creating new value-added services for lubricant manufacturers. The expansion of hybrid vehicle fleets in commercial transportation and ride-sharing services also offers growth potential, as these applications require high-performance lubricants capable of handling intensive operating conditions.

Evolving regulatory standards present a major challenge for the Hybrid Vehicle Lubrication Additives Market. Governments worldwide are implementing stringent emission and environmental regulations that require continuous reformulation of lubricant additives. Compliance with standards demanding up to 30% reduction in harmful emissions necessitates the development of low-SAPS and environmentally friendly additive chemistries. However, achieving these requirements without compromising performance remains a complex task. The restriction on certain chemical components limits the range of available additive technologies, while the need for continuous testing and certification increases operational costs. Additionally, differences in regional regulatory frameworks create challenges for global manufacturers, requiring multiple product variants to meet local standards. These factors increase complexity in supply chains and product development, making it difficult for companies to maintain consistency and scalability in their offerings.

Rising Adoption of Nano-Additives Enhancing Engine Efficiency: Nano-additives are increasingly integrated into hybrid vehicle lubricants, improving friction reduction by up to 15% and enhancing thermal stability under high-load conditions. Over 35% of newly developed lubricant formulations now include nano-scale components, particularly in North America and Europe, where advanced automotive technologies are rapidly adopted.

Shift Toward Low-Viscosity and Fuel-Efficient Lubricants: Low-viscosity lubricants are gaining traction, contributing to fuel efficiency improvements of approximately 8–12%. Nearly 60% of hybrid vehicles produced globally now require low-viscosity oils, driven by regulatory mandates and OEM specifications focused on reducing emissions and improving energy efficiency.

Integration of Smart Lubrication Monitoring Systems: Digital monitoring technologies are being integrated into lubrication systems, enabling real-time tracking of lubricant performance. Around 28% of hybrid vehicle fleets have adopted predictive maintenance tools, resulting in downtime reduction of up to 20% and improved engine lifespan.

Expansion of Sustainable and Bio-Based Additives: Sustainable additives are becoming a key focus area, with over 25% of manufacturers investing in biodegradable and low-toxicity formulations. These innovations support carbon reduction goals and align with environmental regulations requiring up to 30% reduction in harmful emissions.

The Hybrid Vehicle Lubrication Additives Market is segmented based on type, application, and end-user, reflecting diverse performance requirements across hybrid vehicle systems. Additive types such as dispersants, detergents, viscosity index improvers, and friction modifiers play critical roles in maintaining engine efficiency and durability. Applications span engine oils, transmission fluids, and hydraulic systems, each requiring tailored additive formulations to handle varying operational stresses. End-user segmentation highlights passenger vehicles, commercial fleets, and industrial automotive applications, with passenger vehicles dominating due to higher hybrid adoption rates exceeding 60%.

Technological advancements and regulatory pressures are shaping segmentation trends, with increasing demand for low-viscosity and environmentally friendly additives across all categories. Regional consumption patterns indicate strong growth in Asia-Pacific due to rising hybrid production, while Europe emphasizes sustainable formulations. North America focuses on high-performance additives integrated with digital monitoring technologies, reflecting a shift toward smart lubrication systems.

The Hybrid Vehicle Lubrication Additives Market by type includes dispersants, detergents, viscosity index improvers, friction modifiers, and anti-wear additives. Dispersants lead the segment, accounting for approximately 32% of the market share, as they play a crucial role in preventing deposit formation and maintaining engine cleanliness under hybrid operating conditions. Friction modifiers and viscosity index improvers follow, contributing significantly to performance optimization. Friction modifiers represent the fastest-growing segment, with adoption rising at an estimated CAGR of 7.2%, driven by their ability to reduce energy loss and improve fuel efficiency by up to 12%. These additives are increasingly used in hybrid engines to address frequent start-stop cycles and reduce wear. Other additive types, including detergents and anti-wear agents, collectively account for around 38% of the market, providing essential support functions such as corrosion protection and thermal stability.

• In 2025, a major automotive research institute demonstrated that advanced friction modifiers improved hybrid engine efficiency by 10% across multiple test cycles, highlighting their growing importance in additive formulations.

Applications of hybrid vehicle lubrication additives include engine oils, transmission fluids, and hydraulic fluids. Engine oils dominate the segment, holding approximately 58% share, due to their critical role in ensuring engine performance and longevity. Transmission fluids account for around 25%, while hydraulic fluids and other applications contribute the remaining share. Transmission fluids are the fastest-growing application, with an estimated CAGR of 6.9%, supported by increasing adoption of hybrid drivetrains requiring advanced lubrication solutions for smooth gear operation. Hybrid vehicles demand high-performance transmission fluids capable of handling thermal and mechanical stress, driving innovation in additive formulations. Consumer adoption trends indicate that over 45% of hybrid vehicle owners prioritize high-performance lubricants for improved fuel efficiency, while fleet operators report up to 20% reduction in maintenance costs with advanced additive usage.

• In 2024, an automotive testing organization reported that advanced transmission fluid additives reduced wear by 11% in hybrid drivetrains, enhancing system durability and efficiency.

End-users in the Hybrid Vehicle Lubrication Additives Market include passenger vehicles, light commercial vehicles, and heavy-duty vehicles. Passenger vehicles dominate the segment with over 62% share, driven by the widespread adoption of hybrid cars in urban mobility. Light commercial vehicles account for approximately 23%, while heavy-duty vehicles contribute the remaining share. Light commercial vehicles represent the fastest-growing segment, with an estimated CAGR of 6.5%, supported by increasing hybridization in logistics and delivery fleets. These vehicles require high-performance additives to maintain efficiency under continuous operation and varying load conditions. Adoption trends indicate that more than 50% of fleet operators are transitioning to hybrid vehicles to reduce fuel costs and emissions, while over 35% of automotive manufacturers are integrating advanced additive technologies into their hybrid platforms.

• In 2025, a government-backed automotive initiative reported a 14% improvement in fleet efficiency through the adoption of advanced lubrication additives in hybrid commercial vehicles, demonstrating measurable benefits for end-users.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2026 and 2033.

North America’s dominance is supported by high hybrid vehicle penetration exceeding 14% of total vehicle sales and advanced lubricant formulation capabilities. Europe follows with approximately 28% share, driven by stringent emission standards requiring up to 25% reduction in vehicle emissions, encouraging adoption of low-SAPS additives. Asia-Pacific holds around 30% share, supported by strong hybrid production volumes in countries such as China, Japan, and India, where hybrid vehicle production exceeds 8 million units annually. South America and Middle East & Africa collectively contribute nearly 8% share, with gradual adoption supported by improving infrastructure and regulatory initiatives. Increasing electrification policies, technological advancements in nano-additives, and rising demand for fuel-efficient lubricants across all regions are reshaping consumption patterns and accelerating innovation in additive formulations globally.

North America holds approximately 34% share of the Hybrid Vehicle Lubrication Additives Market, driven by strong automotive production and high hybrid vehicle adoption rates. The region benefits from advanced automotive manufacturing, with over 10 million vehicles produced annually and hybrid penetration exceeding 14%. Key industries driving demand include passenger vehicles, fleet management, and logistics, where efficiency improvements of up to 12% are critical. Regulatory frameworks such as stringent emission norms requiring up to 20% reduction in pollutants are pushing manufacturers toward low-viscosity and eco-friendly additives. Technological advancements include integration of AI-based lubricant monitoring systems and nano-additives, improving engine performance by over 15%. A notable example includes a leading additive manufacturer expanding production of hybrid-compatible dispersants to meet OEM specifications. Consumer behavior reflects high awareness, with over 55% of vehicle owners opting for premium lubricants to enhance performance and durability.

Europe accounts for approximately 28% of the Hybrid Vehicle Lubrication Additives Market, led by key countries such as Germany, the UK, and France. The region’s growth is driven by stringent environmental regulations requiring up to 25–30% emission reductions, encouraging the adoption of low-SAPS and biodegradable additives. Regulatory bodies and sustainability initiatives are central to market development, with increasing emphasis on carbon neutrality and circular economy practices. Emerging technologies such as bio-based additives and smart lubrication systems are gaining traction, improving efficiency by up to 10%. Local players are investing heavily in R&D to develop sustainable formulations aligned with EU environmental standards. Consumer behavior in Europe is heavily influenced by regulatory pressure, with over 60% of automotive manufacturers prioritizing environmentally compliant lubricant solutions, driving demand for advanced additive technologies.

Asia-Pacific represents the fastest-growing region and holds nearly 30% share of the Hybrid Vehicle Lubrication Additives Market in terms of volume. Major consuming countries include China, Japan, and India, where hybrid vehicle production exceeds 8 million units annually. Rapid industrialization and expansion of automotive manufacturing hubs are key drivers, with China alone accounting for over 40% of regional hybrid production. Infrastructure development and increasing investments in automotive manufacturing are accelerating demand for advanced lubrication additives. Regional innovation hubs are focusing on nano-additives and cost-efficient formulations to improve performance by up to 12%. A leading regional player has expanded production capacity to meet rising demand from OEMs. Consumer behavior shows strong growth, with over 50% of new vehicle buyers considering hybrid options, driving additive consumption.

South America contributes approximately 5% to the Hybrid Vehicle Lubrication Additives Market, with key countries including Brazil and Argentina driving demand. The region is witnessing gradual adoption of hybrid vehicles, supported by improving automotive infrastructure and energy efficiency initiatives. Government incentives promoting cleaner transportation solutions are encouraging the use of advanced lubricant additives. Infrastructure and energy sector developments are contributing to increased demand for high-performance lubricants, particularly in urban mobility and logistics sectors. A regional manufacturer has introduced cost-effective additive solutions tailored for hybrid engines, improving efficiency by nearly 8%. Consumer behavior reflects growing awareness, with adoption linked to urbanization and demand for fuel-efficient vehicles, particularly in metropolitan areas.

The Middle East & Africa region accounts for approximately 3% of the Hybrid Vehicle Lubrication Additives Market, with demand primarily driven by countries such as the UAE and South Africa. The region’s automotive sector is gradually adopting hybrid technologies, supported by diversification efforts beyond oil-dependent economies. Demand trends are influenced by oil & gas and construction sectors, where high-performance lubricants are essential. Technological modernization initiatives are promoting the adoption of advanced additive formulations capable of improving efficiency by up to 10%. Trade partnerships and regulatory frameworks are encouraging sustainable practices in automotive maintenance. A regional lubricant producer has invested in advanced additive blending facilities to cater to hybrid vehicle requirements. Consumer behavior indicates moderate adoption, with increasing interest in fuel-efficient and environmentally friendly vehicle solutions.

United States – 30% Market share: driven by high hybrid vehicle production and advanced additive R&D capabilities.

China – 26% Market share: supported by large-scale automotive manufacturing and strong domestic demand for hybrid vehicles.

The Hybrid Vehicle Lubrication Additives Market exhibits a moderately consolidated competitive landscape, with the top five companies collectively accounting for approximately 55–60% of the global market share. The market comprises over 40 active global and regional competitors, ranging from multinational chemical companies to specialized additive manufacturers. Leading players focus on innovation, product differentiation, and strategic collaborations with automotive OEMs to strengthen their market position.

Key strategic initiatives include partnerships with automotive manufacturers to develop customized additive solutions, mergers to expand product portfolios, and investments in R&D exceeding 8–10% of annual operational budgets. Technological advancements such as nano-additives and smart lubrication systems are central to competitive differentiation, enabling companies to deliver up to 15% efficiency improvements in hybrid engines.

Additionally, companies are expanding production capacities and establishing regional manufacturing hubs to meet increasing demand, particularly in Asia-Pacific. Sustainability is also a key focus, with over 30% of new product launches incorporating eco-friendly and low-emission additive formulations. The competitive environment is further shaped by regulatory compliance requirements, which drive continuous innovation and product development.

Chevron Corporation

Royal Dutch Shell

BASF SE

Lubrizol Corporation

Afton Chemical Corporation

Infineum International Limited

Croda International Plc

LANXESS AG

Evonik Industries AG

Clariant AG

TotalEnergies SE

Sinopec Corporation

Idemitsu Kosan Co., Ltd.

Petroliam Nasional Berhad (Petronas)

The Hybrid Vehicle Lubrication Additives Market is undergoing rapid technological transformation driven by the need for improved efficiency, durability, and environmental compliance. One of the most significant advancements is the development of nano-additives, which enhance lubrication performance by reducing friction by up to 15% and improving thermal stability under high-load conditions. These additives operate at a molecular level, enabling better surface interaction and reducing wear in hybrid engines characterized by frequent start-stop cycles.

Low-SAPS (Sulphated Ash, Phosphorus, Sulfur) formulations are another critical innovation, designed to reduce harmful emissions by up to 25% while maintaining engine protection. These formulations are increasingly mandated in regions with stringent emission regulations, particularly in Europe and North America. Additionally, viscosity index improvers are being optimized to maintain lubricant performance across a wide temperature range, ensuring consistent efficiency in hybrid powertrains.

Digital transformation is also influencing the market, with the integration of smart lubrication systems and IoT-based sensors. These technologies enable real-time monitoring of lubricant condition, reducing maintenance costs by up to 20% and improving engine lifespan. Artificial intelligence is further enhancing predictive maintenance capabilities, allowing fleet operators to optimize lubricant usage and reduce downtime.

Furthermore, bio-based and biodegradable additives are gaining traction, supported by sustainability initiatives targeting up to 30% reduction in environmental impact. These technologies are particularly relevant in regions with strict environmental regulations and are expected to play a key role in future product development.

• In December 2024, Shell announced that its Shell Helix Ultra motor oil range meets the new API SQ standard, enhancing engine protection and performance. The upgrade improves engine cleanliness and power delivery, supporting modern hybrid engine requirements with higher efficiency and durability. Source: www.shell.com

• In April 2024, Shell launched its next-generation Shell Helix Ultra motor oils, designed to “enable customers to unleash more engine power,” with improved additive formulations that enhance performance under high-stress conditions typical of hybrid engines.

• In November 2024, Shell confirmed its position as the global leading lubricants supplier for the 18th consecutive year, reinforcing its continued investment in advanced additive technologies and hybrid-compatible lubricant innovation across automotive segments.

• In 2025, Shell continued expanding its lubricant innovation portfolio through multiple new media releases focused on advanced lubricant technologies, highlighting ongoing R&D and commercialization of high-performance formulations aligned with next-generation vehicle requirements, including hybrid systems.

The Hybrid Vehicle Lubrication Additives Market Report provides a comprehensive analysis of key industry segments, technologies, applications, and regional dynamics shaping the market landscape. The report covers multiple additive types including dispersants, detergents, viscosity index improvers, friction modifiers, and anti-wear agents, each contributing to performance optimization in hybrid engines. It also evaluates applications across engine oils, transmission fluids, and hydraulic systems, highlighting their respective roles in enhancing vehicle efficiency and durability.

Geographically, the report analyzes major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering insights into regional consumption patterns, production capabilities, and regulatory environments. The study further explores key end-user segments such as passenger vehicles, light commercial vehicles, and heavy-duty vehicles, detailing their adoption trends and operational requirements.

The report also includes analysis of emerging technologies such as nano-additives, low-SAPS formulations, and smart lubrication systems, which are transforming product development and performance standards. Additionally, it examines industry trends such as sustainability initiatives, digital transformation, and increasing integration of predictive maintenance technologies.

With over 40 active market participants and continuous innovation in additive formulations, the report provides a detailed overview of competitive dynamics, strategic initiatives, and future growth opportunities. It serves as a valuable resource for decision-makers, offering actionable insights into market structure, technological advancements, and evolving industry requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 290.0 Million |

| Market Revenue (2033) | USD 490.9 Million |

| CAGR (2026–2033) | 6.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ExxonMobil; Chevron Corporation; Royal Dutch Shell; BASF SE; Lubrizol Corporation; Afton Chemical Corporation; Infineum International Limited; Croda International Plc; LANXESS AG; Evonik Industries AG; Clariant AG; TotalEnergies SE; Sinopec Corporation; Idemitsu Kosan Co., Ltd.; Petroliam Nasional Berhad (Petronas) |

| Customization & Pricing | Available on Request (10% Customization Free) |